| Review | Open Access |

|---|

Application of the Extended Theory of Planned Behavior on Muslims Intentions: Case of Islamic Banking in Spain |

|

|---|

![]() Muhammad Musa* ,

Muhammad Musa* ,

![]() Rusni Bt Hassan , and

Rusni Bt Hassan , and

![]() Nur Harena Binti Redzuan

Nur Harena Binti Redzuan

Institute of Islamic Banking and Finance, International Islamic University, Malaysia

Spain has seen a significant rise in the presence of Islam in the recent years, largely attributed to increased immigration from Muslim-majority countries to Europe. This demographic shift positions Spain as a potential emerging market for Islamic banking and finance (IBF). Hence, it is relatable to examine the perceptions of Muslims towards Islamic banking systems. This study aims to examine the determinants influencing Muslims' intentions towards Islamic banking in Spain. Using the Theory of Planned Behaviour (TPB), the study investigates the relationship between attitude, subjective norms, perceived behavioral control (PBC), awareness and knowledge, religiosity, service quality, and intention of Muslims to use Islamic banking. The study employed a 36-item structured survey instrument to gather data from 300 Muslim respondents residing in Catalonia, Spain. Descriptive statistics, reliability and validity analysis, and PLS-SEM technique was applied to test the hypothesized relationship among the variables. Smart PLS was used to analyze the data. The study finds that attitude, subjective norms, PBC, awareness and knowledge, and service quality have a significant impact on the intention to use Islamic banking products and services among Muslims. Furthermore, the study also asserted that religiosity did not demonstrate a statistically significant influence on behavioral intention. This research contributes to the growing body of Islamic behavioral finance literature by providing evidence from a non-Muslim-majority context. It offers novel insights into how Muslim minorities make financial decisions, and identifies key predictors that Islamic banks should target to enhance service adoption in Spain. The findings suggest that Islamic banking institutions can expand their outreach in Spain by focusing on customer-centric strategies that enhance awareness, highlight service quality, and leverage social influence.

1. INTRODUCTION

Islamic banking and finance (IBF) industry performance can be measured through five sectors, namely Islamic banks, Islamic funds, sukuk, Islamic insurance (Takaful), and other Islamic financial institutions (IFIs) such as micro-finance or investment entities (Kaakeh et al., 2018). In the early 1970s, Islamic banking was introduced as a riba (interest-free) alternative to traditional banking (Eyerci, 2021). Over the years, Islamic banking has gained recognition and acknowledgement in many countries; however, conventional banking is still considered well-structured and the principal rival of Islamic banking (Shah, 2025).

Bacha (2024) highlighted that substantial investments, especially through electronic modes, including infrastructure, halal sectors, and sukuk bonds, have resulted in the rapid growth of the global IBF industry. In all of its financial transactions, the conventional (or traditional) banking stream depends primarily on riba (interest) related activities, which are forbidden in Islam (Rasheed et al., 2012). On the contrary, the Islamic banking system is free from riba and functions on principles set by the Shariah (Ibrahim et al., 2017).

The global Islamic banking sector is worth USD 5.47 trillion at year-end 2024-25 (Mordor Intelligence, 2025), and the asset value is expected to reach USD 4.94 trillion in 2025 (Insifr, 2025). Abiola-Adams et al. (2023) highlighted that the IBF industry is expanding because of growing Muslim population, increased demand for Shariah-complaint financial services and a focus on sustainable and ethical investments. Today, Islamic banks are the prominent pillar of the financial sector, and to widen the customer base and attract new customers, it is necessary to explore people's attitudes and behavioural intentions towards the IBF industry (Mustapha et al., 2023).

Islamic banking, primarily, was considered to be a community-oriented initiative that aimed to fulfil Muslims religious obligations (Zafar & Sulaiman, 2022). Over the period, IBF has evolved into a competitive industry which actively seeks to satisfy existing customers and attract potential new customers for building long-term loyalty (Thaidi et al., 2023). Despite the tremendous progress, the IBF industry has not been able to establish a significant presence in Spain. Kaakeh et al. (2018) argued that the IBF industry is still underdeveloped in Spain. Moreover, it is important to note that Muslims constitute about 4-5% of the Spanish population in 2025, which is higher than several countries where robust IBF structures have already been successfully implemented (Bacha, 2024).

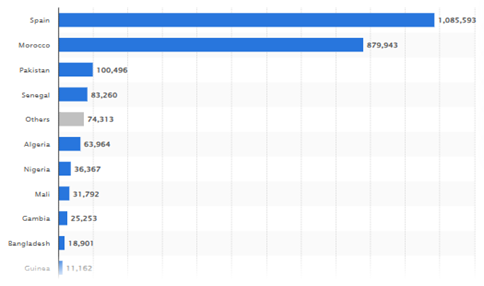

Nonetheless, Spain is a prospective emerging market for IBF due to the demographic shifts. The country has an estimated Muslim population of 2.5 million in 2025 (Bolelli, 2023) which comprises individuals of Spanish (native or naturalised), Moroccan, and Pakistani origin (see Figure 1). The Spanish city, Catalonia, in particular, hosts the largest Muslim community, with over 660,000 Muslim residents, making up around 8 per cent of the region’s total population (Galan, 2025). Keeping this into context, it is timely and pertinent to examine the perceptions of Muslims towards IBF products and services.

Figure 1

Muslim Population in Spain, by Nationality (for 2023)

Note. Source: Galan (2025)

This study points out and determines the factors that may influence Muslim's intention to use Islamic banking in Spain by applying the Theory of Planned Behavior (TPB). It is expected that this study can be a critical theoretical contribution. This research investigates the impact of attitude, subjective norms, perceived behavioral control (PBC), religiosity, awareness and knowledge, and service quality on intention to use Islamic banking in Spain.

Problem StatementThe gradual and limited development of the IBF sector in Spain has raised several critical concerns. These include whether the public possesses sufficient awareness regarding products or services offered by IFIs, and, if so, what challenges or barriers are impeding their adoption. Nevertheless, the absence of a comprehensive regulatory framework specifically designed to accommodate Islamic banking, in contrast to the well-established conventional financial system, poses a significant constraint. Therefore, this study determines the perceptions that may influence Muslim's intention to use Islamic banking in Spain.

Research QuestionsThe study addressed the given research questions:

- Does people’s attitude affect their intention towards using Islamic banking?

- Do subjective norms affect people’s intention towards using Islamic banking?

- Does PBC affect people’s intention to use Islamic banking?

- Does religiosity affect people’s intention towards using Islamic banking?

- Do awareness and knowledge level affect people’s intention towards using Islamic banking?

- Does service quality affect people’s intention towards using Islamic banking?

The present study holds substantial relevance for policymakers and regulatory bodies, as it aims to contribute valuable insights to inform the future development and integration of the IBF sector in Spain. This study also supports scholars and researchers keen on conducting further studies in this sector. The study further enables the Islamic banking product development members and decision-makers to identify factors that may support the clients' requirements by comprehending the clients' opinions towards the use of Islamic banking in the context of Spain.

Literature Review

Attitude and Behavioural IntentionIn TPB, the first construct is the attitude towards the behaviour (Ajzen & Fishbein, 2000). Earlier empirical studies have focused on substantial consequences of attitude towards the behavioural intention (Andespa et al., 2024; Basr & Daud, 2020; Baker & White, 2010; Di Pietro & Pantano, 2012; Davis et al., 1989; Dean et al., 2022; Hanafiah & Handin, 2021; Ramasubbian et al., 2018; Ramayah et al., 2016). Besides, many researchers also explored the connectedness between attitude and intention towards using Islamic banking through survey research (Amin et al., 2014; Baber, 2018; Kaakeh et al., 2018; Sabirzyanov, 2016). A study by Kaakeh et al. (2018) examines the factors affecting the 154 Muslim minorities’ intention to use Islamic banking in Spain. The study identified that awareness, attitude and religious motivation are significant predictors among Muslim minorities in Spain. Mustapha et al. (2023) found that attitude has no significant influence on the intention in the Malaysian context. These contrasting outcomes highlight the significance of contextual and cultural factors in shaping an individual's behaviour.

H1: Attitude significantly impacts people's intent to use Islamic banking.

Subjective Norms and Behavioural IntentionJaffar and Musa (2016) argued that subjective norms influence the intention of non-users to engage with Islamic banking services. In alignment with this, prior studies by Adeel et al. (2024), Ahmed (2021), Wu and Liu (2007), and Cheng and Cho (2011) have also demonstrated a notable impact of subjective norms on individuals’ behavioural intentions to adopt various technologies and systems across different contexts and countries. However, these findings have been contested in the research conducted by Curtis and Payne (2008) and Al-Gahtani et al. (2007), highlighting a period of scholarly disagreement, particularly between 2006 and 2008. More recently, Adeel et al. (2024) reaffirmed the positive effect of subjective norms on the acceptance of Islamic finance. In light of these mixed findings, and building upon the theoretical and empirical evidence, the study proposes the following research hypothesis:

H2: Subjective norms have a direct impact on the intent to use Islamic banking.

Perceived Behavioral Norms (PBC) and Behavioral IntentionPBC is the third important construct of the TPB. PBC is “an individual's perception of the ease or difficulty of performing the behaviour of interest” (Ajzen & Fishbein, 2000). Yazdanpanah and Forouzani's (2015) study found an insignificant effect of PBC on purchasing organic foods. Based on the TPB, Yoke et al.'s (2018) study aimed to examine the variables that impact Malaysians' buying of residential real estate in Kuala Lumpur. The study suggests a positive nexus among PBC, attitude, and economic factors. Shith et al. (2021) also found positive influence of PBC to adopt Islamic banking services in Malaysia. Al-Nahdi et al. (2015) findings concluded that PBC does not affect the intent to purchase real estate. Hence, the study proposes the following research hypothesis:

H3: PBC significantly influences the intent towards using Islamic banking.

Religiosity and Behavioural IntentionReligiosity is commonly understood as the belief in a single God and the adherence to practices guided by Shariah-compliant norms and values. Samad et al. (2022) further conceptualise religiosity as the level to which individuals incorporate the values, practices and beliefs of their religion into their everyday lives. Supporting this notion, Mokhlis (2006) emphasised the importance of perceived levels of religiosity in shaping individuals’ decisions to engage with Islamic banking products. These findings suggest that religiosity plays a pivotal role in the decision-making process concerning Shariah-compliant financial services. Furthermore, Alzadjal et al. (2022) discovered that religion is the most vital variable prompting Islamic banks customers to utilise Islamic banking services. Further, they found that the bank’s profitability usually influenced conventional banks' customers.

H4: Religiosity significantly influences the intent towards using Islamic banking.

Awareness, Knowledge and Behavioural IntentionO’Cass (2004) identified knowledge as a key factor influencing the link between attitude and behaviour toward a product. Iqbal (2016) noted that awareness of Islamic banking products was minimal decades ago, though it has since improved. Clark and Goldsmith (2006) emphasised that limited knowledge contributes to low participation in Islamic banking. Similarly, Hamid and Nordin (2001) found that while most individuals were aware of Islamic finance, only 27 per cent understood the distinctions between the Islamic and conventional financial systems in Malaysia, highlighting a gap between general awareness and detailed product knowledge. Roy (2014) performed a study on customer attitude and awareness about Islamic banking. The research also supports the IBF system to attain a position as the central banking system in finance. The study examined certain factors like brand value, an abundance of Islamic economy, and religious affiliations.

H5: Level of knowledge positively influences the intent towards using Islamic banking.

Service Quality and Behavioural IntentionService quality has emerged as a critical concern in today’s dynamic globalised business environment (Hill et al., 1987). Hegazy (1995) found that efficiency and speed in e-banking services were key factors influencing bank selection among Islamic banking clients in Egypt. Similarly, Spreng and Mackoy (1996) emphasised that service quality has a vital role in attracting potential customers and retaining existing customers, highlighting its importance as a strategic element in customer relationship management within the banking sector. According to Ahmad and Bashir (2014), Islamic banking grows rapidly. They also said various factors can influence Islamic banking, for example, well-located location, service quality and good relationships. The objective of Shariah-complaint banking channels is to promote products and Islamic banking principles. In this study, we read that Islam is the complete code of life. Islamic banking promotes banking which is based on Shariah (Ahmad & Hassan, 2007). Ajmal et al. (2018) examined the service quality role on satisfaction level of customers in Pakistan’s banking sector. The data was taken from the 400 banking customers of four leading banks (NBP, SCBPL, MBL, and HBL) branches across Karachi. Each bank represents a primary sector, such as NBP from the public sector, MBL from the Islamic industry, SCBPL from the international sector, and HBL from the private industry. The results show that empathy, tangibility, and assurance positively and significantly impact customer satisfaction.

H6: The service quality of an Islamic bank positively influences the intention to use an Islamic bank.

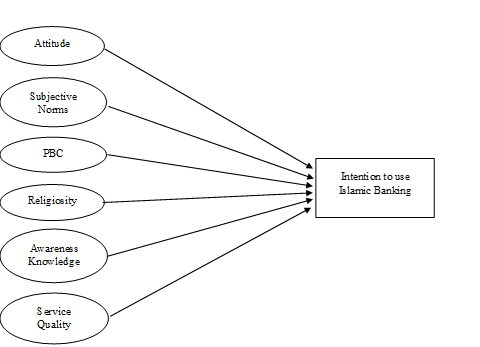

Theoretical Framework

The current study proposes a model, which is an extended TPB model, as given in Figure 2.

Figure 2

Theoretical Framework

Research Methodology

The current study aims to examine the factors affecting the intention of Muslims towards using the Islamic banking. The study adopts a deductive approach and a quantitative research method was applied. Primary data were collected from Muslims in Spain who possess knowledge of Islamic banking and finance. A structured, close-ended questionnaire was employed, with its reliability and validity established through prior studies, some of which were adapted to suit the Islamic banking context (Table 1). The survey instrument was categorized into two parts. Part I entails demographic information of the respondents, while Part II covers the key variables/constructs on a 5-point Likert scale.

Table 1

Research Constructs

|

Construct |

Description |

Key References |

|---|---|---|

|

Attitude |

Reflects personal behaviours and evaluations based on individual beliefs toward Islamic banking. |

Kaakeh et al. (2018) |

|

Subjective Norms |

Captures social influences from family, peers, and society regarding the use of Islamic banking. |

|

|

Perceived Behavioural Control |

Represents perceived ease or difficulty in adopting Islamic banking, considering enabling or hindering factors. |

|

|

Religiosity |

Measures the impact of religious commitment on the intent to use Islamic banking. |

Ibrahim et al. (2017); Bassir et al. (2014); Haron et al. (1994); |

|

Knowledge Level |

Assesses how awareness and understanding of Islamic banking influence adoption intent. |

Ibrahim et al. (2017) |

|

Service Quality |

Evaluates perceived service effectiveness and its role in influencing Islamic banking adoption. |

Kaakeh et al. (2018) |

|

Behavioral Intention |

Indicates the likelihood or willingness to adopt Islamic banking. |

A population is the entire group that a study aims to understand. The population of the current research comprised of Muslims residing within Spain. A sample is a representative subset of the population from which the data is collected. The sample of this study is comprised of 300 respondents from Catalonia. Catalonia was selected because it hosts the largest concentration of Muslims in Spain, thereby increases the likelihood that the sample reflects a broad cross-section of Muslim experiences within Spain (Lems, 2024). A convenient sampling method was used to gather the data from the targeted sample, which, according to Showkat and Parveen (2017), offers advantages such as ease of accessibility, geographical proximity, and availability during data collection, and participant willingness to engage in the study. The study applied multiple regression analysis using Smart PLS software. Besides, factor analysis, discriminant analysis and cronbach alpha tests were also conducted to test reliability and validity.

Response Rate and Pilot SurveyA total of 400 questionnaires were distributed to the target sample. Out of 400 questionnaires, 327 questionnaires were received and other 27 were excluded due to them being missing or having biased data, thereby resulting in a 75% response rate. A pilot survey was also conducted before collecting actual data from the targeted sample. Table 2 presents the reliability statistics for the pilot survey, suggesting that all constructs have above 0.6 Cronbach’s alpha value; hence, the instrument is deemed reliable for the continuation of the research.

Table 2

Reliability Analysis (Pilot Survey)

|

Scale |

Items |

Cronbach's Alpha |

|---|---|---|

|

Attitude |

4 |

0.741 |

|

Subjective Norms |

6 |

0.816 |

|

Perceived Behavioural Control |

4 |

0.870 |

|

Religiosity |

8 |

0.935 |

|

Awareness and Knowledge |

4 |

0.863 |

|

Service Quality |

4 |

0.689 |

|

Intention to use Islamic Banking |

6 |

0.748 |

|

Total |

36 |

0.917 |

Results

DemographicsTable 3 provides the demographics of the targeted sample. The demographic characteristics show that the sample of 300 respondents from Catalonia, Spain was diverse in gender, age, education, marital status, occupation and income. Many respondents were male (58%), aged 26-35 years (35.7%) and held a bachelor’s degree (38%). The respondents nearly half earning under €500 monthly included self-employed individuals, students, and professionals reflecting varied socio-economic backgrounds.

Table 3

Demographic Characteristics (N = 300)

|

Demographic Variable |

Category |

f |

% |

|---|---|---|---|

|

Age (years) |

16–25 |

79 |

26.3 |

|

26–35 |

107 |

35.7 |

|

|

36–45 |

67 |

22.3 |

|

|

46+ |

47 |

15.7 |

|

|

Gender |

Male |

174 |

58.0 |

|

Female |

126 |

42.0 |

|

|

Education / Qualification |

Secondary/O Levels |

22 |

7.3 |

|

Intermediate/A Levels |

41 |

13.7 |

|

|

Bachelors |

114 |

38.0 |

|

|

Masters/PhD |

85 |

28.3 |

|

|

Certifications/Diploma |

30 |

10.0 |

|

|

Professional Qualification |

6 |

2.0 |

|

|

Others |

2 |

0.7 |

|

|

Marital Status |

Single |

169 |

56.3 |

|

Married |

131 |

43.7 |

|

|

Occupation |

Student |

62 |

20.7 |

|

Clerical Staff |

48 |

16.0 |

|

|

Technical Staff |

35 |

11.7 |

|

|

Self-Employed |

80 |

26.7 |

|

|

Professional/Senior Management |

39 |

13.0 |

|

|

Others |

36 |

12.0 |

|

|

Income per Month (EUR) |

<500 |

132 |

44.0 |

|

501–1000 |

82 |

27.3 |

|

|

1001–1500 |

36 |

12.0 |

|

|

>1500 |

50 |

16.7 |

Descriptive include mean, standard deviation, skewness, kurtosis and number of observations, providing a comprehensive overview of the data collected from the selected participants (Table 4). Attitude has a mean value of 4.06, subjective norms have a mean value of 3.99, PBC has a mean value of 3.36, religiosity has a mean value of 3.64, awareness and knowledge have a mean value of 3.74, service quality has a mean value of 3.94 and intention has a mean value of 4.01, respectively. Furthermore, skewness and kurtosis values are within range, that is, skewness is between -3 and +3 while kurtosis is between -10 and +10, indicating no serious concern for normality.

Table 4

Descriptive Analysis (N = 300)

|

|

Mean |

SD |

Skewness |

Kurtosis |

|---|---|---|---|---|

|

Attitude |

4.06 |

.705 |

-1.087 |

2.463 |

|

Subjective Norms |

3.99 |

.892 |

-.475 |

-2.483 |

|

Percieved Behavioural Control |

3.36 |

.952 |

-.908 |

3.400 |

|

Religiosity |

3.64 |

.608 |

.175 |

-1.182 |

|

Awareness and Knowledge |

3.74 |

.374 |

.859 |

-1.126 |

|

Service Quality |

3.94 |

.741 |

-.372 |

-1.961 |

|

Intention towards Islamic Banking |

4.01 |

.674 |

.167 |

-1.022 |

The term reliability refers to “the stability and consistency of the results produced by a test, questionnaire, or survey instrument”. A value closer to 1 indicates greater internal consistency and, consequently, larger scale reliability (Kline, 2015). According to Pallant (2020), a Cronbach’s alpha and composite reliability value of 0.60 or above is considered acceptable for ensuring internal consistency and reliability. Since the reliability value for each variable is above 0.60, it thereby indicates good reliability (Table 5).

Table 5

Reliability and Validity Analysis

|

Scale |

Items |

Cronbach’s Alpha |

Composite Reliability |

AVE |

|---|---|---|---|---|

|

Attitude |

4 |

0.871 |

0.911 |

0.719 |

|

Subjective Norms |

6 |

0.805 |

0.865 |

0.529 |

|

Perceived Behavioral Control |

4 |

0.946 |

0.961 |

0.861 |

|

Religiosity |

8 |

0.909 |

0.936 |

0.786 |

|

Awareness and Knowledge |

4 |

0.894 |

0.915 |

0.576 |

|

Service Quality |

4 |

0.896 |

0.927 |

0.762 |

|

Intention towards Islamic Banking |

6 |

0.920 |

0.938 |

0.715 |

In the current study, the measurement model validity is assessed using the criteria set forth by Hair et al. (2019). The Average Variance Extracted (AVE) indicator in PLS-SEM is typically used to assess convergent validity. The results show that the AVE values are above 0.50, thereby confirming the measurement model’s validity.

Factor LoadingsFactor loadings indicate the contribution of each observable item to the latent variable or construct. Table 6 presents the factor outer loadings indicating a single-factor solution with substantial loadings, all exceeding 0.60, in line with Henseler et al. (2015) study recommendations.

Table 6

Factor Loadings

|

Attitude |

Awareness |

Intention to Use |

PBC |

Religiosity |

Service Quality |

Subjective Norms |

|

|---|---|---|---|---|---|---|---|

|

ATT1 |

0.841 |

||||||

|

ATT2 |

0.866 |

||||||

|

ATT3 |

0.858 |

||||||

|

ATT4 |

0.828 |

||||||

|

BI1 |

0.822 |

||||||

|

BI2 |

0.870 |

||||||

|

BI3 |

0.857 |

||||||

|

BI4 |

0.857 |

||||||

|

BI5 |

0.833 |

||||||

|

BI6 |

0.834 |

||||||

|

K1 |

0.882 |

||||||

|

K2 |

0.902 |

||||||

|

K3 |

0.899 |

||||||

|

K4 |

0.863 |

||||||

|

PBC1 |

0.927 |

||||||

|

PBC2 |

0.915 |

||||||

|

PBC3 |

0.933 |

||||||

|

PBC4 |

0.935 |

||||||

|

RL1 |

0.808 |

||||||

|

RL2 |

0.791 |

||||||

|

RL3 |

0.803 |

||||||

|

RL4 |

0.777 |

||||||

|

RL5 |

0.775 |

||||||

|

RL6 |

0.756 |

||||||

|

RL7 |

0.773 |

||||||

|

RL8 |

|

|

|

|

0.559 |

|

|

|

SAT1 |

0.872 |

||||||

|

SAT2 |

0.872 |

||||||

|

SAT3 |

0.876 |

||||||

|

SAT4 |

0.871 |

||||||

|

SN1 |

0.701 |

||||||

|

SN2 |

0.804 |

||||||

|

SN3 |

0.804 |

||||||

|

SN4 |

0.818 |

||||||

|

SN5 |

0.775 |

||||||

|

SN6 |

0.647 |

Table 7 presents the Fornell-Larcker criterion findings demonstrating an excellent level of discriminant validity, as all the square root values of the AVE are greater than the correlation values between the constructs. Thus, the study's measurement model exhibits satisfactory validity.

Table 7

Discriminant Validity

|

|

ATT |

AK |

BI |

PBC |

RL |

SQ |

SN |

AVE |

|---|---|---|---|---|---|---|---|---|

|

Attitude |

0.83 |

0.719 |

||||||

|

Awareness & Knowledge |

0.13 |

0.89 |

0.786 |

|||||

|

Intention to Use Islamic Banking |

0.38 |

0.52 |

0.85 |

0.715 |

||||

|

Percieved Behavioural Control |

0.30 |

0.36 |

0.54 |

0.93 |

0.861 |

|||

|

Religiosity |

0.41 |

0.37 |

0.50 |

0.57 |

0.76 |

0.576 |

||

|

Service Quality |

0.49 |

0.37 |

0.56 |

0.57 |

0.39 |

0.87 |

0.762 |

|

|

Subjective Norms |

0.38 |

0.46 |

0.62 |

0.56 |

0.67 |

0.55 |

0.73 |

0.529 |

Note. ATT = attitude, AK = awareness & knowledge, BI =intention to use Islamic banking, PBC = perceived behavioural control, RL = religiosity, SQ = service quality, SN = subjective norms.

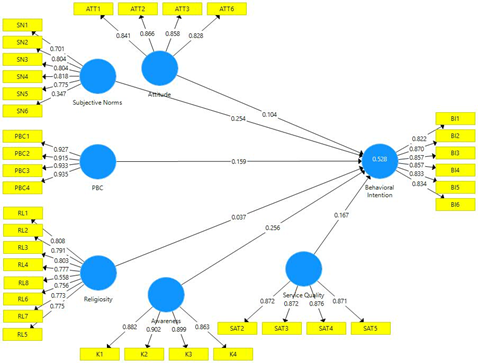

Hypothesis TestingTable 8 depicts that the relationship between Attitude (ATT) and BI demonstrates a positive beta value of 0.107, with a t-stat of 2.332 and a p-value of 0.02, which is below the 0.05 significance level threshold. This indicates a significant positive effect of attitude on intention to use Islamic banking in Spain. Additionally, subjective norms (SN) show a strong positive relationship with BI, reflected in a path coefficient of 0.256, a t-statistic of 3.746, and a highly significant p-value of 0.000. Similarly, Awareness and Knowledge (AK) exhibit a significant influence on BI, with a beta value of 0.254, t-stat value of 5.827, and p-value of 0.000. A significant positive relationship supported by a beta coefficient value of 0.159 also shown by PBC (p < 0.05). Moreover, the relationship between religiosity (RL) and BI yielded a beta value of 0.038, and a t-statistics value of 0.589 (p = 0.556). The p-value suggests an insignificant positive association at the 0.05 significance level. In contrast, service quality (SQ) demonstrates a positive effect on BI, with a beta value of 0.167 and a p-value of 0.006.

Figure 3

Measurement Model with Cross Loadings

Table 8

Hypothesis Testing

|

Sr. |

Hypothesis |

β |

S.D. |

t-stat |

p-value |

Decision |

|---|---|---|---|---|---|---|

|

H1 |

ATT -> BI |

0.107 |

0.045 |

2.332 |

0.020 |

Accepted |

|

H2 |

SN -> BI |

0.256 |

0.068 |

3.746 |

0.000 |

Accepted |

|

H3 |

PBC -> BI |

0.159 |

0.064 |

2.484 |

0.013 |

Accepted |

|

H4 |

RL -> BI |

0.038 |

0.064 |

0.589 |

0.556 |

Rejected |

|

H5 |

AK -> BI |

0.254 |

0.044 |

5.827 |

0.000 |

Accepted |

|

H6 |

SQ -> BI |

0.167 |

0.061 |

2.741 |

0.006 |

Accepted |

Discussion

Hypothesis 1 states that attitude directly affects the intent of Muslims to use Islamic banks in Spain. Kaakeh et al.’ (2018) research findings were consistent to our study, who found religious motivation and attitude to be significant factors impacting the intention towards using Islamic banking. Amin et al. (2014) also concluded that attitude affects Malaysian customers’ choice to select an Islamic credit card. However, these findings were inconsistent with the study of Baber (2018), who revealed that attitude has no relevance in developing intentions about Islamic finance in India.

Hypothesis 2 is supported by prior research, including studies by Marchewka et al. (2007), Cheng and Cho (2011), all of which reported a significant connectedness among behavioural intention and subjective norms across various technologies and cultural settings. Similarly, Baber (2018) found a positive association between subjective norms and the acceptance of Islamic finance. Additionally, the relationship between PBC and Muslim’s intent towards using Islamic banking is positive and significant (Hypothesis 3). It is consistent to earlier studies that suggest a significant positive impact of PBC on people's behavioural intention (Alam & Sayuti, 2011; Arora & Kishor, 2019). Yoke et al. (2018) suggests a positive relationship between PBC and buying intention based on the TPB. However, Pavlou and Chai (2002), Ng and Rahim (2005), and Dean et al. (2008) find that the PBC has no significant effect on the buying intention of an individual.

Hypothesis 4 states that religiosity significantly affects Muslims' intention to use Islamic banks in Spain. It is inconsistent with the study of McDaniel and Burnett (1990) and Osman et al. (2019). McDaniel and Burnett (1990) ascertain that religiosity level is one of the vital predictors of the attitude and intention of participation towards Islamic banking products. Osman et al. (2019) found that religiosity has been a significant determinant in influencing the behavioural intent of young intellectuals in adopting Islamic finance products.

Hypothesis 5 states that awareness and knowledge directly affect Muslims' intent to use Islamic banks in Spain. O’Cass (2004) found that knowledge is a significant factor affecting the relationship between an individual's attitude and behaviour towards a specific product. Clark and Goldsmith (2006) argued that the lack of knowledge of Islamic banking products contributes to low public participation. Hamid and Nordin (2001) concluded that almost everyone is aware of Islamic finance products; however, very limited respondents (27 per cent) were aware of the similarities and differences of the streams in Malaysia.

Hypothesis 6 states that service quality significantly affects Muslims' intention to use Islamic banks in Spain. The SEM analysis showed that service quality is a significant predictor of intention towards utilising Islamic bank products or services. It is challenging for a business entity to identify the customer perception and evaluation regarding the quality of its services (Jamal & Naser, 2002). Dusuki and Abdullah (2007) found that a bank’s good reputation, convenience, and price of the financial products were the most critical factors that customers believed impacted their Islamic financial service provider selection. Ajmal et al. (2018) show that empathy, tangibility, and assurance positively and significantly impact customer satisfaction in Pakistan.

ConclusionThis study determines the variables that influence the intention of Muslims to use Islamic banking in Spain by applying TPB. The study concluded that all understudied variables, except religiosity, are significant determinants of Muslims’ intention to use Islamic banking in Spain, while religiosity alone does not appear to be a decisive factor. These results reinforce the TPB by highlighting that cognitive evaluations, social influence, and perceived control collectively shape behavioural intentions. The study also extends TPB in the context of minority Muslim populations by demonstrating that practical considerations such as service quality and knowledge can be as influential as traditional psychosocial predictors. The positive attitude and social influence surrounding Islamic banking can facilitate market entry, offering Islamic banks a competitive advantage.

The findings suggest several actionable policy implications. Regulators and financial authorities in Spain can support the growth of Islamic banking by promoting awareness campaigns, ensuring transparent service quality standards, and facilitating accessible banking infrastructure tailored to Muslim communities. Banks should focus on culturally and religiously aligned marketing strategies while enhancing service reliability to strengthen consumer trust. However, this study has some limitations. The sample was drawn solely from Muslims in Catalonia, while Muslims residing in other regions may differ in socioeconomic status, integration patterns, and religious community structures. Future studies could use larger, more representative samples and incorporate longitudinal designs to better capture behavioural changes over time.

Author Contribution

Muhammad Musa: conceptualization, formal analysis, software resources investigation, writing- original draft. Datin Dr. Bt Rusni: validation, supervision, writing - review & editing. Nur Harena Binti Redzuan: conceptualization, supervision, methodology, validation.

Conflict of Interest

The authors of the manuscript have no financial or non-financial conflict of interest in the subject matter or materials discussed in this manuscript.

Data Availability Statement

Data supporting the findings of this study will be made available by the corresponding author upon request.

Funding Details

No funding has been received for this research.

The authors did not used any type of generative artificial intelligence software for this research.

REFERENCES

Abiola-Adams, O., Azubuike, C., Sule, A. K., & Okon, R. (2023). Innovative approaches to structuring Sharia-compliant financial products for global markets. Journal of Islamic Finance Studies, 4(1), 615–620.

Adeel, M., Quddoos, M. U., Siddiqi, A. A., & Iqbal, M. (2024). Exploring the influence of subjective norms, perceived behavioral control, and attitudes on trust in Islamic banks: An empirical analysis. Pakistan Islamicus (An International Journal of Islamic & Social Sciences), 4(2), 201–209.

Ahmad, A. U. F., & Hassan, M. K. (2007). Regulation and performance of Islamic banking in Bangladesh. Thunderbird International Business Review, 49(2), 251–277. https://doi.org/10.1002/tie.20142

Ahmad, A., & Bashir, R. (2014). An investigation of customers' awareness level and customers' service utilisation decision in Islamic banking. Pakistan Economic and Social Review, 52(1), 59–74.

Ahmed, A. H. (2021). The impact of attitude and subjective norms on customers' behavior toward Islamic banking: Evidence from Palestine. In V. Ramadani, B. A. Alserhan, L. P. Dana, J. Zeqiri, H. Terzi, & M. Bayirli (Eds.), Research on Islamic business concepts (pp. 53–69). Springer International Publishing.

Ajmal, H., Khan, R. A., & Fatima, M. (2018). Impact of service quality on customer satisfaction in the banking industry of Pakistan: A case study of Karachi. Journal of Social and Administrative Sciences, 5(3), 219–238. https://doi.org/10.1453/jsas.v5i3.1723

Ajzen, I., & Fishbein, M. (2000). Attitudes and the attitude-behavior relation: Reasoned and automatic processes. European Review of Social Psychology, 11(1), 1–33. https://doi.org/10.1080/14792779943000116

Alam, S. S., & Sayuti, N. S. (2011). Applying the Theory of Planned Behavior (TPB) in halal food purchasing. International Journal of Commerce and Management, 21(1), 8–20. https://doi.org/10.1108/10569211111111676

Al-Gahtani, S. S., Hubona, G. S., & Wang, J. (2007). Information technology (IT) in Saudi Arabia: Culture and the acceptance and use of IT. Information & Management, 44(8), 681–691. https://doi.org/10.1016/j.im.2007.09.002

Al-Nahdi, T. S., Habib, S. A., & Albdour, A. A. (2015). Factors influencing the intention to purchase real estate in Saudi Arabia: Moderating effect of demographic citizenship. International Journal of Business and Management, 10(4), 35–48. http://dx.doi.org/10.5539/ijbm.v10n4p35

Alzadjal, M. A. J., Abu-Hussin, M. F., Md Husin, M., & Mohd Hussin, M. Y. (2022). Moderating the role of religiosity on potential customer intention to deal with Islamic banks in Oman. Journal of Islamic Marketing, 13(11), 2378–2402.

Amin, H., Rahman, A. R. A., & Razak, D. A. (2014). Consumer acceptance of Islamic home financing. International Journal of Housing Markets and Analysis, 7(3), 307–332. https://doi.org/10.1108/IJHMA-12-2012-0063

Andespa, R., Yeni, Y. H., Fernando, Y., & Sari, D. K. (2024). A systematic review of customer Sharia compliance behaviour in Islamic banks: Determinants and behavioural intention. Journal of Islamic Marketing, 15(4), 1013–1034. https://doi.org/10.1108/JIMA-06-2023-0181

Arora, A. P., & Kishor, N. (2019). Factors determining purchase intention and behaviour of consumers towards luxury fashion brands in India: An empirical evidence. British Journal of Marketing Studies, 7(4), 34–58.

Baber, H. (2018). How crisis-proof is Islamic finance? A comparative study of Islamic finance and conventional finance during and post-financial crisis. Qualitative Research in Financial Markets, 10(4), 415–426. https://doi.org/10.1108/QRFM-12-2017-0123

Bacha, O. I. (2024). Islamic banking and finance forty years on: A reality check. World Scientific Annual Review of Islamic Finance, 2, Article e2430002. https://doi.org/10.1142/S281102342430002X

Baker, R. K., & White, K. M. (2010). Predicting adolescents' use of social networking sites from an extended theory of planned behaviour perspective. Computers in Human Behavior, 26(6), 1591–1597.

Basr, S. S. S., & Daud, K. A. K. (2020). The impact of purchasing behaviour towards digital marketing in Kangar, Perlis. International Journal of Business and Management, 4(5), 62–69.

Bassir, N. F., Zakaria, Z., Hasan, H. A., & Alfan, E. (2014). Factors influencing the adoption of Islamic home financing in Malaysia. Transformations in Business and Economics, 13(1), 155–174.

Bolelli, S. (2023). Muslim population in Spain increased 10 times in last 30 years. Anadolu Agency. https://www.aa.com.tr/en/europe/muslim-population-in-spain-increased-10-times-in-last-30-years/2854684

Cheng, S., & Cho, V. (2011). An integrated model of employees' behavioral intention toward innovative information and communication technologies in travel agencies. Journal of Hospitality & Tourism Research, 35(4), 488–510. https://doi.org/10.1177/1096348010384598

Chiou, J. S. (1998). The effects of attitude, subjective norm, and perceived behavioral control on consumers' purchase intentions: The moderating effects of product knowledge and attention to social comparison information. Proceedings of the National Science Council, Republic of China, Part C, 9(2), 298–308.

Clark, R. A., & Goldsmith, R. E. (2006). Interpersonal influence and consumer innovativeness. International Journal of Consumer Studies, 30(1), 34–43. https://doi.org/10.1111/j.1470-6431.2005.00435.x

Curtis, M. B., & Payne, E. A. (2008). An examination of contextual factors and individual characteristics affecting technology implementation decisions in auditing. International Journal of Accounting Information Systems, 9(2), 104–121. https://doi.org/10.1016/j.accinf.2007.10.002

Davis, F. D., Bagozzi, R. P., & Warshaw, P. R. (1989). User acceptance of computer technology: A comparison of two theoretical models. Management Science, 35(8), 982–1003. https://doi.org/10.1287/mnsc.35.8.982

Dean, D., Suhartanto, D., & Pujianti, F. N. (2022). Millennial behavioural intention in Islamic banks: The role of social media influencers. Journal of Islamic Marketing, 13(12), 2798–2814. https://doi.org/10.1108/JIMA-02-2021-0042

Di Pietro, L., & Pantano, E. (2012). An empirical investigation of social network influence on consumer purchasing decision: The case of Facebook. Journal of Direct, Data and Digital Marketing Practice, 14(1), 18–29. https://doi.org/10.1057/dddmp.2012.10

Dusuki, A. W., & Irwani Abdullah, N. (2007). Why do Malaysian customers patronise Islamic banks? International Journal of Bank Marketing, 25(3), 142–160. https://doi.org/10.1108/02652320710739850

Eyerci, C. (2021). Basics of Islamic economics and the prohibition of riba. In C. Eyerci (Ed.), The causes and consequences of interest theory: Analyzing interest through conventional and Islamic economics (pp. 87–130). Springer International Publishing.

Galan, S. (2025, November 28). Number of Muslims in Spain in 2023, by nationality. Statista. https://www.statista.com/statistics/989902/muslims-in-spain-by-nationality/?srsltid=AfmBOoq7aIVy9vCl5_z30DUMe811YGYnMm3eQemeiUa_YWG4Ja6rnNwP

Hair, J. F., Risher, J. J., Sarstedt, M., & Ringle, C. M. (2019). When to use and how to report the results of PLS-SEM. European Business Review, 31(1), 2–24. https://doi.org/10.1108/EBR-11-2018-0203

Hamid, A., & Nordin, N. (2001). A study on Islamic banking education and strategy for the new millennium: Malaysian experience. International Journal of Islamic Financial Services, 2(4), 3–11.

Hanafiah, M. H., & Hamdan, N. A. A. (2021). Determinants of Muslim travellers' halal food consumption attitude and behavioural intentions. Journal of Islamic Marketing, 12(6), 1197–1218. https://doi.org/10.1108/JIMA-09-2019-0195

Haron, S., Ahmad, N., & Planisek, S. L. (1994). Bank patronage factors of Muslim and non‐Muslim customers. International Journal of Bank Marketing, 12(1), 32–40. https://doi.org/10.1108/02652329410049599

Hegazy, I. (1995). An empirical comparative study between Islamic and commercial banks' selection criteria in Egypt. International Journal of Commerce and Management, 5(3), 46–61. https://doi.org/10.1108/eb047313

Henseler, J., Ringle, C. M., & Sarstedt, M. (2015). A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science, 43(1), 115–135. https://doi.org/10.1007/s11747-014-0403-8

Hill, T., Smith, N. D., & Mann, M. F. (1987). Role of efficacy expectations in predicting the decision to use advanced technologies: The case of computers. Journal of Applied Psychology, 72(2), 307–313

Ibrahim, M. A., Fisol, W. N. M., & Haji-Othman, Y. (2017). Customer intention on Islamic home financing products: An application of theory of planned behavior (TPB). Mediterranean Journal of Social Sciences, 8(2), 77–86.

Insifr. (2025). The future of Islamic finance: Trends to watch in 2025. https://www.insifr.com/en/blogs/the-future-of-islamic-finance-trends-to-watch-in-2025#:~:text=The%20worldwide%20Islamic%20finance%20sector,friendly%20mobile%20apps%20and%20platforms.

Iqbal, Q. (2016). Job-crafting and organizational commitment: Person-job fit as moderator in banking sector of Pakistan. International Journal of Management, Accounting and Economics, 3(12), 837–851.

Jaffar, M. A., & Musa, R. (2016). Determinants of attitude and intention towards Islamic financing adoption among non-users. Procedia Economics and Finance, 37, 227–233. https://doi.org/10.1016/S2212-5671(16)30118-6

Jamal, A., & Naser, K. (2002). Customer satisfaction and retail banking: an assessment of some of the key antecedents of customer satisfaction in retail banking. International Journal of Bank Marketing, 20(4), 146–160. https://doi.org/10.1108/02652320210432936

Kaakeh, A., Hassan, M. K., & van Hemmen Almazor, S. F. (2018). Attitude of Muslim minority in Spain towards Islamic finance. International Journal of Islamic and Middle Eastern Finance and Management, 11(2), 213–230. https://doi.org/10.1108/IMEFM-11-2017-0306

Kishada, Z. M. E., & Wahab, N. A. (2013). Factors affecting customer loyalty in Islamic banking: Evidence from Malaysian banks. International Journal of Business and Social Science, 4(7), 264–273.

Kline, R. B. (2015). Principles and practice of structural equation modeling. Guilford Publications.

Lems, J. M. (2024). To be or not to be recognized? Claims for recognition among Muslim minorities in Spain. In K. Topidi & E. R. Pastor (Eds.), Minority rights and social change: Norms, actors and strategies (pp. 162–178). Routledge.

Marchewka, J. T., Liu, C., & Kostiwa, K. (2007). An application of the UTAUT model for understanding student perceptions using course management software. Communications of the IIMA, 7(2), 93–104.

McDaniel, S. W., & Burnett, J. J. (1990). Consumer religiosity and retail store evaluative criteria. Journal of the Academy of Marketing Science, 18(2), 101–112. https://doi.org/10.1007/BF02726426

Mokhlis, S. (2006). The influence of religion on retail patronage behaviour in Malaysia [Doctoral dissertation, University of Stirling]. STORRE: Stirling Online Research Repository. https://storre.stir.ac.uk/handle/1893/87

Mordor Intelligence. (2025, June 22). Islamic finance market size & share analysis - growth trends and forecast (2025 - 2030) https://www.mordorintelligence.com/industry-reports/global-islamic-finance-market

Mustapha, N., Mohammad, J., Quoquab, F., & Salam, Z. A. (2023). "Should I adopt Islamic banking services?" Factors affecting non-Muslim customers' behavioral intention in the Malaysian context. Journal of Islamic Marketing, 14(10), 2450–2465. https://doi.org/10.1108/JIMA-03-2022-0094

Ng, B. Y., & Rahim, M. (2005). A socio-behavioral study of home computer users' intention to practice security. AIS Electronic Library. http://aisel.aisnet.org/pacis2005/20

O'Cass, A. (2004). Fashion clothing consumption: Antecedents and consequences of fashion clothing involvement. European Journal of Marketing, 38(7), 869–882. https://doi.org/10.1108/03090560410539294

Osman, I., Maâ, M., Muda, R., Husni, N. S. A., Alwi, S. F. S., & Hassan, F. (2019). Determinants of behavioural intention towards green investments: The perspectives of Muslims. International Journal of Islamic Business, 4(1), 16–38.

Pallant, J. (2020). SPSS survival manual: A step by step guide to data analysis using IBM SPSS. Routledge.

Pavlou, P. A., & Chai, L. (2002). What drives electronic commerce across cultures? Across-cultural empirical investigation of the theory of planned behavior. Journal of Electronic Commerce Research, 3(4), 240–253.

Ramasubbian, H., Priyadarsini, K., & Vasuki, M. (2018). Investment decisions in real estate: A Theory of Planned Behaviour (TPB) based approach. International Journal of Pure and Applied Mathematics, 119(17), 2377–2381.

Ramayah, T., Ling, N. S., Taghizadeh, S. K., & Rahman, S. A. (2016). Factors influencing SMEs' website continuance intention in Malaysia. Telematics and Informatics, 33(1), 150–164. https://doi.org/10.1016/j.tele.2015.06.007

Rasheed, H., Aimin, W., & Ahmed, A. (2012). An evaluation of bank customer satisfaction in Pakistan, comparing foreign and Islamic banks. International Journal of Academic Research in Business and Social Sciences, 2(7), 177–184.

Roy, S. (2014). Customers' preference towards Islamic banking: Religious belief or influence of economic factor [Doctoral dissertation, BRAC University]. Institutional Repository. https://dspace.bracu.ac.bd/xmlui/handle/10361/3335

Sabirzyanov, R. (2016). Islamic financial products and services patronizing behavior in Tatarstan: The role of perceived values and awareness. Journal of King Abdulaziz University: Islamic Economics, 29(1), 111–125.

Samad, S., Kashif, M., Wijeneyake, S., & Mingione, M. (2022). Islamic religiosity and ethical intentions of Islamic bank managers: Rethinking theory of planned behaviour. Journal of Islamic Marketing, 13(11), 2421–2436. https://doi.org/10.1108/JIMA-02-2020-0042

Shah, T. (2025). From criticism to confirmation: A definitive examination of Running Musharakah model and its validity. Journal of Islamic Accounting and Business Research. Advanced online publication. https://doi.org/10.1108/JIABR-03-2024-0072

Shith, M. S. S. P. M., Safruddin, M., Rahim, M. A., & Putera, N. S. F. M. S. (2021). Using the theory of planned behavior and religion to assess customers' behavioral intention to adopt Islamic banking services in Malaysia. Jurnal Islam dan Masyarakat Kontemporari, 22(2), 36–45. https://doi.org/10.37231/jimk.2021.22.2.575

Showkat, N., & Parveen, H. (2017). Non-probability and probability sampling. Media and Communications Study, 6(1), 1–9.

Spreng, R. A., & Mackoy, R. D. (1996). An empirical examination of a model of perceived service quality and satisfaction. Journal of Retailing, 72(2), 201–214.

Thaidi, H. A. A., Ab Rahman, M. F., & Salleh, A. Z. (2023). Addressing challenges, unleashing potentials: Towards achieving impactful Islamic social finance. Ulum Islamiyyah, 35(2), 63–85. https://doi.org/10.33102/uij.vol35no02.554

Wu, J., & Liu, D. (2007). The effects of trust and enjoyment on intention to play online games. Journal of Electronic Commerce Research, 8(2), 128–140.

Yazdanpanah, M., & Forouzani, M. (2015). Application of the Theory of Planned Behaviour to predict Iranian students' intention to purchase organic food. Journal of Cleaner Production, 107, 342–352. https://doi.org/10.1016/j.jclepro.2015.02.071

Yoke, C. C., Mun, Y. W., Peng, L. M., & Yean, U. L. (2018). Purchase intention of residential property in greater Kuala Lumpur, Malaysia. International Journal of Asian Social Science, 8(8), 580–590. https://doi.org/10.18488/journal.1.2018.88.580.590

Zafar, M. B., & Sulaiman, A. A. (2022). CSR narrative under Islamic banking paradigm. Social Responsibility Journal, 17(1), 15–29. https://doi.org/10.1108/20408741011082543