| Review | Open Access |

|---|

Making Road to Makkah Accessible for Pakistanis: A Proposed Model from the Experience of Indonesia and Malaysia |

|

|---|

![]() Hafiz Arif Jamal* and Saqib Sharif

Hafiz Arif Jamal* and Saqib Sharif

Institute of Business Administration, Karachi, Pakistan

Hajj is one of the five pillars of Islam and is mandatory for every Muslim adult. For the management of Hajj funds, several countries including Malaysia, Indonesia, Nigeria, and Maldives have established separate legal entities to provide services to pilgrims and administer their Hajj deposits, simultaneously benefiting from them in the shape of halal returns. This paper aims to evaluate the Hajj fund management of two countries, namely Indonesia and Malaysia, in comparison to the current structure of the management of Hajj funds in Pakistan. The study proposes an efficient model for Pakistan’s Hajj fund management based on the best practices of Indonesia and Malaysia. It argues the setting up of an independent entity, whereby individuals may start saving at an early age by entering into a financial contract. Thus, efficient utilization of Hajj funds can be ensured, providing optimum facilitation to the potential pilgrims of Pakistan at a reasonable cost.

1. INTRODUCTION

Hajj is the annual pilgrimage to Mecca and Mina. It is binding for Muslims who have the financial and physical means to undertake this ritual journey at least once in their lifespan (Sahih Muslim). Hajj requires proper planning and execution. It not only boosts the moral character of the pilgrims, but it also has an impact on various phases of their socioeconomic well-being. Muslims in Pakistan save money via traditional means for years to perform their holy journey to Mecca, since it is the desire of every Muslim to perform Hajj in order to complete the list of the acts of worship preached by Islam (Muneeza et al., 2018). Globally, Muslim communities set aside funds for Hajj in formal and informal ways with a cautious approach to avoid prohibited earnings, especially from interest- or riba-based sources.

The Hajj is a five-day event. The pilgrims visit certain holy sites, complete a sequence of rituals, and offer their prayers. Hajj is the evidence of submission to Allah Almighty. The accomplishment of Hajj has not only religious and social significance but it also entails a significant financial commitment, as it poses considerable financial costs to every Muslim who wishes to perform this journey (Baig, 2016). Each year around 2-3 million people across the globe perform Hajj. To plan for this holy pilgrimage, every Muslim desires to invest in permissible financial avenues.

Since 2023, after the relaxation in COVID-19 restrictions, the Hajj event has attracted the participation of roughly 1.8 million people from across the globe, while 180,000 have made this journey from Pakistan. The government of KSA sets the Hajj quota, which allows 0.1% of the Muslim population of the world (at the rate of one thousand pilgrims per one million inhabitants from each country) to perform Hajj every year, in conformity with the decision made in the gathering of the Foreign Ministers of the Organization of Islamic Conference (OIC) in the year 1987. To perform Hajj, applicants complete the application form authorized by the licensed agency. In Pakistan, Ministry of Religious Affairs and Interfaith Harmony (MoRA) is authorized is to make suitable arrangements for the holy journey. According to the statistics, Hajj expenses in Pakistan for 2023 were around Rs. 1,175,000. This is 422% higher than the year 2015, when the expenses were Rs. 270,181 (MoRA Hajj Publications 2015-2023). The applications from Pakistan have always been in a large number and a lottery method is applied to shortlist the aspirant Hajj applicants’ selection.

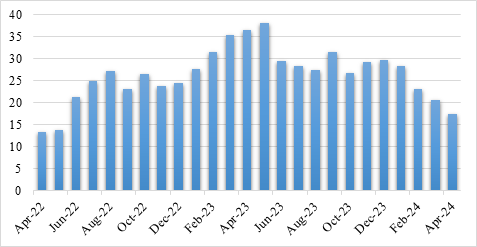

Due to the hike in global inflation following COVID-19, Russia-Ukraine war, domestic inflationary pressure, devaluation of the currency, and exchange rate volatility, performing Hajj has become an expensive affair, as shown in the Figure 1. In Pakistan, the domestic Consumer Price Index (CPI) inflation rate during April 2022-2024 has been alarming; indeed, we can witness a massive hike in the inflation rate from 13.4% in March 2022 to a peak of 38% in May 2023. The rate of inflation is still in double figures and compromises the living standards of many individuals and households. Nearly 40% of the total population cannot afford the Hajj due to its high cost and the prevailing poverty. According to the definition of poverty, households earning less than $3.65 a day are considered poor; thus, 39.4% of the population lives below the poverty line in Pakistan (Rana, 2023).

Figure 1

Rate of Inflation in Pakistan

Note. Source: SBP Publications - Inflation Monitor 2022-2024

In the previous regime of Pakistan Tehreek-e-Insaf (2018-2022), it was decided by the then government to abolish the entire subsidy on Hajj. The Minister of Religious Affairs stated that Hajj is only due on wealthy and affluent citizens, therefore, they abolished the entire subsidy on Hajj cost, thus causing a sharp increase in its cost. Recently, due to high inflation and devaluation of the Pakistani rupee, Hajj cost has gone out of the reach of numerous Pakistanis. Consequently, a significant portion of the Hajj quota remained unutilized for the years 2022 and 2023 (MoRA Hajj Publication 2022/2023, page # 19). This was a very rare occurrence in the history of Pakistan. In this scenario, the setting up of a Shariah-compliant Hajj savings system or a Hajj fund management institution is needed, so that individuals can start allocating small sums for this obligatory duty at an early age with the aim to avail the facility of subsidized Hajj cost through Halal returns on their investments.

To subsidize the Hajj cost and to identify the various avenues for creating and investing Hajj funds, making Hajj more affordable and economical to every class of the society, an alternative and more efficient model for funds management in Pakistan is proposed in this project. The author has evaluated the world’s leading models well-known for providing exemplary Hajj services and managing funds efficiently under the Shariah jurisdiction, that is, Indonesian and Malaysian models through Halal investments. Independent and democratically run institutions are embraced by the citizens and households, as such entities mobilize the pool of savings in riba-free investments and extend their amenities during their destined pilgrimage.

Globally, Islamic countries offer Shariah-compliant savings plans to facilitate citizens in undertaking the Hajj journey. Malaysia established the Hajj savings scheme known as Tabung Haji in 1969, which can become a role model for other countries. Tabung Haji manages approximately $18.2 billion of public money as of 2022, with more than 9 million registered savers and a branch network of 123 branches and over 10,000 touchpoints. The funds are put in Shariah-compliant schemes by allocating 53%, 27%, 15%, and 5% to equities, fixed income securities, real estate, and cash, respectively (Siddiqui & Naz, 2023). Whereas, Indonesia established Badan Pengelola Keuangan Haji (BPKH) to manage Hajj funds in the year 2017. India, with a large percentage of Muslim population, has been efficiently utilizing Hajj funds since 2010 under Zakat Foundation by investing in Shariah-compliant projects. Nigeria has launched a Hajj savings and investment scheme named National Hajj Commission of Nigeria to enroll those who intend to undertake Hajj in the next five years (Siddiqui & Naz, 2023). In view of the financial Hajj models of Malaysia, Indonesia, and some other countries, Pakistan should step up and develop an exclusive Hajj savings plan in order to facilitate millions of people to save and utilize accumulated wealth for the Hajj journey. These funds would potentially cover all Hajj expenditure through Shariah-compliant returns earned from investments.

Research QuestionsThe government announced to abolish the subsidy on Hajj cost in order to cut down the burden on the government exchequer. Hence, there is a strong need to establish an independent institution under the umbrella of MoRA which can manage funds in line with the world’s efficient Hajj fund management entities. To propose an institution for managing Hajj savings, this study strives to answer the following four questions:

- What would be the legal structure of the proposed entity?

- How would the deposited funds be deployed?

- How would the deposits be managed by the fund management entity?

- What would be the monitoring mechanism of funds under management?

The structure of the remaining paper is as follows. The second chapter comprises literature review. The third chapter provides the methodology and evaluates the operation and structure of Tabung Haji (TH) in Malaysia and Badan Pengelola Keuangan Haji (BPKH) in Indonesia through desk research. Further, the Pakistani model is also analyzed critically in the same chapter. The fourth chapter develops a legal structure of the proposed entity in Pakistan, along with the framework for the management and monitoring of the Hajj funds. The fifth chapter concludes the study with a summary of the major findings regarding the efficient utilization of funds to make annual pilgrimage affordable for ordinary citizens through proposed operational structure and policy suggestions.

Literature Review

Islam is a complete code of life. Islamic Shariah is the pathway to be followed by every individual whoever embraces Islam. The Islamic economic system requires conformity with the rules of the Shariah. It sets divine injunctions and laws that regulate every aspect of human life including in day-to-day affairs. There are five categories in which Shariah provides the pathway to be followed by all individuals. These are beliefs (aqaid), acts of worship (ibadaat), dealings with others (muamlaat), manners (ikhlaqiat), and economics (maishat). Islam forbids riba (usury or interest). The Holy Quran says “And Allah has allowed trade and prohibited usury” (Al Baqarah 2:275).

Ibadaat and muamlaat are the two most important categories of life in which certain businesses have a lot of importance due to its practical reasons, such asTabung Haji (TH). Tabung Haji is an exceptional organisation in the world which provides for the requirement of Malaysian Muslims to smoothly undertake Hajj. TH works in nearly the same way as any Islamic Bank (IB) or an Asset Management Company (AMC), that is, collecting funds and doing investments. It receives continuous inflows every year because of its monopolistic status in administering pilgrims’ funds. The organization has several subsidiaries which can be clustered into three major sectors, namely plantation, project management, and services. This type of structure underscores its role in the GDP growth of Malaysia (Ishak, 2011; Rahman, 2000). Besides, its financial performance is quite satisfactory (Mannan, 1996), which suggests that other Muslim countries may possibly follow the TH model.

Badan Pengelola Keuangan Haji (BPKH) is an autonomous public legal unit that manages Hajj funds. It reports to the Indonesian President through the Ministry of Religious Affairs. Indonesia has the world’s largest Muslim population, exclusively providing Hajj services since the 1970s (Bianchi, 2004). They also have the world’s largest Hajj pilgrim quota (Saudi Hajj Statistics, 2023). The Indonesian Ministry of Religious Affairs collects down payment to cover the Hajj pilgrimage cost or Biaya Penyelenggaraan Ibadah Haji (BPIH) from Hajj savers. The BKPH law was passed in 2014. Under this Act of Parliament, the BPKH is declared an official independent agency. It was established in 2017 and commenced her operation in 2018.

Household sector has a greater fraction of savings in emerging economies. Burney et al. (1992) documented that the household sector accounted for almost 83% of the total savings during the last three decades. Income is the key factor and the most important financial indicator impacting household savings in Pakistan. However, the savings rate in Pakistan is very low (Ahmad & Asghar, 2004). Low income, a high cost of living, natural disasters, and the lack of consistent policies has resulted in a low savings rate to GDP (Nasir & Khalid, 2004). Consistent policies, along with institutional and structural reforms, are needed to boost savings and channelize them into productive investment opportunities.

Methodology

Desk research was conducted based on publicly available scholarly works, as well as official documents, to gain a thorough understanding and insights regarding the Hajj fund management systems of Malaysia and Indonesia. Sources, such as laws passed by the parliamentarians, regulatory orders/circulars, decisions, reviews, and regulations issued by the Malaysian and Indonesian government entities were reviewed to understand the legal and financial environment of the two jurisdictions. The websites of Tabung Haji (TH), Badan Pengelola Keuangan Haji (BPKH), books, academic journals, newspapers, and magazines were also studied to meet the research objectives.

A critical analysis was carried out about the prevailing Hajj cost and funds management in the case of Pakistan. Then, the data and information were compared with the above two international organizations offering Hajj services and managing Hajj funds. Following thorough the investigation of entities working in Indonesia, Malaysia, and Pakistan, the current study proposes efficient institutional arrangement in Pakistan in light of the activities, functions and procedures adopted by Malaysia and Indonesia.

Hajj Funds Management in Malaysia and IndonesiaSaudi Arabia sets Hajj quotas for each country every year, allowing 0.1% of the Muslim population all over the world to undertake the Hajj journey. The Hajj authorities of the respective countries invest vast resources to ensure the safety of their pilgrims, such as providing transportation, hotel accommodation, food, and healthcare services. Besides, the cost of Hajj is increasing every year. Malaysia is one of the first economies that set the international standard in pilgrim education and subsidized the Hajj cost (Tabung Haji, n.d.). In 1970s, Indonesia also setup a Hajj regime with centralized resources and powers vested in the Ministry of Religious Affairs (Bianchi, 2004). The Indonesian government passed different resolutions through Acts of Parliament, such as Law No. 17/1999, 23/2008, and 34/2014, to manage Hajj affairs.

Hence, this research critically analyzes the activities of Hajj fund management in these two jurisdictions. More specifically, these jurisdictions were selected due to their robust system of organizing Hajj affairs professionally and subsidizing the Hajj cost in accordance with the need of their subjects.

Lembaga Tabung Haji, MalaysiaLembaga Tabung Haji (TH) is a statutory body established in Malaysia under the Tabung Haji Act, 1995 (Act 535) to facilitate pilgrimage to the holy sites. Its prime responsibilities include Hajj management, as well as depository services and investment. Its consistent track record has gained it worldwide recognition as an efficient Hajj management entity. Almost 32% of Malaysia’s total population have accounts with TH. In addition to the deposits received from potential pilgrims, it receives funds from various other sources, such as grants, donations, gifts, contributions, and bequests.

The Board of Directors (BOD) of TH issued audited its financial statement as of 31 March, 2023. As per the financial statement, the total number of its Hajj depositors increased by 10 million, with a deposit base of RM 87 billion, as shown in Table 1 below.

Table 1

Performance of Tabung Haji

|

Year |

Number of Savers |

Total Amount (RM) |

|---|---|---|

|

1963 |

1,281 |

46,610 |

|

1964 |

6,566 |

816,146 |

|

1990 |

1.7 million |

1 billion |

|

2008 |

4.7 million |

17 billion |

|

2009 |

5.0 million |

23 billion |

|

2012 |

8.2 million |

38 billion |

|

2013 |

8.3 million |

45 billion |

|

2014 |

8.6 million |

54 billion |

|

2015 |

8.8 million |

62 billion |

|

2016 |

9.1 million |

67 billion |

|

2017 |

9.3 million |

70 billion |

|

2022 |

10 million |

87 billion |

One of TH’s corporate social responsibility contribution towards the society is the provision of HAFIS. Through HAFIS, first time pilgrims (that is, muassasah pilgrims) have to pay less than the actual cost of the Hajj.

The eligibility for registration with TH is that the person should be a Malaysian citizen. People of any age can open an account after fulfilling the documentary requirements. For the Hajj season of 2022, the muassasah pilgrims had to pay RM 10,980 for B40 category and RM 12,980 for non-B40 category. Hajj cost for 1443H/2022 was initially estimated at RM 25,540 but subsequently increased to RM 28,632 due to the imposition of certain additional charges by the host country. With the tiered Hajj payment and Hajj costing of RM 28,632 per pilgrim, total HAFIS expenses (Hajj expenses) significantly declined by subsidizing the Hajj cost of nearly RM 14,560 for B40 category and RM 15,652 for non-B40 category.

At TH, funds are usually collected under the wakalah contract. TH acts as an agent to manage the depositors’ funds. Since 1980s, its investment portfolio has been invested in various sectors including agriculture and livestock, construction, and manufacturing. The diversified portfolio allows it to cover the rising costs of Hajj and resultantly subsidize its cost. Further, TH has setup 17 subsidiaries spanning across different sectors, including finance, plantation, construction, telecommunications, utilities, property development, oil and gas, and others (Lembaga Tabung Haji, 2022, 2023). Accordingly, TH fund management ensures that the depositors’ money remains secured and profit distribution remains stable. To achieve the objective of smooth returns, TH has developed long-term strategic asset allocation, reserves, and distribution policies. Moreover, it has the discretion to adjust its strategic asset allocation and investment risk profile in light of the changes in the economy, while following the aforementioned framework.

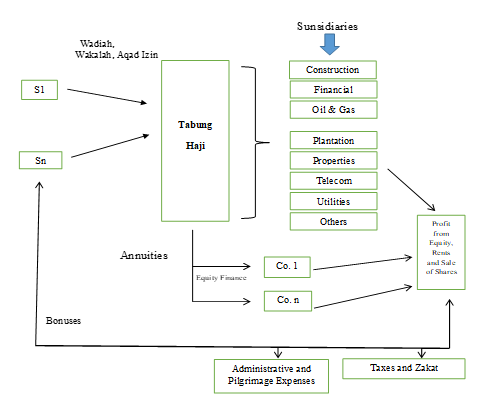

Figure 2

Mode of Operations at Tabung Haji

Note. Source: (Cizakca 2011; Lembaga Tabung Haji, 2023),

The objectives while managing capital are to maintain a solid capital base and protect the ability to sustain itself financially, to maintain the trust of the investor/creditor and the market, and to sustain the future growth of the business. Another objective is to maintain an optimal leverage ratio that is consistent with debt covenants and regulatory requirements. Figure 2 describes the fund management function of TH.

The S1 and Sn in Figure 2 show the deposits made by pilgrims intending to go for the Hajj journey. TH uses the contract ‘wadiah yad dhamanah’, that is, interest free deposits, for safekeeping. Depositors authorize TH through the wakalah contract to invest their savings. The depositors enter into a contract by filling up their personal and nominee forms which include the authorization of aqad izin. The aqad izin document shows that the depositors agree to park money with TH and give discretion to its fund managers to manage their surplus funds for investment purposes (Cizakca, 2011). TH channelizes small savings by investing in major industrial, agricultural, commercial, and real estate projects in accordance with the Shariah principles (Cizakca, 2011; Gomez et al., 2017). Moreover, it has also launched a Restricted Investment Account (RIA) which empowers it to extend financial facilities to Muslim entrepreneurs and small businesses.

TH provides a running finance facility by offering six financial products: profit-loss sharing (musharakah), profit-sharing (mudarabah), leasing (ijarah), cost-plus financing (murabaha), interest-free loan (qardhul hasan), and deferred payment sale (bai bithaman ajil).

Badan Pengelola Keuangan Haji, IndonesiaBadan Pengelola Keuangan Haji (BPKH) was set up as an independent entity to administer Hajj funds and directly reports to the President of Indonesia through the Ministry of Religious Affairs. In 2023, Saudi Arabia approved 221,000 pilgrims from Indonesia to enter the country and perform the Hajj. The government fixed the 2023 Hajj pilgrimage fee at IDR 98.89 million (US$ 6,604) per person, as compared to the 2022 cost of IDR 39.89 million. The government justified the cost due to currency devaluation and higher general price levels for the proposed 2023 Hajj costs. The Ministry of Religious Affairs recently proposed that an individual would need to pay Rp 69.1 million for the Islamic pilgrimage, a significant jump from Rp 39.8 million in 2022. The remaining Rp 29.7 million will be generated from the earnings of the funds (Bona, 2023).

The Ministry of Religious Affairs receives down payment, locally called Biaya Penyelenggaraan Ibadah Haji (BPIH), from potential pilgrims. The payment of Hajj expenses for regular pilgrims is carried out in two stages. The first stage was open from January 10th till February 12th, 2024 and extended until February 23rd, 2024. The second stage was open from March 13th to March 26th, 2024. As only 194,744 members of the pilgrim group settled their fees, the payment period was extended until April 1st-5th, 2024. (Rachmawati, 2024).

The BPKH law was passed in 2014. BPKH was created as an official independent agency in 2017 and commenced its activities in 2018. It manages Hajj finance as well. Hajj financial management strictly follows Shariah laws, prudential principles, is not-for-profit, works transparently, and remains accountable to the public by reporting directly to the President of Indonesia. BPKH aims to improve the quality of the Hajj journey. The Ministry of Religious Affairs Indonesia (Kemenag) plays a dual role, both as a regulator and as an operator, to best serve the prospective pilgrims. However, in the past, some problems hit the Ministry of Religious Affairs and it was subsequently reformed in areas ranging from organizational reforms, regulations, information systems, and so forth. Based on the different challenges that arise, the main question is how effective is the management of pilgrim funds? The main problem of pilgrims in Indonesia today is the length of the waiting list/time for their departure which even goes up to 20 years. The number of applicants continues to pile up, reaching approximately 1.2 million. The average waiting time is 15-18 years. On the other hand, there have been some concerns about the quality of facilities provided for Umroh and hence the disappointment of pilgrims has been increasing.

Funds Management at BKPHDue to the long queue of pilgrims, the Indonesian government has requested the Saudi government for an additional quota of 30,000 people each year (Jumali, 2018). Since 2004, the Hajj fund has been passively managed by placing it with banks in short-term securities, that is, liquidity instruments, as well as in Islamic sukuk with long-term maturity (Bland, 2014). In the past, there have been allegations of misappropriation of funds (Onishi, 2010) and lack of management oversight (Bianchi, 2004). The issuance of Law No. 34/2014 came as good news for Hajj fund management. This law obligated the formation of BPKH that directly reports to the President through the Ministry of Religious Affairs.

In terms of contract (‘aqd), prior to the establishment of Law No. 34/2014, the fund was dedicated for safekeeping purpose only to perform Hajj. Therefore, it could not be used or managed for other purposes. However, under the new contract, the potential Hajj pilgrim depositors sign the wakalah contract agreement when they deposit their down payment as muwakkil, while the Ministry of Religious Affairs acts as a representative (wakil) to manage the down payments in accordance with the regulation (Jumali, 2018). Funds received from deposits and investments are used in three ways: firstly, to subsidize the cost of attending the annual pilgrimage; secondly, to cover the operational expenses; and lastly, to return the leftover sums in prospective pilgrims’ accounts (Winosa, 2017).

Prior to the issuance of Law No. 34/2014, there was no policy for investing the Hajj fund. The collected amount from the potential pilgrims was placed in bank accounts under the administration of the Ministry of Religious Affairs. There were no guidelines for the placement of funds only in Islamic Banks (IBs). Thus, it is likely that some portion of the Hajj fund was parked in non-Shariah-compliant financial products. Mandatory requirement for funds’ placement in IBs was issued in 2013 through the decree of Ministry of Religious Affairs. According to Law No. 34/2014, BPKH is now authorized to diversify the investment portfolio into more productive activities likely to generate greater benefit to the depositors as the primary beneficiaries and increase the wellbeing of Muslims. In 2017, BPKH manages Hajj fund amounting to IDR 106 trillion (Abimanyu, 2017). Moreover, to minimize the risk of the fund’s misappropriation, there is a specific provision which states that the implementation body (i.e., Badan Pelaksana) and the supervisory body (i.e., Dewan Pengawas) of BPKH are jointly and severally held accountable for any losses incurred by not observing prudent practices in managing the fund (Law No. 34/2014).

There is a 70:30 ratio, that is, a Hajj applicant is obligated to pay 70% of the total Hajj expenditure, while 30% is covered by the Hajj fund. The government set the total budget for the Hajj journey (BPIH) at IDR 90 million, while each pilgrim must pay IDR 49.8 million to cover the airfare, living expenses, and a portion of the service package fee. The remaining amount is covered by the average financial benefit value, which includes expenses incurred in organizing the pilgrimage, both in Saudi Arabia and in the home country.

The data by the Ministry of Religious Affairs shows that the cost of performing Hajj has been on a steady rise as compared with the past decade. The recent 4 years of data is given in Table 2. The reasons for the rise in cost are higher general price levels, an increase in the demand for Hajj, and the rising expenses of smoothly managing the annual Hajj event. Besides, the global pandemic has added to the costs due to the strict enforcement of health protocols and to ensure the safety of pilgrims.

Table 2

Performance of Badan Pengelola Keuangan Haji (BPKH)

|

Year |

BPIH Total |

Costs incurred by the Hajjis |

|---|---|---|

|

2018 |

68.96 |

35.24 |

|

2019 |

69.16 |

35.24 |

|

2022 |

97.79 |

39.89 |

|

2023 |

90.05 |

49.81 |

Note. Source: Ministry of Indonesian Religious Affairs from published report of 2023.

Malaysian and Indonesian Investment Approach

The Table 3 below compares Malaysia’s TH and Indonesia’s BPKH regarding their Hajj fund management and investment approaches based on recent studies.

Table 3

Malaysian and Indonesian Investment Approach

|

|

Malaysia |

Indonesia |

|---|---|---|

|

Fund Understanding & Depositor Contract |

Uses wadiah yad dhamanah (safekeeping with guarantee) contract. It gives TH wakalah (agency) to invest funds. Depositor consent required. |

Uses wakalah (agency) contract under Law No. 34/2014; funds are managed productively on Shariah principles. |

|

Investment Portfolio |

Diverse investments across agriculture, manufacturing, finance, real estate, telecom, plantations, and more; direct investments via subsidiaries. |

More conservative; limits on asset types with max allocations - Islamic banking, sukuk, gold (max 5%), direct investments (max 20%), others (max 10%). |

|

Performance & Returns |

Returns supplement Hajj costs and subsidize pilgrims; historically stable but with some subsidiary risks. |

Higher return index than Malaysia’s (according to studies); focuses on growing assets with strict transparency. |

|

Governance & Accountability |

Federal statutory body with Shariah advisory board; some past financial scandals but strong governance structures. |

Independent public legal entity accountable to president; strict transparency, audit, supervisory board with joint liability. |

|

Use of Returns |

Subsidizes Hajj expenses and pays zakat on behalf of depositors. |

Covers operational costs, subsidizes pilgrims, and credits returns back to pilgrim accounts. |

The management of Hajj affairs involves many crucial steps which require thorough attention. This project critically analyzes the current set-up in Pakistan to identify certain gaps and suggest improvements in the existing structure of Hajj management in light of Shariah guidelines. In the following section, certain aspects of Hajj management strategies and challenges are highlighted. The study also highlights some of the problems pilgrims continue to encounter.

Ministry of Religious Affairs and Interfaith Harmony (MoRA)Brief History. According to the Ministry of Religious Affairs and Interfaith Harmony (MoRA) Hajj Publication 2023, the Ministry was established in October 1974. Prior to 1974, different Pakistani ministries had been dealing with Hajj operations. In June 2013, the erstwhile Ministry of National Harmony merged with the Ministry of Religious Affairs to emerge as the Ministry of Religious Affairs and Interfaith Harmony. The Ministry has the following wings:

- Hajj Wing

- Dawah and Ziarat

- Research and Reference

- Zakat and Umrah

- Interfaith Harmony

- Admin and Finance

Pilgrims Selection Procedure. A lottery system is implemented to select the final pilgrims from amongst the potential applicants. Although technological advancement has made Hajj relatively convenient in some ways, yet there are hardships and challenges encountered by pilgrims with limited resources, including accommodation, transport, and limited space at Mashair (Mina Arafat-Muzdalifah). The Government of Pakistan endeavors to make the Hajj journey as smooth as possible within the available financial means by carrying out elaborate arrangements through a well-defined process, so that pilgrims from Pakistan could focus on Hajj rituals as enshrined in the Holy Quran and Sunnah.

Hajj Scheme for Pakistani Pilgrims for the Year 2024.- Pakistanis proceed for Hajj under two schemes, including the “Government Hajj Scheme” for individuals who intend to go under government arrangements and the “Private Hajj Scheme” for individuals who want to go through Hajj Group Organizers (HGOs), in line with the Service Provider Agreement (SPA) between the Ministry and HGOs. The ratio for the allocation of the Hajj quota between government and private schemes is 50:50, that is, 89,605 pilgrims each. Under the government scheme, the applicants can apply and get selected through balloting as per the past practice.

- Hajj collections are deposited in Islamic Banking Institutions (IBIs). MoRA places Hajj funds in IBIs, where they are kept in mudarabah-based savings accounts. This is the common industry practice of IBIs to share the profit at the ratio of 30:70 against funds placed for Hajj related activity. However, apart from the savings plans offered by several banks, there is no entity that can manage Hajj funds for onward investment at the provincial or central/federal level.

- Hajj Compensation Fund-Hajj Policy 2010 envisages compensation for deceased pilgrims for up to PKR 1,000,000 through the takaful insurance policy (MoRA Hajj Policy 2024).

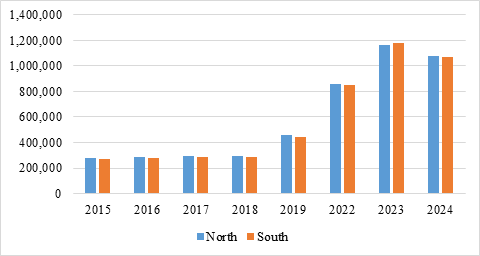

Historical Hajj Pricing at MoRA. Hajj is a true depiction of submission to Almighty Allah. Successfully performing the Hajj has religious and social significance. It also involves financial commitment on behalf of the pilgrim, as substantial cost is associated with this ibadah for every Muslim. As per the statistics of MoRA, Hajj expenses in Pakistan for 2024 were around Rs. 1,140,000/- (including Qurbani), which is 422% higher than the year 2015, when they were Rs. 270,181. The year wise data taken from MoRA Hajj Publications 2015-2023 is shown below in Table 4.

Table 4

Year Wise Hajj Expenditures

|

Years |

North Region (PKR) |

South Region (PKR) |

Additional Details |

|---|---|---|---|

|

2015 |

264,971 |

255,971 |

Without Qurbani |

|

279,181 |

270,181 |

With Qurbani |

|

|

2016 |

270,941 |

261,941 |

Without Qurbani |

|

284,281 |

275,281 |

With Qurbani |

|

|

2017 |

280,000 |

270,000 |

Without Qurbani |

|

293,050 |

283,050 |

With Qurbani |

|

|

2018* |

280,000 |

270,000 |

Without Qurbani |

|

293,050 |

283,050 |

With Qurbani |

|

|

2019 |

436,975 |

426,975 |

Without Qurbani |

|

456,426 |

446,426 |

With Qurbani |

|

|

2022** |

860,177 |

851,127 |

Support Money Provided |

|

2023 |

1,165,000 |

1,175,000 |

Regular Scheme |

|

$4,325 |

$4,285 |

Sponsorship Scheme |

|

|

2024 |

1,075,000 |

1,065,000 |

Normal Hajj Package |

|

1,150,000 |

1,140,000 |

Short Hajj Package |

|

|

$3,800 |

$3,765 |

Sponsorship Normal Hajj |

|

|

$4,015 |

$4,050 |

Sponsorship Short Hajj |

Note. Source: MoRA Hajj Publication 2015-2023 and Hajj Policy 2024.

*Federal Government provided subsidies of Rs. 44,101 for each haji.

**Federal Government approved Rs. 4.88 billion as support money for Pakistani Hajj Pilgrims. Each Pilgrim received Rs. 150,000/-

-For Year 2020-2021 Hajj was cancelled due to the pandemic (Novel Corona Virus 2019).

Figure 3

Year Wise Hajj Expenditures

Note. Data Extracted from MoRA Hajj Publication 2015-2023

Since 2018, an enormous increase in Hajj cost can be witnessed in Figure 3. The government also revoked all the subsidies, resulting in a sharp increase in cost. An unstable economic outlook and 39.4% of people living below the poverty line also indicates that public finds are extremely hard to save for the Hajj journey. Muslim households with higher savings can afford the Hajj cost. However, in emerging economies like Pakistan, not only is the saving rate too low to meet the Hajj obligation, but the higher general price level, especially after the global pandemic, further pushes down the saving habits of households.

The above-mentioned analysis of saving patterns, income levels, and costs to perform this holy journey indicates that a very limited number of people could afford to undertake the Hajj journey. Poverty is defined as households earning less than $3.65 a day, thus 39.4% of the population lives below the poverty line (Rana, 2023). Hence, a serious economic responsibility needs to be assumed to collect and effectively manage pilgrims’ funds if the government wants Muslims to perform Hajj comfortably and for Hajj to remain financially affordable for a large segment of the population.

Regulatory Gap Analysis of the Three Countries

Here’s a quick regulatory gap analysis focusing on Pakistan vs. Malaysia and Indonesia to implement a Hajj fund management body.

Table 5

Regulatory Gap Analysis of Pakistan, Malaysia and Indonesia

|

|

Indonesia |

Malaysia |

Pakistan |

|---|---|---|---|

|

Legal Framework |

Indonesia has Law No. 34/2014 establishing an independent Hajj fund management agency (BPKH) with clear authority, accountability, and investment guidelines. |

Malaysia created a statutory body Tabung Haji under federal law (Pilgrims Management and Fund Board Act), allowing it to manage savings, investments, and pilgrimage arrangements. |

Pakistan currently manages Hajj fund through government banking channels under ministry oversight. However, it lacks a dedicated independent legal entity or a comprehensive regulatory framework specifically for Hajj fund management like Indonesia or Malaysia. |

|

Governance and Accountability |

Indonesia’s BPKH has separate implementation and supervisory bodies, with joint liability for mismanagement. |

Malaysia’s Tabung Haji functions under Shariah governance with clear fiduciary duties, Shariah advisory boards, and investment control. |

Pakistan relies on ministry and banking regulations with auditing but lacks in statutory independence, Shariah governance frameworks, and specific accountability mechanisms for a Hajj fund manager. |

|

Investment and Shariah Compliance |

Indonesia mandates Shariah-compliant investment portfolios with diversification into low-risk productive sectors, regulated by law. |

Malaysia’s Tabung Haji invests in Shariah-compliant assets like Islamic banking products, sukuk, and real estate. |

Pakistan currently does not have formal regulations mandating Shariah-compliant investments for Hajj funds, limiting productive fund growth and compliance clarity. |

|

Operational Autonomy |

Indonesian body operates independently with their own management structures and financial authority. |

Malaysian body operates independently with their own management structures and financial authority. |

Pakistan’s Hajj funds are managed by government ministries and private operators under digital monitoring but lack autonomous operational status. |

- Enact a dedicated law to establish an independent Hajj fund management authority akin to Indonesia’s BPKH or Malaysia’s Tabung Haji.

- Define governance structures, including supervisory and Shariah advisory boards, with clear roles and liabilities.

- Introduce mandatory Shariah-compliant investment regulations for Hajj funds, allowing portfolio diversification in productive, low-risk assets.

- Provide legal accountability provisions for fund mismanagement, with exclusive audit and oversight mechanisms.

- Grant operational autonomy to the fund authority for efficient fund management and transparent reporting. This would bring Pakistan’s system in line with leading Islamic countries, enabling ethical, productive, and transparent Hajj fund management.

Results and Discussion

Tabung Haji or TH effectively mobilizes the Hajj funds by investing as per Shariah guidelines. It diversifies funds in the agriculture, commerce, real estate, plantation, transportation, and oil and gas sectors, in conformity with the Shariah principles. TH investment in the real sector has facilitated the GDP growth of Malaysia. It not only provides economic benefits to the pilgrims but also creates employment opportunities within the Malaysian economy. Similarly, the BKPH of Indonesia also provides exemplary services to the people. It manages one of the biggest crowds of Hajj applicants every year besides managing the investment of pilgrims’ funds in Shariah-compliant investment avenues.

It is the need of the hour that Pakistan should restructure itself like Malaysia and Indonesia, where it provides not only exemplary Hajj services but also manage Hajj funds for prospective Hajjis. This follows the judgement of the Supreme Court of Pakistan regarding the abolishment of riba/interest form the entire banking system and also with State Bank of Pakistan’s resolve to fully convert to the Islamic banking system by 2027. The author expects that a wide range of Shariah-compliant products and services will be available for millions of Pakistani people. The incorporation of an entity similar to TH or BKPH in the economy would benefit the people by opening a wide array of Shariah-compliant investment avenues, such as mudarabah, sukuk, Islamic commercial papers, real estate, agriculture, the manufacturing sector, infrastructure development, renewable energy initiatives, startups, Shariah-compliant equities, placement in IBIs, asset management companies, Islamic mutual and pension funds, and other Shariah-compliant avenues.

If the data for the total Hajj pilgrims from the Saudi General Authority of Statistics is analyzed, Pakistan is second in line by sending the second highest number of Hajj pilgrims after Indonesia. Over the years, Pakistan has been granted with the second highest percentage of Hajj quota due to its population. Table 6 shows the year wise data related to the total quota of pilgrims allowed to visit Saudi Arabia during the years 2015-2024.

Table 6

Year Wise Hajj Quota

|

Hajj Years |

GHS |

HGOs |

TOTAL |

|---|---|---|---|

|

2015 |

71,684 |

71,684 |

143,368 |

|

2016 |

86,201 |

57,347 |

143,368 |

|

2017 |

107,526 |

71,684 |

179,210 |

|

2018 |

107,526 |

71,684 |

179,210 |

|

2019 |

107,526 |

71,684 |

179,210 |

|

2022 |

32,453 |

48,679 |

81,132 |

|

2023 |

89,605 |

89,605 |

179,210 |

|

2024 |

89,605 |

89,605 |

179,210 |

Note. Source: Compiled from the Hajj Policy and Plan (2015 to 2024).

Due to Pandemic for two years pilgrims did not go from Pakistan to perform Hajj.

If we take conservative data for the period 2015-2024 of the Government Hajj Scheme (almost 50% quota) with minimum cost per pilgrim and convert the data into USD, we can see the following details in Table 7.

Table 7

Year Wise Hajj Expenditures (Only Public Sector)

|

Hajj Years |

GHS |

Hajj Cost |

TOTAL PKR |

TOTAL USD |

|---|---|---|---|---|

|

2015 |

71,684 |

270,181 |

19,367,654,804 |

68,195,967.62 |

|

2016 |

86,201 |

275,281 |

23,729,497,481 |

83,554,568.60 |

|

2017 |

107,526 |

283,050 |

30,435,234,300 |

107,166,317.96 |

|

2018 |

107,526 |

283,050 |

30,435,234,300 |

107,166,317.96 |

|

2019 |

107,526 |

446,426 |

48,002,402,076 |

169,022,542.52 |

|

2022 |

32,453 |

851,127 |

27,621,624,531 |

97,259,241.31 |

|

2023 |

89,605 |

1,075,000 |

96,325,375,000 |

339,173,855.63 |

|

2024 |

89,605 |

1,065,000 |

95,429,325,000 |

336,018,750.00 |

Note. *USD=284 (USD Rate assigned to Pakistani Banks by MoRA for 2024 Hajj Pilgrims)

The conservative data depicts an economic activity of around USD 340 million in the short process of Hajj application collection. If the full data (Government Scheme + Private Scheme) is taken, we have the following details in Table 8.

Table 8

Year Wise Hajj Expenditures (Public + Private Sector)

|

Hajj Years |

THS |

Hajj Cost |

TOTAL PKR |

TOTAL USD |

|---|---|---|---|---|

|

2015 |

143,368 |

279,181 |

40,025,621,608 |

140,935,287.35 |

|

2016 |

143,368 |

284,281 |

40,756,798,408 |

143,509,853.55 |

|

2017 |

179,210 |

293,050 |

52,517,490,500 |

184,920,741.20 |

|

2018 |

179,210 |

293,050 |

52,517,490,500 |

184,920,741.20 |

|

2019 |

179,210 |

456,426 |

81,796,103,460 |

288,014,448.80 |

|

2022 |

81,132 |

860,177 |

69,787,880,364 |

245,731,973.11 |

|

2023 |

179,210 |

1,175,000 |

210,571,750,000 |

741,449,823.94 |

|

2024 |

179,210 |

1,150,000 |

206,091,500,000 |

725,674,295.77 |

Note. *USD=284 (USD Rate assigned to Pakistani Banks by MoRA for 2024 Hajj Pilgrims)

If the data in Table 8 is closely analyzed and merged with the data from Table 5, that is, taking the total number of Hajj applicants and incorporating all the private Hajj applicants into the Government Hajj Scheme or under a single scheme, then there is an accumulation of around USD 725 million in a single year. If Pakistan generates this type of activity from a total of around 180,000 Hajj applicants, then there is a strong need for a Shariah-compliant institution within MoRA that can potentially bring 240 million plus population on the platform where people can save, invest, and plan for their future Hajj needs.

The potential of the proposed entity to manage funds is very high, given the Pakistani population of 255 million, with 98% of people practicing Islam. If the proposed fund management entity would be able to attract 20 million account holders with average savings of Rs. 50,000 per annum, this could mean over Rs. 1 trillion per annum. If such a fund is managed optimally, the savings portfolio over time could reach Rs. 10 trillion or USD 35 billion. Such a large fund, if invested in the real sector and in Shariah-compliant businesses, will extend significant economic benefits to the country through employment generation, along with making Hajj affordable for ordinary public. A portion of the profit earned from investments will go back to Hajj savers through digital payment methods, while another portion from returns on investment can be used to provide Hajj-related subsidies, thus reducing the burden on common Pakistanis and generating enormous economic activity. To streamline the activities of the proposed institution, a proper mechanism for audit would have to be instituted under the supervision of regulators, such as SBP and SECP, for proper checks and balances in both banking and non-banking operating procedures.

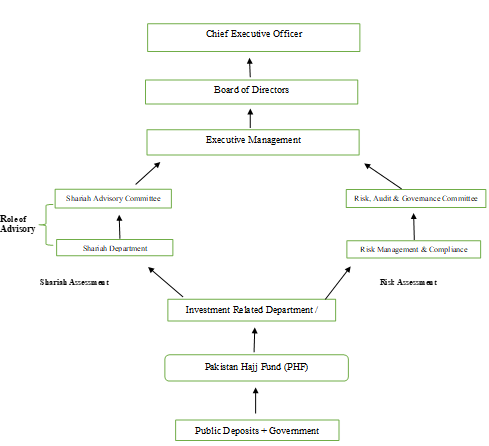

Structure of Proposed EntityAs shown in Figure 4 and based on TH and BKPH models of collecting deposits, it is suggested to establish an entity herein called ‘Pakistan Hajj Fund’ (PHF) as a subsidiary of the Ministry of Religious Affairs through a bill passed by the Parliament or by mandating SBP and/or SECP to issue a framework/guideline for the efficient utilization of Hajj depositors’ money. SBP, as the regulator for financial institutions, is managing them quite efficiently through macroprudential regulation. Besides, the people of Pakistan trust SBP as an independent and autonomous central bank. Likewise, SECP can also be mandated as it works closely with Pakistan Stock Exchange (PSX) and also supervises non-banking financial institutions, such as Islamic AMCs, leasing companies, modarabas, and takaful operators.

Figure 4

Structure of the Proposed Entity

An independent board with seasoned investment advisors/bankers, Shariah scholars, and market specialists should be nominated as members by the government to oversee the strategic level initiatives of the proposed institution. PHF should be empowered to accept Hajj deposits from the government and public, make investments under the guidance of professional and qualified management to cover the cost of all Hajj-related services, ensure the profit distribution ratio, payment of government taxes on returns, zakat payment, and also undertake all the allied and related tasks as deemed necessary.

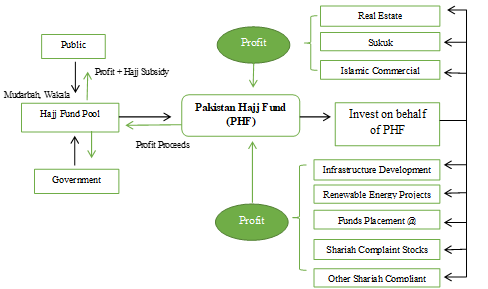

Fund Mechanism of the Proposed EntityFigure 5

Fund Mechanism of the Proposed Entity

The investment and management of funds under the proposed entity would be conducted as shown in Figure 5. PHF, based on mudarabah, receives funds from the general public and the government; directs the funds via different avenues available for investment like sukuks, Islamic commercial papers, real estate, the manufacturing sector, infrastructure development, renewable energy initiatives, financing startups, Shariah-compliant equities, placement in IBIs, as well as Islamic mutual and pension funds, and other Shariah-compliant avenues. The funds under the mudarabah contract might also carry a risk, that is, loss to the business borne by the investor/hajj savers (rabbul maal).

On receiving of profit from the funds, the funds and profit should be utilized for the Hajj management services. Furthermore, allied subsidies and the remaining profit should be disbursed to different stakeholders including the Hajj savers, payment to government through taxes, payment of zakat, and management fee.

ConclusionIt is very difficult for the majority of the public in Pakistan to save persistently for Hajj. Common people save money for many years and then wait for the right time when they can afford to undertake the Hajj journey. Many households in Pakistan participate in the traditional saving techniques. These kinds of savings make very low or no contribution toward economic development; however, these customary practices prevail in many parts of the country. The development process requires the channelization of savings to investments.

The current study proposes a model: an institutional arrangement which can attract general public to deposit savings for the Hajj journey at an early age. This pool of savings can be utilized to fuel productive investment opportunities in the country. Next, a critical analysis of the current setup in Pakistan was undertaken to identify the gaps. Hence, the discussion revolves around the legal structure of the proposed entity, with the right procedure to deploy the deposited funds by various stakeholders. The study discusses the management of funds by the proposed entity along with the monitoring mechanism and oversight by the banking and capital market regulators.

This is the high time for a country like Pakistan to establish an independent fund management entity (i.e., Pakistan Hajj Fund or PHF – proposed name) within MoRA that would cater to the financing needs of pilgrims intending to visit Makkah, Medina, Arafat, and Mina through the government’s Hajj scheme. By establishing the proposed institution, Hajj would become affordable for millions of Muslims across the country and would also help the economy to prosper. PHF would ensure compliance, not just in investment but in ethical governance and transparency as well. Besides, it would promote justice by providing everyone a fair, riba-free way to save for a key religious duty. It would also foster equity by letting people from all income levels to contribute and benefit. Moreover, PHF would support public welfare through charitable waqf funds that help those who can’t fully afford Hajj, reflecting Islamic finance’s core aim of community support, social good, and public welfare.

Recommendations- Following the efficiently run systems of TH and BKPH, a viable operational structure with the name of Pakistan Hajj Fund (PHF) is proposed. It can be established to manage and oversee Hajj savings plan at the federal government level (national level). The proposed fund can potentially benefit millions of people to gradually accumulate wealth or financial assets and use them for the holy pilgrimage. Therefore, the accumulated savings in the form of Shariah-compliant halal profits from varied investment avenues to the registered citizens would cover all Hajj end-to-end expenses.

- The PHF would be established autonomously through an act of parliament to accept Hajj deposits and make investments under the guidance of experienced management with the aim to provide complete Hajj services under the joint supervision of SBP and SECP.

- As per the above mentioned discussion, it is also suggested to merge the overall Hajj pilgrims quota granted by the Saudi government into the proposed organization. Further, the private scheme quota should be completely abolished so that funds may well be placed for investment purposes and Hajj as an ibadah should be affordable equitably for all.

- After the formation of the Hajj-related entity, it is suggested to apply efficient sales management technique and carry out public engagement activities. In this regard, a comprehensive relationship management process should be formulated. It should aim to build an effective relationship with the potential Hajj applicants including the sales blitz activities. The sales blitz activities would highly emphasize the importance of comprehending the significance of the institution. By doing so, a massive response from the public is expected which can lead to greater success for the newly established entity.

- Likewise, IBIs and IFIs should be smartly used to propagate awareness among the public including young savers. Further, a separate booth for one window operation should be installed to facilitate the public, countrywide. This would make people understand the basic reason behind the establishment of the proposed entity with the effect that people including young savers may start to save money at an early age for their future Hajj obligation. Thus, money hoarding would be discouraged and efficient allocation of funds would revive the economy.

- The use of technology can also ignite the entire process of creating awareness among people for account opening, funds placement, savings, profit taking, and planning for performing Hajj in the future. People would have the option of keeping their savings at the proposed organization and looking at their portfolios on a real time basis.

- The use of Fintech and smart wallet accounts can further enhance the efficiency of the proposed PHF. According to the second quarterly payment system review report of 31 December 2023, the number of digital wallets registered with EMIs and Branchless Banking (BB) service providers has increased by 18.1% to 2.4 million (e-Wallets) and by 6.1% to 61.3 million (M Wallets), respectively. In just one year, an immense growth of around 1 million new account holders has been recorded. By using the technology, such as JazzCash, EasyPaisa, RAAST, PayPak, 1Bill Invoice, and others, people may have swift access to their account status and current balance, which may influence their future Hajj planning.

- The PHF might face potential problems including the lack of trust, since public may doubt fund security. It may also be affected adversely by low public awareness, since a large proportion of people might not know about the fund or how to join it, as well as its investment risks. Moreover, inefficient allocation of capital or investment could reduce the rate of return. The solution to the said problems lies in ensuring transparent audits, strong Shariah governance, clear reporting, launching awareness campaigns via mosques, social media platforms, and community events, and by following prudent, Shariah-compliant investment guidelines coupled with professional management.

- In Pakistan, different types of Islamic financial institutions exist, offering Shariah-compliant savings plans for Hajj. However, the need to set up a dedicated, legal, and centralized entity under MoRA is imperative. Such an entity should have the mandate to collect funds, as well as manage, monitor, and audit all financial transactions, thus ensuring an accessible and affordable journey for pilgrims every year. Once the proposed model or entity is approved, a working committee of experts can be formed (as trustees or board of directors of the institution) to oversee the affairs following its commercial launch.

Conflict of Interest

The authors of the manuscript have no financial or non-financial conflict of interest in the subject matter or materials discussed in this manuscript.

Data Availability Statement

The data associated with this study will be provided by the corresponding author upon request.

Funding Details

This research did not receive grant from any funding source or agency.

REFERENCES

Abimanyu, A. (2017, August 23–24). Indonesia Hajj fund enhancing prosperity [Paper presentation]. Proceedings of 2nd Annual Islamic Finance Conference. Yogyakarta, Indonesia

Ahmad, M., & Asghar, T. (2004). Estimation of saving behavior in Pakistan using micro data. The Lahore Journal of Economics, 9(2), 73–92.

Baig, U. (2016). Hajj management in Pakistan in the light of experience of Tabung Haji of Malaysia. International Journal of Islamic Economics and Finance Studies, 2(2), 13–40.

Bianchi, R. (2004). Guests of God: Pilgrimage and politics in the Islamic world. Oxford University Press.

Bland, B. (2014, February 14). Indonesia taps $5.4bn Hajj fund for financial salvation. Financial Times. https://www.ft.com/content/fe4fbfe4-956a-11e3-8371-00144feab7de

Bona, M. A. (2023, January 30). Govt blames rising dollar, inflation for Hajj cost hike. Jakarta Globe. https://jakartaglobe.id/news/govt-blames-rising-dollar-inflation-for-hajj-cost-hike

Burney, N. A., Akhtar, N., & Qadir, G. (1992). Government budget deficits and exchange rate determination: Evidence from Pakistan [with comments]. The Pakistan Development Review, 31(4), 871–882.

Cizakca, M. (2011). Islamic capitalism and finance: Origins, evolution and the future. Edward Elgar Publishing.

Gomez, E. T., Padmanabhan, T., Kamaruddin, N., Bhalla, S., & Fisal, F. (2017). Minister of Finance Incorporated: Ownership and control of corporate Malaysia. Springer.

Ishak, M. S. (2011). Tabung Haji as an Islamic financial institution for sustainable economic development. Proceedings of Economic Development & Research, 1(7), 236–240.

Jumali, E. (2018). Management of Hajj funds in Indonesia. Journal of Legal, Ethical and Regulatory Issues, 21(3), 1–9.

Lembaga Tabung Haji. (2022). Annual report 2022. https://prod-th-assets.s3.ap-southeast-1.amazonaws.com/pdf/tab-content/0/2023-11-16/TH_AR22_25.10.pdf?

Lembaga Tabung Haji. (2023). Annual report 2023. https://prod-th-assets.s3.ap-southeast-1.amazonaws.com/pdf/press-release/0/2024-10-16/TH_AR23_19.07_compressed.pdf

Mannan, M. A. (1996). Islamic socioeconomic institutions and mobilization of resources with special reference to Hajj management of Malaysia. Islamic Research and Teaching Institute (IRTI). https://ideas.repec.org/p/ris/irtiop/0048.html

Muneeza, A., Sudeen, A. S. T., Nasution, A., & Nurmalasari, R. (2018). A comparative study of Hajj fund management institutions in Malaysia, Indonesia and Maldives. International Journal of Management and Applied Research, 5(3), 120–134. https://www.ijmar.org/v5n3/18-009.html

Nasir, S., & Khalid, M. (2004). Saving–investment behavior in Pakistan: An empirical investigation. The Pakistan Development Review, 43(4, Part II), 665–682. https://www.jstor.org/stable/41261020

Onishi, N. (2010, August 6). In Indonesia, many eyes follow money for Hajj. The New York Times. https://www.nytimes.com/2010/08/06/world/asia/06hajj.html

Rachmawati, E. (2024, April 6). Govt closes installment payments as Indonesia’s Hajj quota is fulfilled. Kompas. https://www.kompas.id/baca/english/2024/04/06/en-pelunasan-biaya-haji-ditutup-kuota-jemaah-indonesia-terpenuhi

Rahman, K. (2000). Towards Islamic banking: Experiences and challenges: A case study of Pilgrims Management & Fund Board, Malaysia. Institute of Policy Studies.

Rana, S. (2023, September 23). 95m Pakistanis live in poverty: World Bank. The Express Tribune. https://tribune.com.pk/story/2437352/95m-pakistanis-live-in-poverty-world-bank

Siddiqui, A. A., & Naz, J. (2023, November 13). Hajj fund enabling savings with economic development. Express Tribune. https://tribune.com.pk/story/2446100/hajj-fund-enabling-savings-with-economic-development

Tabung Haji. (n.d.). Corporate profile. Retrieved April 5, 2025, from https://www.tabunghaji.gov.my/en/corporate-profile

Winosa, Y. (2017, February 26). Independent agency to manage Indonesia’s $6.7 billion Hajj fund to start in Q4. Global Islamic Economic Gateway. https://salaamgateway.com/story/independent-agency-to-manage-indonesias-67-bln-hajj-fund-to-start-in-q4