| Review | Open Access |

|---|

Reviving Agricultural Finance via Islamic Contracts: Promoting Risk Management, Economic Empowerment, and Social Justice |

|

|---|

![]() Mohamed Nafeel Mahboob1,2,

Mohamed Nafeel Mahboob1,2, ![]() Fadillah Mansor1* , and

Fadillah Mansor1* , and ![]() Azian Bin Madun1

Azian Bin Madun1

1Universiti Malaya, Kuala Lumpur, Malaysia

2Bait Al-Mashura Finance Consultations Doha, Qatar

Islamic finance provides a diverse range of contracts and concessions to address the financial needs of farmers. However, most Islamic financial institutions remain reluctant to fund agricultural projects despite having excess liquidity, primarily due to perceived financial risks, high uncertainty (Gharar), and limited risk-sharing mechanisms. As a result, many Muslim farmers struggle to access financing, confronting multiple challenges, such as high interest rates, stringent collateral requirements, and ethical or religious constraints. This paper examines the financial risks, uncertainties, and unique risks of selected Islamic agricultural finance contracts, namely Salam, Muzara’ah, and Musaqah. This study utilizes qualitative content analysis to examine the primary Islamic sources, the holy Qur’an, Hadīth, classical jurisprudence, and Hadīth commentaries. Indicatively, to define agricultural financing contracts, this study analyzes their structural features, establishes their permissibility, and assesses the implications of Gharar in the agricultural field. The findings suggest that integrating Islamic financial instruments with social finance mechanisms, such as combining Salam contracts with Zakah funds or implementing Muzara’ah and Musaqah Sukūk, can enhance financial inclusion, stabilize farmers’ incomes, manage price volatility, and reduce wealth disparities. By promoting fair, risk-sharing financial models, these instruments enhance economic empowerment, social justice, and sustainable agricultural finance. Future research should pilot-test these contracts to refine their practical applications and offer innovative financial solutions for agricultural communities worldwide.

1. INTRODUCTION

In risk, the distribution of results is known statistically through experience or a priori, whereas in uncertainty, it is impossible to quantify probabilities. Risk is the situation in which the distribution of results is known statistically through experience or a priori, whereas uncertainty is the situation where it is impossible to quantify probabilities; thus, imperfect information about the outcome of an action and probabilities-based actions are highlighted.1 Harwood et al. discussed risk as an uncertainty that affects an individual's welfare and is frequently linked to adversities and losses.2 Hence, it is the uncertainty that matters with the possibility of adverse events or losses: possible loss of money, potential harm to health, effects to resources, such as water, credit, and others. Uncertainty does not always imply complex situations only; however, it remains integral to understanding risk in complex situations. Risk embodies the potential adversity or failure that involves an individual's resilience and decision-making strategies in an unknown risk-centered situation.3

Hardaker interpreted risk in three different ways: (1) the chances of a negative result, (2) the variability of results (i.e. unstable outcome), and (3) the uncertainty of results.4 According to Bouslama and Lahrichi, despite the apparent ambiguity in the definition of the term risk, risk situations can be characterized by identifying different future situations and assigning them a probability of occurrence. In the case of uncertainty because of the complexity or opacity of a situation, the future of such a situation is unknown.5

The close term that stands for risk and uncertainty found in Islamic finance is Gharar which stems from the root term Gharrara and Taghreer. It means to put oneself in danger or risk and to expose someone, their money, or their property to destruction without even knowing it. The definitions of Muslim jurists for Gharar conclude in the following directions. The first definition limits Gharar to events whose occurrence is unknown, thus excluding unknown Gharar elements. For example, the definition of Ibn al-Abideen defines Gharar as doubt about the existence of the item being sold. Consequently, the second definition limits Gharar to the unknown, i.e., excluding something doubtful to happen from Gharar, whereas the third definition (of Ibn Hazm) combines the previous directions and makes Gharar comprehensive about the known and the unlikely.6 For example, Sarkhasi's definition of Gharar defines Gharar as something the outcome of which is hidden, and it is the opinion of most jurists. This definition was preferred and chosen by the award-winning expert scholar in Gharar related studies, the Late Professor Al-Dhareer, over other definitions because it contains all the jurisprudential particles discussed by the jurists under Gharar.7

Even though the holy Qur'an does not explicitly mention the term Gharar, it implicitly prohibits transactions that involve Gharar through verses emphasizing justice, transparency, clarity, fairness, and mutual consent in financial transactions. These verses have vividly and implicitly prohibited contracts involving Gharar.8 "The Prophet (pbuh) forbade the sale of Gharar."9 According to Imam Nawawi, the above hadīth, which is narrated by many of his companions, applies as the principle for Gharar in contracts.10 The hadīth gives three important determinations: prohibition of the sale of Gharar, the lifting of the sale of Gharar and all sales with Gharar are subject to prohibition and repeal.

Various methodologies can classify risks in agriculture and, from different perspectives; by its sources, probability of occurrence, and severity and correlation are three major methods found in the literature. Regarding sources of risks, there are five fundamental sources of risks faced by farmers: financial issues, production or yield, market or price, institutional policies and regulations, and human behaviors and errors (idiosyncratic). By the probability of occurrence, risk occurs at three layers: micro or individual farm level, meso or farm group level, and macro-level. Concerning the level of correlation, risks can be unique or completely independent at the micro-level, covariant at the meso-level, or perfectly correlated or systemic at the macro-level.11

The central focus of this paper is to examine financial risks, specifically credit and market-oriented risks. Although the lack of funds and capital is among the major problems facing the agricultural sector,12 when analyzing the financial risks in agriculture, financial risks commonly arise from the sources of production, such as exposure to extreme weather and disease shocks, from the need and the way farmers obtain capital and finance their farming activities and business operations. Thus, maintaining adequate cash flow levels to ensure the repayment of debt and other financial obligations and securing necessary loans for farming activities are vital to farming activity.

However, borrowing money introduces several risk factors, such as variability or volatility in borrowing rates, which can negatively affect borrowers' ability to borrow and their capacity to repay the capital. For instance, the default rate on leveraged loans in the United States recently reached to 7.2% in the 12 months leading up to October 2024, marking the highest rate since 2020. Elevated interest rates account for this surge in defaults, increasing borrowing costs and straining borrowers' repayment capacity.13 Such challenges can lead lenders to become reluctant to extend credit or to impose stricter credit terms, thus making conditions unfavorable, particularly for farmers. Moreover, volatility in borrowing costs may lead to insufficient cash reserves or credit availability for production, potential loan recalls by lenders, adverse changes in exchange rates, and increased risks of insolvency or bankruptcy.14

Internal and external factors influence farm financial risks. Internal factors include, for instance, the creditworthiness of the farmers, cashflows, and management and control of the farm assets, uncontrolled family expenses and inadequate reserve of cash or credit for production, and unable to maintain capital equity from going bankrupt. External factors, for instance, include macroeconomic factors, such as farm regulations, supply and demand trends in the global markets, changes in financial markets, potential loan calls by lenders, adverse changes in the exchange rates, (price) risks, increased input costs, and changes in market values of collaterals that could ultimately affect the farmer's ability to maintain a profitable farming activity or farming enterprise.15

This paper advances existing research by moving beyond theoretical discussions and proposing practical Islamic financial solutions for agricultural financing, integrating Islamic social finance mechanisms with commercial models, and introducing innovative instruments. Embedded risk-sharing mechanisms in the selected Islamic finance contracts effectively addressed inherent agricultural risks and uncertainties (Gharar), thereby, promoting financial stability, economic empowerment, and social justice. Nevertheless, Islamic financial institutions, despite having excess liquidity, are hesitant to finance agricultural projects because of perceived financial risks. Consequently, there is a significant need for sustainable, Sharī'ah-compliant financial solutions to address the financing gaps faced by Muslim farmers who cannot access conventional finance because of multiple hurdles, including high interest rates, stringent collateral requirements, and ethical and religious considerations. The research focuses on the under-explored feasibility and practical effectiveness of Islamic agricultural finance contracts and innovative financial instruments therein, with an aim to evaluate the permissibility, practicality, and risk mitigation capabilities of these contracts, comparing their effectiveness against conventional interest-based agricultural financing. Additionally, the study emphasizes how integrating Islamic financial instruments like Salam contracts with Zakah funds and implementing Muzara'ah and Musaqah Sukūk can support farmers' financial inclusion, sustainable income generation, and poverty alleviation. Furthermore, these Islamic contracts mitigate agricultural risks by stabilizing farmers' incomes, managing price volatility, and equitably distributing financial risks between landowners and farmers. Finally, the study highlights social justice by promoting fair financial practices, eliminating exploitative elements such as Riba and Gharar, supporting marginalized agricultural communities, and reducing economic disparities through equitable wealth distribution.

2. Literature Review

Farmers in developed countries face risks of market price volatility and loss of profit, organizations' stress level and poor decision making skills of the farm managers, weakness in the government monitoring mechanisms of the farm credit programs, excessive credits, swings in asset values,16 overconcentration on the problems of farm entities while neglecting the problems of farm people,17 conflicts on common agricultural fund management issues,18 effects of racial and gender bias on loan terms.19 Similarly farm firms have been facing many risks including crop price volatility, inconsistent crop yields, unpredictable costs of fertilizer, financial constraints in meeting the cash flow needs of farm operations and changes in the market value of farmlands20 because of various reasons, including weather affects.21 As for financial institutions, they get affected by production risks, unfavorable government policies, loss of collateral values, legal risks, demographic risks of grey hair syndrome and unfavorable interest rates, etc.22 Researchers have found various approaches to risk management tools in the literature. Livestock Risk Protection (LRP) insurance,23 a Sustainable Supply Chain model of contract combinations,24 AgriStability to reduce the Business Risk of farmers,25 and Diversification of activities by farm and off-farm sectors by rural households26 are some examples proposed in developed countries.

A large body of work pertaining to the developing countries focuses extensively on conditions that limit and/or bar access to credit, such as unpleasant weather and socio-economic factors including literacy, experience, awareness of weather risks factors, income level and distance to financial institutions, etc.27 Moreover, unfavorable government policies related to agricultural trade and the economic welfare of farmers lead them to be depressed with price distortions, import and export risks, and other crucial factors.28 Microfinance institutions' operations in developing countries are challenged by inefficient policies, weak economic foundations of rural agricultural resources, poor agricultural infrastructure problems, less capital, poor management systems, and very relaxed government policies.29

Many strategies have been proposed to deal with the financial risks pertaining to the developing world. For example, Shee et al. developed and piloted a credit model linked with Insurance for Kenya.30 Römer and Musshoff studied the application of microfinance credit- scoring models to contribute to credit scoring accuracy in Madagascar.31 Duguma proposed engaging in farming activities with low-risk and guiding farm households to make informed decisions based on their risk tolerance while emphasizing the need to select appropriate risk management tools, such as selecting of crops based on their resilience, as identified in the Ethiopian context.32 Among the literary works found pertaining to Bangladesh, the proposal for complementary technological and financial innovative solutions for managing weather-related risks like weather-related insurance products and rice varieties that withstand water stress by Ward et al., is significant.33

Existing research on Islamic agricultural finance contracts, such as Muzara'ah, and Musaqah, has mostly focused on their practical applications, community benefits and economic welfare.34 However, scholars have paid limited explicit attention to addressing financial risk, particularly managing the inherent uncertainty (Gharar) in these contracts. Recent literature addressing Salam financing has begun to fill this gap by explicitly discussing financial risks and their management through innovative hybrid models combining commercial and social financing. For instance, Kurniati et al. explicitly proposed the hybrid Salam model integrating Wakalah and Shirkah contracts to mitigate the inherent risks associated with traditional Salam financing, especially in volatile market conditions, such as those experienced during the COVID-19 pandemic.35 Similarly, Majid proposes the Salam-Muzara'ah linked Waqf model, combining commercial and social Islamic finance mechanisms to mitigate risks associated with agriculture financing, addressing issues of limited capital and idle land use simultaneously.36 However, discussions specifically targeting Gharar and financial risk mitigation within Muzara'ah, Musaqah and Salam contracts themselves remain relatively underexplored.

To address this gap and enrich the discussion, this paper undertakes an analysis of the Sharī'ah principles underlying the permissibility of selected Islamic agricultural finance contracts, Salam, Muzara'ah, and Musaqah. Specifically, by examining the foundational sources of Sharī'ah and the jurisprudential perspectives provided by Islamic scholars to better understand the theoretical and practical implications of these contracts. By focusing on these dimensions, this study aims to highlight both the need and the potential approaches for a more comprehensive management of financial risks within Islamic agricultural finance, thus rendering the identified research gap more substantial and accountable.

3. Research Methodology

This paper's objectives necessitated a data collection strategy centered on acquiring primary and secondary data, with a content analysis as the primary research technique. The primary data from the fundamental sources of the Holy Qur'ān and classical Hadīth and some jurisprudence books and hadīth commentary books, such as Al Bassam37 and Al-Dhareer38 were used. These sources were used to define the contracts, analyze their features, extract the proofs of their permissibility and related issues as well and analyze the texts related to Gharar that have come in connection with agriculture whether as Salam, or Muzara'ah, or Musaqah or any other forms of contracting.

The systematic review and synthesis of results from earlier studies to uncover patterns and insights relevant to the current research led to the adoption of content analysis. The significance of content analysis lies in its ability to provide a rigorous and structured approach to analyzing large volumes of qualitative data from various sources. By combining results from various studies, content analysis helps to identify consistent trends, contradictions, and gaps in existing literature, thereby offering a more comprehensive understanding of the topic. This method not only enhances the reliability of the research by triangulating data from different studies but also contributes to the practical applications.39

This paper also examined various data, both in theoretical and empirical forms, collected for content analysis. The other secondary sources include books, journal articles, conference proceedings, and online sources related to uncertainty, risks and financial risks in agriculture, uncertainty and risk aspects of Salam, Muzara'ah and Musaqah contracts by coding and classifying them to derive the understandings of the approaches toward risk, uncertainty, risk taking, the permissibility of risk and uncertainty, their implications, risk and financial risk aspects of the contracts. The paper uses a qualitative approach, since no mathematical or statistical figures were used, in which the description of risk and uncertainty, its management from conventional and Islamic perspectives are discussed, together with the models for managing agricultural financial risk by farmers, farm firms and farm related financial institutions, representing both conventional and Islamic, are explored. This analysis highlights the advantages of Islamic models over conventional ones.

4. Results and Discussion

Islam encourages participation in agricultural activities and offers many contracts and options based on sharing risks, which can provide effective risk management strategies. Although most of the Islamic banks hold excess liquidity, however, they fail to implement Sharī'ah compliant agricultural financial instruments to park funds for agricultural projects. Islamic agricultural finance contracts, which are particularly important sources for funding farmers in Islamic finance on both the small and large scales, allow these funds to be used to finance agricultural enterprises with higher profit-sharing than conventional agricultural loans. Therefore, Islamic finance contracts can play a vital role in enhancing risk management capabilities for financial institutions that provide agricultural finance globally. To build on this argument, the following sections will be elaborating on the potential application of the contracts of Salam, Muzara'ah, and Musaqah in the agriculture sector, supported by illustrations.

4.1. Innovative Application of Salam ContractIf Salam-based products are developed with innovation, the perceived risks can be mitigated. The classic form of Salam with innovation can be used to boast agricultural productivity, famers' income, their standards of living, food security and exports, all of which benefit the country's economy and provide sustainability. Other benefits of Salam include financing without middlemen, price stabilization against seasonal price fluctuations and price protection against market price drops, promoting large-scale agriculture, providing an alternative loan choice to conventional financial institutions, protecting farmers from adversities and marketing expenses, providing hedging opportunities for buyer and seller, while protecting against revenue risk and price-indexed debts among other advantages. Concessions given by Sharī'ah in Salam contract aimed to satisfy the economic and social needs of the poor, small and medium producers in the economy and being responsible for its growth.40

4.1.1. Zakah Linked Salam Contract for AgricultureSalam could also be used by linking Zakah's funds into the process. Hossain et al.,41 in Bangladesh, provided a strategy as illustrated in (figure 1) to link Zakah with Salam contract. This suggested that a food bank will be set up with pooled Zakah funds for serving vulnerable people who will get food vouchers. The local smallholder farmers are engaged with the food bank to deliver target agricultural yields in the future. Through institutional demand, this strategy provides an opportunity to source food at a fair price, open doors to new markets, and provide smallholder farmers with a secure income.

Figure 1. Zakah Linked Salam Contract (authors' own illustration based on the work of Hossain et. al.)42

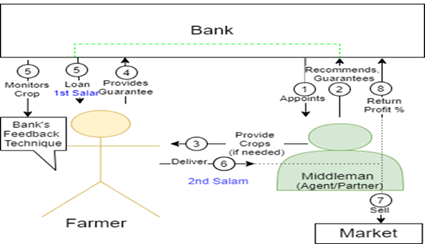

4.1.2. Parallel Salam Contract via BanksAlternatively, for managing the suspected commodity risk faced by financial institutions, parallel Salam could be an important strategy. A bank enters into two separate contracts of Salam contracts: one with the farmer (seller) and another with the commodity buyer, who will purchase the object from the bank, thus playing the intermediary role between the two parties. Contracts with both parties must be completely independent of one another. Kaleem and Abdul Wajid43 introduced three different models for Salam contract as given in figures 2-4, where the bank provides credit to the farmers under the first Salam contract, while bringing in a middleman (Model 1) or a mill (Model 2) or a subsidiary firm (Model 3) to ensure the marketability of crops and execute the second Salam contract.

Figure 2. Functionality Model 1 of Salam and Parallel Salam (authors' own illustration based on the work of Ahmad Kaleem and Rana Abdul Wajid)44

Nevertheless, the practical application of Salam and Parallel Salam contracts in modern times presented multiple challenges and issues. It includes the second buyer purchasing an object whose price has been paid but has not been delivered yet to the seller (i.e., bank for example). This constitutes a fundamental violation of Sharī'ah, i.e., the nature of the transaction in Salam is a debt because the seller is obliged to deliver the commodity in the future, which creates a debt on their part, thus it is executed under the primary concessions applicable to Salam.

Figure 3. Functionality Model 2 of Salam and Parallel Salam (authors' own illustration based on the work of Ahmad Kaleem and Rana Abdul Wajid)45

A parallel Salam contract could add to another controversy if the seller of the first Salam probably fails to deliver as promised. It is possible that the original buyer/bank could not deliver the commodities as agreed under the parallel Salam contract, contributing to the dispute and causing the legal bottleneck. However, this can be resolved by guarantees and collateral in place taken from and on behalf of the seller.

Figure 4. Functionality Model 3 of Salam and Parallel Salam (authors' own illustration based on the work of Ahmad Kaleem and Rana Abdul Wajid)46

There is also another perceived problem with Parallel Salam that it could be easily turned into a promissory note produced from a single transaction and traded by different parties on different contract terms. Thus, the first seller (i.e., farmer) receives a disadvantageous financial position because a lower starting price would be required to be tradable with profits in the transaction that follows. Frequently, the farmer receives a guaranteed price that is much less than the prevailing market rate, perhaps in order to get financing from the bank, which prevents him from negotiating, resulting in the exploitation of the first seller and a complete nullification of Sharī'ah law's purposes regarding Salam sale. Muslim economists argue this practice is similar to the interest-based loan because it compensates for time value of money and losses to the farmer because of advance prices. In spite of the fact that Sharī'ah permits advance payments at a lower price than the current market price, a price risk management solution called Band al Ihsān47 developed in Sudan, has been known to be effective in protecting and compensating both the banks and the farmers in cases of price fluctuations beyond certain threshold, either upwards or downwards.

Also, the current generation of Islamic financial institutions might not have adequate resources to participate in the commodities market, as there are very few or no commodity markets in most Islamic countries, whereas non-Islamic countries have standardized markets for commodities, which could disadvantage financiers who would have to compete with experienced middlemen, and with producers in order to trade commodities. Therefore, standardization and competitive disadvantage of the bank (buyer) over the middlemen in the Bai Salam contract poses a challenge to the sale, pricing, and marketability of commodities in the contract.48

4.2. Innovative Application of Muzara'ah and Musaqah Contracts Integrated with SukūkSukūk is more sophisticated and standardized instrument proposed to financing agriculture. It can provide a fixed rate of return and regular payments in order to provide the working capital, necessary property, plant and equipment and instruments required by agricultural units. AAOIFI has approved and issued several methods for Sukūk in its standard No. 17 including Salam (3/3), Muzara'ah (3/7) and Musaqah (3/8) related Sukūk for trading and investing.49

Muzara'ah and Musaqah contracts have been categorized as forms of partnership contracts in farming for sharing agricultural product and loss (aPLS).50 In Musaqah a share of what the trees produce is given, while in Muzara'ah a share of whole crops/plantation is the subject of the agreement. It is allowed to mix and match between Musaqah and Muzara'ah contracts. However, it is necessary to agree and include a term in the contracts of Musaqah and Muzara'ah.51 As such the following section will focus on the practical application of Sukūk in both Muzara'ah and Musaqah contracts.

4.2.1. Muzara'ah Sukūk (Farm-letting Sukūk)Despite the Muzara'ah contract has been known as "a type of partnership contract where one party gives another a piece of agricultural farmland for a defined period so that he can work on it, and then the harvest is shared among them according to the conditions of the agreement", however, the integration of Sukūk differs from the classical Muzara'ah contact. The operation model of Muzara'ah Sukūk is given in (figure 5).

Figure 5. Operating Model of Muzara'ah Sukūk (authors' own illustration based on the data from the website )https://www.Sukūk.ir52

The issuer of Muzara'ah Sukūk transfers the Sukūk and collects the money paid by the Sukūk owners (investors), then uses this fund to purchase agricultural land. On behalf of the investors, it then transfers these lands to farmers who work on them under the Muzara'ah contract, and at the end of the cultivation year, the crop will be distributed. In Muzara'ah Sukūk, the owners play the role of landowners, the issuer plays the function of attorney for the owners, and the farmers play the role of an agent in Muzara'ah contract. Muzara'ah Sukūk is deeds of joint ownership of certain agricultural lands by Sukūk-owners. This facilitates the enhancement of agricultural land, especially in the poor region, by taking uncertainty problems into account, which would create job opportunities and economic development. These alternatives are valuable in such regions where traditional financing may not accessible.53

4.2.2. Musaqah SukūkMusaqah Sukūk operates slightly differently from Muzara'ah Sukūk, and the operational flow is given in (figure 6). First, the Sukūk issuer transfers the Sukūk and collects the money paid by the Sukūk applicants, using this money to buy agriculture fields. The fields are subsequently given to farmers on behalf of the Sukūk owners, based on the Musaqah contract, to work on the lands, and later, the crop will be distributed.

Figure 6. Operating Model of Musaqah Sukūk (authors' own illustration based on the data from the website https://www.suku.ir54)

In the Musaqah Sukūk, the owners function as landowners, the issuer as an attorney, and the farmer as an agent in the Musaqah contract. The deeds of joint ownership of particular cultivated fields by Sukūk-owners are known as Musaqah Sukūk. This Sukūk also allows a Shari'ah-compliant and sustainable source of finance to the agriculture industry.55 Especially looking into countries where farmers cannot operate because of financial constraints corresponding to the COVID-19 impact, the Musaqah Sukūk would help the farmers restart their operation by going into joint ownership of the fields and sharing the business risk. Therefore, the Sukūk could be used just more than uplifting the agriculture sector; however, helping the country depending on the primary sector to revive their economy in a sustainable mechanism in line with the Islamic principles and teachings.

5. Discussions

Islamic Shari'ah prohibits any transaction that involves interest, falsifying, speculation, fraud, risks or uncertainties that are unmanageable (Gharar), hegemony, greed, exploitation, unfairness, and the unjust taking of other people's money. Another significant feature of the Islamic financial system is that assets must back all funds issued.56 Although multiple problems cause devastation in the agricultural sector, the financial problem is significant and leads to other issues. Thus, a solution for lack of funds could control other issues. The availability of adequate funding sources, for example, can contribute to the recovery of the agricultural sector, including modernization of agricultural machinery, improvement of processing and storage facilities, and other agricultural infrastructure.

In line with the findings of this study, two applications of Salam contract have been explained in the previous section. Undoubtedly, the issues related to capital and funds can be solved through the sale of Salam, which was practiced by the farmers in Madinah during the early Islamic era. Since the commodity risk has been a key obstacle in implementing Salam based financing, a Parallel Salam sale with a commodity dealer or a third party can be used to mitigate the commodity risk of financier.

Salam financing constitutes many risk mitigating techniques in agriculture and agricultural financing. It saves from interest risk being an alternative instrument for interest bearing loans; thus, Shari'ah compliance is maintained by individuals and institutions. It also helps mitigate market risk, price risks and revenue or income risk saving farmers from adversity, additional marketing expenses and price volatility by giving stability in price and in income with the direct involvement of the financier, whether as an investor, or as a buyer or as a fund provider, farmers can avoid middlemen risk as well through Salam financing.

Financial contracts embedded with Gharar, and uncertainty are subject to specific considerations regarding the level of Gharar and uncertainty therein. The permissibility or tolerance of uncertainty and risk in the contracts and/or the prohibition of the same are determined by the level of Gharar contained thereupon.

In Salam sales, moving the price to an unknown date or selling an item that is unlikely to exist when due are relevant examples of a major Gharar. However, suppose there exists a legitimate need, whether public, private, or personal, for such a contract of major Gharar, while all other legitimate means to reach the need are obstructed. In that case, the Gharar is tolerated, and the contract shall not be considered as prohibited because of major Gharar. Salam contracts are permitted, because the farmer needs them, despite the Gharar in it, according to the opinion of most jurists. This demonstrates that the Sharī'ah's aim of meeting the economic and social needs of the poor, thereby ensuring the prevalence of social justice.

However, it is noteworthy that the Salam sale contract in agriculture has not been permitted in Sharī'ah with a free hand. A farmer cannot sell all that his land or tree will produce neither before planting, nor after planting but before harvesting and becoming fit for sale, neither conditional sale on getting harvest, nor confirmed sale with guaranteed crop regardless of the status of its harvest. These forms of sales are prohibited in Islamic jurisprudence.

Some of them have no room for scholars to maneuver because of clear Sharī'ah prohibitions (e.g. hadīth that forbids selling fruit before it becomes good57 besides the general prohibition of Gharar that is present in both cases referred above; when conditional sale the quantity of a sold item is not known, when the confirmed sale, existence of the sold item is doubtful and Gharar (uncertainty) in its quantity if exists. Unlike selling something that may or may not be available in the future, selling an item which will be most likely to exist according to customs and practices is acceptable in Sharī'ah, where Salam sale is applicable.

The sale of objects that may or may not exist in future is non-permissible. However, this can be permitted exceptionally within narrow limits and if there was any hardship and embarrassment in the postponement of such sale until the existence of those things or their existence becomes more real. For example, sale of what has not appeared yet from the melon etc., with what has already appeared in good condition.58 Hence, it is understood that the notion of necessity leads to tolerance even with some major risks and permissibility, which means Islam encourages taking and managing risks rather than avoiding risks.

While scholars agree that the small Gharar is negligible and the large Gharar is forbidden, they disagree on the status of the medium level Gharar and its effect on relatively large transactions. Sale of what lies on the ground, sale of plants that are there one after another, Muzara'ah and Musaqah contracts are examples. The part of the harvest received by the landowner in these contracts cannot be predetermined. Therefore, these types of Gharar are treated as non-avoidable.59

There are many precedents in Shari'ah law showing tolerance with Gharar when prioritizing farmers' needs. Permissibility of Ariyyah60 Sale as an exemption from the prohibited transaction of Muzabanah[61], permissibility to give fruits as gift before it becomes ripen, permissibility to make a will for the fruits while on the tree (the bequest of the non-existent), overall negligibility of Gharar in non-commutative or voluntary contracts, which is not permitted in commutative or exchange contracts according to all jurists, are further examples.

Apparently, the exemption of Ariyyah came solely for prioritizing the needs of poor farmers, the owners of Ariyyah those who do not have anything to buy fresh dates, neither gold nor silver, other than dry dates. Gharar is forgiven because there is a genuine need to sell. All jurists agree that the effect of Gharar in non-commutative contracts, such as gift, is less than its effect in commutative contracts; however, they differ in the extent of this effect. The Shafi'is hold the strictest opinion on the impact of Gharar on contracts. In contrast, the Malikis are the most lenient in the impact of Gharar on contracts, which is the most correct approach according to Al-Dhareer.62

Hence, Islamic law has offered a clear boundary between the prohibition of Gharar versus tolerance of Gharar and a clear understanding of the Sharī'ah's perception in offering certain exceptions to the prohibition of Gharar or risks in contracts. Some contracts have been allowed because of their Gharar embedded nature. In contrast, other contracts have been allowed based on need and necessity arising from such contracts. Contracts that have been embedded with Gharar and allowed when such permission does not harm either of the parties. Muzara'ah and Musaqah contracts are good examples of this category where one party owns the land, and others cultivate or irrigate in exchange for a part of the harvest. This part cannot be predetermined.

On the other hand, exceptions arise from the need or necessity open some rooms for scholars to maneuver based on Shari'ah principles of "easing" or "avoiding difficulty", even to the extent of tolerating excessive Gharar, without invalidating such contracts.63 Examples include Salam and other agricultural financing precedents. By granting concessions in the Salam contract, Sharī'ah aims to satisfy the economic and social needs of the poor, small, and medium producers, promoting inclusive economic growth. Zakah-linked Salam contracts, for instance, play a crucial role in uplifting marginalized communities by providing financial support to needy farmers, thereby contributing to social welfare. Similarly, Muzara'ah and Musaqah contracts embody Islamic principles of social justice through equitable wealth distribution and cooperative agricultural development. The inherent risk-sharing nature of these contracts protects small farmers from financial uncertainties, preventing them from disproportionate burdens and reducing economic disparities. Islamic finance institutions, therefore, should actively utilize Salam, Muzara'ah, and Musaqah-based products to protect vulnerable farming communities.64

6. Conclusion

The current research investigates the feasibility and effectiveness of Islamic agricultural finance contracts and innovative financial instruments. It highlights how Islamic finance caters for risk sharing, financial inclusion, and economic sustainability in agriculture. Additionally, this study highlighted the traditional Salam contracts, which help to mitigate agricultural risks and enhance food security, while innovative adaptations, such as Zakah-linked and Parallel Salam models, provide fair pricing, stabilize farmers' income, and expand market access. These innovations also manage commodity risks for financial institutions by ensuring crop marketability. Furthermore, Muzara'ah and Musaqah contracts facilitate equitable risk-sharing between landowners and farmers. Thus, showcasing that integrating these contracts with Sukūk can further drive agricultural development, employment, and sustainable finance, particularly benefiting vulnerable and crisis-prone regions.

6.1. Further Research ImplicationsTo address critical financial gaps in agriculture, policymakers and financial institutions must facilitate the adoption of Salam, Muzara'ah and Musaqah contracts, which enhance income stability, manage risks, and promote ethical financial practices. These instruments align with faith-based principles while supporting resilience and growth for the agricultural sector.

Islamic finance embraces a pragmatic risk-tolerance approach, prioritizing economic and social necessities. The principle of necessity, allows contracts like Salam despite their inherent Gharar (uncertainty), highlights the value of proactively taking and managing risks rather than merely avoiding or transferring them, to support farmers' needs Similarly, Muzara'ah and Musaqah contracts accept manageable uncertainties, underscoring Islam's emphasis on balancing risk mitigation with social justice and economic equity. Historical precedents in Islamic jurisprudence, such as the Ariyyah contract, further illustrate the Islamic legal tradition's adaptability in serving the genuine interests and welfare of vulnerable groups, particularly farmers and the economically disadvantaged. Moreover, from a theoretical perspective, Islamic jurisprudence schools' leniency toward specific risk-embedded contracts contributes to a richer, adaptable legal framework, emphasizing the necessity of balancing risk mitigation with the broader goals of social justice and economic equity.

However, this research was only limited to qualitative content analysis, which constrains its ability to provide empirical validation of the proposed financial models. Therefore, future research should explore the piloting of Islamic agricultural finance contracts in countries like Sri Lanka, where such facilities are either unavailable or inaccessible because of strict credit requirements. Studies could focus on innovative financing models that incorporate concessions and exemptions for uncertainty and risk, ensuring compliance with Islamic principles. Additionally, further research should assess the practicality of Zakah-linked Salam contracts, Muzara'ah Sukūk, and Musaqah Sukūk through quantitative studies with industry practitioners. Investigating the role of Waqf in agricultural finance can also be considered addressing farmers' financial challenges, mitigate high-interest and collateral issues, and provide a sustainable mechanism for the economically disadvantaged. A study on generating Waqf for agricultural causes could further enhance its applicability.

Thus, a strategic adoption of Islamic financial instruments can strengthen agricultural resilience, support vulnerable farming communities, and promote sustainable and inclusive economic growth.

Author Contribution

Mohamed Nafeel Mahboob: Conceptualization, Data Curation, Formal Analysis, Investigation, Methodology, Resources Visualization, Writing Original Draft. Fadillah Mansor: Funding Acquisition, Data Curation, Project Administration, Supervision, Validation, Writing-review & Editing. Azian Bin Madun: Funding Acquisition, Resources Supervision, Validation, Writing-review & Editing.

Conflict of Interest

The author has absolutely no financial or non-financial conflict of interest regarding the subject matter or material discussed in this manuscript.

Data Availability Statement

The data associated with this paper is available from the authors upon request.

Funding Details

This research is associated with Universiti Malaya (UM) research projects, APIUM Research PV039-2024 and RMF0039-2021.

Generative AI Disclosure Statement

The authors did not use any type of generative AI software for this research.

Bibliography

AAOIFI. Shari'ah Standards. Bahrain, 2017. https://aaoifi.com/shariah-standards-3/?lang=en.

Abu Dawood, Sulaymān ibn al-Ashʻath. Sunan Abī Da’ūd [Abu Dawood’s Collection of Sayings and Deeds of Prophet Muhammad (pbuh)]. Edited by Muḥammad Muḥyī al-Dīn ʻAbd al-Ḥamīd (Beirut, Saida: Al Maktabah Al Asriya, 1392 AH), https://al-maktaba.org/book/33759/4843. Accessed 15 December 2021.

Aburaida, Khalid M. Mustafa. “Rural Finance as a Mechanism for Poverty Alleviation in Sudan with an Emphasis on Salam Mode.” European Scientific Journal 7, no.26 (2014): 157–166.

Adedapo, Alagabi Abdghaffar, Abubakar Tabiu, Ladan Sahnun, Hamid Mohsin Jadah, Ehsan Saeed Yaqoot, Hadiza Garba Isah, and Alagabi Modinat Remi, “Bai Salam in the Light of Contemporary Application: Issues, Challenges and Recommendations.” Paper presented at Islamic Business Management Conference (IBMC), Kuala Lumpur, August 18-19, 2014. https://www.researchgate.net/publication/318317523.

Aditto, Satit, Christopher Gan, and Gilbert V. Nartea. “Sources of Risk and Risk Management Strategies: the Case of Smallholder Farmers in a Developing Economy.” In Risk Management - Current Issues and Challenges. Edited by Nerija Banaitiene. Intech Open, 2012.

Anderson, Kym. “Agricultural Price Distortions: Trends and Volatility, Past, and Prospective.” Agricultural Economics 44, no. 1 (2013): 163-171. https://doi.org/10.1111/agec.12060.

Al-Bassam, Abdullah. Tawḍīḥ al-Aḥkām min Bulūgh al-Marām [Clarification of the Provisions of Bulugh al-Maram]. Makkah: Maktaba Al Asadi, 1423 AH.

Bouslama, Ghassen., and Younes Lahrichi. “Uncertainty and Risk Management from Islamic Perspective.” Research in International Business and Finance 39, (2017): 718-726. https://doi.org/10.1016/j.ribaf.2015.11.018.

Central Asset Management Capital Market. “Muzara’a Sukūk (Farm-letting Sukūk).” Accessed January 11, 2025, https://www.Sukūk.ir/Sukūk/types-of-Sukūk/farm-papers/.

Central Asset Management Capital Market. “Musaqah Sukūk (Irrigation Sukūk).” Accessed January 11, 2025, https://www.Sukūk.ir/Sukūk/types-of-Sukūk/employment-papers/.

Cole, Jeremy Michael Gregory. “Behavioural Determinants of the Adoption of Financial Price Risk Management Tools by Wheat Farmers in England.” Ph.D. diss., The University of Reading, 2014, https://centaur.reading.ac.uk/66398/.

DeVuyst, Eric A., Cesar L. Escalante, Jaclyn D. Kropp, Rodney Jones, and Phil Kenkel. “Sources of Institutional Financial Risks in Agriculture.” Risk Education Publication Series. Southern Risk Management Education Center, University of Arkansas System, (2013). Accessed August 8, 2021, https://www.uaex.edu/publications/PDF/srme01fs.pdf.

Dhakal, Chandra K., Cesar L. Escalante, and Charles Dodson. “Heterogeneity of Farm Loan Packaging Term Decisions: A Finite Mixture Approach.” Applied Economics Letters 26, no. 18 (2019): 1528–1532, https://doi.org/10.1080/13504851.2019.1584360.

Al-Dhareer, Siddiq Mohammad Al-Ameen. “al-Salam wa-Taṭbīqātuhu al-Muʻāṣirah.” [Salam and its Contemporary Practices]. Majallat Mujamma' Al Fiqh Al Islami Al Duwali [Journal of the OIC Fiqh Academy] 9, (1991), https://al-maktaba.org/book/8356/17703.

Al-Dhareer, Siddiq Mohammad Al-Ameen. Al-Gharar in Contracts and Its Effects on Contemporary Transactions. Jeddah: Islamic Research and Training Institute, 1999.

Drollette, Sarah A. “Managing Financial Risk in Agriculture.” Utah State, USA: Department of Applied Economics, Utah State University Extension, 2009. Accessed December 14, 2021, https://extension.usu.edu/apec/files/uploads/agribusiness-and-food/risk-management/risk-management-factsheets/Managing-Financial-Risk.pdf.

Duguma, Ashenafi. “The Role of Agricultural Cooperatives in Risk Management and Impact on Farm Income: Evidence from Southern Ethiopia.” International Journal of Economic Behavior and Organization 4, no. 4 (2016): 28–39, https://doi.org/10.11648/j.ijebo.20160404.11.

Elhiraika, Adam B. On the Experience of Islamic Agricultural Finance in Sudan: Challenges and Sustainability. Jeddah, KSA: Islamic Development Bank, 2003.

Escalante, Cesar L., Adenola Osinubi, Charles Dodson, and Carmina E. Taylor. “Looking Beyond Farm Loan Approval Decisions: Loan Pricing and Nonpricing Terms for Socially Disadvantaged Farm Borrowers.” Journal of Agricultural and Applied Economics 50, no. 1 (2018): 129–148, https://doi.org/10.1017/aae.2017.25.

Fałkowski, Jan., Maciej Jakubowski, and Paweł Strawiński. “Returns From Income Strategies in Rural Poland.” Economics of Transition and Institutional Change 22, no.1 (2013): 139–178, https://doi.org/10.1111/ecot.12032.

Fletschner, Diana, Catherine Guirkinger, and Steve Boucher. “Risk, Credit Constraints and Financial Efficiency in Peruvian Agriculture.” The Journal of Development Studies 46, no. 6 (2010): 981–1002, https://doi.org/10.1080/00220380903104974.

Hardaker, John Brian. “Some Issues in Dealing with Risk in Agriculture.” Working Paper, University of New England Graduate School of Agricultural and Resource Economics, Australia, (2000). Acccessed August 1, 2021, http://www.une.edu.au/febl/EconStud/wps.htm.

Harwood, Joy, Richard Heifner, Keith Coble, Janet Perry, and Agapi Somwaru. “Managing Risk in Farming: Concepts, Research, and Analysis.” Agricultural Economic Report No. 774. Washington DC: U.S. Department of Agriculture, 1999.

Hossain, Ishrat, Aliyu Dahiru Muhammad, Binta Tijjani Jibril, Simeon Kaitibie. “Support for Smallholder Farmers through Islamic Instruments: The Case of Bangladesh and Lessons for Nigeria.” International Journal of Islamic and Middle Eastern Finance and Management 12, no. 2 (2019): 154–168, https://doi.org/10.1108/IMEFM-11-2018-0371.

Ibn Al Hajjaj, Muslim. Sahih Muslim [Muslim’s Authentic Collections of the Sunnah of the Prophet (pbuh)]. Edited by Muhammad Fuad Abdul Baqi. Beirut: Dar Ihya' Al Thurath Al Arabi, 1388 AH), https://al-maktaba.org/book/33760. Accessed 7 September 2021.

Kaleem, Ahmad., and Rana Abdul Wajid. “Application of Islamic Banking Instrument (Bai Salam) for Agriculture Financing in Pakistan.” British Food Journal 111, no. 3 (2009): 275–292, https://doi.org/10.1108/00070700910941471.

Klapper, Leora., Dorothe Singer, Saniya Ansar, and Jake Hess. Financial Risk Management in Agriculture: Analyzing Data from a New Module of the Global Findex Database. Washington DC: The World Bank, 2019.

Komarek, Adam. M., Alessandro De Pinto, and Vincent H. Smith. “A Review of Types of Risks in Agriculture: What We Know and What We Need to Know.” Agricultural Systems 178 (2020): 102738, https://doi.org/10.1016/j.agsy.2019.102738.

Klaus, Krippendorff. “Content Analysis: An Introduction to Its Methodology.” 4th ed., Los Angeles: SAGE Publications, 2018.

Kumar, Chandra S., Calum G. Turvey, and Jaclyn D. Kropp, “The Impact of Credit Constraints on Farm Households: Survey Results from India and China.” Applied Economic Perspectives and Policy 35, no. 3 (2013): 508-527, https://doi.org/10.1093/aepp/ppt002.

Kurniati, Sunuwati, Muhammad Majdy Amiruddin, and Abdul Syatar, “Bay Al Salam as Financing Alternative During Pandemic Outbreak: A Proposal to Indonesia,” Academy of Entrepreneurship Journal 27, no 5S: (2021): 1–7.

http://repositori.uin-alauddin.ac.id/id/eprint/19738.

Li, Shasha. “Financial Stress Test Under Multiple Risks for Representative Farms of Central Illinois.” Master's Thesis, Purdue University, 2012. Purdue e-Pubs (AAI1535051).

Livsey, Alan, and Harriet Clarfelt. “Defaults on Leveraged Loans Soar to Highest Rate in 4 Years.” www.ft.com, The Financial Times Limited, December 24, 2024. accessed March 8, 2025. https://www.ft.com/content/e6ba508c-4612-4b4a-9a6b-ecde6fc91c12.

Majid, Rifaldi. “Designing Salam-Muzara’ah Linked Waqf to Financing Agricultural Sector.” Journal of Islamic Monetary Economics and Finance 7, no. 3 (2021): 503–526, https://doi.org/10.21098/jimf.v7i3.1309.

Maurer, Klaus. “Where Is the Risk? Is Agricultural Banking Really More Difficult than Other Sectors?” In Finance for Food: Towards New Agricultural and Rural Finance, edited by Doris Köhn. Berlin, Heidelberg: Springer, 2014, https://doi.org/10.1007/978-3-642-54034-9_7.

Merritt, Meagan G., Andrew P. Griffith, Christopher N. Boyer, and Karen E. Lewis. “Probability of Receiving an Indemnity Payment from Feeder Cattle Livestock Risk Protection Insurance.” Journal of Agricultural and Applied Economics 49, no. 3 (2017): 363–381, https://doi.org/10.1017/aae.2016.44.

Morgan, Kim., Peter Callan, Allyssa Mark, Kim Niewolny, Theresa Nartea, Kelli Scott, and Jim Hilleary. “Farm Financial Risk Management: Overview of Financial Systems for New and Beginning Farmers.” Verginia State University, 2016. https://www.pubs.ext.vt.edu/AAEC/AAEC-114/AAEC-114.html.

Muneeza, Aishath., Nik Nurul Atiqah Nik Yusuf, and Rusni Hassan. “The Possibility of Application of Salam in Malaysian Islamic Banking System.” Humanomics 27, no. 2 (2011): 138–147, https://doi.org/10.1108/08288661111135135.

Narastri, Maulidah. “Muzara'ah in Efforts for Economic Prosperity: Between Patterns of Behavior, Improvements and Demands.” (Paper presented at International Conference on Economic Business Management, and Accounting (ICOEMA), 2, 474-480. Universitas 17 Agustus 1945. Surabaya, 2023, https://conference.untag-sby.ac.id/index.php/icoema/article/view/3028.

Al Nasaei, Ahmad bin Al Shuaib. Al Sunan Al Kubra [Al Nasaei’s Collection of Sayings and Deeds of Prophet Muhammad (pbuh)]. Edited by Hasan & Abdul Mohsin Al Turki Al Shalbi, 2001, (Beirut: Al Risala, 2001), Accessed December 15, 2021, https://al-maktaba.org/book/33867/8601.

Obaidullah, Mohammad. “Enhancing Food Security with Islamic Microfinance: Insights from Some Recent Experiments.” Agricultural Finance Review 75, no. 2 (2015): 142-168. https://doi.org/10.1108/AFR-11-2014-0033.

Ogunbado, Ahamad Faosiy., and Umar Ahmed. “Bay' Salam as an Islamic Financial Alternative for Agricultural Sustainability in Nigeria.” Journal of Islamic Economics Banking and Finance 11, (2015): 63–75, https://dx.doi.org/10.12816/0024789.

Othman, Rohana., Nooraslinda Abdul Aris, Rafidah Mohd Azli, and Roshayani Arshad, “Islamic Banking: The Firewall Against the Global Financial Crisis.” Journal of Applied Business Research 28, no. 1 (2012): 9–14, https://doi.org/10.19030/jabr.v28i1.6679.

Popescu,Gabriel., Alina Zaharia, Daniela Mihai, and Roxana Chiocaru. “The Financial Relationships between Farmers, Credit Institutions and Public Authorities - Short Review.” Ekonomika Poljoprivrede 65, no. 1 (2018): 427–436, https://doi.org/10.5937/ekoPolj1801427P.

Purves, Nigel, Scott James Niblock, and Keith Sloan. “On the Relationship between Financial and Non-Financial Factors.” Agricultural Finance Review 75, no. 2 (2015): 282-300. https://doi.org/10.1108/AFR-04-2014-0007.

Ramadani, Mustika Lestrai, Siti Kholis Napsiah, and Muhammad Nur Iqbal. “Muzara'ah, Musaqoh And Mugharasah Contracts in Fiqh Muamalah.” Jurnal Multidisiplin Sahombu 5, no 1 (2025): 89–101.

Reinsel, Edward I. “Off-Farm Income of People Involved in Farming.” Journal of Agricultural and Applied Economics 2, no. 1 (2015): 115–119, https://doi.org/10.1017/S0081305200009900.

Romer, Ulf, and Oliver Musshoff. “Can Agricultural Credit Scoring for Microfinance Institutions Be Implemented and Improved by Weather Data?” Agricultural Finance Review 78, no. 1 (2018): 83–97, https://doi.org/10.1108/AFR-11-2016-0082

Salisu, Yahuza, Ahmed Ibrahim Mohammed, and Anas Muhammad Yakub. “The Mediating Effect of Murabahah Financing on the Relationship between Farm Land, Farm Infrastructure and Agricultural Output in Nigeria.” International Journal of Management Research and Reviews 7, no. 12, (2017): 1080–1089, https://www.proquest.com/scholarly-journals/mediating-effect-murabahah-finance-on/docview/1992208983/se-2?accountid=28930

Saqib, Shahab E., Mokbul Morshed Ahmad, Sanaullah Panezai, and Ubaid Ali. “Factors Influencing Farmers' Adoption of Agricultural Credit as a Risk Management Strategy: The Case of Pakistan.” International Journal of Disaster Risk Reduction 17, (2016): 67–76, https://doi.org/10.1016/j.ijdrr.2016.03.008.

Shafiai, Muhammad Hakimi Mohd., and Mohammed Rizki Moi. “Financial Problems Among Farmers in Malaysia: Islamic Agricultural Finance as a Possible Solution.” Asian Social Science 11, no. 4 (2015): 1–16. http://dx.doi.org/10.5539/ass.v11n4p1.

Shee, Apurba, Calum G. Turvey, and Liangzhi You. “Design and Rating of Risk-Contingent Credit for Balancing Business and Financial Risks for Kenyan Farmers.” Applied Economics 51, no. 50 (2019): 5447–5465, https://doi.org/10.1080/00036846.2019.1613502.

Sifa, Eka Nurhalimatus., and Sudarso Kaderi Wiryono. “How does Salam Financing Affect Farmers’ Income? A System Dynamics Approach.” Journal of Islamic Accounting and Business Research 15. no. 1 (2024): 119–135, https://doi.org/10.1108/JIABR-02-2022-0042.

Singhal, Parmod Kumar, and Vivek Mittal. “PMFBY - A Financial Inclusion Initiate for Farmers Development.” International Journal of Business Ethics in Developing Economies 6, no. 2 (2017): 39–43.

Al Thirmithi, Abu ’Eisa Mohammad Ibn ’Eisa. Sunan Al Thirmidhi [Al Thirmithi’s Collection of Sayings and Deeds of Prophet Muhammad (pbuh)]. Edited by Ahmad Muhammad Shakir and Muhammad Fuad Abdul Baqi, (Egypt: Mustafa Al Babi Al Halabi, 1975), Accessed December 15, 2021, https://al-maktaba.org/book/33754/2138.

Ulfah, Khalishah, and Muryani Arsal. “Muzara’ah Contract of Farmer Perspective.” Paper presented at International Economics and Business Conference 1, no. 1 (2023): 235-240. https://jurnal.amertainstitute.com/index.php/IECON/article/view/57.

Uzea, Nicoleta., Kenneth Poon, David Sparling, and Alfons Weersink. “Farm Support Payments and Risk Balancing: Implications for Financial Riskiness of Canadian Farms.” Canadian Journal of Agricultural Economics 62, no. 4 (2014): 595-618, https://doi.org/10.1111/cjag.12043.

Ward, Patrick S., David J. Spielman, David L. Ortega, Neha Kumar, and Sumedha Minocha. “Demand for Complementary Financial and Technological Tools for Managing Drought Risk: Evidence from Rice Farmers in Bangladesh.” Paper presented at the Agricultural and Applied Economics Association & Western Agricultural Economics Association Joint Annual Meeting, San Francisco, CA, July 26–28, 2015. Washington, DC: International Food Policy Research Institute..

Yoder, Joshua R., Corinne Alexander, Rastislav Ivanic, Stephanie Rosch, Wallace Tyner, and Steven Y. Wu. “Risk Versus Reward, a Financial Analysis of Alternative Contract Specifications for the Miscanthus Lignocellulosic Supply Chain.” Bioenergy Research 8, (2015): 644–656. https://doi.org/10.1007/s12155-014-9548-z.

1Adam. M. Komarek, Alessandro De Pinto, and Vincent H. Smith, "A Review of Types of Risks in Agriculture: What We Know and What We Need to Know," Agricultural Systems 178 (2020): 102738, https://doi.org/10.1016/j.agsy.2019.102738; Joy Harwood et al., Managing Risk in Farming: Concepts, Research, and Analysis (Washington DC: U.S. Department of Agriculture, 1999).

2Harwood et al., Managing Risk in Farming..

3Kim Morgan et al., Farm Financial Risk Management: Overview of Financial Systems for New and Beginning Farmers (Virginia State University, 2016), https://www.pubs.ext.vt.edu/AAEC/AAEC-114/AAEC-114.html.

4John Brian Hardaker, Some Issues in Dealing with Risk in Agriculture (Working Paper, University of New England Graduate School of Agricultural and Resource Economics, Australia, 2000), accessed August 1, 2021, http://www.une.edu.au/febl/EconStud/wps.htm.

5Ghassen Bouslama, and Younes Lahrichi, "Uncertainty and Risk Management from Islamic Perspective," Research in International Business and Finance 39, (2017): 718–726, https://doi.org/10.1016/j.ribaf.2015.11.018.

6Siddiq Mohammad Al-Ameen Al-Dhareer, Al-Gharar in Contracts and Its Effects on Contemporary Transactions (Jeddah: Islamic Research and Training Institute, 1997), 10.

7Ibid., 10.

8See for instance, al-Baqarah 2:188 which implies the prohibition of transactions involving ambiguity, uncertainty, fraud, or deception, as such practices lead to unjust consumption of wealth; al-Nisa' 4:29 which highlights the importance of mutual consent and clarity in trade, prohibiting transactions that involve deception, ambiguity, or uncertainty (Gharar); and al-Ma'idah 5:90 which prohibits gambling (Maysir), which shares similarities with Gharar by involving uncertainty, chance, and speculation.

9Sulaymān ibn al-Ashʻath Abu Dawood, Sunan Abī Da'ūd, ed. Muḥammad Muḥyī al-Dīn ʻAbd al-Ḥamīd (Beirut, Saida: Al Maktabah Al Asriya, 1392 AH), hadīth no. 3376; Ahmad bin Al Shuaib Al Nasaei, Al Sunan Al Kubra, ed. Hasan & Abdul Mohsin Al Turki Al Shalbi (Beirut: Al Risala, 2001), hadīth no. 4626 and 4518; Muslim ibn al-Hajjaj, Saheeh Muslim, ed. Muhammad Fuad Abdul Baqi (Beirut: Dar Ihya' Al Thurath Al Arabi, 1388 AH), hadīth no. 1513 and Abu Isa Mohammad Ibn 'Eisa al-Thirmithi, Sunan Al Thirmidhi, ed. Ahmad Muhammad Shakir and Muhammad Fuad Abdul Baqi (Egypt: Mustafa Al Babi Al Halabi, 1975), hadīth no. 1274.

10Al-Dhareer, Al-Gharar in Contracts and Its Effects on Contemporary Transactions, 9.

11Klaus Maurer, "Where is the Risk? Is Agricultural Banking Really More Difficult than Other Sectors?" in Kohn, D. (Ed.), Finance for Food: Towards New Agricultural and Rural Finance, (Berlin, Heidelberg: Springer, 2014); Harwood et al., Managing Risk in Farming.

12Ahamad Faosiy Ogunbado, and Umar Ahmed, "Bay' Salam as an Islamic Financial Alternative for Agricultural Sustainability in Nigeria," Journal of Islamic Economics Banking and Finance 11, (2015): 63–75, https://dx.doi.org/10.12816/0024789.

13Alan Livsey, and Harriet Clarfelt, "Defaults on Leveraged Loans Soar to Highest Rate in 4 years," www.ft.com, The Financial Times Limited, December 24, 2024, accessed March 8, 2025, https://www.ft.com/content/e6ba508c-4612-4b4a-9a6b-ecde6fc91c12.

14Sarah A. Drollette, "Managing Financial Risk in Agriculture," (Utah State, USA: Department of Applied Economics, Utah State University Extension, 2009), accessed December 14, 2021, https://extension.usu.edu/apec/files/uploads/agribusiness-and-food/risk-management/risk-management-factsheets/Managing-Financial-Risk.pdf; Satit Aditto, Christopher Gan, and Gilbert V. Nartea, "Sources of Risk and Risk Management Strategies: the Case of Smallholder Farmers in a Developing Economy," in Risk Management - Current Issues and Challenges, ed. Nerija Banaitiene (Intech Open, 2012), 449–474; Harwood et al., Managing Risk in Farming.

15Morgan et al. "Farm Financial Risk Management: Overview of Financial Systems for New and Beginning Farmers".

16Jeremy Michael Gregory Cole, "Behavioural Determinants of the Adoption of Financial Price Risk Management Tools by Wheat Farmers in England," (PhD diss., The University of Reading, 2014).

17Nigel Purves, Scott James Niblock and Keith Sloan, "On the Relationship between Financial and non-Financial Factors," Agricultural Finance Review 75, no. 2 (2015): 282–300, https://doi.org/10.1108/AFR-04-2014-0007; Edward I. Reinsel, "Off-Farm Income of People Involved in Farming," Journal of Agricultural and Applied Economics 2, no. 1 (2015): 115–119, https://doi.org/10.1017/S0081305200009900.

18Gabriel Popescu et al. "The Financial Relationships between Farmers, Credit Institutions and Public Authorities - Short Review," Ekonomika Poljoprivrede 65, no. 1 (2018): 427–436, https://doi.org/10.5937/ekoPolj1801427P.

19Cesar L. Escalante et al. "Looking Beyond Farm Loan Approval Decisions: Loan Pricing and Nonpricing Terms for Socially Disadvantaged Farm Borrowers," Journal of Agricultural and Applied Economics 50, no. 1 (2018): 129-148, https://doi.org/10.1017/aae.2017.25; Chandra K. Dhakal, Cesar L. Escalante, and Charles Dodson, "Heterogeneity of Farm Loan Packaging Term Decisions: A Finite Mixture Approach," Applied Economics Letters 26, no. 18 (2019): 1528–1532, https://doi.org/10.1080/13504851.2019.1584360.

20Shasha Li, "Financial Stress Test under Multiple Risks for Representative Farms of Central Illinois," (Master's Thesis, Purdue University, 2012), Purdue e-Pubs (AAI1535051).

21Meagan G. Merritt et al., "Probability of Receiving an Indemnity Payment from Feeder Cattle Livestock Risk Protection Insurance," Journal of Agricultural and Applied Economics 49, no.3 (2017): 363–381, https://doi.org/10.1017/aae.2016.44.

22Eric A. DeVuyst, et al., "Sources of Institutional Financial Risks in Agriculture," Risk Education Publication Series, Southern Risk Management Education Center, University of Arkansas System, (2013), accessed August 8, 2021. https://www.uaex.edu/publications/PDF/srme01fs.pdf.

23Meagan G. Merritt et al., "Probability of Receiving an Indemnity Payment from Feeder Cattle Livestock Risk Protection Insurance".

24Joshua R. Yoder et al., "Risk Versus Reward, a Financial Analysis of Alternative Contract Specifications for the Miscanthus Lignocellulosic Supply Chain," Bioenergy Research 8, (2015): 644–656, https://doi.org/10.1007/s12155-014-9548-z.

25Nicoleta Uzea et al. "Farm Support Payments and Risk Balancing: Implications for Financial Riskiness of Canadian Farms," Canadian Journal of Agricultural Economics 62, No. 4 (2014): 595–618, https://doi.org/10.1111/cjag.12043.

26Jan Fałkowski, Maciej Jakubowski, and Paweł Strawiński, "Returns From Income Strategies in Rural Poland," Economics of Transition and Institutional Change 22, no. 1 (2013): 139-178. https://doi.org/10.1111/ecot.12032.

27Apurba Shee, Calum G. Turvey, and Liangzhi You, "Design and Rating of Risk-Contingent Credit for Balancing Business and Financial Risks for Kenyan Farmers," Applied Economics 51, no. 50 (2019): 5447–5465, https://doi.org/10.1080/00036846.2019.1613502; Yahuza Salisu, Ahmed Ibrahim Mohammed, and Anas Muhammad Yakub, "The Mediating Effect of Murabahah Financing on the Relationship between Farm Land, Farm Infrastructure and Agricultural Output in Nigeria," International Journal of Management Research and Reviews 7, no. 12 (2017): 1080–1089. https://www.proquest.com/scholarly-journals/mediating-effect-murabahah-finance-on/docview/1992208983/se-2; Diana Fletschner, Catherine Guirkinger, and Steve Boucher, "Risk, Credit Constraints and Financial Efficiency in Peruvian Agriculture," The Journal of Development Studies 46, no. 6 (2010): 981–1002, https://doi.org/10.1080/00220380903104974; Chandra S. Kumar, Calum G. Turvey, and Jaclyn D. Kropp, "The Impact of Credit Constraints on Farm Households: Survey Results from India and China," Applied Economic Perspectives and Policy 35, no. 3 (2013): 508-527, https://doi.org/10.1093/aepp/ppt002; Shahab E. Saqib et al. "Factors Influencing Farmers' Adoption of Agricultural Credit as a Risk Management Strategy: The Case of Pakistan," International Journal of Disaster Risk Reduction 17, (2016): 67–76, https://doi.org/10.1016/j.ijdrr.2016.03.008.

28Kym Anderson, "Agricultural Price Distortions: Trends and Volatility, Past, and Prospective," Agricultural Economics 44, no. 1 (2013): 163–171, https://doi.org/10.1111/agec.12060; Parmod Kumar Singhal, and Vivek Mittal, "PMFBY - A Financial Inclusion Initiate for Farmers Development," International Journal of Business Ethics in developing Economies 6, no. 2 (2017): 39–43.

29Mohammad Obaidullah, "Enhancing Food Security with Islamic Microfinance: Insights from Some Recent Experiments," Agricultural Finance Review 75, no. 2 (2015): 142–168, https://doi.org/10.1108/AFR-11-2014-0033.

30Shee, Turvey, and You, "Design and Rating of Risk-Contingent Credit for Balancing Business and Financial Risks for Kenyan Farmers".

31Ulf Romer, and Oliver Musshoff, "Can Agricultural Credit Scoring for Microfinance Institutions be Implemented and Improved by Weather Data?" Agricultural Finance Review 78 (2018): 83–97, https://doi.org/10.1108/AFR-11-2016-0082.

32Ashenafi Duguma, "The Role of Agricultural Cooperatives in Risk Management and Impact on Farm Income: Evidence from Southern Ethiopia," International Journal of Economic Behavior and Organization 4, no.4, (2016): 39–67, https://doi.org/10.11648/j.ijebo.20160404.11.

33Patrick S. Ward et al., "Demand for Complementary Financial and Technological Tools for Managing Drought Risk: Evidence from Rice Farmers in Bangladesh" (Paper presented at the Agricultural and Applied Economics Association 2015 Joint Annual Meeting, San Francisco, CA, July 26–28, 2015), International Food Policy Research Institute.

34Khalishah Ulfah, and Muryani Arsal, "Muzara'ah Contract of Farmer Perspective," International Economics and Business Conference, 1 no. 1 (2023): 235–240, https://jurnal.amertainstitute.com/index.php/IECON/article/view/57; Maulidah Narastri, "Muzara'ah in Efforts for Economic Prosperity: Between Patterns of Behavior, Improvements and Demands," International Conference on Economic Business Management, and Accounting 2, 474–480, https://conference.untag-sby.ac.id/index.php/icoema/article/view/3028; Mustika Lestrai Ramadani, Siti Kholis Napsiah, and Muhammad Nur Iqbal, "Muzara'ah, Musaqoh And Mugharasah Contracts In Fiqh Muamalah," Jurnal Multidisiplin Sahombu 5, no. 1 (2025): 89–101; Eka Nurhalimatus Sifa, and Sudarso Kaderi Wiryono, "How Does Salam Financing Affect Farmers' Income? A System Dynamics Approach," Journal of Islamic Accounting and Business Research 15, no. 1 (2024): 119–135. https://doi.org/10.1108/JIABR-02-2022-0042.

35Kurniati, Sunuwati, Muhammad Majdy Amiruddin, and Abdul Syatar, "Bay Al Salam as Financing Alternative During Pandemic Outbreak: A Proposal to Indonesia," Academy of Entrepreneurship Journal 27, no. 5S (2021): 1–7, http://repositori.uin-alauddin.ac.id/id/eprint/19738.

36Rifaldi Majid, "Designing Salam-Muzara'ah Linked Waqf to Financing Agricultural Sector," Journal of Islamic Monetary Economics and Finance 7, No.3 (2021): 503–526, https://doi.org/10.21098/jimf.v7i3.1309.

37Abdullah Al-Bassam, Tawdheeh Al Ahkam Min Al Buloogh Al Maram, [Clarification of the provisions of Bulugh al-Maram] (Makkah: Maktaba Al Asadi, 1423 AH).

38Siddiq Mohammad Al-Ameen Al-Dhareer, "al-Salam wa-Taṭbīqātuhu al-Muʻāṣirah," [Salam and its Contemporary Practices], Majallat Mujamma' Al Fiqh Al Islami Al Duwali [Journal of the OIC Fiqh Academy] 9, (1991), https://al-maktaba.org/book/8356/17703. Accessed 17 July 17 2021; Al-Dhareer, Al-Gharar in Contracts and Its Effects on Contemporary Transactions.

39Krippendorff, Klaus, Content Analysis: An Introduction to Its Methodology, 4th ed. (Los Angeles: SAGE Publications, 2018).

40Aishath Muneeza, Nik Nurul Atiqah Nik Yusuf, and Rusni Hassan, "The Possibility of Application of Salam in Malaysian Islamic Banking System," Humanomics 27, (2011): 138–147, https://doi.org/10.1108/08288661111135135.

41Ishrat Hossain et al., "Support for Smallholder Farmers through Islamic Instruments: The Case of Bangladesh and Lessons for Nigeria," International Journal of Islamic and Middle Eastern Finance and Management 12, no. 2 (2019): 154–168, https://doi.org/10.1108/IMEFM-11-2018-0371.

42Ibid.

43Ahmad Kaleem, and Rana Abdul Wajid, "Application of Islamic Banking Instrument (Bai Salam) for Agriculture Financing in Pakistan," British Food Journal 111, no. 3 (2009): 275–292. https://doi.org/10.1108/00070700910941471.

44Ibid.

45Ibid.

46Ibid.

47Adam B. Elhiraika, On the Experience of Islamic Agricultural Finance in Sudan: Challenges and Sustainability (Jeddah, KSA: Islamic Development Bank, 2003); Khalid M Mustafa Aburaida, "Rural Finance as a Mechanism for Poverty Alleviation in Sudan with an Emphasis on Salam Mode." European Scientific Journal 7, no. 26 (2014): 157–166.

48Alagabi Abdghaffar Adedapo et al., "Bai Salam in the Light of Contemporary Application: Issues, Challenges and Recommendation," (Paper presented at Islamic Business Management Conference (IBMC), (Kuala Lumpur, August 18–19 2014). https://www.researchgate.net/publication/318317523.

49AAOIFI, Sharī'ah Standards (Bahrain, 2017). https://aaoifi.com/shariah-standards-3/?lang=en.

50Muhammad Hakimi Mohd Shafiai, and Mohammed Rizki Moi, "Financial Problems Among Farmers in Malaysia: Islamic Agricultural Finance as a Possible Solution," Asian Social Science 11, No. 4, (2015): 1-16, http://dx.doi.org/10.5539/ass.v11n4p1.

51Al-Bassam, Tawdheeh Al Ahkam Min Al Buloogh Al Maram [Clarification of the provisions of Bulugh al-Maram].

52Central Asset Management Capital Market, "Muzara'ah Sukuk (Farm-letting Sukūk)," accessed January 11, 2025, https://www.sukuk.ir/sukuk/types-of-sukuk/farm-papers/.

53AAOIFI, Shari'ah Standards (Bahrain, 2017), https://aaoifi.com/shariah-standards-3/?lang=en; Central Asset Management Capital Market, "Muzara'ah Sukuk (Farm-letting Sukūk)," accessed January 11, 2025, https://www.sukuk.ir/sukuk/types-of-sukuk/farm-papers/.

54Central Asset Management Capital Market, "Musaqah Sukūk (Irrigation Sukuk)," accessed January 11, 2025, https://www.sukuk.ir/sukuk/types-of-sukuk/employment-papers/.

55Ibid.

56Rohana Othman et al., "Islamic banking: The Firewall against the Global Financial Crisis," Journal of Applied Business Research 28, no. 1 (2012): 9–14. https://doi.org/10.19030/jabr.v28i1.6679.

57Ibn 'Umar reported that Allah's Messenger (pbuh) forbade the sale of fruits until they were clearly in good condition, he forbade it both to the seller and to the buyer (Sahih Muslim, Book 10 (KITAB AL-BUYU'), Number 3665)

58Al-Dhareer, Al-Gharar in Contracts and Its Effects on Contemporary Transactions.

59Al-Dhareer, Al-Gharar in Contracts and Its Effects on Contemporary Transactions; Ghassen Bouslama and Younes Lahrichi, "Uncertainty and Risk Management from Islamic Perspective,".

60This is a sale by which some trees in the garden that are dedicated for the use of poor. Ariyya Sale of a tree or two in which case the members of a poor farmer's family can get fresh dates for eating against the dry dates that they own is permitted exceptionally, provided that it does not exceed five wasaqs (i.e., 645kg), which he can sell to whomever he wants, to anyone who eats it fresh and to others. This is called Ariyyah or Araya sale.

61Muzabanah refers to the prohibition of selling fresh dates on palm trees, the prohibition of selling grapes in the vineyard for raisins, and the prohibition of selling crops before they are harvested. The reason for the prohibition in ribawi items, i.e., items sold by weight and measure, is the inequality and gharar, and in other than ribawi items the gharar arises as a result of not being able to verify the amount sold.

62Al-Dhareer, Al-Gharar in Contracts and Its Effects on Contemporary Transactions.

63Ghassen Bouslama and Younes Lahrichi, "Uncertainty and Risk Management from Islamic Perspective".

64Adedapo et al., "Bai Salam in the Light of Contemporary Application: Issues, Challenges and Recommendation".