| Review | Open Access |

|---|

Impact of Fintech Adoption, Green Innovation, and Green Finance on Environmental Performance: Evidence From Pakistani Islamic Banks |

|

|---|

![]() Muhammad Shoaib Hassan1*, Ayesha Siddiqa2, and Muqaddas Waseem2

Muhammad Shoaib Hassan1*, Ayesha Siddiqa2, and Muqaddas Waseem2

1Hailey College of Commerce, University of the Punjab, Lahore, Pakistan

2Superior College, Daska, Pakistan

Guided by the resourced-based view (RBV) and the stakeholder theory, this study is motivated to examine the impact of fintech adoption (FA), green innovation (GI), and green finance (GF) on the environmental performance (EP) of Pakistani Islamic banks (IBs). A quantitative research methodology was adopted, employing a structured questionnaire to collect data from 209 bank managers, operations managers, and financial analysts. The respondents were selected using the stratified random sampling technique from the IBs operating in four major cities of Punjab, Pakistan, namely Lahore, Sialkot, Gujranwala, and Gujrat. SEM results confirmed that fintech adoption significantly enhanced environmental performance (β = 0.372, p = 0.000), implying that digital banking reduces resource consumption and improves operational efficiency. Green finance was also found to be a strong predictor of environmental performance (β = 0.426, p = 0.000), suggesting that financial institutions investing in green projects achieve better sustainability outcomes. Among the three independent variables, green innovation exhibited the highest impact on environmental performance (β = 0.498, p = 0.000), emphasizing the role of paperless banking, energy-efficient infrastructure, and sustainable financial practices. The findings underscore the critical role of fintech-driven financial solutions, green banking innovations, and environmentally responsible investments in enhancing sustainability in the Islamic banking sector. Policymakers should develop regulatory frameworks and provide incentives to encourage banks to promote green financial services and sustainability-driven fintech solutions. Future studies should conduct cross-country comparisons, adopt longitudinal designs, and explore moderating variables, such as government regulations and corporate governance structures. This study examines the combined impact of fintech adoption, green innovation, and green finance on the environmental performance of Pakistan IBs, an area with limited empirical evidence.

JEL Codes: G21, O33, Q56, M14

1. INTRODUCTION

Environmental performance (EP) has emerged as a critical concern across various industries, including the financial sector. With a global focus on fighting climate change and reducing environmental degradation, banks are expected to practice sustainable ways to minimize their ecological footprint (Guang-Wen & Siddik, 2023; Park & Kim, 2020). Siddik and Zheng (2021) and Zheng et al. (2021) claimed that although traditionally considered a low-impact industry, the banking sector is a key financier of activities that strongly impact the environment. Moreover, banks can encourage EP by integrating sustainable financial practices, promoting green investment, and utilizing technological advancements, while still maintaining financial stability. The ethical and Shariah-compliant principles of Islamic banking provide an opportunity to link financial operations to environmental sustainability (Jan et al., 2019). Unlike conventional banks, Islamic banks (IBs) operate on a profit-and-loss-sharing basis and do not invest in industries that harm society, such as tobacco, alcohol, and gambling. Keeping in view their ethical foundation, IBs pose as potential leaders in the area of sustainability through responsible investment and operational efficiency (Jan et al., 2019; Muhamad et al., 2022). In Pakistan, where Islamic banking is growing rapidly, the integration of sustainable practices in financial activities can improve both EP and long-term economic development. However, despite the potential of this sector, the use of modern financial tools to advance environmentally sustainable performance by IBs has not been explored to the extent (Rehman et al., 2021; Sarker et al., 2020).

Fintech adoption (FA) is one of the significant factors influencing the EP of banks (Bhuiyan et al., 2024; Guang-Wen & Siddik, 2023). Financial technology helps to digitize every transaction performed in traditional banking, optimizes resource allocation, and increases the efficiency of the service provided by the banks. Within Islamic banking, fintech also helps to develop the transparency of funds to facilitate responsible financing and greening of revenues by allocating funds to sustainable projects (Karim et al., 2022). Nevertheless, fintech in Islamic banking in Pakistan is at its initial stages of integration (Karim et al., 2022; Saba et al., 2019). Therefore, it should be explored further in terms of its role in environmentally sustainable performance.

Simultaneously, with the growing adoption of fintech, green innovation (GI) has emerged as a natural complement to improve the EP of banks (Hsu et al., 2021). GI in banking is the development and application of environmentally friendly products, services, and operations. This includes paperless banking, energy-efficient infrastructural support, and e-documents (Guang-Wen & Siddik, 2023; Hsu et al., 2021). IBs, which also follow ethical financing principles, are ideal to incorporate GI in their operations (Sarker et al., 2020). Park and Kim (2020) and Hsu et al. (2021) highlighted that banks can serve an important role in reducing the carbon footprint just by adopting sustainable branch designs that feature energy-efficient systems, solar power solutions, and good waste management strategies, all of which should prove beneficial towards executing the respective bank’s corporate social responsibility (CSR). In the Pakistani context, where the issue of environmental challenges including air pollution and deforestation persists, GI in banking can be considered as a starting point towards broader sustainability goals (Bukhari et al., 2020; Nabi et al., 2025).

Another critical aspect of sustainable banking is green finance (GF), namely financial services and products that aim to support environmentally sound investments (Guang-Wen & Siddik, 2023). It includes green bonds, eco-friendly investment funds, and funding for renewable energy projects. Moreover, IBs can position GF in line with Shariah-compliant principles by directing financial resources to ethical and sustainable activities (Malini, 2021; Pathan et al., 2022). Long-term environmental protection may be supported by investments in solar energy, sustainable agriculture, and water conservation projects, which also contribute to economic development.

While there is a growing global focus on sustainability, there is very little research available on how the adoption of fintech, GI, and GF affects the EP of Pakistani IBs, owing to the fact that the Islamic banking literature to date is mostly concerned with financial performance, risk management, and customer satisfaction, but not with environmentally sustainable performance (Jan et al., 2019; Muhamad et al., 2022; Pathan et al., 2022). Pakistani IBs are only at the initial stage of adopting ESG principles-driven financial practices, whereas conventional banks have already taken some serious strides to integrate the same (Karim et al., 2022; Saba et al., 2019). This gap is important to fill in order to understand how modern financial technologies and green activities can facilitate sustainable banking operations. In the current era of rapidly growing Islamic banking, the integration of sustainability into financial practices is necessary to ensure long-term economic and environmental well-being.

Research ObjectivesIn light of the above, this study aims to examine the influence of fintech adoption (FA), green innovation (GI), and green finance (GF) on the environmental performance (EP) of Pakistani Islamic banks (IBs). It aims to offer valuable insights to Islamic banking institutions, regulators, and policymakers. This research also adds valuable knowledge to sustainable finance literature, as well as practical recommendations, to improve the EP of IBs. This would allow us to better understand the role that FA, GF, and GI can play in improving banking and making it more efficient. Further, it would also highlight the potential of GI to minimize environmental footprints and evaluate how GF promotes eco-friendly investments in order to develop strategies to make the entire financial sector eco-friendlier.

Research Questions

Primarily, this research addresses the following research questions:

- How does FA influence the EP of Pakistani IBs?

- What is the impact of GI on the EP of Pakistani IBs?

- To what extent does GF contribute to the EP of Pakistani IBs?

The remaining manuscript is structured as follows: The literature review examines the studies available on the relationship between the selected variables. The methodology section details the research design, data collection ways, and how the data was analyzed. The next section reports and discusses the results aligned with the existing literature and theoretical framework. Finally, the study concludes with a discussion of its implications (theortical and practical) and recommendations for future scholars.

Literature Review

Literature Review and Hypothesis DevelopmentThere have been conducted several studies revealing a positive relationship between FA and EP, contending then to be useful tools for promoting sustainability. For example, Guang-Wen and Siddik (2023) demonstrated that fintech-enabled digital banking reduces paper usage, decreases energy usage, and also lowers carbon emissions. Bhuiyan et al. (2024) stated that blockchain-based fintech solutions can improve transparency in GF, so that the proceeds are allocated in an efficient way towards environmentally friendly projects. Together, these studies suggest that FA can induce the enhancement of EP through a move towards the promotion of GF, energy efficiency, and sustainable consumption of resources. Similar findings were reported by Allahham et al. (2024), who contended that the use of mobile payment systems reduces reliance on cash transactions through paper currency, which has an associated environmental impact related to its production and disposal. Scholars also noted that the use of AI-powered fintech solutions can optimize energy consumption patterns in financial institutions, resulting in a reduced carbon footprint and high EP. Karim et al. (2022) investigated the role of digital payment ecosystems in reducing carbon footprints, noting that individuals move to digital banking and contactless payment with minimal energy consumption during the banking processes. Scholars also noted that fintech-enabled smart contracts facilitate sustainable supply chain financing for companies, which encourages them to adopt environmentally responsible practices that lead to positive EP.

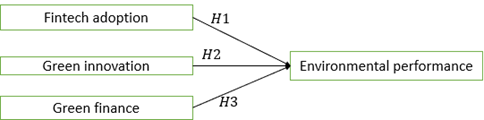

H1: FA and EP of Pakistani IBs are positively related.

Multiple studies have identified GI as a strong driver of EP. For example, as shown by Hsu et al. (2021), GI practices (which include eco-friendly product design and cleaner production processes) simply lead to reduced carbon emissions and resource efficiency in firms. The study concluded that firms engaged in GI benefit from regulatory compliance and competitive advantages that lead them towards a high EP. Likewise, Nabi et al. (2025) extended this discussion and affirmed that green technological development increases efficient waste management and causes pollution reduction. The research focused on the fact that companies with GIs are more likely to achieve sustainable development goals (SDGs) and operational efficiency. Based on these findings, Guang-Wen and Siddik (2023) examined the effects of green R&D investment on corporate EP and noted that firms which seriously invest into the research and development of sustainable technologies cuase less environmental risks, incur lower energy costs, cost reductions, and stronger brand reputation, leading them to have high EP levels. These outcomes were reinforced by Singh et al. (2020), who found that GI leads to green manufacturing by enhancing a firm’s sustainable manufacturing. This is possible when green product development and sustainable supply chain are combined. Together, both studies imply that green investments have a positive effect on environmental outcomes, as well as a positive impact on the long-term sustainability of firms.

H2: GI and the EP of Pakistani IBs are positively related.

Several studies have shown that GF has a significant positive influence on EP. For instance, Guang-Wen and Siddik (2023) found that green financial instruments (e.g., green bonds and sustainability-linked loans) significantly enhance corporate EP by permitting firms to engage in clean production technologies. The study found that such firms also result in lower carbon emissions and better sustainability metrics. Siddik and Zheng (2021) concluded the same results, stating that green credit policies encourae businesses to embrace green practices and consequently, save energy and reduce their ecological footprint. Scholars have also pointed out that financial incentives are key in determining corporate environmental strategies and lead the firms towards a high EP. Malini (2021) subsequently explored the contribution of green investment funds towards transforming environmental sustainability. The study concluded that companies that receive green investment outperform others in terms of their EP, especially in sectors with the highest pollution levels. Moreover, Hussain et al. (2024) and Ahmed et al. (2024) showed that GF promotes environmental innovation, since companies with better GF invest more in the R&D of eco-friendly technologies. Together, these studies point to the broader business advantages that GF provides beyond mere compliance, affirming that it plays a key role in improving EP through investment in sustainable technologies, regulatory compliance, and innovation.

H3: GF and EP of Pakistani IBs are positively related.

Figure 1

Conceptual Model

The Resource-Based View (RBV) is a foundational theory that describes how firms use their internal capabilities to increase their EP (Guang-Wen & Siddik, 2023), stating that organizations can gain a sustainable competitive advantage by using resources that are valuable, rare, inimitable, and non-substitutable. The adoption of fintech allows firms to create optimal financial transactions, eliminate operational inefficiencies, and promote cost-effective and environment-friendly solutions (Bhuiyan et al., 2024; Hidayat-ur-Rehman & Hossain, 2024). Allahham et al. (2024) asserted that better resource allocation is achieved through the use of digital payment systems, blockchain-based transparency, and AI-driven risk management which, in turn, results in more sustainable outcomes. Furthermore, GI (not only as an external competency but also as an internal one) helps organizations to develop eco-friendly products and processes that reduce their carbon footprint, facilitate energy efficiency, and minimize environmental degradation (Akhtar et al., 2024; Hsu et al., 2021; Singh et al., 2020). Scholars have put forth that green R&D and cleaner production investments by firms can provide them with long-term sustainability, while differentiating them from the competition in the market. These green capabilities, being valuable, rare, and hard to imitate, align with RBV’s criteria for strategic resources. When embedded into core operations, GI allows firms to reduce costs, comply with environmental regulations, and enhance their reputation, factors that collectively contribute to a sustained competitive advantage. GF is another resource that helps to invest in sustainable projects by providing access to environmentally oriented financial instruments, such as green bonds and carbon credit trading (Ahmed et al., 2024; Pathan et al., 2022; Siddik & Zheng, 2021). Guang-Wen and Siddik (2023) affirmed that firms that effectively integrate FA, GI, and GF as internal resources within their resource base are able to achieve superior EP, while also develpoing resilience to regulatory and market pressures.

On the other hand, the stakeholder theory focuses on the impact of external pressures on corporate strategies towards environmental sustainability (Betts et al., 2015), especially with respect to stakeholders, such as regulatory bodies, investors, customers, and communities. In general, all of these affect decision-making processes and the way organizations operate. The adoption of fintech solutions allows to meet the expectations of stakeholders by introducing transparency in financial transactions, as well as accountability and responsibility in investing. Sustainable lending (or green lending) and impact investing are two GF initiatives that are responsive to investor and regulatory demands for environmentally and socially conscious business practices (Bhuiyan et al., 2024; Guang-Wen & Siddik, 2023; Hidayat-ur-Rehman & Hossain, 2024).

Secondly, the demand for GI in services and products by customers encourages firms to become more sustainable and to adopt such investments. Policies and incentives implemented by governments and regulatory agencies force organizations to adopt sustainability measures within their operational activities (Akhtar et al., 2024; Singh et al., 2020). Furthermore, firms can meet compliance regulations and build stakeholder trust and long-term support through the adoption of fintech and green financial practices. Similar to GI, firms that emphasize GF respond well to social concerns regarding environmental degradation and climate change, addressing the concerns and strengthening corporate reputation as well as the existing relationships between them and key stakeholders (Ahmed et al., 2024; Hidayat-ur-Rehman & Hossain, 2024; Hussain et al., 2024). Guang-Wen and Siddik (2023) pointed out that organizations that effectively align their resource-based strengths with stakeholder expectations only enhance their EP but also enjoy a strategic competitive advantage in a progressively eco-conscious global market.

Methodology

The positivist research philosophy and the deductive research design are followed in this study. These are deemed suitable to investigate objective realities through empirical evidence and statistical analysis, while adopting a structured quantitative research methodology based on numerical data (Saunders et al., 2019). This aligns with the use of a mono-method quantitative research approach to examine the cause and effect relationship between the variables and draw generalizable conclusions. For this purpose, a structured questionnaire was used as primary data collection tool, thus avoiding subjectivity in the findings. To ensure statistical validity, the scales for the studied variables were adapted from previous studies; the seven-item scale for FA was adapted from Hu et al. (2019), the six-item scale for GF was adapted from Zheng et al. (2021), the four-item scale for GI was adapted from Khatun et al., (2021), and the seven-item scale for EP was adapted from Suganthi (2020). Previously, these scales have been used by Guang-Wen and Siddik (2023), aligning closely with the environmental and technological focus of this research. Their proven reliability in similar financial contexts ensured their relevance to Islamic banking practices in Pakistan. All the scales were operationalized on a five-point Likert scale.

In IBs, fintech can be applied across core operations including Shariah-compliant digital payments, blockchain-based smart contracts for Islamic financing, digital onboarding of customers, and AI-powered risk management systems. The aim is not only to enhance operational transparency and efficiency but to also support environmental objectives by reducing reliance on paper-based, energy-intensive processes and physical infrastructure. The FA scale used in this study included items such as mobile banking, blockchain applications, AI-integrated financial services, and online banking platforms, each directly linked to sustainable banking operations, reflecting the extent to which IBs utilize fintech tools to ensure environmentally responsible practices (Bhuiyan et al., 2024; Karim et al., 2022).

A cross-sectional research design was used to analyze the current trends and relationships between the variables within a specific time frame, that is, data was collected from September 2024 to December 2024. This approach was deemed appropriate for the evaluation of the present state of banking practices and their immediate effect on EP. The stratified random sampling technique ensured a fair and unbiased selection of the target respondents (bank managers, operations managers, and financial analysts) working in IBs in four Pakistani cities, namely Lahore, Sialkot, Gujranwala, and Gujarat. These cities were selected because they represent both metropolitan and semi-urban banking environments, offering a balanced perspective on sustainable banking practices. Targeted professionals were chosen as they are the kind of people with the required knowledge and experience to shed light on banking operations, sustainability initiatives, and financial technology adoption. Based on the 10:1 items response theory suggested by Kline (2023) and also used by Hassan (2023), the current study determined a sample size of 240 respondents. A total of 60 questionnaires were administered in each city ensuring proportionate sampling. The researcher obtained 209 completed responses with a valid response rate of 87.08%. Ethical considerations were strictly followed. All respondents received an informed consent form before participating in the survey and all of them were made aware of the study’s purpose, confidentiality measures, and their voluntary participation. All responses were kept anonymous and access to the collected data was restricted to the researchers to maintain data privacy. To ensure ethical compliance, all information was encrypted so it could not be tampered with. Moreover, the participants had the right to withdraw at any point without any consequences and with respect to their autonomy.

Structural Equation Modelling (SEM) was used for data analysis. The demographic variable summary gave a snapshot of respondent characteristics, while descriptive statistics gave an understanding of data distribution and its central tendencies, followed by convergent and discriminant validity tests. To investigate the strength and direction of the associations among the studied variables, correlation analysis was employed and the influence of each independent variable over the dependent variable was analyzed with effect size. Through the application of these rigorous statistical techniques, the study ensured that its findings remained reliable and meaningful, giving insights into how Pakistani IBs may improve their EP through financial innovation and sustainable banking.

Results

Demographic Profile StatisticsTable 1 shows that 113 respondents (54.10%) were male, while 96 (45.90%) were female, indicating a nearly equal balance that may lead to different views. Age breakdown shows that 40 respondents (19.10%) were 18-25 years old, 88 (42.10%) were 26-35, 50 (23.90%) were 36-45, 22 (10.50%) were 46-55, and 9 (4.30%) were above 55; a predominantly young to middle-aged sample likely receptive to innovation. Job positions were differentiated with 64 bank managers (30.62%), 75 operations managers (35.89%), and 70 financial analysts (33.49%) with different roles and diverging views of banking operations.

Table 1

Demographic Variables (N = 209)

|

Variables |

Particulars |

Frequency |

Percentage (%) |

|---|---|---|---|

|

Gender |

Male |

113.00 |

54.10 |

|

Female |

96.00 |

45.90 |

|

|

Age (years) |

18-25 |

40.00 |

19.10 |

|

26-35 |

88.00 |

42.10 |

|

|

36-45 |

50.00 |

23.90 |

|

|

46-55 |

22.00 |

10.50 |

|

|

Above 55 |

9.00 |

4.30 |

|

|

Job position |

Bank managers |

64.00 |

30.62 |

|

Operations Manager |

75.00 |

35.89 |

|

|

Financial analyst |

70.00 |

33.49 |

|

|

Experience |

Less than 1 year |

15.00 |

7.20 |

|

1-3 years |

42.00 |

20.10 |

|

|

4-6 years |

55.00 |

26.30 |

|

|

7-10 years |

48.00 |

23.00 |

|

|

Above 10 years |

49.00 |

23.40 |

|

|

City of Work |

Sialkot |

52.00 |

24.90 |

|

Gujranwala |

53.00 |

25.40 |

|

|

Lahore |

54.00 |

25.80 |

|

|

Gujrat |

50.00 |

23.90 |

The experience levels of the respondents, from less than 1 year (15 respondents, 7.20%) to more than 10 (49 respondents, 23.40%) reflect both the beginners and experienced professionals. While, the geographic distribution of the respondents from Sialkot (52 respondents, 24.90%), Gujranwala (53 respondents, 25.40%), Lahore (54 respondents, 25.80%), and Gujrat (50 respondents, 23.90%) indicates a sound regional presence. Overall, Table 1 depicts a demographically diverse sample with a balanced gender distribution, a largely young and middle-aged workforce, and varied professional roles and experience levels.

Descriptive StatisticsTable 2 shows that FA has a mean and standard deviation score of 4.12 and 0.68 respectively, along with a slightly negative skewness (-0.45) and kurtosis value (2.15). The low standard deviation and the high mean score reflect that the respondents have positive and similar attitudes toward FA within the Pakistani IBs. GF (M = 4.08, SD = 0.71) and GI (M = 4.25, SD = 0.62) have negative a skewness value of -0.39 and -0.51, respectively. Furthermore, they have a positive kurtosis value of 2.08 and 2.32 respectively, indicating stable responses. EP (M = 4.18, SD = 0.65) mirrors this pattern with a skewness value of -0.47 and a kurtosis value of 2.25. In general, the results indicate that the mean values of these variables are moderately high (between 4.08 and 4.25), indicating generally favorable perceptions among the respondents. Further, skewness and kurtosis values, following the criteria of Hair et al. (2019), strongly support the robustness of measurement instruments and normal data distribution (skewness and kurtosis values should be between +/-2 and +/7 respectively), which indicates that subsequent analyses are based on valid data.

Table 2

Descriptive Statistics

|

Variables |

Items |

Mean |

Std. Dev. |

Skewness |

Kurtosis |

|---|---|---|---|---|---|

|

FA |

7.00 |

4.12 |

0.68 |

-0.45 |

2.15 |

|

GI |

4.00 |

4.25 |

0.62 |

-0.51 |

2.32 |

|

GF |

6.00 |

4.08 |

0.71 |

-0.39 |

2.08 |

|

EP |

7.00 |

4.18 |

0.65 |

-0.47 |

2.25 |

Table 3 shows that the measurement model met the requisite criteria in terms of convergent validity. Regarding the EP variable, all the items have strong factor loadings, which are greater than the acceptable threshold of 0.60 (Comrey & Lee, 2013), thereby indicating that each item contributes significantly to the underlying construct. The Cronbach’s alpha value of 0.87, CR value of 0.902, and AVE value of 0.597 for EP are all well above the recommended benchmarks of 0.70 for reliability and 0.50 for AVE (Saunders et al., 2019). Similarly, the FA factor loadings range from 0.671 to 0.805. Although there is one item (FA2) with a slightly lower loading of 0.671, overall CA (0.845), CR (0.884), and AVE (0.522) values suggest robust convergent validity.

Table 3

Convergent Validity

|

Constructs |

Items |

Factor Loadings |

Cronbach Alpha |

Composite Reliability |

Average Variance Extracted |

|---|---|---|---|---|---|

|

FA |

FA1 |

0.718 |

0.845 |

0.884 |

0.522 |

|

FA2 |

0.671 |

||||

|

FA3 |

0.742 |

||||

|

FA4 |

0.805 |

||||

|

FA5 |

0.689 |

||||

|

FA6 |

0.759 |

||||

|

FA7 |

0.674 |

||||

|

GI |

GI1 |

0.812 |

0.708 |

0.835 |

0.625 |

|

GI2 |

0.795 |

||||

|

GI4 |

0.755 |

||||

|

EP |

EP1 |

0.742 |

0.87 |

0.902 |

0.597 |

|

EP2 |

0.779 |

||||

|

EP3 |

0.825 |

||||

|

EP4 |

0.812 |

||||

|

EP6 |

0.769 |

||||

|

EP7 |

0.701 |

||||

|

GF |

GF1 |

0.751 |

0.88 |

0.911 |

0.63 |

|

GF2 |

0.841 |

||||

|

GF3 |

0.873 |

||||

|

GF4 |

0.819 |

||||

|

GF5 |

0.794 |

||||

|

GF6 |

0.668 |

Further, the measurement model’s reliability is supported by the CA value of 0.88, CR value of 0.911, and AVE value of 0.63 of the GF construct, with factor loadings ranging from 0.668 to 0.873. The CA, CR, and AVE values of GI items are 0.708, 0.835, and 0.625 respectively, with loadings between 0.755 and 0.812. According to Fornell-Larcker criterion, these results confirm that each construct is being measured properly. Thus, the constructs capture the intended theoretical dimensions accurately and reliably.

Discriminant Validity (Fornell Larker Criteria)Table 4 presents the results of discriminant validity. The values in the diagonal of the table are the square roots of the AVE value for each construct, which should exceed the inter-construct correlations (Saunders et al., 2019). The square root of AVE for EP is 0.773, which is higher than the correlations with FA (0.532), GF (0.578), and GI (0.561). Likewise, the square root of AVE of FA (0.723) is greater than its correlations with EP (0.553), GF (0.553), and GI (0.512).

Table 4

Discriminant Validity (Fornell Larker Criteria)

|

Variables |

EP |

FA |

GF |

GI |

|---|---|---|---|---|

|

EP |

0.773 |

|||

|

FA |

0.532 |

0.723 |

||

|

GF |

0.578 |

0.553 |

0.794 |

|

|

GI |

0.561 |

0.512 |

0.537 |

0.789 |

Moreover, GF and GI exhibit square roots of the AVE values of 0.794 and 0.789, respectively. Both exceed their correlation with other constructs, supporting that the measurement model satisfies the Fornell-Larcker criterion. So, discriminant validity remains adequate.

Correlation MatrixThe correlation matrix (Table 5) reveals that FA, GF, and GI are associated positively with EP (r = 0.532, 0.578, and 0.561, respectively).

Table 5

Correlation Matrix

|

Variables |

EP |

FA |

GF |

GI |

|---|---|---|---|---|

|

EP |

1.00 |

|||

|

FA |

0.532*** |

1.00 |

||

|

GF |

0.578*** |

0.553*** |

1.00 |

|

|

GI |

0.561*** |

0.512*** |

0.537*** |

1.00 |

All of these associations are statistically significant, implying that there is a direct link of FA, GF, and GI with the improvement in EP.

SEM Analysis and Effect Size EstimatesAccording to SEM results shown in Table 6, beta coefficient, standard error, and t value of the FA effect on EP are 0.372 (p = 0.000), 0.065, and 5.723 respectively (p < 0.001), while the relationship remains statistically significant. The effect size (F² = 0.215) is medium, indicating that improvements in FA are positively related to improvements in environmental outcomes (Cohen, 1988). Similarly, GF also has a positive and significant relationship with EP, evidenced by a beta coefficient of 0.426, standard error of 0.059, t value of 7.220 (p = 0.000), and effect size of 0.287 (medium). In particular, GI has the highest impact, with a beta coefficient of 0.498 (SE = 0.054, t = 9.222, p = 0.000, and large F2 = 0.341), indicating its significant contribution.

Table 6

Regression and Effect Size Estimates

|

Relationship |

β |

SE |

t |

p |

Effect Size (F²) |

Decision |

|---|---|---|---|---|---|---|

|

FA → EP |

0.372 |

0.065 |

5.723 |

0.000 |

0.215 |

Supported |

|

GF → EP |

0.426 |

0.059 |

7.220 |

0.000 |

0.287 |

Supported |

|

GI → EP |

0.498 |

0.054 |

9.222 |

0.000 |

0.341 |

Supported |

R² = 0.451, Adjusted R² = 0.443, NFI = 0.658 and SRMR = 0.04

Overall, the model accounts for 45.1% of the variance in EP (R² = 0.451, adjusted R² = 0.443) and remains statistically significant (NFI = 0.658 > 0.60 and SRMR = 0.04 < 0.08), aligning with the threshold proposed by Hair et al. (2019).

Discussion

SEM analysis revealed a significant positive relationship between FA and EP in Pakistani IBs, with a beta coefficient of 0.372 (t = 5.723, p = 0.000). This indicates that FA contributes to enhancing EP, suggesting that digital financial technologies play a crucial role in promoting sustainability within Islamic banking. The findings suggest that FA enables banks to optimize energy consumption, reduce paper-based transactions, and enhance operational efficiency, leading to improved environmental outcomes. From a practical standpoint, IBs should continue investing in fintech solutions that support environmental sustainability. Whereas, regulatory authorities may also consider incentivizing fintech-driven green initiatives, fostering a more sustainable banking ecosystem. Additionally, financial institutions should integrate fintech strategies into their CSR frameworks to further enhance their environmental impact. Similar findings were reported by Karim et al. (2022), who contended that the use of mobile payment systems reduces reliance on cash transactions via paper currency. This has an associated environmental impact related to the latters production and disposal. Moreover, scholars noted that fintech enabled smart contracts facilitate sustainable supply chain financing for companies which encourages them to adopt environmentally responsible practices that lead to positive EP. The obtained results also align with RBV, as FA represents a strategic resource that enhances operational efficiency and environmental sustainability (Bhuiyan et al., 2024). Moreover, the stakeholder theory supports these findings, as FA addresses the expectations of regulators, customers, and environmental advocates by promoting responsible banking practices.

The second research objective was to assess the relationship between GI and EP in Pakistani IBs. The results revealed a strong positive relationship with a beta coefficient of 0.498 (t = 9.222, p = 0.000). This indicates that GI plays a critical role in enhancing environmental sustainability within the banking sector, implying that by integrating AI-driven risk assessment, paperless banking, and carbon footprint tracking systems, IBs can significantly improve their EP. Additionally, investing in green fintech solutions, such as blockchain for sustainable finance and AI-powered energy efficiency models, strengthens their commitment to sustainability.

From a practical perspective, IBs should actively promote research and development in GI to drive long-term sustainability. In this regard, collaboration with fintech firms and regulatory bodies can accelerate the adoption of innovative green technologies. Additionally, policymakers should introduce supportive frameworks and incentives to encourage financial institutions to integrate GI into their strategic operations. Multiple studies have recognized GI as a strong driver of EP. For example, Akhtar et al. (2024) and Nabi et al. (2025) demonstrated that organizations that GI takes enhance environmental compliance. Moreover, there is increased stakeholder trust, proving the GI’s positive impact on corporate sustainability. The above studies focused on the fact that companies with GI are more likely to achieve sustainable development goals and operational efficiency. The result also align with RBV, as GI serves as a valuable organizational resource that enhances competitive advantage and environmental sustainability. This further suggests that by embedding GI into their core operations, IBs can strengthen their market position while fulfilling sustainability commitments (Hsu et al., 2021; Singh et al., 2020).

The third research objective concerns the relastionship between GF and EP. SEM analysis revealed a strong positive relationship with a beta coefficient of 0.426 (t = 7.220, p = 0.000), suggesting that GF initiatives significantly enhance EP in the banking sector. This implies that GF supports environmentally responsible investments, including green bonds, sustainable lending, and climate-friendly projects. By allocating financial resources to renewable energy projects and eco-friendly business initiatives, IBs can minimize their carbon footprint and promote sustainable economic growth. Additionally, integrating GF with Shariah-compliant banking principles further strengthens its impact by aligning ethical finance with environmental responsibility, incentivizing green financing mechanisms and providing tax benefits or lower capital requirements for environmentally responsible investments. Guang-Wen and Siddik (2023) and Hidayat-ur-Rehman and Hossain (2024) found that green financial instruments (e.g., green bonds and sustainability linked loans) significantly enhance corporate EP by permitting firms to engage in clean production technologies, pointing out that green financing mechanisms make a positive contribution to EP. The above studies point to the broader business advantages that GF provides beyond compliance, affirming that it plays a key role in improving corporate EP by investing in sustainable technologies, regulatory compliance, and innovation. The result also align with the stakeholder theory, as GF addresses the expectations of multiple stakeholders, including customers, investors, regulators, and environmental organizations. Resultantly, by prioritizing GF, banks not only enhance their sustainability performance but also fulfill their social responsibility (Ahmed et al., 2024; Hussain et al., 2024).

One possible reason GI outperforms fintech and GF in driving EP is that it directly alters banks’ internal operations and infrastructure, leading to immediate and visible environmental benefits, such as reduced energy use, minimized paper consumption, and lower carbon emissions. Unlike GF (which often relies on third-party investment outcomes) and fintech (which enhances efficiency more indirectly), GI involves tangible, operational changes within the bank itself. These include adopting energy-efficient branch designs, implementing digital documentation, and reducing waste through eco-friendly processes. Such internal integration offers stronger control and measurable impact, making GI a more potent driver of environmental outcomes in the short-run.

ConclusionThis study investigated the impact of FA, GI, and GF on the EP of Pakistani IBs. A quantitative research methodology was adopted, employing a structured questionnaire to collect data from 209 respondents, including bank managers, operations managers, and financial analysts from IBs in Lahore, Sialkot, Gujranwala, and Gujrat. The SEM results confirmed that FA significantly enhanced EP, highlighting that digital banking reduces resource consumption and improves operational efficiency. GF was also found to be a strong predictor of EP, suggesting that financial institutions investing in green projects achieve better sustainability outcomes. Among the three independent variables, GI exhibited the highest impact on EP, emphasizing the role of paperless banking, energy-efficient infrastructure, and sustainable financial practices. The model explained 45.1% of the variance in EP and model significance, confirming the strong influence of these variables. The findings underscore the critical role of fintech-driven financial solutions, green banking innovations, and environmentally responsible investments in enhancing sustainability in the Islamic banking sector. Given the increasing global focus on climate-conscious financial practices, Pakistani IBs must accelerate the integration of fintech and GF to align with sustainability goals. This research fills an existing gap by extending the discourse on Islamic banking beyond financial performance and risk management, positioning sustainability as a core banking function, rather than a secondary concern. Compared to studies on conventional banks in other countries, such as those in Bangladesh or Malaysia (Hsu et al., 2021; Siddik & Zheng, 2021), this study found that Pakistani IBs show relatively stronger effects of GI on EP. Moreover, while fintech and GF are emphasized in conventional banks, IBs appear to leverage their ethical and Shariah-aligned values to prioritize internal operational sustainability, which highlights the originality and contextual contribution of this study.

ImplicationsTheoretically, the study contributes to the literature on sustainable banking by demonstrating that FA, GI, and GF positively influence EP. By integrating RBV, the study highlights that financial technology and green banking practices are valuable strategic resources that enhance operational efficiency and sustainability. The findings also support the stakeholder theory, emphasizing that banks implementing environmentally responsible practices meet regulatory expectations, enhance investor confidence, and align with customer preferences for sustainable banking solutions. These insights contribute to the broader understanding of sustainable banking practices, emphasizing that environmental sustainability is not merely a regulatory requirement but also a strategic initiative that strengthens long-term financial stability and corporate reputation.

On practical grounds, this study provides very useful insights to banking institutions, policymakers, and regulators, showing a path to reduce Islamic banking’s environmental footprint by accelerating the adoption of fintech-driven solutions, such as blockchain based transactions, integrated fintech driven risk assessment, and paperless banking. Regulatory bodies should ensure that there is partnership between IBs and fintech service providers to develop advanced financial technologies which are more resource efficient, such as green regulatory sandboxes to test and scale innovative fintech models aimed at environmental sustainability. Additionally, tax incentives, reduced capital requirements, and priority lending quotas may be introduced for IBs that invest in verified green technologies or offer sustainability-linked products. Moreover, policymakers can put incentives and regulatory frameworks in place to encourage banks to promote expansion in green financial services, including renewable bonds and sustainability leveraged loans, thus improving EP through investment in GI. Financial institutions need to take a step further by integrating sustainability into their corporate strategies. Further, GF initiatives should be aligned with the Shariah-compliant investment principles based on customer awareness campaigns aimed at driving the adoption of green financial products.

Limitations and Future DirectionsDespite its contributions, this study has certain limitations. Firstly, it focuses exclusively on Pakistani IBs, limiting the generalizability of the findings to other banking systems and geographical contexts. Future studies should conduct cross-country comparisons or explore conventional banking institutions to assess whether similar fintech-driven sustainability trends exist across different financial sectors. Secondly, the research design is cross-sectional, capturing data at a single point in time. A longitudinal study would provide deeper insights into the long-term impact of FA, GI, and GF on EP, allowing for an assessment of various trends over time. Thirdly, the study relies on self-reported survey data, which may introduce social desirability bias. Future research should incorporate objective EP indicators, such as carbon footprint reduction and energy efficiency metrics, to enhance the reliability of the results. Additionally, while this study focused on direct relationships, future scholars should focus on potential moderating and mediating variables, for instance, government regulations, institutional policies, and corporate governance structures may influence the effectiveness of FA and GF in enhancing EP. Examining these factors could provide a more nuanced understanding of how financial institutions may optimize their sustainability strategies. Lastly, qualitative research methods, such as case studies or interviews, may complement quantitative findings by offering deeper insights into the opportunities and challenges associated with green banking initiatives.

Conflict of InterestThe authors of the manuscript have no financial or non-financial conflict of interest in the subject matter or materials discussed in this manuscript.

Data Availability StatementThe data associated with this study will be provided by the corresponding author upon request.

Funding DetailsThis research did not receive grant from any funding source or agency.

REFERENCES

Ahmed, D., Hua, H. X., & Bhutta, U. S. (2024). Innovation through green finance: A thematic review. Current Opinion in Environmental Sustainability, 66, Article e101402. https://doi.org/10.1016/j.cosust.2023.101402

Akhtar, S., Li, C., Sohu, J. M., Rasool, Y., Hassan, M. I. U., & Bilal, M. (2024). Unlocking green innovation and environmental performance: the mediated moderation of green absorptive capacity and green innovation climate. Environmental Science and Pollution Research, 31(3), 4547–4562. https://doi.org/10.1007/s11356-023-31403-w

Allahham, M., Sharabati, A., Almazaydeh, L., Shalatony, Q., Frangieh, R., & Al-Anati, G. (2024). The impact of fintech-based eco-friendly incentives in improving sustainable environmental performance: A mediating-moderating model. International Journal of Data and Network Science, 8(1), 415–430.

Betts, T. K., Wiengarten, F., & Tadisina, S. K. (2015). Exploring the impact of stakeholder pressure on environmental management strategies at the plant level: What does industry have to do with it? Journal of Cleaner Production, 92, 282–294. https://doi.org/10.1016/j.jclepro.2015.01.002

Bhuiyan, M. A., Rahman, M. K., Patwary, A. K., Akter, R., Zhang, Q., & Feng, X. (2024). Fintech adoption and environmental performance in banks: Exploring employee efficiency and green initiatives. IEEE Transactions on Engineering Management, 71, 11346–11360. https://doi.org/10.1109/TEM.2024.3415774

Bukhari, S. A. A., Hashim, F., & Amran, A. (2020). The journey of Pakistan’s banking industry towards green banking adoption. South Asian Journal of Business and Management Cases, 9(2), 208–218. https://doi.org/10.1177/227797792090530

Cohen, J. (1988). Statistical power analysis for the behaviors science (2nd ed.). Laurence Erlbaum Associates, Publishers.

Comrey, A. L., & Lee, H. B. (2013). A first course in factor analysis. Psychology Press.

Guang-Wen, Z., & Siddik, A. B. (2023). The effect of Fintech adoption on green finance and environmental performance of banking institutions during the COVID-19 pandemic: The role of green innovation. Environmental Science and Pollution Research, 30(10), 25959–25971. https://doi.org/10.1007/s11356-022-23956-z

Hair, J. F., Risher, J. J., Sarstedt, M., & Ringle, C. M. (2019). When to use and how to report the results of PLS-SEM. European Business Review, 31(1), 2–24. https://doi.org/10.1108/EBR-11-2018-0203

Hassan, M. S. (2023). Dynamics of employee motivation and employee performance in banking sector. Business Review, 18(2), 32–50. https://doi.org/10.54784/1990-6587.1580

Hidayat-ur-Rehman, I., & Hossain, M. N. (2024). The impacts of Fintech adoption, green finance and competitiveness on banks’ sustainable performance: Digital transformation as moderator. Asia-Pacific Journal of Business Administration. Advance online publication. https://doi.org/10.1108/APJBA-10-2023-0497

Hsu, C.-C., Quang-Thanh, N., Chien, F., Li, L., & Mohsin, M. (2021). Evaluating green innovation and performance of financial development: Mediating concerns of environmental regulation. Environmental Science and Pollution Research, 28(40), 57386–57397. https://doi.org/10.1007/s11356-021-14499-w

Hu, Z., Ding, S., Li, S., Chen, L., & Yang, S. (2019). Adoption intention of fintech services for bank users: An empirical examination with an extended technology acceptance model. Symmetry, 11(3), Article e340. https://doi.org/10.3390/sym11030340

Hussain, S., Rasheed, A., & Rehman, S. U. (2024). Driving sustainable growth: exploring the link between financial innovation, green finance and sustainability performance: Banking evidence. Kybernetes, 53(11), 4678–4696. https://doi.org/10.1108/K-05-2023-0918

Jan, A., Marimuthu, M., bin Mohd, M. P., & Isa, M. (2019). The nexus of sustainability practices and financial performance: From the perspective of Islamic banking. Journal of Cleaner Production, 228, 703–717. https://doi.org/10.1016/j.jclepro.2019.04.208

Karim, S., Rabbani, M. R., Bashar, A., & Hunjra, A. I. (2022). Fintech innovation and its application in Islamic banking from Pakistan. In M. K. Hassan, M. R. Rabbani, & M. Rashid (Eds.), FinTech in Islamic financial institutions: Scope, challenges, and implications in Islamic finance (pp. 157–174). Springer.

Khatun, M. N., Mitra, S., & Sarker, M. N. I. (2021). Mobile banking during COVID-19 pandemic in Bangladesh: A novel mechanism to change and accelerate people’s financial access. Green Finance, 3(3), 253–267. https://doi.org/10.3934/GF.2021013

Kline, R. B. (2023). Principles and practice of structural equation modeling. Guilford Publications.

Malini, H. (2021). Islamic bank sustainability in Indonesia: Value and financial performances based on social responsibility and green finance. Cepalo, 5(2), 93–106. https://doi.org/10.25041/cepalo.v5no2.2360

Muhamad, S. F., Zain, F. A. M., Samad, N. S. A., Rahman, A. H. A., & Yasoa, M. R. (2022). Measuring sustainable performance of Islamic banks: Integrating the principles of environmental, social and governance (ESG) and maqasid shari’ah. Earth and Environmental Science, 1102, Article e012080. https://doi.org/10.1088/1755-1315/1102/1/012080

Nabi, A. A., Ahmed, F., Tunio, F. H., Hafeez, M., & Haluza, D. (2025). Assessing the impact of green environmental policy stringency on eco-innovation and green finance in Pakistan: A Quantile Autoregressive Distributed Lag (QARDL) analysis for sustainability. Sustainability, 17(3), Article e1021. https://doi.org/10.3390/su17031021

Park, H., & Kim, J. D. (2020). Transition towards green banking: Role of financial regulators and financial institutions. Asian Journal of Sustainability and Social Responsibility, 5(1), 1–25. https://doi.org/10.1186/s41180-020-00034-3

Pathan, M. S. K., Ahmed, M., & Khoso, A. A. (2022). Islamic banking under vision of green finance: The case of development, ecosystem and prospects. International Research Journal of Management and Social Sciences, 3(1), 193–210. https://doi.org/10.53575/irjmss.v3.1(22)20.193-210

Rehman, A., Ullah, I., Afridi, F.-e.-A., Ullah, Z., Zeeshan, M., Hussain, A., & Rahman, H. U. (2021). Adoption of green banking practices and environmental performance in Pakistan: A demonstration of structural equation modelling. Environment, Development and Sustainability, 23(9), 13200–13220.. https://doi.org/10.1007/s10668-020-01206-x

Saba, I., Kouser, R., & Chaudhry, I. S. (2019). FinTech and Islamic finance-challenges and opportunities. Review of Economics and Development Studies, 5(4), 581–890. https://doi.org/10.26710/reads.v5i4.887

Sarker, M. N. I., Khatun, M. N., & Alam, G. M. M. (2020). Islamic banking and finance: Potential approach for economic sustainability in China. Journal of Islamic Marketing, 11(6), 1725–1741. https://doi.org/10.1108/JIMA-04-2019-0076

Saunders, M., Lewis, P., & Thornhill, A. (2019). Research methods for business students. Prentice Hall.

Siddik, A., & Zheng, G.-W. (2021). Green finance during the COVID-19 Pandemic and beyond: Implications for green economic recovery. Priprints. https://doi.org/10.20944/preprints202108.0215.v2

Singh, S. K., Del Giudice, M., Chierici, R., & Graziano, D. (2020). Green innovation and environmental performance: The role of green transformational leadership and green human resource management. Technological Forecasting and Social Change, 150, Article e119762. https://doi.org/10.1016/j.techfore.2019.119762

Suganthi, L. (2020). Investigating the relationship between corporate social responsibility and market, cost and environmental performance for sustainable business. South African Journal of Business Management, 51(1), 1–13. https://doi.org/10.4102/sajbm.v51i1.1630

Zheng, G.-W., Siddik, A. B., Masukujjaman, M., & Fatema, N. (2021). Factors affecting the sustainability performance of financial institutions in Bangladesh: the role of green finance. Sustainability, 13(18), Article e10165. https://doi.org/10.3390/su131810165