Formulating an Islamic Corporate Social Responsibility (I-CSR) Model: Integrating Maqāṣid Sharī‘ah and Iḥsān

Usmanul Khakim*

Centre for Islamic and Occidental Studies (CIOS)

Faculty of Ushuluddin, Universtas Darussalam Gontor

Ponorogo, Indonesia

Hamid Fahmy Zarkasyi

Universitas Darussalam Gontor

Ponorogo, Indonesia

Fuad Mas'ud

Faculty of Economics and Business

Universitas Diponegoro (UNDIP)

Semarang, Indonesia

Muhammad Faqih Nidzom

Universitas Darussalam Gontor

Ponorogo, Indonesia

Abstract

This research aims to formulate a conceptual model of Islamic Corporate Social Responsibility (I-CSR) by incorporating the principles of ihsān and maqāṣid sharī’ah. The research hypothesizes that maqāṣid sharī’ah provides a foundation for defining I-CSR dimensions, while ihsān theory offers a hierarchical structure. The study adopts a basic-level research and development (R&D) approach, employing qualitative content analysis through a textual examination of two theories. The process begins with an in-depth examination of maqāṣid sharī’ah and ihsān theories, followed by their integration. The research findings are as follows: First, specific I-CSR dimensions were identified rooted in maqāṣid sharī’ah, including faith (īmān), human dignity (fiṭrah), the self (nafs), intellect (‘aql), prosperity (nasl), society (ijtimā’), wealth (māl), and ecology (bī’ah). Second, companies within the I-CSR framework were categorized according to ihsān theory into seven types: fāsid, ṭayyib, khair, ma’rūf, ṣālih, birr, and ihsān. The limitations of the research are: (1) it focuses solely on the theories of maqāṣid sharī’ah and ihsān; (2) the conceptual model is in its preliminary stage and requires further refinement with additional indicators. Despite these limitations, the findings have practical implications, particularly in enhancing the assessment of I-CSR practices.

Introduction

The concept of Corporate Social Responsibility (CSR) has evolved significantly over time, with Archie Carroll introducing one of its most influential models in 1991.1 Carroll's CSR pyramid, outlined four levels of corporate responsibility: (1) Economic responsibility, emphasizing i profitability as a fundamental business requirement; (2) Legal responsibility, requiring a company to not only be profitable but also operate within the framework of legal regulations and laws; (3) Ethical responsibility, promoting moral standards and ethical practices beyond legal compliance to embrace moral principles (4) Philanthropic responsibility, underscoring a company's commitment to enhancing the quality of life within the broader community.2 Carroll's framework has profoundly shaped CSR discourse, inspiring extensive research by scholars such as Nalband & Kelabi (2014),3 Schwartz & Carroll (2014),4 Naderian and Baharun (2015),5 Baden (2016),6 Ehie (2016),7 Brin & Nehme (2019),8 and Wagner & Tsukamoto (2019).9

Similarly, many Muslim scholars have adapted and reinterpreted Carroll's CSR model within an Islamic framework. For instance, Wajdi Dusuki incorporated Carroll's CSR pyramid into the Taqwā paradigm.10 While Jawed Akhtar proposed an Islamic-CSR (I-CSR) framework grounded in three Islamic axioms: Tauḥīd, 'Adl, and Ikhtiyar.11 The I-CSR model proposed by Khurshid also revisits Carroll's ideas through an Islamic lens.12 Despite these diverse approaches, the core dimensions of CSR—economic, legal, ethical, and philanthropic responsibilities remain central, alongside the moral hierarchy of immoral, amoral, and moral behavior.13 This research seeks not to critique existing studies but to provide a fresh perspective on the I-CSR by integrating two Islamic theories: maqāṣid sharī'ah and ihsān. While previous studies have applied maqāṣid sharī'ah theory to the I-CSR framework, its originality lies in pioneering the incorporation of ihsān theory—justifying this claim, which will be further explained in the literature review. The current research aims to develop an I-CSR conceptual model informed by the concept of ihsān and the objectives of maqāṣid sharī'ah. It is hypothesized that the principles of maqāṣid sharī'ah defines the dimensions of I-CSR, while ihsān establishes its hierarchical structure. This research endeavors to validate this hypothesis.

2.Literature Review

A wide range of scholars has explored the concept of I-CSR, analysing its principles, frameworks, and applications in various contexts. The key findings and contributions of these studies are summarized in the following table for clarity and reference:

Table 1. Literature Review: Highlights the Extensive Research Conducted on Islam and CSR

|

No |

I-CSR |

Researchers |

Authors' Comments |

|

1 |

CSR and Islam |

Mohammed, (2007),14 Dusuki, (2008),15 A. W. Hassan & Salma Binti Abdul Latiff, (2009),16 Ibrahim et al., (2010),17 Zahid & Hassan, (2012),18 Lahuri, (2013),19 Khurshid et al., (2014),20 Elasrag, (2015),21 Afif, (2017),22 Mais et al., (2017),23 Muslihati et al., (2018),24 Sayed Ahmed & Abu Zaid, (2019),25 (Ermawati et.el., 2021),26 |

This research group exemplifies the integration of Western CSR theory with Islamic teachings, values, and principles. Their approach involves aligning these theories with the guidance provided by Qur'anic verses and Hadith directly. |

|

2 |

CSR and Islamic Institutions |

Dusuki, (2005),27 Islam & Deegan, (2008),28 Hassam & Abdul Lathif, (2009),29 Fauziah et.al., (2016),30 Zafar & Sulaiman, (2019),31 Ahmad, (2021),32 Ermawati et al., (2021),33 Nurdin & Subri, (2021),34 Ascarya & Masrifah, (2023).35 |

This research group validates Western CSR theories by examining their application within Islamic institutions, such as Islamic banks, Muslim-owned companies, or Islamic philanthropic organizations. |

|

3 |

Developing an Islamic CSR Model |

Dusuki & Abdullah (2007),36 Mohamad & Mukhazir (2008),37 Khurshid (2014),38 Triyuwono (2016),39 Badriah et al., (2021),40 Ascarya & Masrifah (2023).41 |

This research group redefines and adapts Western CSR theories by integrating Islamic concepts and teachings. |

|

4 |

CSR and Maqāṣid sharī'ah |

This research group modifies Western CSR theories by embedding the principles of maqāṣid sharī'ah into their framework. |

The concept of Islamic Corporate Social Responsibility (I-CSR) has been explored in notable works such as those by Dusuki & Abdullah (2007);44 and Ascarya & Masrifah (2023);45 being particularly relevant to this research due to their focus on the intersection of CSR and maqāṣid sharī'ah. Dusuki & Abdullah employed Imam al Ghazāli's framework;46 while Ascarya & Masrifah utilized Abdul Madjīd al Najjar's model to examine I-CSR dimensions, including religion (al-din), life (nafs), intellect (aql), lineage (nasl), wealth (māl), society (ijtimā'), and ecology (bī'ah).47 They further structured a CSR hierarchy based on maslahah, encompassing dzarūriyāt (necessities), hajiyāt (complements), and taḥsīniyāt (improvement).48

This research builds upon their work by further examining maqāṣid sharī'ah as an integral I-CSR dimension and introducing iḥsān theory into its hierarchy; thus advancing the scholarly work initiated by Ascarya & Masrifah and Dusuki & Abdullah.

2. Method

This study adopts a basic-level research and development (R&D) approach, guided by Gutterman's statement that R&D focuses on producing technical insights that differs from existing models, frameworks, or products.49 The purpose of this research aligns with this definition, as it seeks to develop a unique framework model distinct from existing CSR models. Basic-level R&D research also entails providing theoretical explanations for new models without extending to application, implementing, testing, or evaluating.50 Since this study does not involve practical implementation or evaluation, it will focus solely on a literature review. The data is collected from diverse sources, including books, journal articles, and Islamic text such as the Qur'an, and Hadith. The primary data sources include al-Maqāṣid al-Sharī'ah bi Ab'ād al Jadīdah by Abdul Madjid al-Najjar51 and Minhaj by Hamid Fahmy Zarkasyi.52 Using qualitative content analysis technique, the current study interprets textual data.53 The research unfolds in three stages: 1) thoroughly examining the theory of maqāṣid sharī'ah and iḥsān; 2) exploring their significance in relation to the dimensions and hierarchical structure of Corporate Social Responsibility (CSR); and 3) integrating them to construct a new conceptual framework for I-CSR. This foundational work establishes theoretical justifications for developing an I-CSR framework grounded in these Islamic principles.

3. Results and Discussion

3.1. Maqāṣid sharī'ah as I-CSR's Dimensions

Corporate Social Responsibility (CSR) has been studied extensively, with various scholars identifying dimensions that organizations must consider.54 These dimensions of CSR include economic, legal, ethical, and philanthropic responsibilities.55 Elkington and Hartman & Desjardin identified three dimensions: economic, social, and ecological.56 Additionally, Bariah et.al expanded these by introducing ethics, profit, people, planet, and prophet as essential dimensions.57 This diversity of perspectives highlights the multifaceted nature of CSR, underscoring its broad scope.

This study seeks to integrate the principles of maqāṣid sharī'ah into the dimensions of Islamic Corporate Social Responsibility (I-CSR). Numerous scholars, including Imam al-Ghazālī, Ibn 'Ashūr, Al-Shātibi, al-Raisuni, Abu Zahrah, and al-Najjar, have extensively discussed the concept of maqāṣid sharī'ah.58 Central to these discussions are the five essential objectives ḍarūriyāt al-khamsah): safeguarding (hifẓ) religion (al-dīn), life (nafs), intellect ('aql), lineage (nasl), and wealth (māl). This framework has evolved to explicitly include an ecological dimension, reflecting modern environmental concerns in the broader CSR discourse. Among the scholars of maqāṣid sharī'ah theory, Abdul Madjid al-Najjar explicitly mentions the natural environment (bī'ah) as a critical aspect of life. Therefore, this study focuses on al-Najjar's interpretation of maqāṣid sharī'ah theory.

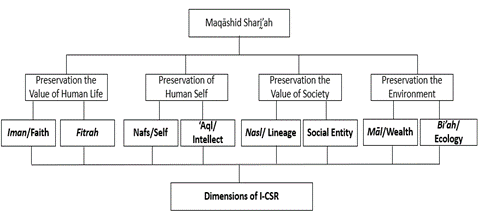

Before proceeding further, it is essential to explain the meaning of Maqāṣid al-Sharī'ah. This term refers to the goals, wisdom, purposes, secrets, and underlying rationale for the establishment of Islamic law (sharī'ah).59 The core of Maqāṣid is to promote benefit while preventing harm, encapsulated by the principle (dar'u al-mafāsid wa jalb al-maṣālih) (averting harm and attracting benefit).60 These objectives arise the dimensions of life that are the focus of its preservation. In his seminal work Maqāṣid al-Sharī'ah bi Ab'ād Jadīdah, al-Najjar presents a nuanced classification of Maqāṣid al-Sharī'ah into four categories and eight dimensions as follows.

Figure 1. The dimensions of I-CSR (Source: An Najjar 2008, developed by authors)

Figure 1 illustrates that the concept of I-CSR is structured around eight key dimensions: faith (īmān), innate nature (fitrah), self (nafs), intellect ('aql), lineage (nasl), social entity (ijtimā'), wealth (māl), and environment (bī'ah). This discussion begins with the dimension of faith, which lies at the heart of the Islamic worldview. This perspective emphasizes belief in God as a core principle and adherence to Islamic sharī'ah, which governs acts of worship (ibādah) and worldly dealings (mu'āmalah) as pathways to manifest one's faith.61 Upholding sharī'ah signifies true faith in God and involves one's beliefs, words, and actions with Islamic principles,62 as reflected in acts of worship and mu'āmalah.63

The faith dimension encompasses two critical aspects emerge in the context of I-CSR.64 The first is worship (ibādah), calls for organizations to create an environment where religious practices are supported. This can be achieved by providing worship spaces, allocating prayer schedules, granting leave for religious duties, and providing spiritual guidance. The second aspect is mu'āmalah, which suggests that Islamic companies must adhere to Islamic rules of transactions. Key practices include: 1) Ḥalāl-ḥarām considerations, ensuring that products and services are permissible, while rejecting usury, bribery, and fraud; 2) promoting ethical considerations through positive respectful and cooperative interactions; and 3) Observing aesthetic standards by maintaining appropriate dress codes and appearances. These elements together underline the corporate responsibility to foster justice, trustworthiness, and a sense of brotherhood.65

The second dimension of discussion is the natural state known as fitrah.66 Linguistically, fiṭrah refers to "al-ibtidā'," meaning the beginning or origin;67 it denotes the original state of a thing in accordance with its inherent conditions.68 For humans, this includes their physical and spiritual constitution, a natural inclination to believe in Allah, an affinity for goodness, and a desire for harmony and well-being.69 Arif identifies:"Fiṭra not only as (i) a natural tendency to act or think in a particular way, but also as (ii) the religious instinct, (iii) the power of the mind to think and understand in a logical way, and (iv) the inner voice or conscience of what is right and wrong in one's conduct or motives that drive the individual towards right action'.70

Islam views humans as creations of God, endowed with the essence of life through the union of body and spirit. This divine gift includes attributes such as faith, an inclination towards goodness, and a need for consistency, and safety.71 This inherent nature is inviolable, with the sanctity of life, freedom, and security being fundamental human rights. Consequently, Islam forbids actions such as murder, colonialism, enslavement, and intimidation, which contradict this natural state. In the realm of I-CSR, corporations bear the responsibility to safeguard this inherent nature, which translates into two key commitments: 1) a commitment to combat violations against humanity and 2) a commitment to the protection of human dignity.72

In the self (nafs) dimension,73 Islam acknowledges individuals as entities possessing both physical and non-physical elements.74 These two aspects are intricately linked, with mental well-being influencing physical health, and vice versa.75 Thus, nurturing the material and spiritual facets of individuals is crucial. From an I-CSR perspective, corporations must address the overall welfare of people, ensuring support for both their physical and spiritual needs.76The fourth dimension, 'aql (intellect), highlights intellect as a cornerstone of human attribute.77 It enables individuals to acquire knowledge, comprehend and apply knowledge in various contexts.78 In the framework of I-CSR, Islamic companies are responsible for nurturing intellectual development through education and the advancement of knowledge. This includes efforts to build individual capabilities and contribute to theoretical and technological advancements.79

The fifth dimension, nasl (lineage or heredity),80 highlights the necessity of ensuring the continuity of society through the birth and proper upbringing of future generations.81 In the context of I-CSR, corporations have a responsibility to support the well-being of future generations. This involves a two-pronged approach: ensuring stable and healthy family systems by improving the quality of life and opportunities available to younger generations.82

The sixth dimension, ijtimā' (society), emphasizes the critical role of social relationships and communal structures. Human beings are inherently social creatures, relying on community interactions to fulfill their life purposes.83 Under I-CSR, companies bear the responsibility to maintain and strengthen social connections. This involves actively engaging with various social groups, fostering harmonious and positive interactions within society.84

The seventh dimension, māl (wealth), emphasizes the importance of acquiring and managing wealth ethically in Islam. Proper ownership and utilization of wealth are central, as they reflect its significance in fulfilling one's obligations to Allah.85 Within the perspective of Islamic Corporate Social Responsibility (I-CSR), while generating profit remains a primary goal for companies,86 the focus shifts towards ensuring that profits are halāl (permissible) and ṭayyib (pure). This involves adherence to sharī'ah principles in all aspects of wealth generation, management, and distribution. Thus, safeguarding wealth in I-CSR entails two primary commitments: the commitment to generating ethical profits and the commitment to protecting assets from corruption and misuse.

The eighth dimension, bī'ah (ecology or environment), highlights the conservation of the environment as a fundamental aspect of the maqāṣid al-sharī'ah (objectives of sharī'ah).87 Humans, as stewards of the Earth (khalīfah fi al-ard), are divinely entrusted with the responsibility to care for the natural world.88 This stewardship implies that while nature serves humanity, it also deserves preservation and respectful treatment.89 The Qur'an provides clear warnings against environmental destruction, affirming the necessity of conservation.90 In I-CSR, environmental stewardship involves two key commitments: first, active participation in conservation efforts to protect and sustain natural resources; and second, support for initiatives and practices that promote ecological well-being.

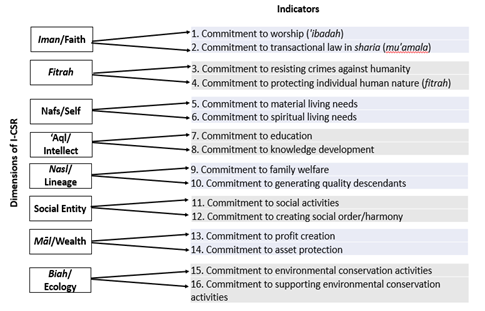

Figure 2. The Indicators of I-CSR

According to Figure 2, the framework of Islamic Corporate Social Responsibility (I-CSR) is derived from Najjar's interpretation of maqāṣid al-sharī'ah. It comprises eight dimensions and 16 commitment indicators. These indicators serve as essential elements for assessing I-CSR, enabling an in-depth evaluation of its various components.

3.2. Ihsān as The Hierarchy of I-CSR

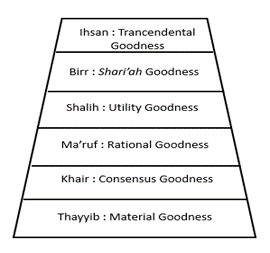

Building on the dimensions of Islamic Corporate Social Responsibility (I-CSR), this section introduces the concept of an I-CSR hierarchy, inspired by Carroll's classification of Western CSR into immoral, amoral, and moral categories.91 This Islamic adaptation is rooted in the principle of ihsān. Theologically, ihsan signifies the state of worshiping God with an awareness of His presence. In the social realm, ihsan represents God-consciousness in all aspects of human interaction and behavior.92 In short, ihsan concerns what is conceptualized as social good or social responsibility categorized into stages such as ṭayyib, khair, ma'rūf, ṣālih, birr, and ihsān,93 as shown in the following figure.

Figure 3. Ihsān as the Hierarchy of I-CSR

The figure 3 discussed highlights different dimensions of social goodness, categorizing them into different types. These include "ṭayyib," which pertains to material benefits; "khair," signifying consensus-driven virtue; "ma'rūf," based on rational considerations; "ṣālih," emphasizing practicality and utility; "birr," rooted in adherence to Sharia; and "ihsān," representing the highest level of goodness tied to transcendental values. On the other hand, undesirable behaviors fall under the "fāsid" category. This framework offers valuable insights into Islamic Corporate Social Responsibility (I-CSR), particularly when viewed through the lens of the "ihsān" hierarchy, and underscores its relevance to guiding corporate behavior.

The term fāsid is used to describe deviations from fairness and justice, whether these deviations are minor or extensive. It contrasts with what is beneficial and virtuous,94 referring to actions that fail to produce positive outcomes. When applied to Islamic Corporate Social Responsibility (I-CSR), a fāsid company is one that either neglects its social responsibilities entirely or conducts its business in a manner where the harm outweighs any potential benefits (maslahat). Following the guiding principles of maqāṣid sharī'ah, I-CSR, emphasizes maximizing benefits (jalb al maṣālih) and minimizing harm (dar'u al mafāsid).95 Therefore, a company that causes substantial harm with little benefit aligns with the definition of a fāsid entity, as it contributes to societal and environmental detriment. The recommended course of action for such a company is either to cease operations or to be suspended to prevent further adverse effects on society and the environment. A complete transformation is required for such entities to resume operations without being a source of harm, ensuring their practices align with ethical and sustainable values.

Secondly, the discourse extends to ṭayyib-type corporations. Thayyib is delineated as a form of goodness that is exclusively material in nature. For illustration, ṭayyib, when referenced in relation to food, denotes items that are not only palatable but also conducive to health.96 Within the Islamic worldview's hierarchy of realities, material aspects are considered the most basic level.97 Consequently, in the context of Islamic Corporate Social Responsibility (I-CSR), ṭayyib-type corporations are acknowledged for their contributions, though they occupy the foundational tier of social responsibility.

Thirdly, corporations are further classified under the khair type. Khair represents a higher form of goodness that transcends ṭayyib. As described by Raghib al-Asfahani, khair embodies qualities that achieve universal approval,98 reflecting consensus-based goodness. From the perspective of Islamic Corporate Social Responsibility (I-CSR), khair-type corporations are those that fulfill their social responsibilities to a level broadly regarded as acceptable by societal standards. For instance, the provision of worship facilities by a corporation might be deemed "sufficiently good' by consensus if such facilities exist. However, questions about the adequacy of these facilities may prompt considerations for advancing to a higher category, namely ma'rūf.

Fourthly, the discourse culminates with the examination of ma'rūf-type corporations, which are characterized by its alignment with rational human considerations and with sharī'ah principles. Raghib al-Asfahani defines ma'rūf as goodness recognized through logic or divine law.99 Unlike other categories, this classification goes beyond basic social responsibility, demanding a superior level of quality of and rationality in its practices. For instance, while a corporation possesses a mosque, rational analysis extends to ensuring essential facilities such as validity of one's prayer, which depends upon the proper performance of ablution, requires the availability of adequate ablution facilities. Similarly, in the context of aiding victims of natural disasters, a ma'rūf-type corporation does more than solicit aid. It implements a well-structured approach to aid, encompassing both programmatic and personnel frameworks to effectively address disaster relief. Thus, in the I-CSR model, ma'rūf-type corporations are held in higher regard than the khair category, reflecting a higher valuation of their social responsibility endeavors. Fifthly, the discourse introduces ṣālih-type corporations. The term "ṣālih' shares its etymological roots with "maslahat," highlights righteousness as the result of actions that generate beneficial outcomes. It transcends the ma'rūf category by evaluating social goodness, through practical and tangible benefits rather than just rational consensus. Differing from the pragmatic and utilitarian outlooks of Western philosophy,100 this perspective is rooted in scriptural references that align righteous acts with faith. These actions, when performed by believers, are thought to yield benefits in both the temporal and eternal dimensions.101 Conversely, righteousness manifested by non-believers is acknowledged to contribute positively, albeit confined to worldly benefits.102 Within the framework of Islamic Corporate Social Responsibility (I-CSR), ṣālih-type corporations are those that manifest their social responsibility through a deliberate focus on the resultant benefits. Technically, these corporations are expected to design and maintain management systems ensuring that social benefits are appropriately directed to the deserving recipients. For instance, providing worship facilities alone is insufficient; these corporations must implement effective management systems to ensure that these facilities serve their intended purpose for the rightful users. The sixth and highest level explores birr-type corporations, which set the benchmark for sharī'ah-compliant social responsibility. Asfahani explains birr as complete obedience to Islamic law, requiring that every act of kindness aligns with sharī'ah mandates.103 The evaluative criteria for birr-type entities extend beyond the mere assessment of benefits, questioning whether an act of kindness aligns with Islamic sharī'ah. For instance, corporate meetings conflicting with prayer times must be rescheduled. Similarly, charitable efforts must follow Islamic guidelines, ranging from obligatory zakat to voluntary acts like waqf, infaq, sadaqah, and gifts, always adhering to sharī'ah stipulations regarding eligibility and execution. Companies of the birr category serve as exemplars of I-CSR implementation, where sharī'ah is the foremost guide in all social endeavors.

Seventhly, the concept of Ihsān-type companies represents the highest level of goodness within the Islamic Corporate Social Responsibility (I-CSR) framework. The essence of Ihsān, deeply rooted in a profound coneection with Allah, transcends basic compliance, incorporating a spiritual essence where actions are carried out with a deep consciousness of Allah's constant presence.104 Al Nawawi defines Ihsān as worshipping Allah as though one sees Him, or at least with the unwavering belief that Allah is always watching.105 This perspective fosters an introspective attitude, driven solely by the desire to please Allah, devoid of any intention to impress others or to get worldly rewards.

Philosophically, Ihsān-type corporations resonate with the Islamic epistemological framework and worldview, which centers on supremacy of Allah and embraces ma'rifah —the divine knowledge imparted to humanity.106 This alignment confirms the legitimacy of the Ihsān-type approach to corporate social responsibility (CSR), affirming its legitimacy as directly sanctioned by Allah. Just as ma'rifah, or divine knowledge, is determined in its scope and form by Allah's will,107 as well as the nature and extent of social responsibilities under the Ihsān category aligned with divine will. Consequently, Ihsān-type companies transcend traditional CSR, embodying a commitment rooted in spiritual purity and adherence to sharī'ah.108 They signify a paradigmatic shift in I-CSR, incorporating accountability to Allah alongside responsibilities toward society and the environment.

Although Ihsān-type corporations cannot be assessed using traditional categorization scale, their role within the Islamic Corporate Social Responsibility (I-CSR) system is apparent.109 These enterprises demonstrate an unwavering commitment to social welfare, driven by a profound spiritual accountability to Allah, rather than the pursuit of profit or human acclaim.

One notable example is a livestock company in Tafahna al-Ashraf, Egypt, founded by Ir Ṣalāh Aṭiyah and eight of his friends, who took the initiative to engage in animal husbandry. Uniquely, they incorporated God as the tenth member of their partnership, formalizing an agreement that allocated a share of profits to God. Over time, the company continued to flourish, and God's share of the profits increased annually, growing from 10% to 20%, until eventually, 100% of the company's profits were dedicated to God.110 This arrangement signifies that the founders ceased to be shareholders, operating instead as employees of the company, making this venture an exemplary model of Ihsān. All of the company's proceeds are dedicated to human welfare in accordance with God's regulations.

Similarly, Al-Azhar University stands out for its centuries-long tradition of offering scholarships to its students for hundreds of years. This enduring success is attributed to the effective management of its waqf, which has been made productive through various means, including the establishment of a company.111 In Indonesia, there are still many similar companies such as Muhammadiyah; 112 Nahdhatul Ulama'; 113 and institutions under Pondok Modern Darussalam Gontor, Ponorogo, Indonesia. 114 These companies are not privately owned but belong to organizations with waqf status, using their profits entirely to serve the people in accordance with God's commands. These are among the examples of Islamic companies developing in Muslim countries; which can be expected to be real examples of I-CSR implementation.

The key point highlighted by these examples is that Ihsān-type companies are not motivated by the desire for human validation. Instead, their operations are driven by a desire for divine acceptance, with every business decision and profit directed toward fulfilling Allah's commandments and serving the community. Based on the details provided, it becomes evident that the concept of social good in Islam encompasses multiple levels. When these levels are compared to a company's conduct in adopting Islamic Corporate Social Responsibility (I-CSR), it facilitates the categorization of companies into distinct types: ṭayyib, khair, ma'rūf, ṣālih, birr, and ihsān.

3.3. Constructing a Conceptual Framework

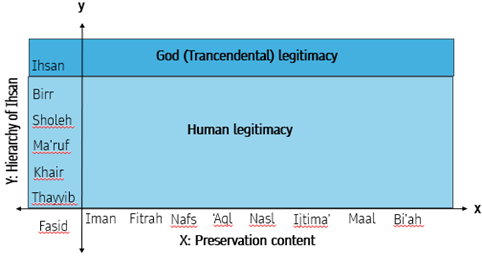

To be able to operate, it is necessary to create an I-CSR conceptual framework based on the integration of the concepts of maqāṣid sharī'ah and ihsān. The diagram below illustrates how these concepts can be integrated to form a comprehensive approach to corporate social responsibility within an Islamic context.

Figure 4. The Conceptual Framework of I-CSR

Figure 4 illustrates the Integrated Corporate Social Responsibility (I-CSR) model, which is based on a variety of concepts. Initially, it incorporates the principle of maqāṣid sharī'ah. As detailed in the preceding section, the development of this model is influenced by the perspectives of Abdul Madjid An-Najjar. The I-CSR framework comprises eight dimensions: Īmān, Fitrah, Nafs, Aql, Nasl, Ijtimā', Māl, and Bī'ah. Each dimension is further broken down into various indicators, with specific questions created to evaluate the application of I-CSR within a corporate environmental setting.

The second key component of the model is the I-CSR hierarchy, which is based on the concept of Ihsan and includes categories such as Ṭayyib, Khair, Ma'rūf, Ṣālih, Birr, and Ihsān. These categories are crucial in evaluating a company's performance across the dimensions of I-CSR. Observing this framework, it is clear that not all companies can achieve the "birr" or "ihsān" levels. Due to the secular nature of I-CSR metrics, few companies can attain the top levels of the hierarchy, with most only reaching "ma'rūf" or "ṣālih". This highlights the unique aspect of the I-CSR model, with its highest standards being nearly unreachable, unlike other CSR models.

4. Conclusion and Recommendation for Future Studies

This research has uncovered several significant findings related to Islamic Corporate Social Responsibility (I-CSR). First, it identifies key dimensions of I-CSR derived from maqāsid shariah, including Īmān (faith), fitrah (natural disposition), nafs (self), 'aql (intellect), nasl (lineage), ijtimā' (society), māl (wealth), and bī'ah (environment). Second, it categorizes companies into seven types based on their I-CSR performance: fāsid (corrupt), ṭayyib (kind), khair (good), ma'rūf (favorable), ṣālih (beneficial), birr (righteous), and ihsān (benevolence).

Despite these findings, the research acknowledges certain limitations. It primarily relies on two theoretical frameworks —maqāsid sharī'ah and ihsān—that integrating additional Islamic concepts such as maṣlaḥah (public interest) and maqāsid 'aqīdah (objectives of faith). Furthermore, the conceptual model remains in its early stages, requiring further refinement of its indicators for comprehensive evaluation. Future research directions could focus on include enhancing the assessment tool to a level that allows for practical application.

In conclusion, this research provides valuable insights by introducing a novel I-CSR model that is deeply rooted in Islamic principles. Moreover, the study's implications extend to refining I-CSR assessment methods and advocating for a multidisciplinary approach that incorporates expertise from various scientific domains to establish a robust evaluation framework.

Conflict of Interest

The author of the manuscript has no financial or non-financial conflict of interest in the subject matter or materials discussed in this manuscript.

Data Availability Statement

The data associated with this study will be provided by the corresponding author upon request.

Funding Details

The current research received financial support by the Republic of Indonesia’s Ministry of Education and Culture through its Higher Education grant for the fiscal year 2024-2025. Contract number: 109/E5/PG.02.00.PL/2024, 059/SP2H/PT/LL7/2024, 24/UNIDA/LPPM-PE-y/XII/1445

Bibliography

Abu Faris, Hamzah. "Al Madkhal Ilā Dirāsah 'Ilmi Maqāṣid Al Sharī'ah Al Islāmiyah (The Introduction to the Study of Objectives of Islamic Law)." Tharabuls-Libya: Daar Ibn Hazm, 2012. https://doi.org/978-9959-823-34-2

Actforhumanity. Biografi Ir. Sholah Athiyah (Biography of Ir. Sholah Athiyah). Indonesia, n.d. https://www.youtube.com/watch?v=nBgvH3oGze0.

Afif, Mufti. "Corporate Social Responsibility dalam Perspektif Islam (Corporate Social Responsibility in Islamic Perspective)." Islamic Economic Journal 3, no. 2 (2017): 145–59. https://doi.org/10.21111/iej.v3i2.2716

Ahmad, Muhamad Fazil. "Corporate Social Responsibility Management (CSRM) With Islamic Philanthropy Concept For Enhancing Mudarabah Family Takaful Model In Malaysia." AZKA International Journal of Zakat and Social Finance 2, no. 1 (2021): 179–96. https://doi.org/10.51377/azjaf.vol2no1.49.

Al-Asfahani, Husain Raghib. Mu'jam Mufradātu Alfādz Al Qur'ān (Dictionary of Qur'anic Word), n.d.

Al-Attas, Syed Muhamed Naquib. Islam dan Filsafat Sains. Bandung: Mizan, 1995.

Al-Attas, Syed Muhammad Naquib. "Islam: The Concept of Religion and the Foundation of Ethics and Morality." In Prolegomena to The Metaphysics of Islam: An Exposition of the Fundamental Elements of the Worldview of Islam, 358. Kuala Lumpur: International Institute of Islamic Thought and Civilization (ISTAC), 1995.

—. Islam and Secularism. 2nd ed. Kuala Lumpur: ISTAC, 1993.

—. "Islam and the Philosophy of Science." In Prolegomena to The Metaphysics of Islam: An Exposition of the Fundamental Elements of the Worldview of Islam, 385. Kuala Lumpur: International Institute of Islamic Thought and Civilization (ISTAC), 1995.

—. "The Nature of Man and the Psychology of the Human Soul." In Prolegomena to The Metaphysics of Islam: An Exposition of the Fundamental Elements of the Worldview of Islam, 1995.

Ammrullah, Khasib., Usmanul Khakim, and Rakhmad Agung Hidayatullah. Islamisasi Teori Motivasi Pada Menejemen Bisnis Barat: Sebuah Elaborasi Worldview Islam Dan Barat (Islamisation of Motivation Theory in Western Business Management: An Elaboration of Islamic and Western Worldviews). Edited by Ahmad Farid Saifuddin. Ponorogo: Unida Gontor Press, 2023.

Amrullah, Khasib., Mulyono Jamal, Usmanul Khakim, Eko Nur Cahyo, and Khurun'in Zahro'. "The Concept of Waqf From Worldview Theory: The Study of Sharia-Philosophy." ULUL ALBAB Jurnal Studi Islam 23, no. 1 (2022): 22–41. https://doi.org/10.18860/ua.v23i1.15694.

Arif, Syamsuddin. "Rethinking the Concept of Fiṭra: Natural Disposition, Reason and Conscience." American Journal of Islam and Society 40, no. 3–4 (2023): 77–103 https://doi.org/10.35632/ajis.v40i3-4.3189.

Ascarya, and Atika Rukminastiti Masrifah. "Developing Maqasid Index for Islamic CSR: The Case of Ummah's Endowment Fund in Indonesia." International Journal of Islamic and Middle Eastern Finance and Management 16, no. 4 (2023): 835–55. https://doi.org/10.1108/IMEFM-12-2021-0474.

Baden, Denise. "A Reconstruction of Carroll's Pyramid of Corporate Social Responsibility for the 21st Century." International Journal of Corporate Social Responsibility 1, no. 1 (2016): 0–15. https://doi.org/10.1186/s40991-016-0008-2.

Badria, Nuril, Eko Ganis Sukoharsono, and Lilik Purwanti. "Business Sustainability and Pentuple Bottom Line: Building the Hierarchical Pyramid of the Pentuple Bottom Line." International Journal of Research in Business and Social Science (2147- 4478) 10, no. 3 (2021): 123–31. https://doi.org/10.20525/ijrbs.v10i3.1156.

Bloor, Michael., and Fiona Wood. Keyword in Qualitative Method. London: SAGE Publications, 2006.

Brin, Pavlo., and Mohamad Nassif Nehme. "Corporate Social Responsibility: Analysis of Theories and Models." EUREKA: Social and Humanities 5, no. 5 (2019): 22–30. https://doi.org/10.21303/2504-5571.2019.001007.

Carroll, Archie B. "A History of Corporate Social Responsibility: Concepts and Practices." The Oxford Handbook of Corporate Social Responsibility, no. October (2009). https://doi.org/10.1093/oxfordhb/9780199211593.003.0002.

Carroll, Archie B. "The Pyramid of Corporate Social Responsibility: Toward Organizational Stakeholders." Bisiness Horizon 112, no. 44 (1991): 31–48. http://dx.doi.org/10.1016/0007-6813(91)90005.

Dusuki, Asraf, and Nurdianawati Abdullah. "Maqasid Al-Shari`ah, Maslahah, and Corporate Social Responsibility (Objectives of Islamic Law, Public Interests and Corporate Social Responsibility)." The American Journal of Islamic Social Sciences 24, no. 01 (2007): 25–45. http://www.scirp.org/journal/doi.aspx?DOI=10.4236/ib.2014.63013.

Dusuki, Asyraf Wajdi. "Corporate Social Responsbility of Islamic Banking in Malaysia: A Synthesis of Islamic and Stakeholder' Perspectives." Loughborough University, 2005.

—. "What Does Islam Say About Corporate Social Responsibility ( CSR )?" Review Literature And Arts of The Americas 12, no. 1 (2008): 1–28. https://www.researchgate.net/publication/237104927_What_Does_Islam_Say_about_Corporate_Social_Responsibility

Ehie, Ike C. "Examining the Corporate Social Responsibility Orientation in Developing Countries: An Empirical Investigation of the Carroll's CSR Pyramid." International Journal of Business Governance and Ethics 11, no. 1 (2016): 1–20. https://doi.org/10.1504/IJBGE.2016.076337.

Elasrag, Hussein. "Corporate Social Responsibility in Islam." SSRN Electronic Journal, no. April (2015). 25-35 https://doi.org/10.2139/ssrn.2593945.

Elkington, John. Cannibals with Forks: The Triple Bottom Line of 21st Century Business. Capstone. Vol. 1. Oxford UK: Capstone, 1997.

Ermawati, Siti Musyahidah., and Nurdin. "Muslim Society Perspective on Islamic Banking Corporate Social Responsibility in Indonesia (Based on Qur'an and Hadits Economic Themes)." International Journal of Business and Management Review 9, no. 3 (2021): 29–40. www.eajournals.org @ECRTD-UK.

Fauzan, Shalih. Kitāb Tauhīd (Book of Unification). Edited by Trans. Agus Hasan Bashori. Jakarta: Darul Haq, 2000.

Fauziah, Eva., Ifa Hanifia Senjiati, and Zaini Abdul Malik. "Penerapan Corporate Social Responsibility (CSR) Pendidikan di Perbankan Syariah (Implementation of Corporate Social Responsibility (CSR) for Education in Islamic Banking)." In Prosiding SNaPP2016 Sosial, Ekonomi, Dan Humaniora, 41–48, 2016. ISSN: 2089-3590 EISSN: 2303-2472

Friedman, Milton. "The Social Responsibility of Business Is to Increase Its Profits." The New York Time Magazine. New Jersey, 1970. https://link.springer.com/chapter/10.1007/978-3-540-70818-6_14.

Gutterman, Alan S. "Research and Development." SSRN Electronic Journal 12, no. 2 (2023): 40–41. https://doi.org/10.12968/npre.2007.5.5.23745

Hadi, Abdul. "Konsep Dan Praktek Kesehatan Berbasis Ajaran Islam (Concepts and Practices of Health Based on Islamic Teachings)." Al-Risālah 11, no. 2 (2020): 53–70. https://doi.org/10.34005/alrisalah.v11i2.822.

Hartman, Laura., and Joseph DesJardins. Business Ethics: Decision-Making for Personal Integrity & Social Responsibility. 4th ed. New York: Mc Graw Hill Education, 2018. http://www.amazon.com/Business-Ethics-Decision-Making-Integrity-Responsibility/dp/0078137136.

Hasiah, and Shafra. "Makanan Sehat Dalam Al-Qur'an Menurut Pedagang Masakan Di Kota Padangsidimpuan (Healthy Food in the Qur'an According to Cookery Traders in Padangsidimpuan City)." El Fawatih 3, no. 2 (2022): 1–23. https://doi.org/10.24952/alfawatih.v3i2.6237

Hassan, Abul., and Hjh Salma Binti Abdul Latiff. "Corporate Social Responsibility of Islamic Financial Institutions and Businesses: Optimizing Charity Value." Humanomics 25, no. 3 (2009): 177–88. https://doi.org/10.1108/08288660910986900.

Ibn Manzur, Abi al Fadhil Jamaluddin Ibn Muhammad Ibn Makrami. Lisān Al 'Arab (Tongue (Words) of Arab) (Beirut: Dār Sādir, n.d.).

Ibrahim, Othman, Siti Z. Melatu Samsi, and M. Fazil Ahmad. "Halal Business Corporate Social Responsibility." International University Social Responsibility Conference and Exhibition, no. October (2010): 1–5.

Ihsan, Nur Hadi, Khasib Amrullah, Usmanul Khakim, and Hadi Fatkhurrizka. "Hubungan Agama Dan Sains: Telaah Kritis Sejarah Filsafat Sains Islam Dan Modern (The Relationship of Religion and Science: A Critical Examination of the History of Islamic and Modern Philosophy of Science)." Intizar 27, no. 2 (2021): 97–111. https://doi.org/10.19109/intizar.v27i2.9527.

Islam, Azizul Muhammad, and Craig Deegan. "Motivations for an Organisation within a Developing Country to Report Social Responsibility Information: Evidence from Bangladesh." Accounting, Auditing and Accountability Journal 21, no. 6 (2008): 850–74. https://doi.org/10.1108/09513570810893272.

Khakim, Usmanul. "Islamic Worldview-Based Corporate Social Responsibility." Universitas Darussalam Gontor, 2024.

—. "Syed Muhammad Naquib Al-Attas' Theory of Worldview of Islam and Its Significance on Islamization of Pesent-Day Knowledge." UNIDA Gontor, 2020.

Khakim, Usmanul., Teguh Kurniyanto, Mahendra Utama Cahya Ramadhan, Muhammad Habiburrahman, and Muhammad Iksan Rahmadian. "God and Worldview According to Al-Attas and Wall." Tsaqafah 16, no. 2 (2020): 223–44. https://doi.org/10.21111/tsaqafah.v16i2.4853.

Khurshid, Muhammad Adnan., Abdulrahman Al-Aali, Ahmed Ali Soliman, and Salmiah Mohamad Amin. "Developing an Islamic Corporate Social Responsibility Model (ICSR)." Competitiveness Review 24, no. 4 (2014): 258–74. https://doi.org/10.1108/CR-01-2013-0004.

Lahuri, Setiawan bin. "Corporate Social Responsisbility Dalam Perspektif Islam (Corporate Social Responsisbility in Islamic Perspective)." Ijtihad : Jurnal Hukum Dan Ekonomi Islam 7, no. 2 (2013): 219–38.

Al-Mahalli, Jalāluddīn., and Jalāluddīn Al Suyuthi, Tafsīr Jalālain (Interpretation of Jalalain) (Cairo: Dār Hadīst, n.d.).

Maiaweng, Peniel C.D. "Manfaat Kebenaran Perbuatan: Suatu Analisis Terhadap Ajaran Filsafat Pragmatisme (The Benefits of Righteous Actions: An Analysis of the Philosophical Teachings of Pragmatism)." Jurnal Jaffray 11, no. 1 (April 2, 2013): 1. https://doi.org/10.25278/jj71.v11i1.69.

Mais, Rimi Gusliana., S. Eko Ganis, Aulia Fuad Rahman, and Aji Dedi Mulawarman. "Building Concept of Corporate Social Responsibility Reporting through Islamic Perspective on Sharia Bank." International Journal of Economic Research 14, no. 17 (2017): 107–32.

Masrina, Dewi Maharani., and Verina Ayustrialni. "Konsep Harta Aan Kepemilikan Dalam Prespektif Ekonomi Islam (The Concept of Treasure and Ownership in the Islamic Economic Perspective)." Jurnal Ilmiah Ekonomi Islam 9, no. 01 (2023): 7–8.

Masruchin. "Wakaf Produktif Dan Kemandirian Pesantren: Study Tentang Pengelolaan Wakaf Produktir Di Pondok Modern Darussalam Gontor Ponorogo (Productive Waqf and Pesantren Sutainability: A Study of Productive Waqf Management at Pondok Modern Darussalam Gontor Ponorog." UIN Surabaya, 2014.

Maya, Rahendra. "Penafsiran Al-Sa'dî Tentang Konsep Al-Taskhîr (Al-Sa'dî's Interpretation of the Concept of Al-Taskhîr)." Al - Tadabbur: Jurnal Ilmu Al-Qur'ān Dan Tafsir 2, no. 03 (2017): 1–24. https://doi.org/10.30868/at.v2i03.192.

Mohamad, Rusnah., and Mohd Rizal Muwazir Mukhazir. "Corporate Social Responsibility and Islamic Business Organizations: A Proposed Model." Islamic Finance and Business Review 3, no. 1 (2008): 30–42 DOI:10.30993/tifbr.v3i1.20

Mohammed, Jawed Akhtar. "Corporate Social Responsibility in Islam." Auckland University of Technology, 2007. https://doi.org/10.2139/ssrn.2593945.

Muslih, M., Nur Ihsan, Usmanul Khakim, and Winda Roini. "Lakatosian Perspective of Islamic Science Research Programmes (Case: Islamization in Welfare Theory)," 2019, 1–8. https://doi.org/10.4108/eai.10-9-2019.2289377.

Muslih, M. Kholid. Worldview Islam (Worldview of Islam) Ponorogo: Pusat Islamisasi Ilmu (PII) dan Unida Gontor Press, 2018.

Muslihati, Muslihati., Siradjuddin Siradjuddin, and Syahruddin Syahruddin. "Corporate Social Responsibility (CSR) Dalam Perspektif Ekonomi Islam Pada Bank Syariah (Corporate Social Responsibility (CSR) in the Perspective of Islamic Economics at Islamic Banks)." Jurnal Hukum Ekonomi Syariah 2, no. 1 (2018): 29–42. https://doi.org/10.26618/j-hes.v2i1.1390.

Naderian, Anahita., and Rohaizat Baharun. "Corporate Social Responsibility and Consumer Behavior." Asian Journal of Management 6, no. 4 (2015): 225-249. https://doi.org/10.5958/2321-5763.2015.00036.0.

Al-Najjār, Abdul Majīd. "Maqāṣid Sharī'ah bi Ab'ād Jadīdah (The Objective of Islamic Law in a New Dimensions)." Beirut: Daar Gharb al Islamy, 2008.

Nalband, Nisar Ahamad., and Saad Al Kelabi. "Redesigning Carroll's CSR Pyramid Model." Journal of Advanced Management Science 2, no. 3 (2014): 236–39. https://doi.org/10.12720/joams.2.3.236-239.

Nawawi, Muhyiddin Yahya Ibn Syaraf Al. Hadīth Arba'īn Nawawiyah (Nawawiah Fourty Prophetic Traditions). Edited by Abdullah Haidir. Edisi Terj. Riyadh: al Maktab al Ta'awwuni li ad da'wah wa Tau'iyah al Jaliyah, 2007.

Nurdin, Azlinda Boheran., and Mohd Rohiman Subri. "The Impact of Islamic-Based Corporate Social Responsibility Practice Toward Employees." Asian People Journal 4, no. 1 (2021): 65–83. http://dx.doi.org/10.37231/apj.2021.4.1.253

OCDE. Frascati Manual 2015: Guidelines for Collecting and Reporting Data on Research and Experimental Development. The Measurement of Scientific, Technological and Innovation Activities. Paris: OECD Publishing, 2015. https://doi.org/https://doi.org/10.1787/24132764.

Paryadi. "Maqashid Syariah : Definisi Dan Pendapat Para Ulama (Maqashid Sharia: Definitions and Conceptions of Scholars)." Cross-Border 4, no. 2 (2021): 201–16.

PBNU. Anggaran Dasar Dan Anggaran Rumah Tangga Nahdlatul Ulama Keputusan Muktamar Ke-34 NU Lampung. Jakarta: Pengurus Besar Nahdhatul Ulama', 2022.

Pimpinan Pusat Muhammadiyah. "Anggaran Dasar Dan Anggaran Rumah Tangga Muhammadiyah." Yogyakarta: Pimpinan Pusat Muhammadiyah, 2019.

Al-Raisuni, Ahmad. Al Dzarī'ah Ila Maqāṣid Al Sharī'ah (The Pretext to the Objectives of Islamic Law). Cairo: Daar Kalim, 2016.

Rivai, Zainal. Veithzal, and Chusnul Indah Lupitasari. "Model Pengelolaan Wakaf Produktif Di Pondok Modern Darussalam Gontor Dan Perannya Terhadap Pengembangan Universitas Darussalam Gontor (Productive Waqf Management Model at Pondok Modern Darussalam Gontor and Its Role in the Development of Darussalam Gontor." Al-Awqaf 10, no. 1 (2017): 69–79. https://doi.org/10.47411/al-awqaf.v10i1.48

Salim, Mohammad Syam'un. Al Attas on Reality. University of Darussalam Gontor, 2019.

Samindjaya, Syahruddin Sumardi., Abdelkader Laallam, Fahmi Ali Hudaefi, Bechir Mahamat Issa, Saidi Ouassaf, and Mohamed Imad Oussedik. "Imam Zarkasyi's Contribution to Indonesia's Modern Waqf Education System." Journal of Islamic Thought and Civilization 14, no. 1 (2024): 74–91. https://doi.org/10.32350/jitc.141.05.

Saryono. "Konsep Fitrah Dalam Perspektif Islam (Fitrah on Islamic Perspective)." Jurnal Studi Islam 14, no. 2 (2016): 11–12. http://jurnal.radenfatah.ac.id/index.php/medinate.

Sayed Ahmed, Nael Y. M., and Samir A. Abu Zaid. "Sustainable Development and Social Responsibility from an Islamic Perspective." Journal of Social and Political Sciences 2, no. 4 (2019): 1–20. https://doi.org/10.31014/aior.1991.02.04.135.

Schwartz, M.S., and Archie B Carroll. "Corporate Social Responsibility: A Three-Domain Approach." Business Ethics Quartely 13, no. 4 (2014): 503–30. https://doi.org/10.2307/3857969"

Triyuwono, Iwan. "Taqwa: Deconstructing Triple Bottom Line (TBL) to Awake Human's Divine Consciousness." Pertanika Journal of Tropical Agricultural Science 24, no. May (2016): 20–35. http://119.40.116.186/pjtas/browse/regular-issue?article=JSSH-S0194-2016.

Wagner-Tsukamoto, Sigmund. "In Search of Ethics: From Carroll to Integrative CSR Economics." Social Responsibility Journal 15, no. 4 (2019): 469–91. https://doi.org/10.1108/SRJ-09-2017-0188.

Weruin, Urbanus Ura. "Teori-Teori Etika dan Sumbangan Pemikiran Para Filsuf Bagi Etika Bisnis (Ethical Theories and Philosophers' Contributions to Business Ethics)." Jurnal Muara Ilmu Ekonomi dan Bisnis 3, no. 2 (2019): 313. https://doi.org/10.24912/jmieb.v3i2.3384.

Zafar, Muhammad Bilal., and Ahmad Azam Sulaiman. "Corporate Social Responsibility and Islamic Banks: A Systematic Literature Review." Management Review Quarterly 69, no. 2 (2019): 159–206. https://doi.org/10.1007/s11301-018-0150-x.

Zahid, Md Anowar., and Kamal Halili Hassan. "Corporate Social Responsibility to Employees: Considering Common Law Vis-à-Vis Islamic Law Principles." Pertanika Journal of Social Science and Humanities 20, no. SPEC. ISS. (2012): 87–100. https://ssrn.com/abstract=2750264

Zarkasyi, Hamid Fahmy. Minhaj (Way). 2nd ed. Jakarta: INSIST, 2021.

1Archie B Carroll, "The Pyramid of Corporate the Moral Management of Social Responsibiiity: Toward Organizational Stakeholders," Bisiness Horizon 112, no. 44 (1991): 31–48.

2Ibid., 40–42.

3Nisar Ahamad Nalband, and Saad Al Kelabi, "Redesigning Carroll's CSR Pyramid Model," Journal of Advanced Management Science 2, no. 3 (2014): 236–39, https://doi.org/10.12720/joams.2.3.236-239.

4M.s. Schwartz, and Archie B Carroll, "Corporate Social Responsibility: A Three-Domain Approach," Business Ethics Quartely 13, no. 4 (2014): 503–30, https://doi.org/10.2307/3857969.

5Anahita Naderian, and Rohaizat Baharun, "Corporate Social Responsibility and Consumer Behavior," Asian Journal of Management 6, no. 4 (2015): 249, https://doi.org/10.5958/2321-5763.2015.00036.0.

6Denise Baden, "A Reconstruction of Carroll's Pyramid of Corporate Social Responsibility for the 21st Century," International Journal of Corporate Social Responsibility 1, no. 1 (2016): 0–15, https://doi.org/10.1186/s40991-016-0008-2.

7Ike C. Ehie, "Examining the Corporate Social Responsibility Orientation in Developing Countries: An Empirical Investigation of the Carroll's CSR Pyramid," International Journal of Business Governance and Ethics 11, no. 1 (2016): 1–20, https://doi.org/10.1504/IJBGE.2016.076337.

8Pavlo Brin, and Mohamad Nassif Nehme, "Corporate Social Responsibility: Analysis of Theories and Models," EUREKA: Social and Humanities 5, no. 5 (2019): 22–30, https://doi.org/10.21303/2504-5571.2019.001007.

9Sigmund Wagner-Tsukamoto, "In Search of Ethics: From Carroll to Integrative CSR Economics," Social Responsibility Journal 15, no. 4 (2019): 469–91, https://doi.org/10.1108/SRJ-09-2017-0188.

10Asyraf Wajdi Dusuki, "Corporate Social Responsbility of Islamic Banking in Malaysia: A Synthesis of Islamic and Stakeholder' Perspectives" (Loughborough University, 2005); Asyraf Wajdi Dusuki, "What Does Islam Say About Corporate Social Responsibility ( CSR )?," Review Literature And Arts Of The Americas 12, no. 1 (2008): 1–28.

11Jawed Akhtar Mohammed, "Corporate Social Responsibility in Islam" (Auckland University of Technology, 2007), 102–28, https://doi.org/10.2139/ssrn.2593945.

12Muhammad Adnan Khurshid et al., "Developing an Islamic Corporate Social Responsibility Model (ICSR)," Competitiveness Review 24, no. 4 (2014): 258–74, https://doi.org/10.1108/CR-01-2013-0004.

13Carroll, "The Pyramid of Corporate the Moral Management of Social Responsibiiity: Toward Organizational Stakeholders," 44–45.

14Mohammed, "Corporate Social Responsibility in Islam."

15Dusuki, "What Does Islam Say About Corporate Social Responsibility ( CSR )?"

16Abul Hassan and Hjh Salma Binti Abdul Latiff, "Corporate Social Responsibility of Islamic Financial Institutions and Businesses: Optimizing Charity Value," Humanomics 25, no. 3 (2009): 177–88, https://doi.org/10.1108/08288660910986900.

17Othman Ibrahim, Siti Z. Melatu Samsi, and M. Fazil Ahmad, "Halal Business Corporate Social Responsibility," International University Social Responsibility Conference and Exhibition, no. October (2010): 1–5.

18Md Anowar Zahid and Kamal Halili Hassan, "Corporate Social Responsibility to Employees: Considering Common Law Vis-à-Vis Islamic Law Principles," Pertanika Journal of Social Science and Humanities 20, no. SPEC. ISS. (2012): 87–100.

19Setiawan bin Lahuri, "Corporate Social Responsisbility Dalam Perspektif Islam (Corporate Social Responsisbility in Islamic Perspective)," Ijtihad : Jurnal Hukum Dan Ekonomi Islam 7, no. 2 (2013): 219–38.

20Khurshid et al., "Developing an Islamic Corporate Social Responsibility Model (ICSR)."

21Hussein Elasrag, "Corporate Social Responsibility in Islam," SSRN Electronic Journal, no. April (2015), https://doi.org/10.2139/ssrn.2593945.

22Mufti Afif, "Corporate Social Responsibility Dalam Perspektif Islam (Corporate Social Responsibility in Islamic Perspective)," Islamic Economic Journal 3, no. 2 (2017): 145–59.

23Rimi Gusliana Mais et al., "Building Concept of Corporate Social Responsibility Reporting through Islamic Perspective on Sharia Bank," International Journal of Economic Research 14, no. 17 (2017): 107–32.

24Muslihati Muslihati, Siradjuddin Siradjuddin, and Syahruddin Syahruddin, "Corporate Social Responsibility (CSR) Dalam Perspektif Ekonomi Islam Pada Bank Syariah (Corporate Social Responsibility (CSR) in the Perspective of Islamic Economics at Islamic Banks)," Jurnal Hukum Ekonomi Syariah 2, no. 1 (2018): 29–42, https://doi.org/10.26618/j-hes.v2i1.1390.

25Nael Y. M. Sayed Ahmed and Samir A. Abu Zaid, "Sustainable Development and Social Responsibility from an Islamic Perspective," Journal of Social and Political Sciences 2, no. 4 (2019): 1–20, https://doi.org/10.31014/aior.1991.02.04.135.

26Ermawati, Siti Musyahidah, and Nurdin, "Muslim Society Perspective on Islamic Banking Corporate Social Responsibility in Indonesia (Based on Qur'ān and Hadīts Economic Themes)," International Journal of Business and Management Review 9, no. 3 (2021): 29–40, www.eajournals.org @ECRTD-UK.

27Dusuki, "Corporate Social Responsbility of Islamic Banking in Malaysia: A Synthesis of Islamic and Stakeholder' Perspectives."

28Azizul Muhammad Islam and Craig Deegan, "Motivations for an Organisation within a Developing Country to Report Social Responsibility Information: Evidence from Bangladesh," Accounting, Auditing and Accountability Journal 21, no. 6 (2008): 850–74, https://doi.org/10.1108/09513570810893272.

29Hassan and Salma Binti Abdul Latiff, "Corporate Social Responsibility of Islamic Financial Institutions and Businesses: Optimizing Charity Value."

30Eva Fauziah, Ifa Hanifia Senjiati, and Zaini Abdul Malik, "Penerapan Corporate Social Responsibility (CSR) Pendidikan Di Perbankan Syariah (Implementation of Corporate Social Responsibility (CSR) for Education in Islamic Banking)," in Prosiding SNaPP2016 Sosial, Ekonomi, Dan Humaniora, 2016, 41–48.

31Muhammad Bilal Zafar and Ahmad Azam Sulaiman, "Corporate Social Responsibility and Islamic Banks: A Systematic Literature Review," Management Review Quarterly 69, no. 2 (2019): 159–206, https://doi.org/10.1007/s11301-018-0150-x

32Muhamad Fazil Ahmad, "Corporate Social Responsibility Management (CSRM) With Islamic Philanthropy Concept For Enhancing Mudarabah Family Takaful Model In Malaysia," AZKA International Journal of Zakat & Social Finance 2, no. 1 (2021): 179–96, https://doi.org/10.51377/azjaf.vol2no1.49.

33Ermawati, Musyahidah, and Nurdin, "Muslim Society Perspective on Islamic Banking Corporate Social Responsibility in Indonesia (Based on Qur'ān and Hadīts Economic Themes)."

34Azlinda Boheran Nurdin and Mohd Rohiman Subri, "The Impact of Islamic-Based Corporate Social Responsibility Practice Toward Employees," Asian People Journal 4, no. 1 (2021): 65–83.

35Ascarya and Atika Rukminastiti Masrifah, "Developing Maqasid Index for Islamic CSR: The Case of Ummah's Endowment Fund in Indonesia," International Journal of Islamic and Middle Eastern Finance and Management 16, no. 4 (2023): 835–55, https://doi.org/10.1108/IMEFM-12-2021-0474.

36Asraf Dusuki and Nurdianawati Abdullah, "Maqāṣid Sharī'ah, Maṣlahah, and Corporate Social Responsibility (Objectives of Islamic Law, Public Interests and Corporate Social Responsibility)," The American Journal of Islamic Social Sciences 24, no. 01 (2007): 25–45, http://www.scirp.org/journal/doi.aspx?DOI=10.4236/ib.2014.63013.

37Rusnah Mohamad and Mohd Rizal Muwazir Mukhazir, "Corporate Social Responsibility and Islamic Business Organizations: A Proposed Model," Islamic Finance and Business Review 3, no. 1 (2008): 30–42.

38Khurshid et al., "Developing an Islamic Corporate Social Responsibility Model (ICSR)."

39Iwan Triyuwono, "Taqwā: Deconstructing Triple Bottom Line (TBL) to Awake Human's Divine Consciousness," Pertanika Journal of Tropical Agricultural Science 24, no. May (2016): 20–35, http://119.40.116.186/pjtas/browse/regular-issue?article=JSSH-S0194-2016.

40Nuril Badria, Eko Ganis Sukoharsono, and Lilik Purwanti, "Business Sustainability and Pentuple Bottom Line: Building the Hierarchical Pyramid of the Pentuple Bottom Line," International Journal of Research in Business and Social Science (2147- 4478) 10, no. 3 (2021): 123–31, "https://doi.org/10.20525/ijrbs.v10i3.1156.

41Ascarya and Masrifah, "Developing Maqāṣid Index for Islamic CSR: The Case of Ummah's Endowment Fund in Indonesia."

42Dusuki and Abdullah, "Maqāṣid Sharī'ah, Maṣlahah, and Corporate Social Responsibility (Objectives of Islamic Law, Public Interests and Corporate Social Responsibility)."

43Ascarya and Masrifah, "Developing Maqasid Index for Islamic CSR: The Case of Ummah's Endowment Fund in Indonesia."

44Dusuki and Abdullah, "Maqasid Al-Shari`ah, Maslahah, and Corporate Social Responsibility (Objectives of Islamic Law, Public Interests and Corporate Social Responsibility)."

45Ascarya and Masrifah, "Developing Maqāṣid Index for Islamic CSR: The Case of Ummah's Endowment Fund in Indonesia."

46Dusuki and Abdullah, "Maqāṣid Sharī'ah, Maṣlahah, Maslahah, and Corporate Social Responsibility (Objectives of Islamic Law, Public Interests and Corporate Social Responsibility)," 31.

47Ascarya and Masrifah, "Developing Maqāṣid Index for Islamic CSR: The Case of Ummah's Endowment Fund in Indonesia," 838.

48Dusuki and Abdullah, "Maqāṣid Sharī'ah, Maṣlahah, and Corporate Social Responsibility (Objectives of Islamic Law, Public Interests and Corporate Social Responsibility)," 35; Ascarya and Masrifah, "Developing Maqasid Index for Islamic CSR: The Case of Ummah's Endowment Fund in Indonesia," 832.

49Alan S. Gutterman, "Research and Development," SSRN Electronic Journal 12, no. 2 (2023): 3, https://doi.org/10.12968/npre.2007.5.5.23745.

50OCDE, Frascati Manual 2015: Guidelines for Collecting and Reporting Data on Research and Experimental Development, The Measurement of Scientific, Technological and Innovation Activities. (Paris: OECD Publishing, 2015), 45, https://doi.org/https://doi.org/10.1787/24132764.

51Abdul Majīd Al Najjār, "Maqāṣid Sharī'ah bi Ab'ād Jadīdah (The Objective of Islamic Law in a New Dimensions)" (Beirut: Dār Gharb al Islāmy, 2008).

52Hamid Fahmy Zarkasyi, Minhaj (Ways), 2nd ed. (Jakarta: INSIST, 2021).

53Michael Bloor and Fiona Wood, Keyword in Qualitative Method (London: SAGE Publications, 2006).

54Archie B. Carroll, "A History of Corporate Social Responsibility: Concepts and Practices," The Oxford Handbook of Corporate Social Responsibility, no. October (2009), https://doi.org/10.1093/oxfordhb/9780199211593.003.0002; Carroll, "The Pyramid of Corporate the Moral Management of Social Responsibiiity: Toward Organizational Stakeholders."

55Carroll, "The Pyramid of Corporate the Moral Management of Social Responsibiiity: Toward Organizational Stakeholders," 40–43.

56Laura Hartman and Joseph DesJardins, Business Ethics: Decision-Making for Personal Integrity & Social Responsibility, 4th ed. (New York: Mc Graw Hill Education, 2018), http://www.amazon.com/Business-Ethics-Decision-Making-Integrity-Responsibility/dp/0078137136; John Elkington, Cannibals with Forks: The Triple Bottom Line of 21st Century Business, Capstone, vol. 1 (Oxford UK: Capstone, 1997), 20.

57Badria, Sukoharsono, and Purwanti, "Business Sustainability and Pentuple Bottom Line: Building the Hierarchical Pyramid of the Pentuple Bottom Line," 124.

58Al Najjār, "Maqāṣid Sharī'ah bi Ab'ād Jadīdah (The Objective of Islamic Law in a New Dimensions)"

59Al Najjār, 15–20.

60Al Najjār, 46; Paryadi, "Maqāṣid Sharī'ah: Definisi Dan Pendapat Para Ulama (Maqāṣid Sharī'ah: Definitions and Conceptions of Scholars)," Cross-Border 4, no. 2 (2021): 206.

61Usmanul Khakim et al., "God and Worldview According to Al-Attas and Wall," Tsaqafah 16, no. 2 (2020): 223–44, https://doi.org/10.21111/tsaqafah.v16i2.4853; Usmanul Khakim, "Syed Muhammad Naquib Al-Attas' Theory of Worldview of Islam and Its Significance on Islamization of Pesent-Day Knowledge" (UNIDA Gontor, 2020); Khasib Amrullah et al., "The Concept of Waqf From Worldview Theory: The Study of Sharia-Philosophy," ULUL ALBAB Jurnal Studi Islam 23, no. 1 (2022): 22–41, https://doi.org/10.18860/ua.v23i1.15694; Usmanul Khakim, "Islamic Worldview-Based Corporate Social Responsibility" (Universitas Darussalam Gontor, 2024); M. Muslih et al., "Lakatosian Perspective of Islamic Science Research Programmes (Case: Islamization in Welfare Theory)," (2019): 1–8, https://doi.org/10.4108/eai.10-9-2019.2289377 Khasib Ammrullah, Usmanul Khakim, and Rakhmad Agung Hidayatullah, Islamisasi Teori Motivasi Pada Menejemen Bisnis Barat: Sebuah Elaborasi Worldview Islam Dan Barat (Islamisation of Motivation Theory in Western Business Management: An Elaboration of Islamic and Western Worldviews), ed. Ahmad Farid Saifuddin (Ponorogo: Unida Gontor Press, 2023).

62Shalih Fauzan, Kitāb Tauhīd (Book of Unification), ed. Trans. Agus Hasan Bashori (Jakarta: Darul Haq, 2000), 58.

63Jalāluddīn Al Mahalli and Jalāluddīn Al Suyuthi, Tafsīr Jalālain (Interpretation of Jalalain) (Cairo: Dār Hadīst, n.d.), 576.

64Al Najjār, "Maqāṣid Sharī'ah bi Ab'ād Jadīdah (The Objective of Islamic Law in a New Dimensions)."

65For more elaboration, see: Syed Muhammad Naquib Al-Attas, "Islam: The Concept of Religion and the Foundation of Ethics and Morality," in Prolegomena to The Metaphysics of Islam: An Exposition of the Fundamental Elements of the Worldview of Islam (Kuala Lumpur: International Institute of Islamic Thought and Civilization (ISTAC), 1995), 358.

66Al Najjar, "Maqashid Al Syariah Bi Ab'ad Jadidah (The Objective of Islamic Law in a New Dimensions)."

67Abi al Fadhil Jamaluddin Ibn Muhammad Ibn Makrami Ibn Manzur, Lisān Al 'Arab (Tongue (Words) of Arab) (Beirut: Dār Sādir, n.d.), vol. 5 : p. 56.

68Husain Raghib Al-Asfahani, Mu'jam Mufradātu Alfādz Al Qur'ān (Dictionary of Qur'anic Word), n.d., vol. 2, p. 494.

69Ahmad Ar Raisuni, Al Dzarī'ah Ila Maqāṣid Al Sharī'ah (The Pretext to the Objectives of Islamic Law) (Cairo: Daar Kalim, 2016), 160–65.

70Syamsuddin Arif, "Rethinking the Concept of Fiṭra: Natural Disposition, Reason and Conscience," American Journal of Islam and Society 40, no. 3–4 (2023): 79.

71Saryono, "Konsep Fitrah Dalam Perspektif Islam (Fitrah on Islamic Perspective)," Jurnal Studi Islam 14, no. 2 (2016): 161, http://jurnal.radenfatah.ac.id/index.php/medinate.

72Khakim, "Islamic Worldview-Based Corporate Social Responsibility," 179.

73Al Najjar, "Maqashid Al Syariah Bi Ab'ad Jadidah (The Objective of Islamic Law in a New Dimensions)."

74Syed Muhammad Naquib Al-Attas, "The Nature of Man and The Psychology of The Human Soul," in Prolegomena to The Metaphysics of Islam: An Exposition of the Fundamental Elements of the Worldview of Islam, 1995.

75Hadi, "Konsep dan Praktek Kesehatan Berbasis Ajaran Islam (Concepts and Practices of Health Based on Islamic Teachings)," 53.

76Khakim, "Islamic Worldview-Based Corporate Social Responsibility," 180.

77Al Najjār, "Maqāṣid Sharī'ah bi Ab'ād Jadīdah (The Objective of Islamic Law in a New Dimensions)."

78Nur Hadi Ihsan et al., "Hubungan Agama dan Sains: Telaah Kritis Sejarah Filsafat Sains Islam dan Modern (The Relationship between Religion and Science: A Critical Examination of the History of Islamic and Modern Philosophy of Science)," Intizar 27, no. 2 (2021): 97–111, https://doi.org/10.19109/intizar.v27i2.9527; Al Najjar, "Maqashid Al Syariah Bi Ab'ad Jadidah (The Objective of Islamic Law in a New Dimensions)."

79Khakim, "Islamic Worldview-Based Corporate Social Responsibility," 182.

80Al Najjār, "Maqāṣid Sharī'ah bi Ab'ād Jadīdah (The Objective of Islamic Law in a New Dimensions)."

81Ibid., 145.

82Khakim, "Islamic Worldview-Based Corporate Social Responsibility," 184.

83Al Najjār, "Maqāṣid Sharī'ah bi Ab'ād Jadīdah (The Objective of Islamic Law in a New Dimensions)," 157.

84Khakim, "Islamic Worldview-Based Corporate Social Responsibility," 187.

85Masrina, Dewi Maharani, and Verina Ayustrialni, "Konsep Harta Aan Kepemilikan Dalam Prespektif Ekonomi Islam (The Concept of Treasure and Ownership in the Islamic Economic Perspective)," Jurnal Ilmiah Ekonomi Islam 9, no. 01 (2023): 7–8; Al Najjār, "Maqāṣid Sharī'ah bi Ab'ād Jadīdah (The Objective of Islamic Law in a New Dimensions)," 183.

86 Milton Friedman, "The Social Responsibility of Business Is to Increase Its Profits.," The New York Time Magazine (New Jersey, 1970), https://link.springer.com/chapter/10.1007/978-3-540-70818-6_14.

87Al Najjār, "Maqāṣid Sharī'ah bi Ab'ād Jadīdah (The Objective of Islamic Law in a New Dimensions)," 207.

88Al Baqaraa 02: 30.

89Rahendra Maya, "Penafsiran Al-Sa'dī Tentang Konsep Al-Taskhīr (Al-Sa'dî's Interpretation of the Concept of Al-Taskhîr)," Al - Tadabbur: Jurnal Ilmu Al-Qur'an Dan Tafsir 2, no. 03 (2017): 1–24, https://doi.org/10.30868/at.v2i03.192; M. Kholid Muslih, Worldview Islam (Ponorogo: Pusat Islamisasi Ilmu(PII) dan Unida Gontor Press, 2018); Al Najjār, "Maqāṣid Sharī'ah bi Ab'ād Jadīdah (The Objective of Islamic Law in a New Dimensions)," 207.

90Al Baqaraa 02: 11-12.

91Carroll, "The Pyramid of Corporate the Moral Management of Social Responsibiiity: Toward Organizational Stakeholders," 44.

92Hamid Fahmy Zarkasyi, Minhaj (Way) (Jakarta: INSISTS Jakarta, 2021), 87; Hamzah Abu Faris, "Al Madkhal Ilā Dirāsah 'Ilmi Maqāṣid Al Sharī'ah Al Islāmiyah (The Introduction to the Study of Objectives of Islamic Law)" (Tharabuls-Libya: Daar Ibn Hazm, 2012), https://doi.org/978-9959-823-34-2.

93Khakim, "Islamic Worldview-Based Corporate Social Responsibility"; Zarkasyi, Minhaj (Ways), 2021, 80.

94Al-Asfahani, Mu'jam Mufradātu Alfādz Al Qur'ān (Dictionary of Qur'anic Word), 236.

95Hamzah Abu Faris, "Al Madkhal Ilā Dirāsah 'Ilmi Maqāṣid Al Sharī'ah Al Islāmiyah (The Introduction to the Study of Objectives of Islamic Law)" (Tharabuls-Libya: Dār Ibn Hazm, 2012), 14, https://doi.org/978-9959-823-34-2.

96Hasiah and Shafra, "Makanan Sehat Dalam Al-Qur'ān Menurut Pedagang Masakan Di Kota Padangsidimpuan (Healthy Food in the Qur'ān According to Cookery Traders in Padangsidimpuan City)," El Fawatih 3, no. 2 (2022): 204–5.

97Mohammad Syam'un Salim, "Al Attas on Reality" (University of Darussalam Gontor, 2019), 87.

98Al-Asfahani Mu'jam Mufradātu Alfādz Al Qur'ān (Dictionary of Qur'anic Word), 300.

99Ibid., 521.

100Urbanus Ura Weruin, "Teori-Teori Etika Dan Sumbangan Pemikiran Para Filsuf Bagi Etika Bisnis (Ethical Theories and Philosophers' Contributions to Business Ethics)," Jurnal Muara Ilmu Ekonomi Dan Bisnis 3, no. 2 (2019): 315, https://doi.org/10.24912/jmieb.v3i2.3384; Peniel C.D. Maiaweng, "Manfaat Kebenaran Perbuatan: Suatu Analisis Terhadap Ajaran Filsafat Pragmatisme (The Benefits of Righteous Actions: An Analysis of the Philosophical Teachings of Pragmatism)," Jurnal Jaffray 11, no. 1 (April 2, 2013): 1, https://doi.org/10.25278/jj71.v11i1.69.

101Yunus 10:9.

102Imam Muslim, Ṣhahīh Muslim (The valids of Muslim) vol. 8, 135.

103Al-Asfahani, Mu'jam Mufradātu Alfādz Al Qur'ān (Dictionary of Qur'anic Word), 114.

104Zarkasyi, Minhaj (Way), 86.

105Muhyiddin Yahya Ibn Syaraf Al Nawawi, Hadīts Arba'īn Nawawiyah (Nawawiah Fourty Prophetic Traditions), ed. Abdullah Haidir, (Riyādh: al Maktab al Ta'āwuni li ad da'wah wa Tau'iyah al Jaliyah, 2007), 9

106Syed Muhammad Naquib Al-Attas, "Islam and The Philosophy of Science," in Prolegomena to The Metaphysics of Islam: An Exposition of the Fundamental Elements of the Worldview of Islam (Kuala Lumpur: International Institute of Islamic Thought and Civilization (ISTAC), 1995), 385.

107Syed Muhamed Naquib Al-Attas, Islam dan Filsafat Sains (Bandung: Mizan, 1995), 33; Syed Muhammad Naquib Al-Attas, Islam and Secularism, 2nd ed. (Kuala Lumpur: ISTAC, 1993), 35.

108Al-Attas, Islam Dan Filsafat Sains, 36; Al-Attas, Islam and Secularism, 25.

109Khakim, "Islamic Worldview-Based Corporate Social Responsibility," 228.

110Act for humanity, Biografi Ir. Sholah Athiyah (Biography of Ir. Sholah Athiyah) (Indonesia, n.d.), https://www.youtube.com/watch?v=nBgvH3oGze0.

111Syahruddin Sumardi Samindjaya et al., "Imam Zarkasyi's Contribution to Indonesia's Modern Waqf Education System," Journal of Islamic Thought and Civilization 14, no. 1 (2024): 83, https://doi.org/10.32350/jitc.141.05.

112Pimpinan Pusat Muhammadiyah, "Anggaran Dasar dan Anggaran Rumah Tangga Muhammadiyah"(Muhammadiyah's Constitution and Bylaws) (Yogyakarta: Pimpinan Pusat Muhammadiyah, 2019), v. IX.

113PBNU, Anggaran Dasar dan Anggaran Rumah Tangga Nahdlatul Ulama (Nahdlatul Ulama's Constitution and Bylaws) (Jakarta: Pengurus Besar Nahdhatul Ulama', 2022), 99.

114Masruchin, "Wakaf Produktif dan Kemandirian Pesantren: Study Tentang Pengelolaan Wakaf Produktir Di Pondok Modern Darussalam Gontor Ponorogo (Productive Waqf and Pesantren Autonomy: A Study of Productive Waqf Management at Pondok Modern Darussalam Gontor Ponorogo)" (UIN Surabaya, 2014); Zainal. Veithzal Rivai and Chusnul Indah Lupitasari, "Model Pengelolaan Wakaf Produktif Di Pondok Modern Darussalam Gontor Dan Perannya Terhadap Pengembangan Universitas Darussalam Gontor," (Productive Waqf Management Model at Pondok Modern Darussalam Gontor and its Role in the Development of University of Darussalam Gontor) Al-Awqaf 10, no. 1 (2017): 69–79.