| Review | Open Access |

|---|

The Moderating Role of Corporate Governance in the Nexus between Digital Transformation and Corporate Restructuring: Evidence from Shariah-Compliant Firms of Pakistan |

|

|---|

![]() Abida Irum and

Abida Irum and

![]() Rafiullah Sheikh*

Rafiullah Sheikh*

Riphah International University, Islamabad, Pakistan

The current research analyses how digital transformation (DT) influences the outcomes of corporate restructuring (CR) with respect to Shariah-compliant companies emphasizing four dimensions, namely financial (FR), operational (OR), asset (AR), and governance restructuring (GR). It also addresses the moderating effect of corporate governance (CG), especially board size, on such a relationship. The study fills the literature gap regarding the role of digital transformation, as well as governance practices, in restructuring problems in Shariah-compliant firms by examining a sample of 100 such firms listed on the Pakistan Stock Exchange (PSX) between 2018-2023. Using the principles of the Knowledge-Based View (KBV), the study conceptualizes digital capabilities as organizational knowledge assets capable of driving organizational reconfiguration when backed by governance systems that are in line with Islamic ethical principles. The research implements a two-step System GMM estimator to overcome endogeneity as well as the bias of missing variables. It also assesses the effects of digital transformation and board aspects in influencing the form of corporate restructuring outcomes. Notably, it introduces a novel text-mining methodology to quantify digital transformation based on the information extracted from the firms’ annual reports, offering a replicable and innovative approach for future research. - The study uncovers that digital transformation significantly enhances financial restructuring, while its effects on operational, asset, and governance restructuring are not straightforward, rather they are mixed. Board size is found to positively influence asset restructuring but has limited or no effect on other dimensions. Notably, the interaction between digital transformation and corporate governance yields a negative moderation effect in financial and governance restructuring, suggesting that larger boards may inhibit the transformative impact of digital initiatives, potentially due to strategic inertia or insufficient digital literacy. The study significantly contributes to the Knowledge-Based View (KBV) and Islamic governance literature by illustrating the dual role of corporate governance, both as an enabler and a constraint in digital transformation. It also develops a new text-mining formula to measure digital transformation using annual reports, as well as potential introduction of a replicable and innovative mechanism to estimate it in annual reports of upcoming studies.

1. INTRODUCTION

Digital transformation (DT) has turned out to be a strategic need of any company in the modern world. Digital transformation is supposed to make the company competitive and relevant to the more digitized global economy. It involves the introduction of new digital technologies, such as cloud computing, big data, artificial intelligence, mobile systems, and social media and consists of their integration with the main business functions and models (Bharadwaj et al., 2013; Verhoef et al., 2021). The change allows innovation, improves customer connections, improves operation work, and creates value in the long-term (Schwertner, 2017). Although digital technologies bear a strong potential, there are also rather serious problems that occur during their implementation. These include data security challenges, technological interoperability, resistance to change, large-scale investment in the digital infrastructure, and talent (Schwertner, 2017).

With the pressures and opportunities afforded by digital transformation, a significant number of firms are engaging in corporate restructuring programs. Corporate restructuring refers to fundamental changes introduced to the structure, operations, and financial framework of any organization with the motive of enhancing performance, boosting productivity, or revamping a rapidly changing market environment (Hoskisson et al., 2002). Such restructuring work is especially needed in digital spaces where customer expectations, supply chains, and competition are evolving rapidly and need a flexible and adaptive organizational approach.

Corporate governance (CG) in this evolving business environment plays the important roles of streamlining and mediation of the impact that digital transformation has on restructuring decisions in companies. Corporate governance can be characterized as a regime of laws, practices, and processes by which a firm is directed and guided, as long as transparency, accountability, and integrity in the undertakings of the management is observed (Tricker, 2015). This purpose is furthered in Shariah-compliant firms where governance structures also serve the Islamic provisions of ethical and legal life (Metwally, 1996). Thus, in such institutions, restructuring practices not only involve efficiency and performance goals, but also need align to religious and moral prescriptions. Therefore, governance is not a dispensable constituent in the transformation process. Regarding the successful forms of governance, there are positive implications of their strategic outcomes, including the ability to manage digital risks, ensuring that the stakeholders remain on board, and make structural changes along with achieving the long-term objectives (Benson et al., 2021; Khan et al., 2020).

To the extent that the interplay between digital transformation and corporate performance has been thoroughly researched, the mediating or the moderating effect of corporate governance, particularly in the Islamic forms of business, remains under researched. With respect to Shariah-compliant firms in Pakistan, this control is particularly relevant, because such businesses exist both in the context of conventional economies and in Shariah-compliant environments. Ethics and operations dynamics that are unique to such firms require more academic scrutiny regarding the role of governance structures in influencing the digital transformation-restructuring nexus. Since the Pakistani economy continues to be more focused on technological modernisation and Shariah-compliant institutions continue to increase their presence in the Pakistani corporate environment, this triadic relationship is both practically and theoretically relevant.

The fact that only a thin slice of empirical evidence that considers the interplay between digital transformation and corporate restructuring processes driven by the impetus of governance mechanisms within the context of Islamic businesses is present reveals a significant research gap. Most existing studies emphasize the technological or operational aspects of digital transformation (Kraft et al., 2022; Zhao et al., 2022), often neglecting how corporate restructuring unfolds in response to such changes, especially in emerging markets. Furthermore, while governance has been widely discussed in terms of firm performance and risk management, its specific role as a moderator in digital-structural transitions has received insufficient empirical attention (Devadoss & Pan, 2007).

Responding to these gaps, this study is conducted to identify how corporate governance mediates the connections between digital transformation and corporate restructuring in the context of Shariah-compliant firms in Pakistan. This research contributes to the literature in three ways. Firstly, it further develops the insights into how digital transformation is a driver of corporate restructuring through an extension of the Knowledge-based View (KBV). Secondly, it adds to the existing empirical data on an emerging Islamic market, demonstrating that the level of digitalization has a profound influence on the governance structure and the amount of restructuring activities. Thirdly, it examines how corporate governance and in this case, Islamic governing principles can moderate this relationship, which may improve the effectiveness of transformation-induced structural reforms. Hence, this paper provides emerging theoretical and practical knowledge in terms of how governance mechanisms can be harnessed to traverse the process of organizational transformation within digital economies.

The rest of the study is organized in the following way. Section 2 covers literature review and hypothesis development. Section 3 maps the research methodology namely data sources, variables, and tools of data analysis. Section 4 discusses the empirical results. Finally, Section 5 and Section 6 offer concluding insights, theoretical implications, and policy recommendations relevant to scholars, practitioners, and policymakers alike.

Literature Review

Theoretical BackgroundIn the current study, the Knowledge-based View (KBV) is adopted. According to this view, sustainable competitive advantage of a firm is largely the by-product of its competency to create, integrate, and leverage knowledge. In this regard, knowledge is not as only a resource but the most strategic resource of the firm. The integrative process of knowledge and its application throughout different units is of crucial importance; this can be achieved through managers.

In the context of 21st century digitalization, KBV focuses on the idea of dynamic capabilities, including the capability of the firm to change, adapt, merge and re-align its internal and external competencies within the dynamic environment setting (Zollo & Winter, 2002). These capabilities are crucial when enterprises seek to take advantage of digital technologies in terms of aligning business operations, execution of business decisions, and customer-engaging models (Vinocur et al., 2023).

Digital transformation is normally associated with structural change between and among departments, which calls upon changes in functions and roles to enable the adoption of emerging technologies effectively (Li & Zhao, 2023). In addition, the portals including the internal digital communication tools support the cooperation and alignment of strategies and reinforce the organization with regard to flexibility (Rottner et al., 2019). Considering the important role of digital technologies in the work of firms, restructuring is required when attempting to utilize the potential of digital technologies to the utmost extent possible (Hautz et al., 2017).

Digital Transformation and Corporate RestructuringDigital transformation refers to the technique of integrating digital technology in every facet of a business. This revolution has overturned the way organizations conduct their business and deliver customer value (Fitzgerald et al., 2014). It comprises efforts that result in reworking conventional business with automation, data analytics, artificial intelligence, and cloud computing (Verhoef et al., 2021). To achieve digital transformation successfully, there should be an intention on the part of the leaders, as well as a change in culture and versatile governance settings, in order to manage the intricacies and the risks that the digital transition bears (Kane et al., 2015; Schwertner, 2017).

Corporate restructuring is the logical organization an institution or its financial structure, which allows it to be able to compete and demonstrate higher efficiency (Hoskisson et al., 2002). These include mergers, acquisitions, divestitures, and overhauls in operations. In this digital era, restructuring choices constitute a balance between the digital preparedness of a firm and what new technological capabilities the particular firm has integrated (Bellucci et al., 2023). This is due to the fact that integrating digital tools offer greater possibilities in financial analysis, risk analysis, optimization of resources, and shaping better de-mobilization strategies (Verhoef et al., 2021).

Hypothesis 1 (H1): Digital transformation positively influences corporate restructuring.

The Role of Corporate GovernanceCorporate governance is defined as how a firm is governed by rules, practices, and processes. It focuses on accountability, transparency, ethical leadership, and remains one of the key mechanisms of aligning corporate actions with the needs of stakeholders (Riaz et al., 2022). When it comes to Shariah-compliant companies, the issue of governance assumes a broader scope since it also considers Islamic ethics and rules of jurisprudence. This two tier structure warrants that business operations remain not only compliant with the internationally prevailing standards of corporate governance but that they also comply with the doctrines of Islamic law (Metwally, 1996).

Governance is especially critical in moments of digital transformation, when ongoing organizational renewal can achieve balance between technological disruption and workplace continuity in preserving strategic coherence. Effective governance mechanisms facilitate the alignment of innovation with long-term organizational objectives, as well as effective management of risk, and also increase the level of stakeholder trust (Benson et al., 2021). In this context, board-level attributes, including size, independence, and diversity, have been observed as key variables predicting top quality governance. Bigger boards are likely to provide a wider pool of expertise and enhanced oversight ability in the context of restructuring efforts, whereas smaller boards may lead to more nimble decisions (Goodstein et al., 1994).

There is growing empirical evidence that robust governance enhances the success of corporate restructuring by enforcing strategic discipline, ensuring due diligence, and reducing transformation-related risks (Tran et al., 2024). However, in Shariah-compliant firms, governance is further complicated by religious and ethical obligations. These firms must ensure that all strategic decisions, including those related to restructuring and innovation, remain consistent with Islamic moral and financial principles. This dual governance requirement presents both challenges and opportunities for firms operating within Islamic financial systems (Khan et al., 2020).

Hypothesis 2 (H2): Corporate governance positively influences corporate restructuring.

The Moderating Role of Corporate GovernanceAlthough an effective governance system can support the process of aligning technological innovation and business strategy, it can also become a barrier when being too intrusive or not having sufficient digital literacy (Hanelt et al., 2021).

Digital restructuring requires the Board of Directors (BOD) to steer organizational change. The role it plays in digital technologies, risk management, resource allocation, and performance evaluation gains even more significance as firms increasingly embrace digital technologies. What makes these obligations even more sensitive to Shariah-compliant firms is the perceived expectation that it considers maqasid al-Shariah, the higher objectives of Islamic law, during the upholding of all phases of the transformation (Devadoss & Pan, 2007). This requires that boards have competency not only in corporate governance but they also have a sense of Islamic ethical aspects in the digital era.

An expert-based, technology-sensitive board is able to provide useful advice on how to fix technological uncertainty. Digital restructuring risks can be assessed more efficiently by such boards, which can warrant such ethical compliance and achieve transparent communication with stakeholders (Dery et al., 2017). Conversely, governance may limit the transformative opportunities of digital initiatives by becoming too rigid or out of touch with digital strategy. Hence, the association of digital transformation with restructuring could be partially dependent on the quality and strategic inclination of the governing structure.

Hypothesis 3 (H3): Corporate governance moderates the relationship between digital transformation and corporate restructuring.

Islamic Views on Corporate Governance, Digital Transformation, and ReconstructionRecent articles point to the influential role that corporate governance plays in mediating the relationship between digitalization and corporate restructuring, at least among Shariah-compliant companies. Laksono et al. (2025) stated that Islamic fintech, blockchain, and artificial intelligence improve business operations in Islamic financial institutions, provided that digital inventions are aligned with the Shariah. Although these technologies are promising, they have issues that need to be addressed, such as regulatory preparedness and Shariah digital literacy, to ensure that Islamic ethical principles are not violated.

Moreover, Wati et al. (2024) evaluated the involvement of digital accounting innovations into the accounting system that follows Shariah principles. Their observations showed that although digital innovation has been adopted in areas related directly with the customers, such as payments and treasury management, adoption in core accounting and governance functions such as Shariah, is not significant. This highlights the need to have a distinctive theoretical construct that incorporates Islamic accounting principles and digital transformation models to enable sound ethical adherence and efficient operation.

In addition, Tran et al. (2024) considered the moderating role of digital transformation in corporate governance and its impact on the corporate restructuring axis in Vietnam. They determine that, whereas digital transformation and corporate governance are autonomous and make different additions to corporate restructuring, the conjunction of the two increases the impact of the former in the change and outcomes of restructuring. The main consequence of this finding is the realization that the true benefit of digital transformation in the reorganization of labor can be achieved only through well-designed corporate governance systems.

Enhancing digital infrastructure to support Shariah-compliant contracts such as murābahah, ijārah, mushārakah, and mudārabah and making them accessible through online and mobile banking platforms is a part of the digital transformation of Islamic financial systems (Desky & Maulina, 2022). To increase financial inclusion, Islamic banks also digitize waqf, zakat, and ṣadaqah management. Innovations including Shariah-compliant P2P financing, robo-takaful, halal investment robo-advisory, and blockchain-enabled smart contracts that promote transparency and steer clear of gharar and riba are introduced through partnerships with Islamic fintech companies (Laksono et al., 2025). To warrant compliance and trust, these developments call for robust cybersecurity, digital Shariah governance, automated Shariah audit systems, and e-KYC procedures. In general, digital transformation improves Islamic finance by coordinating technological advancement with fundamental values, such as justice, openness, etc.

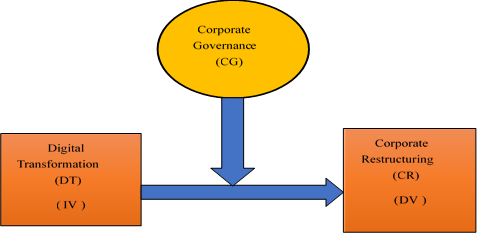

Theoretical FrameworkFigure 1

Theoretical Framework

This paper utilizes the Knowledge-Based View (KBV) approach, such that knowledge is considered as one of the most important organizational assets that enable the organizations to achieve sustainable competitive advantage. The conceptualisation of digital capabilities brings to play the knowledge assets that facilitate the reconfiguration of an organisation. Further, it is only through this reconfiguration that the organisation is effectively governed in accordance with the values aligned with the Islamic ethical principles. Corporate governance, in this instance board size, has a moderator role and influences the relationship between digital transformation and corporate restructuring in the Shariah-compliant firms. Although digital transformation is the key to structural modification, its success depends on the governance system that ensures an adequate degree of technological development and alignment with the ethical principles of Islam, so that restoration projects not only lead to the positive dynamics of business development but also comply with the moral values articulated in the Islamic law.

Research Methodology

Data Collection Approach and Research DesignThe proposed study is quantitative and aims to examine the impact of digital transformation on the process of corporate restructuring in Shariah-compliant companies listed on the Pakistan Stock Exchange (PSX). The moderating role of the relationship between corporate governance measured using board size is also an important part of the current research. The decision to select the Shariah-compliant firms is due to the ethical and operating structure within which these firms operate. These are embedded in the core values of Islam. The presence of Shariah Supervisory Boards (SSBs) guide these companies which are destined to be governed by Islamic values such as amanah (trust), sidq (truthfulness), and masooliyyah (accountability). These values shape the constitution and methods of decision-making in these companies.

To undertake the current study, annual reports of 100 Shariah-compliant firms listed within a six-year period, from 2018 to 2023, were used as secondary data. Annual reports were chosen as the source of primary information since they offer insights into technology adoption strategies and answers related to re-organization based on these strategies. Firms with incomplete annual report data of at least five years were excluded, so that the panel could provide a balanced dataset and was not skewed with missing data.

The extent of digital transformation was measured using the text mining methodology adopted from Zhao et al. (2022), Unerman (2000), and Roberts (1997). Digital initiatives stated in the annual reports were analysed and the frequency and occurrence of their related keywords were used as proxies of firm engagement in digital transformation. The choice of digitalization, cloud computing, blockchain, artificial intelligence, and big data as keywords was made after studying the entire digital innovation and Islamic fintech literature. To measure the extent of reliability, two investigators applied the manual count of the frequency of keywords with each on conducting across all reports, and a small number of disagreements were resolved through this process of cross-validating. The digital transformation index was then constructed using the natural logarithm of the keyword count plus one (to account for zero frequencies). This log transformation ensured normalization and mitigated the effect of extreme values.

Variables and MeasurementThe dependent variable, corporate restructuring (CR), is operationalized as a composite index with three distinct dimensions:

- Financial Restructuring (FR): Measured by the change in a firm’s debt-to-equity ratio, capturing efforts to realign capital structure.

- Operational Restructuring (OR): Measured by changes in operating expenses relative to total income, reflecting cost efficiency and internal realignment.

- Asset Restructuring (AR): Measured through changes in total assets, indicating resource reallocation, divestitures, or acquisitions.

The CR composite index is calculated by using principal component analysis (PCA). It is a statistical technique used to reduce dimensions and to assign weights in accordance to data variance.

A fourth restructuring indicator, namely governance restructuring (GR), is also analyzed separately and measured through the board gender diversity ratio. This variable reflects the alignment of firm governance practices with both Islamic ethics (emphasizing equity and inclusion) and SECP guidelines promoting female representation in corporate leadership.

The independent variable digital transformation (DT) is measured by log-scale numbers of digital-related keywords, as described above.

The moderating variable corporate governance is proxied by board size (BSIZE), which represents the number of Board Directors. Although larger boards are often associated with greater expertise and a wider range of perspectives, the literature also cautions that they may suffer from coordination inefficiencies.

The control variables include

- Firm Size (SIZE): Measured by using the natural logarithms of total assets. It controls the scale and availability of resources.

- Firm Age (AGE): The age of the firm since its incorporation portrays organizational maturity and years of experience.

An interaction term (DT * BSIZE) is used to test whether corporate governance moderates the effect of digital transformation on restructuring.

Research Model and Econometric StrategyThe dataset comprised 600 firm-year observations (100 firms over 6 years), making panel data analysis suitable. However, panel datasets often suffer from endogeneity, heteroskedasticity, and autocorrelation, especially when lagged dependent variables are involved.

To overcome these econometric problems, this study used a two-step System Generalized Method of Moments (GMM) estimator developed by Arellano and Bover (1995) and Blundell and Bond (1998). The approach involves the use of internal instruments based on the lagged variables to eliminate simultaneity bias, omitted variable bias, and unobserved heterogeneity bias. Also, the Windmeijer (2005) correction was carried out to discount the standard errors of finite-sample bias.

Instrumental validity was ensured by using Hansen J-test leaving the serial correlation in residuals tested with the Arellano-Bond AR(2) test. To avoid the effect of multicollinearity in regression results, the variance inflation factors (VIFs) were computed.

Research ModelThe current research is based on 100 firms tracked over a span of 6 years (2018 to 2023) using panel data. It is desirable to use panel data techniques taking into consideration the fact that cross-sectional units are more than time periods. The conventional OLS estimation can be biased because of endogeneity issues, such as the relationship between the lags of dependent variables and error terms (Tran et al., 2024).

This is countered by the two-step System Generalized Method of Moments (System GMM). The estimation procedure copes with endogeneity, heteroscedasticity, and serial autocorrelation due to internal instruments being applied. The estimate is corrected to make the results more robust with a finite sample correction (Windmeijer, 2005). The ability of the instruments is determined by Hansen test and Arellano-Bond AR(2) test (Arellano & Bover, 1995).

The connection between digital transformation and corporate restructuring was assessed with regard to the following regression models:

|

1. |

FRit= |

β0 |

+ |

β1DTit |

+ |

β2BSIZEit |

+ |

β3SIZEit |

+ |

β4AGEit |

+ |

Ɛit |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

2. |

ORit= |

β0 |

+ |

β1DTit |

+ |

β2BSIZEit |

+ |

β3SIZEit |

+ |

β4AGEit |

+ |

Ɛit |

|

3. |

ARit= |

β0 |

+ |

β1DTit |

+ |

β2BSIZEit |

+ |

β3SIZEit |

+ |

β4AGEit |

+ |

Ɛit |

- CRit= β0 + β1DTit + β2BSIZEit + β3SIZEit + β4AGEit + Ɛit

- GRit= β0 + β1DTit + β2BSIZEit + β3SIZEit + β4AGEit + Ɛit

The moderating effect of corporate governance was realized through the addition of interaction terms between digital transformation (DT) and board size (BSIZE):

- FRit= β0 + β1DTit + β2BSIZEit + β3DT * BSIZEit + β4SIZEit + β5AGEit + Ɛit

- ORit= β0 + β1DTit + β2BSIZEit + β3DT * BSIZEit + β4SIZEit + β5AGEit + Ɛit

- ARit= β0 + β1DTit + β2BSIZEit + β3DT * BSIZEit + β4SIZEit + β5AGEit + Ɛit

- CRit= β0 + β1DTit + β2BSIZEit + β3DT * BSIZEit + β4SIZEit + β5AGEit + Ɛit

- GRit= β0 + β1DTit + β2BSIZEit + β3DT * BSIZEit + β4SIZEit + β5AGEit + Ɛit

|

Variable |

Definition |

Measurement |

|---|---|---|

|

CR |

Corporate Restructuring |

Composite index via PCA (FR, OR, AR) |

|

FR |

Financial Restructuring |

Change in debt-to-equity ratio |

|

OR |

Operational Restructuring |

Change in operating expenses over total income |

|

AR |

Asset Restructuring |

Change in total assets |

|

GR |

Governance Restructuring |

Board gender diversity ratio |

|

DT |

Digital Transformation |

Natural log of digital keywords frequency |

|

BSIZE |

Board Size |

Total number of board members |

|

DT × BSIZE |

Interaction Term |

Product of DT and BSIZE |

|

SIZE |

Firm Size |

Natural log of total assets |

|

AGE |

Firm Age |

Years since firm’s incorporation |

The information utilised in the current paper is publically available and has been employed as per the ethical norms of academic practice. As the study only uses and analyzes secondary data, no formal human involvement was undertaken and as such no formal ethical approval was deemed necessary. Nonetheless, the study is anchored in the values of Islamic finance in so far as it encompasses honesty, fairness, and social responsibility, in the way that it is carried out methodologically. The consideration of gender diversity as a governance variable is indicative of the dedication to maqasid al-Shariah, especially that of justice, inclusion, and institutional reform.

Results

Descriptive statistics present a description of the major features of a data set. These measures can be of three types: central tendency (mean, median, mode) which represents the middle of the data, variability (standard deviation, variance) which represents the spread or dispersion of the data, and frequency distribution which describes how often the values appear in the dataset.

Table 2 Descriptive Statistics|

Variable |

Obs |

Mean |

Std. Dev. |

Min |

Max |

|---|---|---|---|---|---|

|

Years |

600 |

2020.5 |

1.71 |

2018 |

2023 |

|

CR |

599 |

-0.001 |

1.03 |

-4.213888 |

16.42678 |

|

FR |

600 |

3.13 |

23.53 |

0.0098568 |

560.9695 |

|

GR |

600 |

14.36 |

11.82 |

0 |

71.42857 |

|

OR |

600 |

0.79 |

65.00 |

-844.5186 |

880.8654 |

|

AR |

600 |

266.30 |

6190.42 |

-99.87732 |

151646.1 |

|

DT |

600 |

1.44 |

1.45 |

0 |

6.131227 |

|

BSIZE |

600 |

7.96 |

1.86 |

3 |

18 |

|

SIZE |

600 |

18.84 |

3.46 |

1.428436 |

24.86978 |

|

AGE |

600 |

48.29 |

19.90 |

17 |

137 |

Note. CR = corporate restructuring, FR = financial restructuring, GR = governance restructuring, OR = operational restructuring, AR = asset restructuring, DT = digital transformation, BSIZE = board size (proxy to corporate governance), SIZE = firm size (log total assets), AGE = firm age.

Table 2 gives descriptive information about all the variables used in the study. It is primarily an analysis of 600 firm-years of different publicly listed firms. The variable corporate restructuring (CR) has a mean value of -0.001, a standard deviation of 1.027, and a range of -4.213 to 16.426, which implies significant variation in the restructuring activities of the firms within the sample. The standard deviation of financial restructuring (FR) is also relatively high (23.53), which indicates that the rating varies significantly across the firms because the values vary between 0.009 and 560.97, with an average of 3.13.

The mean of governance restructuring (GR) is 14.36, with the minimum value of 0 and the maximum of 71.42. However, operational restructuring (OR) remains erratic within the range of -844.51 to 880.86. This unrealistically large dispersion (Std. Dev. = 64.99) is indicative of significant changes at the operational level of certain companies. The dispersion of asset restructuring (AR) is also extreme (Std. Dev. = 6190.43), within the range of -99.87 to 151,646.10. Such large deviations in the standard deviation between OR and AR indicate extreme cases of restructuring which can be linked to either a major impact of economic shocks or strategic changes (Klein, 2020).

The average of digital transformation (DT) is 1.44, within the range of 0 to 6.13, indicating that the firms have different levels of digital maturity. Board size (BSIZE) has an average value of 7.96, varying between 3 and 18, acting as a proxy of corporate governance. This is an indication of medium board size variance in firms. The natural logarithm of total assets (SIZE), used as the measure of firm size, has an average value of 18.83 with a standard deviation of 3.46, indicating a large variation in the size of firms. The mean firm age (AGE) is 48.29 years, with a minimum of 17 and a maximum of 137 years, thus indicating a large variation among firms in terms of their maturity within the sample.

Such descriptive findings are consistent with past studies which proposed that the characteristics of firms, such as age in years, size in terms of sales, and governance structure present significant effects on the decision of restructuring and strategic transformation (Bergh et al., 2021; Nguyen & Nguyen, 2020)

Table 3 Pairwise Correlation Matrix and the Variance Inflation Factor (VIF)|

Variables |

CR |

FR |

GR |

OR |

AR |

DT |

BSIZE |

SIZE |

AGE |

VIF |

|---|---|---|---|---|---|---|---|---|---|---|

|

CR |

1 |

|

|

|

|

|

|

|

|

|

|

FR |

0.18 |

1 |

|

|

|

|

|

|

|

|

|

GR |

-0.73 |

-0.01 |

1 |

|

|

|

|

|

|

|

|

OR |

0.25 |

-0.001 |

-0.02 |

1 |

|

|

|

|

|

|

|

AR |

0.65 |

-0.003 |

-0.05 |

0.0002 |

1 |

|

|

|

|

|

|

DT |

0.13 |

0.05 |

-0.18 |

-0.07 |

0.01 |

1 |

|

|

|

1.03 |

|

BSIZE |

0.06 |

0.02 |

-0.11 |

-0.01 |

-0.02 |

0.18 |

1 |

|

|

|

|

SIZE |

0.10 |

0.04 |

-0.16 |

0.01 |

-0.03 |

0.18 |

0.17 |

1 |

|

1.04 |

|

AGE |

-0.11 |

0.04 |

0.20 |

-0.02 |

0.04 |

0.02 |

0.06 |

-0.10 |

1 |

1.01 |

Note. CR = corporate restructuring, FR = financial restructuring, GR = governance restructuring, OR = operational restructuring, AR = asset restructuring, DT = digital transformation, BSIZE = board size (proxy to corporate governance), SIZE = firm size (log total assets), AGE = firm age, VIF = variance inflation factor.

Table 3 shows the results of Pearson pairwise matrix and Variance Inflation Factor (VIF). These tests were used to check the magnitude of multicollinearity. The correlation results show the strongest correlation between CR and GR, as their value is -0.7305, indicating an inverse relationship. Nonetheless, the correlation coefficients are all below the 0.80 mark, which alleviates the issue of multicollinearity (Gujarati & Porter, 2009). Moreover, the values of VIF are between 1.01 and 1.04 and very much below the critical value of 10, thus reaffirming the lack of multicollinearity between the independent variables of the study (García et al., 2015).

These results confirm the adequacy of data for regression analysis and show that corporate restructuring can be statistically related to several firm-level figures, including asset structure (r = 0.6539), operational restructuring (r = 0.2488), and digital transformation (r = 0.1276). These findings also indicate that there is a low yet negative relationship with AGE (r = -0.1108) and GR (r = -0.7305), showing that younger firms are more prone to the execution of strategic restructuring initiatives (Datta et al., 2010).

Table 4

Modified Wooldridge Test Results

| Variable | Model | p-Value | F-Test | Wooldridge Test for Autocorrelation |

|---|---|---|---|---|

| CR | Model 1 | 0 | 18.365 | ✔ |

| FR | Model 2 | 0 | 113.64 | ✔ |

| AR | Model 3 | 0 | 4.33E+06 | ✔ |

| GR | Model 4 | 0 | 76.316 | ✔ |

| OR | Model 5 | 0.2246 | 1.493 | ✖ |

| CR | Model 6 | 0 | 18.284 | ✔ |

| FR | Model 7 | 0 | 72.098 | ✔ |

| AR | Model 8 | 0 | 4.25E+06 | ✔ |

| GR | Model 9 | 0 | 76.441 | ✔ |

| OR | Model 10 | 0.2273 | 1.476 | ✖ |

Note. CR = corporate restructuring, FR = financial restructuring, GR = governance restructuring, OR = operational restructuring, AR = asset restructuring.

Table 4 gives the periphery of the Modified Wooldridge Test of autocorrelation in ten different models that are linked to various financial performance variables (CR, FR, AR, GR, OR). Wooldridge test is a conventional method of analysis through panel data to identify first-order autocorrelation (Wooldridge, 2002). In the current analysis, autocorrelation is identified in models 1-4 and 6-9, as indicated by the p-values of 0.000 and corresponding high F-statistics (e.g., F = 4.33E+06 for Model 3 and F = 76.441 for Model 9). This consistent detection of autocorrelation across these models suggests the presence of serial autocorrelation, which violates classical regression assumptions and may lead to biased and inefficient estimators, if not corrected (Baltagi, 2005).

However, models 5 and 10, both associated with OR, show p-values above 0.05 (0.2246 and 0.2273, respectively), suggesting no significant autocorrelation. These results align partially with the base paper’s claim that "no autocorrelation exists in our models except for Models 2 and 6," although the findings indicate a broader presence of autocorrelation across multiple models. This discrepancy might be due to model specification differences or the inclusion of different time frames or variable interactions in the study.

Wooldridge (2002) emphasized the importance of testing for autocorrelation in panel data models, especially when using fixed-effects estimators. Baltagi (2005) explained that ignoring autocorrelation can lead to underestimated standard errors and misleading inference in panel data.

Table 5 Modified War Test Results| Variable | Model | p-Value | χ² (Scientific Notation) | Modified Wald Test of Heteroskedasticity |

|---|---|---|---|---|

| CR | Model 1 | 0 | 4.92E+08 | ✔ |

| FR | Model 2 | 0 | 3.69E+12 | ✔ |

| AR | Model 3 | 0 | 7.40E+10 | ✔ |

| GR | Model 4 | 0 | 7.44E+08 | ✔ |

| OR | Model 5 | 0 | 7.58E+08 | ✔ |

| CR | Model 6 | 0 | 1.02E+08 | ✔ |

| FR | Model 7 | 0 | 4.70E+12 | ✔ |

| AR | Model 8 | 0 | 1.01E+10 | ✔ |

| GR | Model 9 | 0 | 3.29E+07 | ✔ |

| OR | Model 10 | 0 | 8.47E+08 | ✔ |

Note. CR = corporate restructuring, FR = financial restructuring, GR = governance restructuring, OR = operational restructuring, AR = asset restructuring.

Table 5 summarizes the Modified Wald test results of group-wise heteroskedasticity in fixed-effects panel data models. All models capture significantly high p-values (0.000) and notably high significant two (2) values in the scientific notation (e.g., 4.70E+12 in Model 7 and 7.40E+10 in Model 3), indicating the existence of heteroskedasticity in all ten models. These results imply that the error terms variance is not constant across entities, as stated in the fundamental tenets of the classical linear regression model. Heteroskedasticity may result in inefficient estimates of the coefficients and give unreliable standard errors, leading to wrong hypothesis testing (Greene, 2012).

The results confirm that there is heteroskedasticity problem in our model. This, in turn, requires the use of robust standard errors/generalized least squares (GLS) to rectify this situation and enhance the reliability of the findings. According to Greene (2012), heteroskedasticity is a rising problem in panel data and especially in the financial data set. It should be solved in the form of standard heticoskedasticity-consistent standard errors. According to Drukker (2003), the Modified Wald test is useful in examining whether there is group-wise heteroskedasticity in fixed-effects models, which provides support to the credibility of this type of analysis in the current study.

Table 6

Impact of Corporate Governance and Digital Transformation on Corporate Restructuring

|

Variables |

Model 1 (CR) |

Model 2 (FR) |

Model 3 (GR) |

Model 4 (OR) |

Model 5 (AR) |

|---|---|---|---|---|---|

|

DT |

0.063** |

0.286*** |

0.014 |

0.032 |

-0.02 |

|

BSIZE |

-0.029 |

-0.059 |

0.119 |

-0.043 |

0.001** |

|

SIZE |

-0.061 |

0.016 |

-0.164* |

0.054 |

0.015*** |

|

AGE |

-0.336*** |

-0.006 |

-0.014 |

0.177** |

0.005*** |

|

_cons |

-0.088 |

-0.032 |

0.120** |

0.02 |

-0.056*** |

|

Wald chi2 |

309.460*** |

834.640*** |

50.600*** |

64.28*** |

3.720*** |

|

Sargan |

0.483 |

0.03 |

0.769 |

0.605 |

0.002 |

|

AR(2) test |

0.772 |

0.177 |

0.419 |

0.165 |

0.112 |

Note. DT = digital transformation, BSIZE = board size (proxy to corporate governance), SIZE = firm size (log total assets), AGE = firm age, AR = asset restructuring.

*, ** and *** are noted to be significant at 10, 5 and 1%, respectively

CR indicates a restructuring of the corporation; FR indicates a restructuring of the finances; GR indicates a restructuring of the governance; OR indicates a restructuring of the operations; DT indicates digital transformation; BSIZE indicates the corporate governance; SIZE indicates the natural logarithm of the total assets and AGE indicates firm age

Table 6 shows the output of five regressions to examine the influence of digital transformation (DT), board size (BSIZE), and firm-wise controls (SIZE and AGE) on different types of corporate restructuring. Model estimation is done by employing the Generalized Method of Moments (GMM) and the quality of the results is confirmed by the significant values of Wald chi-square, as well as acceptable results of the Sargan and AR(2) tests. The results imply that there are no problematical aspects of instrument invalidity and second-order autocorrelation.

For Model 1, which describes the overall corporate restructuring (CR), the coefficient of digital transformation is positive and statistically significant (0.063), implying that digital efforts make noteworthy contributions to corporate restructuring efforts. The effect can be amplified further in Model 2 which deals with financial restructuring (FR), whereby the value of digital transformation (DT) remains significantly positive (0.286). The results lead to the speculation that digital transformation alleviates financial restructuring, which can be done in the shadow of improved access to financial data, automated processes, and the increased ability to make decisions. These results align with other the results of another research work, such as Liu et al. (2023) and Tran et al. (2024). They also reinforced that firms which engage in digital technology are in a more advantageous state of reorganizing their financial systems.

Model 3 and Model 4 focus on governance-related restructuring (GR) and operational restructuring (OR), whereas the DT coefficients turn out to be positive (positive but not significant, 0.014 and 0.032, respectively). This indicates that despite the hype that can be associated with the improvement of governance or operations through the use of digital tools, there is no real data to indicate that there is a major impact. For Model 5 which focuses on asset restructuring (AR), DT has a weak and statistically insignificant relationship (=0.02). This suggests that digitalization does not have a direct connection to the transformation of the physical asset portfolio of companies. This could be because priority keeps changing from physical to intangible assets, such as platforms, data infrastructure, and software, during digital transformation.

The effects of corporate governance, quantified by board size (BSIZE), also remain inconsistent. For Model 1 (CR) and Model 2 (FR), the coefficient of BSIZE assumes negative and statistically insignificant values (-0.029 and -0.059, respectively), which implies an undefined association between board size and an overall financial restructuring. Model 3 (GR) yields a positive but insignificant coefficient (0.119), suggesting a weak association between larger boards and governance-related restructuring. Model 4 (OR) again reports a negative and insignificant relationship (-0.043). It is worth noting that BSIZE exhibits a positive and significant coefficient (0.001) for Model 5 (AR). Hence, there is the likelihood that a greater numerosity of the board leads to an increased chance of asset restructuring. This may be attributable to an increased variety of skills and with the expanded capacity to provide oversight, which increases the ability of firms to evaluate and rearrange their asset base. This fact is consistent with the results of Adams and Mehran (2012), who contend that the effect of governance structures is different with respect to the types of strategic decisions.

Such results are aligned with those achieved by Tran et al. (2024), reflecting the influence of corporate governance on the relationship between digital transformation and corporate restructuring of Vietnamese listed companies. They inferred that their independence of effect is not always high. However, their can be a powerful influence exerted through alignment and integration between digital transformation and governance structures, which can lead to greater success of restructuring initiatives. Tran et al. (2024) leveraged board size as the major proxy of governance and adopted a close GMM analysis in an 11-year sample, hence restating the methodological and empirical correlation with the one employed in this study.

There is also the variance in the influence of control variables. Model 3 indicates the significant negative effect (- 0.164) of firm size (SIZE), which implies that larger firms could be more inflexible concerning the restructuring of governance. On the other hand, SIZE takes a positive and extremely important effect (0.015) in Model 5. This implies that a bigger firm can be more efficient in asset restructuring. Firm age (AGE) is strongly and negatively correlated with overall restructuring (-0.336) in Model 1, while positively and statistically significant operational (0.177) and asset restructurings (0.005) are correlated in Model 4 and Model 5, respectively.

These findings indicate that although older companies have been reluctant to large-scale restructuring, there is value in their experience in initiating operational and asset-level changes.

The findings are to some extent in line with the hypothesis that digital transformation and board size determine corporate restructuring. The effects of digital transformation are particularly significant for financial restructuring, whereas board size appears to be significant only in asset restructuring. These results highlight that digital transformation and governance effectiveness are context-specific and differ on the basis of restructuring type.

Table 7

Moderating Role of Corporate Governance in the Relationship between Digital Transformation and Corporate Restructuring

|

Variables |

Model 6 (CR) |

Model 7 (FR) |

Model 8 (GR) |

Model 9 (OR) |

Model 10 (AR) |

|---|---|---|---|---|---|

|

DT |

0.055 |

0.820*** |

0.274** |

0.072 |

0.02 |

|

BSIZE |

-0.031 |

0.204** |

0.178 |

-0.023 |

0.001* |

|

DT × CG |

0.02 |

-0.040*** |

-0.019*** |

-0.004 |

0.02 |

|

SIZE |

-0.066 |

-0.001 |

-0.205** |

0.018 |

0.015*** |

|

AGE |

-0.336*** |

-0.045 |

-0.057 |

0.179** |

0.005*** |

|

_cons |

-0.093 |

0.451** |

0.346*** |

0.071 |

-0.06*** |

|

Wald chi2 |

309.790*** |

599.220*** |

53.810*** |

63.600*** |

3.750*** |

|

Sargan |

0.484 |

0.036 |

0.695 |

0.661 |

0.002 |

|

AR(2) test |

0.769 |

0.19 |

0.337 |

0.193 |

0.108 |

Note. DT = digital transformation, BSIZE = board size (proxy to corporate governance), CG = corporate governance, SIZE = firm size (log total assets), AGE = firm age, AR = asset restructuring.

*, ** and *** are significant 10, 5 and 1 percent, respectively

Table 7 reports the regression estimates of models 6-10 that test whether corporate governance (CG) moderates the impact of digital transformation (DT) on various kinds of corporate restructuring (CR). The interactions (as the variable of interest) include any term multiplied by DT and CG (the main effect) to show the effect of corporate governance on the relationship between digital transformation and restructuring outcome. The interaction term in Model 6 (CR), that is, overall corporate restructuring has a weak and insignificant positive coefficient (0.02), implying that there is no significant moderating influence. Although DT has a positive coefficient (0.055 on its own), it is also insignificant; therefore, it implies that neither digital transformation or its interrelationship with governance has a significant impact on total restructuring. The results correlate with those of Tran et al. (2024), who claimed that with developing markets, governance systems might not necessarily amplify the advantages of digitalization on account of institutional or cultural constraints.

Model 7 (FR), which is concerned with financial restructuring, indicates the effect of DT as very strong, highly significant, and positive (0.820***), thus highlighting the transformative role of digital tools in reshaping financial strategies. However, the interaction term DT × CG remains negative and highly significant (– 0.040***), suggesting that stronger corporate governance reduces this positive effect. This could imply that well-governed firms exercise more caution in financial restructuring during digital transition, possibly to mitigate risk (Magnusson et al., 2022).

Model 8 (GR), concerning the redesign of governance structure, indicates a positive and significant DT effect (0.274), but with negative and significant interaction (--0.019). This indicates that profits gained by the firms with existing good governance systems could be characterized by less-intense marginal benefits of digital restructuring programs. In models 9 (OR) and 10 (AR), which focus on operational and asset restructuring, the interaction terms remain less insignificant (-0.004, 0.02), hence show no moderating effect of governance. Model 10, where governance variable (BSIZE) remains statistically significant at 10% (0.001) level, indicates an insignificant direct effect on the decision to restructure assets, which is consistent with the findings of Adams and Mehran (2012).

The coefficients of the Wald chi-square statistics are significant in all models and indeed represent good model fit. The results of Sargan and AR(2) suggest the reliability of the instruments and estimations with the exception of a low p-value in Model 7 and Model 10 (0.036 and 0.002) that should be interpreted with caution. All in all, these results indicate a non-trivial and, at times, limiting role of corporate governance in mediating the effect of digital transformation, especially on financial and governance outcomes, akin to the findings of Tran et al. (2024).

Discussion

This study aimed to examine the linked functionalities of digital transformation (DT) and corporate governance (CG) (board size [BSIZE]) in leading to corporate restructuring (CR) in Shariah-compliant firms in Pakistan. The empirical results presented are framed by reference to the Knowledge-Based View (KBV) which emphasizes the role of knowledge assets as a strategic capability that can indeed facilitate the process of organizational renewal and restructuring (Grant, 1996).

Hypothesis (H1) which suggests the positive role of digital transformation in the restructuring of corporations is highly supported in technological and financial restructuring (TR, FR), where its effect remains huge and statistically significant. It conforms to the results of Liu et al. (2023) and Tran et al. (2024), which proved that digital technologies can increase the levels of transparency, operational efficiency, and access to capital, which are the main drivers of financial restructuring. Digital dashboards, automated reporting, and integrated financial platforms allow Shariah-compliant companies to redesign their capital base as long as they stay within Islamic financial conventions.

The impact of DT on other forms of restructuring, such as governance restructuring (GR), operational restructuring (OR), and asset restructuring (AR) is less pronounced, with coefficients which are statistically insignificant. This finding indicates that digital maturity does not necessarily lead to wider organizational change despite the contribution it makes to financial agility. Therefore, it requires the additional effects of matching organizational strategies of change, as well as being instilled within the institution. Another point highlighted in catalyzing digital transformation in previous studies is that it should be incorporated into the strategic purpose and culture of the firm to achieve extensive restructuring. This may be especially prevalent in a scenario where ethical requirements and religious conformity can impede rapid radical adjustment as is seen in Shariah-compliant firms.

Hypothesis (H2) is based on assumptions that corporate governance positively influences corporate restructuring; collectively, the construct shows partial support. The size of board, perhaps due to large boards having a given prerogative to consider and oversee divestment and acquisition of assets, can be an important factor in asset restructuring (AR). This is in line with the observation made by Adams and Mehran (2012) that large boards with extensive expertise are in a better place to support complex decisions (e.g., reconfiguring the asset base). Although in the rest of the restructuring dimensions (FR, GR, OR, and CR), the size factor does not carry significance at the statistical level, indicating that a large board, by itself, may not be enough to lead to any strategic transformation. This creates apprehensions when phony governance is present in emerging markets, where formal governance structures are likely to be in existence without making any real impact on strategic decisions (Judge et al., 2008). Moreover, since in the Islamic environment the supervisory role of Shariah Supervisory Board (SSB) coexists with the role of traditional boards. This can result in dispersal of authority and a reduction in the importance of board size as a sole indicator of governance (Aribi & Gao, 2010; Haniffa & Hudaib, 2007).

The third hypothesis (H3), which examines whether corporate restructuring moderated by corporate governance—within the context of digital transformation—holds empirical validity, is only partially supported. The two negative and significant coefficients associated with interaction terms indicate that, instead of amplifying the positive impact of digital transformation, robust governance structures may in fact constrain it. This paradoxical finding is supported by the fact presented by Magnusson et al. (2022) that governance systems in emerging markets may serve as a sort of a double-edged sword. Although it serves to increase responsibility and control, the extra-hardline or tradition-based boards can hamper radical restructuring decisions supported by digital innovation. This can be even more evident in Shariah-compliant companies where the corporate governance of such firms has to reconcile innovation and ethical and religious limitations. Further, OR and AR lack substantial moderating effects which implies that, in more technical or asset-intensive restructuring areas, digital strategy and board governance are less interconnected.

Notably, the Islamic approach to governance provides more details as to the nature of such mixed outcomes. The incentive of the Shariah-compliant firms cannot be limited to profitability or effectiveness, since they must also correspond with maqasid al-shariah, that is, the goals of Islamic law. This makes loyalty, fairness, and the common good be at the top of the list of priorities. These governance dynamics might not be best captured using the traditional proxy to board size. Under dual forms of governance, corporate boards and SSBs co-exist and need to make decisions in parallel. Consequently, digital restructuring efforts can be slow or diluted by their modes of decision-making. As per the arguments by Haniffa and Hudaib (2007), the discourse of Islamic governance ought to be viewed as both procedural and ethical. The independence, financial expertise, and regularity of SSB meetings should also be included in future studies to obtain a more comprehensive view of Islamic firm governance.

To ensure that innovation remains consistent with Shariah values, Islamic governance concepts must be included into Islamic financial systems, especially in light of the growth of fintech and digital transformation. The management of financial institutions and resources should be guided by Islamic governance, which emphasizes accountability, openness, moral behavior, and rigorous adherence to the Shariah (Ihsan & Ayedh, 2015). Stakeholder trust, social responsibility, and sustainable sector growth can be fostered by integrating strong governance frameworks into these digital platforms to help balance technology advancement with Shariah principles. In order to demonstrate how Shariah oversight can be successfully operationalized in a quickly changing digital financial landscape, future research could examine more useful governance mechanisms for AI-driven financial services, blockchain-based transactions, and smart contracts (Ihsan & Ayedh, 2015; Nawi, 2025).

ConclusionA substantial and consequential argument of this paper dwells on how digital transformation and corporate governance relate to each other in influencing the corporate restructuring of Shariah-compliant firms listed at the Pakistan Stock Exchange (PSX). Using a strong two-step system GMM estimation and imbibing KBV to provide the theoretical perspective, the research makes important observations.

First, digital transformation emerges as a critical driver of corporate restructuring, particularly financial restructuring, confirming that digital capabilities enable firms to reconfigure capital and financing arrangements more effectively. This supports the KBV proposition, which posits that knowledge assets, such as digital tools and data infrastructures, enhance organizational adaptability by facilitating the reconfiguration of resources to meet the changing market conditions (Grant, 1996).

Second, corporate governance, measured through board size, plays a limited yet targeted role. Its significance in asset restructuring underscores that governance influence may be contingent on the complexity and risk associated with the restructuring type. However, its insignificance in other aspects begs the question of the success of the current governance framework in Shariah-compliant companies.

Third, the moderating role of governance reveals a complex dynamic. Rather than enhancing the benefits of digital transformation, governance appears to constrain it in key areas, particularly financial and governance restructuring. This suggests a potential misalignment between digital and governance strategies, possibly rooted in the tension between innovation and religious compliance.

ContributionsThese findings make several notable contributions. Theoretically, the study extends the KBV into Islamic corporate settings, highlighting that digital assets can drive restructuring but are moderated by culturally and religiously embedded governance frameworks. It also adds to the body of research on Islamic corporate governance by demonstrating that the conventional indicators might not be enough, since scholars should consider including variables such as SSB presence or the application of the Islamic ethical standards.

Empirically, the study provides large-sample evidence from an under-researched context, namely Shariah-compliant firms in Pakistan. It introduces a novel content analysis method to measure digital transformation based on annual report narratives. This method involves a systematic analysis of the language used in these reports to identify digital initiatives and their impact on firm operations. This approach offers a replicable model for future research in Islamic and emerging markets.

Furthermore, managerial and policy implications of the study remain unambiguous and provide the audience with practical information. To advise ethically sound restructuring, boards should be reconstituted to include members who have both digital and Islamic financial literacy. Regulatory authorities like Securities and Exchange Commission of Pakistan (SECP) need to provide guidelines exclusive to digital government in Islamic institutions. Also, companies need to coordinate digitalisation according to the principles of maqasid al-Shariah to make the change not only effective but also ethical and socially conscious.

To conclude, digital transformation holds great promise for revitalizing Shariah-compliant firms, offering a beacon of hope for the future. However, this potential can only be realized when governance systems are appropriately aligned, both technically and ethically, with the firms’ strategic vision.

Author Contribution

Abida Irum: Data curation, Formal analysis, Writing – original draft. Rafiullah Sheikh: Conceptualization, Supervision, Writing – review & editing

Conflict of Interest

The authors of the manuscript have no financial or non-financial conflict of interest in the subject matter or materials discussed in this manuscript.

Data Availability Statement

Data supporting the findings of this study will be made available by the corresponding author upon request.

Funding Details

No funding has been received for this research.

Generative AI Disclosure Statement

The authors did not used any type of generative artificial intelligence software for this research.

REFERENCES

Adams, R. B., & Mehran, H. (2012). Bank board structure and performance: Evidence for large bank holding companies. Journal of Financial Intermediation, 21(2), 243–267. https://doi.org/10.1016/j.jfi.2011.09.002

Arellano, M., & Bover, O. (1995). Another look at the instrumental variable estimation of error-components models. Journal of Econometrics, 68(1), 29–51. https://doi.org/10.1016/0304-4076(94)01642-D

Aribi, Z. A., & Gao, S. S. (2010). Corporate social responsibility disclosure: A comparison between Islamic and conventional financial institutions. Journal of Financial Reporting and Accounting, 8(2), 72–91. https://doi.org/10.1108/19852511011088352

Baltagi, B. H. (2005). Econometric analysis of panel data (3rd ed.). Wiley.

Bellucci, M., Marzi, G., Orlando, B., & Papa, A. (2023). Dynamic capabilities and digital transformation: A systematic literature review. Journal of Business Research, 158, Article e113603.

Benson, V., Filippaios, F., & Morgan, S. (2021). Digital transformation and corporate governance: A systematic literature review. Information Systems Frontiers, 23, 1029–1049. https://doi.org/10.1007/s10796-020-10011-6

Bergh, D. D., Sharp, B. M., Aguinis, H., & Li, M. (2021). Is there a credibility crisis in strategic management research? Evidence on the reproducibility of empirical results. Strategic Organization, 19(3), 472–489. https://doi.org/10.1177/1476127020952406

Bharadwaj, A., El Sawy, O. A., Pavlou, P. A., & Venkatraman, N. (2013). Digital business strategy: Toward a next generation of insights. MIS Quarterly, 37(2), 471–482. https://doi.org/10.25300/MISQ/2013/37:2.3

Blundell, R., & Bond, S. (1998). Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics, 87(1), 115–143. https://doi.org/10.1016/S0304-4076(98)00009-8

Cruz-García, D., López-Torres, L., & Ramón-Llorens, M. C. (2020). Digital transformation and restructuring: Challenges in emerging economies. Technological Forecasting and Social Change, 157, Article e120105.

Desky, H., & Maulina, I. (2022). Digital transformation in Islamic banking. International Journal of Multidisciplinary Research and Analysis, 5(12), 3616–3622.

Datta, D. K., Guthrie, J. P., Basuil, D., & Pandey, A. (2010). Causes and effects of employee downsizing: A review and synthesis. Journal of Management, 36(1), 281–348. https://doi.org/10.1177/0149206309346735

Dery, K., Sebastian, I. M., & van der Meulen, N. (2017). The digital workplace is key to digital innovation. MIS Quarterly Executive, 16(2), 135–152.

Devadoss, P., & Pan, S. L. (2007). Enterprise systems use: Towards a structurational analysis of enterprise systems-induced organizational transformation. Communications of the Association for Information Systems, 19, 352–376. https://doi.org/10.17705/1CAIS.01917

Drukker, D. M. (2003). Testing for serial correlation in linear panel-data models. Stata Journal, 3(2), 168–177. https://doi.org/10.1177/1536867X0300300206

Fahndrich, R. (2022). Corporate governance and digital transformation: A balancing act. Journal of Business Research, 144, 203–214.

Fitzgerald, M., Kruschwitz, N., Bonnet, D., & Welch, M. (2014). Embracing digital technology: A new strategic imperative. MIT Sloan Management Review, 55(2), 1–12.

García, F., García-Olalla, M., & García-Sánchez, I.-M. (2015). CEO duality and firm performance: A study from a legal perspective. BRQ Business Research Quarterly, 18(4), 206–217.

Goodstein, J., Gautam, K., & Boeker, W. (1994). The effects of board size and diversity on strategic change. Strategic Management Journal, 15(3), 241–250. https://doi.org/10.1002/smj.4250150305

Grant, R. M. (1996). Toward a knowledge-based theory of the firm. Strategic Management Journal, 17(S2), 109–122. https://doi.org/10.1002/smj.4250171110

Greene, W. H. (2012). Econometric analysis (7th ed.). Pearson.

Gujarati, D. N., & Porter, D. C. (2009). Basic econometrics (5th ed.). McGraw-Hill/Irwin.

Hanelt, A., Bohnsack, R., Marz, D., & Marante, C. A. (2021). A systematic review of the literature on digital transformation: Insights and implications for strategy and organizational change. Journal of Management Studies, 58(5), 1159–1197. https://doi.org/10.1111/joms.12639

Haniffa, R., & Hudaib, M. (2007). Exploring the ethical identity of Islamic banks via communication in annual reports. Journal of Business Ethics, 76, 97–116. https://doi.org/10.1007/s10551-006-9272-5

Hautz, J., Seidl, D., & Whittington, R. (2017). Open strategy: Dimensions, dilemmas, dynamics. Long Range Planning, 50(3), 298–309. https://doi.org/10.1016/j.lrp.2016.12.001

Hoskisson, R. E., Johnson, R. A., & Moesel, D. D. (2002). Corporate divestiture intensity in restructuring firms: Effects of governance, strategy, and performance. Academy of Management Journal, 45(6), 1207–1221. https://doi.org/10.5465/256671

Ihsan, H., & Ayedh, A. (2015). A proposed framework of Islamic governance for awqaf. Journal of Islamic Economics, Banking and Finance, 11(2), 117–133.

Judge, W. Q., Douglas, T. J., & Kutan, A. M. (2008). Institutional antecedents of corporate governance legitimacy. Journal of Management, 34(4), 765–785. https://doi.org/10.1177/0149206308318615

Kane, G. C., Palmer, D., Phillips, A. N., Kiron, D., & Buckley, N. (2015). Strategy, not technology, drives digital transformation. MIT Sloan Management Review, 14, 1–25.

Khan, M. T. I., Khan, F., & Zubair, S. S. (2020). Corporate governance and firm performance: Evidence from Shariah-compliant firms in Pakistan. Cogent Business & Management, 7(1), Article e1771074. https://doi.org/10.1080/23311975.2020.1771074

Klein, P. G. (2020). Organizing for innovation: Conceptual and empirical perspectives on corporate restructuring and technological change. Academy of Management Perspectives, 34(3), 396–411. https://doi.org/10.5465/amp.2018.0150

Kraft, C., Söllner, M., & Leimeister, J. M. (2022). Digital transformation of organizations: Literature review and research agenda. Journal of Strategic Information Systems, 31(1), Article e101694. https://doi.org/10.1016/j.jsis.2022.101694

Laksono, S., Yuliana, R., & Harahap, D. (2025). Digital transformation in the Islamic economy: Innovations and challenges in 2025. Journal of Islamic Finance and Technology, 32(2), 145–167. https://doi.org/10.1016/j.jift.2025.02.003

Li, J., & Zhao, X. (2023). Digital transformation and firm restructuring: Evidence from emerging markets. Technological Forecasting and Social Change, 190, Article e122349.

Liu, Y., Luo, Z., & Wang, H. (2023). Digital transformation and firm restructuring: Evidence from China's listed firms. Technological Forecasting and Social Change, 191, Article e122481.

Lorenz, A., & Buchwald, A. (2023). Governance as a driver of digital transformation. Long Range Planning, 56(2), Article e102153.

Magnusson, J., Koutsikouri, D., & Stahlbrost, A. (2022). Digital transformation in public sector organizations: The role of structural inertia. Government Information Quarterly, 39(2), Article e101667.

Metwally, M. M. (1996). The behavior of Islamic banks as interpreted by the theory of the firm. Managerial Finance, 22(5), 1–12. https://doi.org/10.1108/eb018558

Nawi, N. A. M. (2025). Islamic fintech and digital transformation: Opportunities and Shariah governance challenges. Progress in Islamic Banking and Finance, 2(1), 32–56.

Nguyen, P. T., & Nguyen, T. T. (2020). Corporate governance, digital transformation, and firm performance: Evidence from Vietnam. Asian Economic and Financial Review, 10(2), 224–239. https://doi.org/10.18488/journal.aefr.2020.102.224.239

Riaz, Z., Shahid, H., & Abbas, A. (2022). The role of board characteristics in shaping corporate restructuring strategies: Evidence from Pakistan. Corporate Governance: The International Journal of Business in Society, 22(4), 785–801.

Roberts, C. W. (1997). A generic semantic grammar for quantitative text analysis: Applications to East and West Berlin radio news content from 1979. Sociological Methodology, 27(1), 89–129. https://doi.org/10.1111/1467-9531.271020

Rottner, R. M., Hargadon, A., & Kim, B. (2019). Institutional uncertainty and the durability of organization innovations. Academy of Management Journal, 62(4), 1010–1035.

Schwertner, K. (2017). Digital transformation of business. Trakia Journal of Sciences, 15(1), 388–393.

Tran, N. P., Le, Q. T., & Vo, A. T. (2024). Digital transformation and corporate restructuring: Does corporate governance matter? International Journal of Business and Economics Studies, 31(2), 115–130. https://doi.org/10.1080/23234845.2024.0575281

Tricker, B. (2015). Corporate governance: Principles, policies, and practices (3rd ed.). Oxford University Press.

Unerman, J. (2000). Methodological issues‐Reflections on quantification in corporate social reporting content analysis. Accounting, Auditing & Accountability Journal, 13(5), 667–681. https://doi.org/10.1108/09513570010353756

Verhoef, P. C., Broekhuizen, T., Bart, Y., Bhattacharya, A., & Dong, J. Q. (2021). Digital transformation: A multidisciplinary reflection and research agenda. Journal of Business Research, 122, 889–901.

Vinocur, J., Lopes, A. P., & Maia, J. (2023). Knowledge integration capabilities and digital transformation: A dynamic capabilities perspective. Journal of Knowledge Management, 27(2), 316–333.

Wati, M. F., Nurul, L. R., & Putra, A. F. (2024). Digital transformation in Islamic financial institutions with challenges and opportunities for Sharia-compliant accounting systems. International Journal of Islamic Accounting and Business Research, 13(1), 98–112. https://doi.org/10.1108/IJIABR-04-2024-0020

Windmeijer, F. (2005). A finite sample correction for the variance of linear efficient two-step GMM estimators. Journal of Econometrics, 126(1), 25–51. https://doi.org/10.1016/j.jeconom.2004.02.005

Wooldridge, J. M. (2002). Econometric analysis of cross section and panel data. MIT Press.

Zhao, Y., Xue, L., & Zhang, C. (2022). Digital transformation and organizational change: A review and future research directions. Information & Management, 59(5), Article e103592. https://doi.org/10.1016/j.im.2022.103592

Zollo, M., & Winter, S. G. (2002). Deliberate learning and the evolution of dynamic capabilities. Organization Science, 13(3), 339–351.