Muhammad Mansoor Javed*, Adnan Bashir, and Waseemullah

University of Gujrat, Pakistan

* Corresponding Author: [email protected]

The present study evaluates the impact of Shariah compliance on profitability. By applying the fixed effect model, this study examines the impact of investment in partnership-based and non-partnership-based modes of financing on the financial performance of Islamic banks. Unbalanced panel data has been extracted from the financial reports (2008-2021) of all full-fledged Islamic banks operating in Pakistan. Shariah compliance is measured using two self- constructed proxies following experts survey; whereas financial performance is calculated as net income to average total assets. The study finds that investment in partnership-based modes of financing had a positive association with financial performance. However, the study fails to find any association between investments in non-partnership-based modes of financing and financial performance of Islamic banks. Moreover, the study recommends that Islamic banks should increase their investment in partnership-based mode of financings as it will increase their profitability and improve their public image of being ‘Islamic’.

Keywords: financial performance, fixed effect model, financial banks Islamic banks, Shariah compliance

JEL Classification: C43, G21, Z12

Shariah refers to that part of Islamic law, which is revealed and known as the primary source of Islamic law. These primary sources include the Holy Quran and the Sunnah (recited and non-recited revelations). Along with these primary sources, there are some other sources, which are derived through Ijtihaad. Ijtihaad is the process of reasoning by a Shariah scholar to develop Islamic legislation related to a new issue, while ensuring the true essence of Shariah and by applying other legitimate sources (Moqbel & Ahmed, 2021). These other legitimate sources can be further classified into secondary sources and tertiary sources. The secondary sources are ijma (unanimous agreement) and qiyaas (analogy); whereas tertiary sources include additional tools like isthisaan (juristic preference), istishaab (presumption of continuity), and maslahah (unrestricted interest). The main difference between these two sources is that all major fiqhi (jurisprudential) schools recognize the application of secondary sources; however, they are not unanimous in the application of tertiary sources. For example, Hanfi School allows the application of isthisaan (juristic preference); whereas Shafi School strictly prohibit it. This infers that Shariah compliance cannot be measured objectively (Moqbel & Ahmed, 2021).

In the context of Islamic finance, Shariah compliance is described as the compliance of operations and activities with the precepts of Shariah in terms of the pronouncements and their implementation, requisites of various contracts, as well as, fulfillment of the welfare objectives” (Khaleequzzaman et al., 2016). Therefore, Shariah compliance framework can be considered as a benchmark, which provides assurance regarding the Shariah legitimacy of financial products offered by Islamic banks. In other words, the Shariah compliance framework assists Islamic banks to differentiate themselves from their other conventional equivalents.

After its modest start in 1970, the Islamic banking industry has evolved globally. This rapid development can be considered as a success story; however, many experts opined that this dramatic growth was not a natural progress, which raised many questions regarding the legitimacy of Islamic financial products. This subjective criticism is based on the notion that instead of innovating new products, Islamic banks replicated conventional product and overlooked the social-economic values of the Islamic law in its true spirit.

Conversely, it was argued that in the absence of Islamic financial structure Muslim financial practitioners had to reluctantly rely on the conventional structure by adopting ‘replication approach’ (Laldin & Furqani, 2016). The ‘replication approach’ was adopted for two major reasons. Firstly, the functions of financial intermediaries and associated problems were similar in both Islamic and secular economies. Secondly, both Islamic and conventional finance were sharing the same financial market. Consequently, Islamic banks had to compete conventional banks to attract customers. Therefore, Islamic finance practitioners had to replicate conventional products and align profit rates to some conventional benchmarks to compete in the financial market. Contextually, the structuring of Islamic financial products was limited towards the transformation of conventional products, which occurred only by meeting minimum Islamic legal requirements (Saeed, 2004).

The financial products offered by the Islamic banks are mainly classified into two groups, namely , partnership-based products and non-partnership-based modes (Tegambwage & Kasoga, 2023). The partnership-based products were developed by applying the concepts of Musharakah and Muḍarabah. Non-partnership-based modes were further divided into Trade-based products and leased-based products. Trade-based modes are based on the notions of Murabaha, Istisna, and Salam. The leased-based products were based on the Shariah concept of Ijarah (renting).

The partnership-based products are the spirit of Islamic finance as they ensure the sharing of both risk and reward by the contracting parties. However, trade-based products and leased-based products do not differ from their conventional alternatives, considering their economic substance,therefore, should only be used when Shariah compliant alternatives are not available (Hanif, 2018). Kalim and Arshed (2018) argued that the dependency on trade-based modes of financing would decrease the deposit returns of Islamic banks.The main criticism on trade-based and leased-based products is that Islamic banks are not expose to any kind of business risk, while offering such trade-based financing. Consequently, they failed to meet the key requirement of the Islamic law that stated “any benefits derived from a transaction must be accompanied with the liability arising from a potential loss.” This undermined the Shariah legitimacy of these non-partnership based mode of financing (Javed et al., 2022).

Nevertheless, as per Islamic Banking Bulletin by State Bank of Pakistan (September 2022), more than 85% of the financial products of Islamic banks are trade-based. According to this report, diminishing Musharakah is the most frequently used mode of financing, which is offered for non-current asset financing such as auto, plant, and house financings (Javed et al., 2015). Diminishing Musharakah is a combination of three separate contracts, namely Musharakah (partnership), Ijarah (leasing), and bay(sale). The sequence of the transactions is as follows. Firstly, partnership contract is executed where the customer and the bank jointly purchase a particular asset. Second, Ijarah contract is executed where the bank gives units of its share to the customer on rent. Lastly, sale contract is executed where the customer gradually purchased the units of the bank’s share; accordingly, the rent starts decreasing (Hassan, 2020). Shariah require that all contracts should be independent of each other (Ayub, 2007). However, arguably it was claimed that Islamic banks violate this requirement and negotiate these three contracts in one deal (Shaikh, 2023).

Similarly, Murabahah is a type of sale where the seller discloses purchasing cost of the product to the buyer and profit margin is decided through bargain. However, Islamic banks execute this type of sale as a mode of financing. The customer approaches the bank to purchase a certain commodity. The bank appoints the customer as its agent and assign him a duty to purchase the required commodity on bank’s behalf, whereas the bank directly makes the payment to the seller. Later, the customer purchases the commodity from the bank on cost plus profit and makes deferred payment. Thus, the bank never takes even the constructive procession of the commodity and does not expose to any type of trading risk; consequently, the transaction becomes invalid. Furthermore, some Islamic banks offer Murabahah financing for the payment of operating expense, which is also unacceptable as no acquisition of commodity involves such transactions (Usmani, 2021).

Likewise, Salam is a type of sale contract where payment of the commodity is received in full at spot but goods are delivered at some specified future date. Thus, the Salam can be used as a mode of financing especially for agriculture sector. The Islamic banks provide financing as a cash price for goods to be produced and delivered in future at some lower rate as compared to the rate of those goods delivered on spot. The difference between two prices is a legitimate profit for Islamic banks. Later, Islamic banks sell the purchased commodity to a third party through a contract of parallel Salam. However, sometimes bank sell back the same commodity to the original seller even before taking the delivery of goods through a pre-arranged sale back contract. This practice is against the dictates of Shariah (Waluyo & Rozza, 2020).

Similarly, Ijarah is originally a contract of transferring the usufruct of some asset to another person for an agreed rent and for a specified period. However, most Islamic banks use this rental contract as a long-term mode of financing and link the rental rate to some conventional benchmark. This arrangement of Ijarah is identical to conventional financial lease. Moreover, in Ijarah contract, many other Shariah requirements are also overlooked. For example, being the owner of the leased asset, it is the bank’s responsibility to bear takaful (Islamic insurance) expenses. However, in practice, Islamic banks (lessor) recover these expenses from the customer (lessee), which is questionable. Likewise, as per Islamic law, lessee can be responsible for the loss incurred due to his negligence and cannot be responsible for the loss incurred by any unavoidable circumstances. However, in practice, both situations are not considered separately and lessee has to bear all types of expenses (Saleem et al., 2022).

Usmani (2021) argued that one of the main differences between conventional and Islamic banks is that profit maximization is not a sole objective of Islamic banks. In fact, as per Islamic ideologies, business transaction is related to the ethical objective of the prosperity of the society. This ethical objective can be achieved by realizing Maqasid al-Shariah (rationale behind Shariah ruling). In other words, financial products offered by Islamic banks cannot be considered Shariah compliant unless these products have a role in achieving the Maqasid al-Shariah. In the context of Islamic finance, these Maqasid al-Shariah requires “circulation of wealth, transparency, and justice” (Laldin & Furqani, 2013). Circulation of wealth ensures that wealth is not accumulated in a few hands (Quran 6:141). Transparency ensures that contracting parties are well aware of all the details of the contract (Quran 2: 282). Justice ensures that all individuals have equal opportunities (Quran 2:188).

However, prior empirical studies reported that Islamic banks failed to realize the above stated Maqasid al-Shariah due to their reliance on the controversial financial products. (Javed et al., 2020; Javed & Kalim et al., 2022).Therefore, Islamic banks are required to improve their Shariah compliant rating to differentiate themselves from other conventional banks in true spirit. In this context, to encourage the top management of Islamic banks, this study evaluated the impact of Shariah compliance on financial performance, as better Shariah compliance may lead to better financial performance.

This research is sub-categorized as follows: section 2 summarizes the existing literature, section 3 describes the research methodology deployed for this study, section 4 explains the findings of the study, and section 5 concludes the overall research.

The premise of the association between Shariah compliance and profitability is based on the concept of Islamic worldview, which considers each person as Allah's vicegerent who has been bestowed with resources to be consumed for the benefit of the whole society. The fulfillment of this obligation brings Divine blessing, which can be defined as an increase in the benefits of the entrusted resources. It infers that compliance to Divine ruling or Shariah compliance increase utility and profitability (Javed & Bukhari et al., 2022)

In the context of the objective selected for the current study, the existing literature can be classified into two groups. The first group observes the impact of Shariah compliance on customers behaviour, and the second examines the effect of Shariah compliance on the financial performance and profitability of Islamic banks as discussed below.

Impact of Shariah Compliance on Customers Behaviour

A large number of studies have concluded that Shariah compliance has a positive impact on the customer satisfaction (Okumus, 2015; Ongera & Ndede, 2019). However, some studies identified various mediators and moderators that influence this relationship. For example, Suhartanto et al. (2018) claimed that the positive impact of religiosity on loyalty of customers is mediated by customer's trust. Likewise, Suhartanto et al. (2019) asserted that customer loyalty is based on religiosity and emotional attachment regardless of service quality. On the other hand, Ahmed at el. (2022) reported that service quality mediate the association between Shariah legitimacy and customer satisfaction. Usman et al. (2022) found that Shariah compliance, belief in Shariah compliance, and knowledge about Shariah compliance have a significant positive effect on the satisfaction of customers using e banking. In a recent study, Tegambwage and Kasoga (2023) reported that religious affiliation is a significant moderator of association between customer satisfaction and customer loyalty, as well as service quality and loyalty. However, they reported insignificant effect of religious affiliation based on the association between relationship quality and loyalty.

In contrast, some studies claimed that Shariah compliance has no impact on the customer behaviour as customers prefer Islamic banks due to some non-religious reasons. For example, Javed et al. (2015) analyzed the demand of Islamic house financing in Pakistan and found that majority of the potential customers of Islamic banks are conventional who use Islamic financial services only when they are less expensive regardless of their Shariah compliant status.

Impact of Shariah Compliance on Financial Performance

Numerous studies have evaluated the association between social and financial performances of Islamic banks. Nevertheless, only a limited number of studies have explored the impact of Shariah compliance on the financial performance as summarize below.

Arshad et al. (2012) used Islamic CSR disclosures as a proxy to measure Shariah legitimacy of Islamic banks and examined its impact on the financial performance of Malaysian Islamic banks. After analyzing three years's data (2008-2010), they reported that Islamic CSR disclosures had a positive relationship with both financial performance and bank reputation. Similar results were reported by Iqbal et al. (2013) who measured Shariah compliance using three dimensions, namely health, donation, and education. Zaki et al. (2014) measured Shariah compliance through Shariah board characteristics and Zakah performance and examined its influence on financial performance taking the sample from seven Islamic banks operating in Asia. They found a significant negative impact of both Shariah board characteristics and Zakah performance on financial performance. Similarly, Fahlevi et al. (2017) measured Shariah legitimacy using a Shariah conformity index based on three elements, namely profit-sharing ratio, Islamic investment, and Islamic income. After analyzing three years data of 18 Malaysian and Indonesian Islamic banks, they reported a negative relationship between Shariah legitimacy and profitability. On the contrary,Firman et al. (2016) reported a significant positive relationship between Zakah performance and profitability after analyzing the data form nine Indonesian Islamic banks. Conversely, Kholidah (2018) measured Shariah compliance by constructing Islamic social performance index, which was based on four items, namely Qard financing, Zakah ratio, Musharakah financing, and Muḍarabah financing. He found a positive relationship between Shariah compliance based on composite index and the financial performance. However, he did not find any relationship between Musharakah financing and financial performance, and Muḍarabah financing and financial performance.

Conversely, in a similar study, Sutrisno and Widarjono (2018) reported a positive association between Musharakah financing and profitability and negative relationship between Muḍarabah financing and profitability. In another study, Nasution et al. (2018) found a significant positive correlation between profit sharing ratio and profitability, which had a negative association between Zakat performance ratio and profitability. Additionally, they reported insignificant relationship between Islamic income ratio and profitability. These results are in consistent with the findings of Romadhonia and Kurniawati (2022). On the other hand, Hosen et al. (2019), measured Shariah compliance based on the Maqasid al-Shariah orientation using three constructs, namely educating individuals, justice, and public interest as proposed by Dzuljastri et al. (2008). By analyzing three years data (2010-2012) of eight full-fledged Indonesian Islamic banks, they found an insignificant correlation between Maqasid al-Shariah orientation and the financial performance. In a similar study, Hidayat et al. (2019) analyzed six year's data (2010-2015) of six full-fledged Indonesian Islamic banks and revealed that the composite Maqasid oriented performance has a positive correlation with the financial performance. However, they reported that only public interest dimension of Maqasid oriented performance had a positive association with profitability.

However, in a similar study, Hamsyi (2019) reported contradictory results as he found a significant positive correlation between Islamic income ratio and profitability and insignificant correlation between profit sharing ratio and profitability.

Siswanti et al. (2021) found that the impact of Islamic income ratio on profitability is moderated by corporate social performance. On the other hand, Alam et al. (2022) found that Shariah Supervisory Board management had a positive relationship with Shariah compliance and bank reputation. In a similar study, Nidyanti and Siswantoro (2022) found that most Islamic banks operating in Asia meet Shariah compliant criteria. However, their study could not find any significant relationship between Shariah compliance and profitability, considering both accounting-based and market-based measures. Sari et al. (2023) found that Islamic investment ratio has a positive impact on the internal fraud, whereas profit sharing ratio had a negative impact on internal fraud.

The inconsistent results of the existing literature warrant further research in this area. In this context, the current study contributes to two fold results. First, it constructs an improved proxy to measure Shariah compliance. Second, the study evaluated the impact of both Shariah compliant participatory and non-participatory financial products on financial performance of Islamic banks, whereas, as per authors knowledge, existing literate excludes the effect of non-participatory financial products.

The current study developed the following two hypotheses based on the above literature.

H1= Shariah compliant partnership-based products positively affect the profitability of Islamic banks.

H2 = Shariah compliant non-partnership-based products positively affect the profitability of Islamic banks.

The current study's population comprised all full-fledged Islamic banks operating within Pakistan. Since there are only five such banks all of them were considered as the sample for conducting this study's analysis. These banks are Meezan Bank, Dubai Islamic Bank, Al-Baraka Bank, MCB Islamic Bank, and Bank Islami, respectively. The unbalanced panel data was extracted from the financial statements of these banks ranging from 2008-2021.

Following regression model was developed to examine the effect of Shariah compliance on the financial performance of the selected Islamic banks.

|

ROAAit |

= f (ShP it , ShN it ,CV it) |

|

Where |

|

|

ROAAit |

= Return on Average Asset of Bank i in year t |

|

ShPit |

= Shariah Compliant Participatory Products of Bank i in year t |

|

ShNit |

= Shariah Compliant Non-Participatory Products of Bank i in year t |

|

CVit |

= Control Variables of Bank i in year t |

The variables used in the model are explained below.

Profitability is the dependent variable of the current study. Therefore, the existing literature measured profitability using a wide range of market-based and accounting-based proxies. However, market-based proxies cannot be used, while examining the relationship between profitability and Shariah compliance as all the sampled banks are not listed on Pakistan Stock Exchange (PSX). Therefore, this study used accounting-based proxy, namely return on average asset (ROAA), which is frequently used in the existing literature (Platonova et al., 2018). The current study also measured ROAA as net income to average total assets (Platonova et al., 2018).

Shariah compliance is the independent variable of this study. Therefore, the existing literature measures Shariah compliance by using different proxies such as Musharakah and Muḍarabah financing to total financing ratio (Sutrisno & Widarjono, 2018), Zakat to total assets ratio (Nasution et al., 2018), Islamic income ratio (Hamsyi, 2019), and ratio of non-controversial modes of financing (Javed et al., 2020). The major limitations of all these proxies was that they reduced the scope of Shariah compliance and tried to measure Shariah compliance objectively; whereas Shariah compliance cannot be measured objectively due to its diverse interpretations of various sources of Islamic jurisprudence.

Considering the above limitations, the current study measured the Shariah compliance through an expert survey method following some similar studies (Javed et al., 2020). Eight Shariah experts, who had a relevant experience, were requested to assign weights to different financial products, considering their application in the modern Islamic banking and their compliance to Shariah principles. The average of these weights are shown in Table 1.

Table 1

Average Weights

|

Type |

Modes |

Average Weights |

|

Partnership-based Financial Products |

Musharakah |

96% |

|

Muḍarabah |

94% |

|

|

Diminishing Musharakah |

72% |

|

|

Running Musharakah |

69% |

|

|

Non-Partnership based Financial Products |

Murabaha |

58% |

|

Musawamah |

74% |

|

|

Salam |

68% |

|

|

Istisna |

70% |

|

|

Ijarah |

68% |

Using the above weights, this study develops following two proxies to measure Shariah compliance so that the effect of Shariah complaint partnership-based products and Shariah complaint non-partnership-based products can be compared.

ShPit = ∑PitW

ShNit = ∑NitW

Where

|

ShPit = |

Shariah Compliant Partnership based Products of bank i in year t |

|

ShNit = |

Shariah Compliant Non-Partnership based Products of bank i in year t |

|

Pit = |

Percentage of the given partnership based product to total products of bank i in year t |

|

Nit = |

Percentage of the given non-partnership based product to total products of bank i in year t |

|

W = |

Average Weight assigned to the given product (shown in Table 1) |

Control Variables

Following some earlier studies, this study uses some control variables, while examining the relationship between Shariah compliance and profitability. These control variables are shown in Table 2.

Table 2

Description of Variables

|

Variable |

Measurement |

Reference |

|

Dependent Variable |

||

|

Return on Average Asset (ROAA) |

Net income to average total assets |

Jewell and Mankin (2011) |

|

Independent Variable |

|

|

|

Partnership Based Products (ShP) |

Self-constructed proxy |

Authors’ contribution |

|

Non-Partnership Based Products (ShN) |

Self-constructed proxy |

Author’s contribution |

|

Control Variables |

||

|

Capital Ratio (CapRto) |

Equity capital to average total assets |

Platonova et al. (2018) |

|

Operating Expense Ratio (OprExp) |

Total non-interest expense to average total assets |

Iskandar (2017) |

|

Liquidity Risk (LiqRsk) |

Total financing to total assets |

Hassan and Khan (2019) |

|

Capital Intensity (CapInt) |

FixeTd assets to total assets |

Maqbool and Zameer (2018) |

The above Table 3 exhibits descriptive statistics related to various variables. The values of ROAA vary between -.0311-.0294. The mean of ROAA is .0034, whereas its standard deviation is .0103. The value of standard deviation is higher than the value of mean. This indicates that ROAA is over dispersed such as the ROAA of the sampled banks is not following a similar pattern. The reason of this dissimilar pattern is that some Islamic banks earn profits, whereas other Islamic banks suffer from major loss during the same period.

Similarly, the values of ShP range between .0435-0.7985 with mean value of .4289 and standard deviation 0.1594. Likewise, the values of ShN vary between 0.1254-.9986. Its mean value is registered at 0.4512, whereas standard deviation is recorded .2306. The minimum and maximum values of CapRto are registered at 0.469 and 0.5309, respectively with a mean value of .1062 and standard deviation of .0782. Similarly, the maximum and minimum values of OprExp are recorded at .0206 and .0791, respectively. Its mean value is .0377 and standard deviation is .0129. Likewise, the values of LiqRsk range between .0063-1.836, whereas its mean value is .5512 and standard deviation is .2613. Similarly, the values of CapInt vary between .0060-.100. Its mean value is recorded at .0325 and standard deviation is registered at .0205. The values of standard deviation of all these variables are lower than the value of mean, indicating that these variables are under dispersed and their data is following the same pattern.

Table 3

Descriptive Statistics

|

Variable |

N |

Mean |

Std. Dev |

Min |

Max |

|

ROAA |

62 |

0.0034 |

0.0103 |

-0.0311 |

0.0294 |

|

ShP |

62 |

0.4289 |

0.1594 |

0.0435 |

0.7985 |

|

ShN |

62 |

0.4512 |

0.2306 |

0.1254 |

0.9986 |

|

CapRto |

62 |

0.1062 |

0.0782 |

0.0469 |

0.5309 |

|

OprExp |

62 |

0.0377 |

0.0129 |

0.0206 |

0.0791 |

|

Liqrsk |

62 |

0.5512 |

0.2613 |

0.0063 |

1.836 |

|

CapInt |

62 |

0.0325 |

0.0205 |

0.0060 |

.1001 |

The current study applied some diagnostic tests to confirm the validity of the given data for the application of regression analysis. These tests include Pearson Correlation Matrix, Wooldridge test, Modified Wald test, and Hausman test. Correlation values of the given variables (shown in Table 4) confirmed that no multicollinearity exists among the stated variables (Brooks, 2008). However, Modified Wald test (p value = 0.000) confirms the existence of heteroscedasticity in the data set. This issue is resolved by applying robust model. On the other hand, Wooldridge test (p value = 0.2504) confirmed that data has no autocorrelation. Hausman test (p value = 0.004) confirmed that fixed effect model was more reliable than random effect model.

Table 4

Pearson Correlation Matrix

|

|

ROOA |

ShN |

ShP |

CapRto |

OprExp |

Lqrisk |

CapInt |

|

ROAA |

1.0000 |

|

|

|

|

|

|

|

ShP |

0.6722 |

1.0000 |

|

|

|

|

|

|

ShN |

0.0442 |

0.1546 |

1.0000 |

|

|

|

|

|

CapRto |

-0.4319 |

-0.5321 |

-0.2068 |

1.0000 |

|

|

|

|

OprExp |

-0.6454 |

-0.4871 |

-0.1885 |

0.7456 |

1.0000 |

|

|

|

Lqrisk |

0.0498 |

0.3234 |

0.2796 |

-0.2433 |

-0.1070 |

1.0000 |

|

|

CapInt |

-0.6376 |

-0.6929 |

-0.2395 |

0.7411 |

0.7755 |

-0.1865 |

1.0000 |

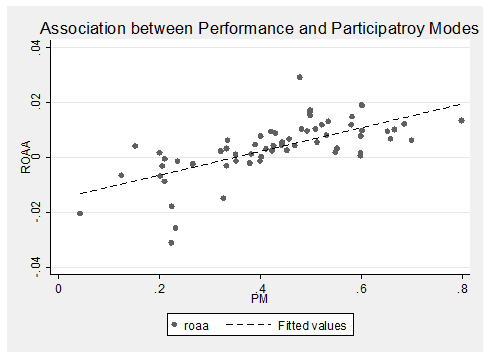

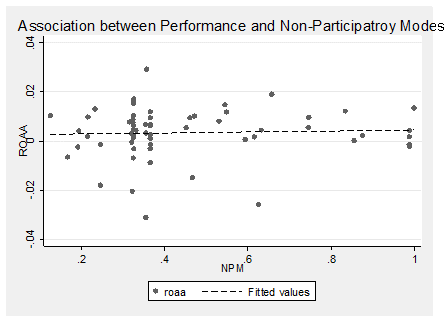

Figure 1 presents the graphical relationship between financial performance of Islamic banks and their investment in participatory modes of financings. The figures show that banks with higher investment in participatory modes of financings have better financial performance. On the other hand, no such relationship is found in case of investment in non-participatory modes of financings as shown in Figure 2.

Figure 1

Association between Performance and Participatory Modes of Financings

Figure 2

Association between Performance and Non-participatory Modes of Financings

Though the Hausman test (p value = 0.004) suggested that fixed effect model was more appropriate than random effect model; however, the current study applied both models for the comparison purposes. Table 5 shows the results of both Fixed Effect and Random Effect models. The Model Significance values (0.000) suggested that both models were significant. Similarly, the value of R2 proposed that fixed effect model described 62% of variation in ROAA; whereas random effect model described almost 65% of variations in ROAA.

The fixed effect model showed that the relationship between partnership-based products (ShP) and profitability (ROAA) was positive but the association between non-partnership-based products (ShN) and profitability was negative.Consequently, ROAA increased by 2.4% if ShP increase by one unit. On the other hand, ROAA decreased by 0.1% if ShN increase by one unit. However, p-values suggested that the relationship between ShP and ROAA was significant but the association between ShN and ROAA was insignificant. The random effect model highlighted the similar results.

A possible reason of the significant positive relationship between ShP and financial performance was that investing in ShP increase customer's trust on Islamic banks resulting in gaining customers loyalty. Accordingly, the current study confirmed the first hypothesis regarding the existence of a positive relationship between ShP and ROAA. On the other hand, this study does not support the second hypothesis regarding the existence of a positive relationship between ShN and ROAA. These findings were in consistent with the results of Javed et al. (2022) who found a significant positive relationship between financial performance and Shariah compliance. Furthermore, the Islamic concept of barakah also supported the results of this study.

Considering the control variables, the current study found a significant positive relationship between CapRto and ROAA. The identified reason of this positive relationship was that banks who had a better capital ratio were in a desirable position to invest in profitable projects than banks who had a worse capital ratio. In contrast, the study found a negative association between OprExp and ROAA as increase in expenses would simultaneously reduce the distributable profits. Random effect model also produced similar results.

Table 5

Regression Analysis Results Considering ROAA as Dependent Variable

|

|

Robust Fixed Effect Model |

Robust Random Effect Model |

||

|

|

Coefficient |

p-Values |

Coefficient |

p-Values |

|

ShP |

0.024 |

0.031** |

0.035 |

0.000*** |

|

ShN |

-0.001 |

0.658 |

-0.003 |

0.800 |

|

CapRto |

0.048 |

0.014** |

0.039 |

0.002*** |

|

OprExp |

-0.497 |

0.021** |

-0.449 |

0.002*** |

|

Lqrisk |

-0.003 |

0.212 |

-0.004 |

0.281 |

|

CapInt |

-0.027 |

0.806 |

-0.039 |

0.696 |

|

Constant |

0.010 |

0.029** |

0.006 |

0.015** |

|

p |

|

0.000*** |

|

.000*** |

|

R2 |

|

0.6215 |

|

0.645 |

Note. Dependent Variable: ROAA.

Significant *10%. **5%,***1%

Islamic banking institutions were introduced as an alternative to conventional banking institutions to eliminate the interest elements, uncertainty, and speculations from financial transactions. Accordingly, Islamic banks developed several alternative financial products, which meet various financial needs of customers without violating the ruling of Islamic law.

These products can be broadly divided into two categories, namely participatory financial products and non-participatory financial products. The participatory financial products are the essence of Islamic finance as they are profit and loss-based sharing principles. On the other hand, non-participatory financial products are mostly trading and renting-based agreements. However, in this paper it was argued that while pursuing the main objective of wealth maximization, Islamic banks avoid risk and rely on trade and rental-based financial products. Arguably, these non-participatory financial products were developed in such a way that their economic substance should be the same as that of their conventional equivalent. This practice of developing identical financial products jeopardizes the reputation of Islamic banks. Thereby, the current study explored the impact of both participatory and non-participatory financial products on financial performance as better Shariah compliance, which may lead to a better financial performance.

Therefore, the current study examined the unbalanced panel data extracted from the financial reports (2008-2021) of all full-fledged Islamic banks operating in Pakistan. By applying both fixed and random effects models, the study found that participatory-based financial products had significant positive impact on the financial performance; whereas non-participatory-based financial products had an insignificant negative impact on the financial performance of Islamic banks. Hence, the study suggested that Islamic banks should increase their reliance on participatory-based financial products, as it would not only improve their image of being Islamic but it would also increase their financial performance as a whole. Additionally, the current study recommended that future studies should explore the abiding relationship between investment in individual financial products and performance so that optimum level of profitability could be determined.

Ahmed, S., Mohiuddin, M., Rahman, M., Tarique, K. M., & Azim, M. (2022). The impact of Islamic Shariah compliance on customer satisfaction in Islamic banking services: Mediating role of service quality. Journal of Islamic Marketing, 13(9), 1829–1842. https://doi.org/10.1108/JIMA-11-2020-0346

Alam, M. K., Rahman, M. M., & Runy, M. K. (2022). The influences of Shariah governance mechanisms on Islamic banks performance and Shariah compliance quality. Asian Journal of Accounting Research, 7(1), 2–16. https://doi.org/10.1108/AJAR-11-2020-0112

Arshad, R., Othman, S., & Othman, R. (2012). Islamic corporate social responsibility, corporate reputation and performance. World Academy of Science, Engineering and Technology, 64(1), 1070–1074. http://doi.org/10.5281/zenodo.1074857

Ayub, M. (2007). Understanding Islamic Finance. John Wiley & Sons Ltd.

Brooks, C. (2008). Introductory econometrics for finance. Cambridge University Press.

Dzuljastri, A. R., Omar, M. M., & Fauziah, M. T. (2008). The performance measures of Islamic banking based on the Maqasid framework (Paper presentations). Paper presented at IIUM International Accounting Conference, Putra Jaya Marroitt.

Fahlevi, H., Irsyadillah, & Randa, P. (2017). Financial performance and sharia compliance: A comparative analysis of Indonesian and Malaysian Islamic banks. Business & Economics Review, 26(2), 41–52.

Firman, M., Lanita, W., & Mohammad, H. (2016). The Influence of CSR Practices on Financial Performance: Evidence From Islamic Financial Institutions in Indonesia. Journal of Modern Accounting and Auditing, 12(2), 77–90.

Hamsyi, N. F. (2019). The impact of good corporate governance and sharia compliance on the profitability of Indonesia’s Sharia banks. Problems and Perspectives in Management, 17(1), 56–66. http://dx.doi.org/10.21511/ppm.17(1).2019.06

Hanif, M. (2018). Sharīʿah-compliance ratings of the Islamic financial services industry: A quantitative approach. ISRA International Journal of Islamic Finance, 10(2), 162–184. https://doi.org/10.1108/IJIF-10-2017-0038

Hassan, K., & Khan, A. (2019). Liquidity risk, credit risk and stability in Islamic and conventional banks. Research in International Business and Finance, 48, 17–31. https://doi.org/10.1016/j.ribaf.2018.10.006

Hassan, S. (2020). Diminshing musharakah: Concept and practice by Islamic financial institutions of Malaysia and Bangladesh. Talent Development & Excellence, 12(2), 2280–2294.

Hidayat, R., Oktaviani, Y., & Aminudin, A. (2019). Financial performance of Islamic banking In Indonesia with maqasid shariah approach. Manajemen Bisnis, 9(1), 85–97.

Hosen, M. N., Jie, F., Muhari, S., & Khairman, M. (2019). The effect of financial ratios, Maqasid sharia index, and index of Islamic social reporting to profitability of Islamic bank in Indonesia. Al-Iqtishad: Jurnal Ilmu Ekonomi Syariah, 11(2), 201–222.

Iqbal, N., Ahmad, N., & Kanwal, M. (2013). Impact of corporate social responsibility on profitability of Islamic and conventional financial institutions. Applied Mathematics in Engineering, Management and Technology, 1(2), 26–37.

Iskandar, Y. (2017). The effect of non performing loans, operating expense to operating income, and loan to deposit ratio on stock return at conventional banks. Jurnal Entrepreneur dan Entrepreneurship, 6(1), 25–30. https://doi.org/10.37715/jee.v6i1.636

Javed, M. M., Ayaz, M., & Kalim, R. (2020). Revisiting the index to measure Maqasid Al-Shariah oriented performance of Islamic banks: Evidence from Pakistan. Journal of Islamic Business and Management, 10(1), 12–27. https://doi.org/10.26501/jibm/2020.1001-002

Javed, M. M., Bukhari, S. M. H., & Bashir, A. (2022). Impact of shariah compliance on financial performance of Islamic banks: Evidence from Pakistan. Islamic Banking and Finance Review, 9(1), 1–18. https://doi.org/10.32350/ibfr.91.01

Javed, M. M., Kalim, R., & Ayaz, M. (2022). Impact of Maqasid al-Shariah based social performance on financial performance of Islamic banks: Evidence from Pakistan. Empirical Economic Review, 5(1), 74–89. https://doi.org/10.29145.eer.51

Javed, M. M., Khan, M. M. S., & Aslam, H. (2015). Islamic house financing in Pakistan: A demand analysis. Islamic Banking and Finance Review, 2, 01–15. https://doi.org/10.32350/ibfr.2015.02.01

Jewell, J. J., & Mankin, J. A. (2011). What is your ROA? An investigation of the many formulas for calculating return on assets. Academy of Educational Leadership Journal, 15, 79–91. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2155943

Kalim, R., & Arshed, N. (2018). What determines the social efficiency of Islamic banking investment portfolio? Journal of Islamic Business and Management, 8(2), 386–406. https://doi.org/10.26501/jibm/2018.0802-004

Khaleequzzaman, M., Mansoori, M. T., & Rashid, A. (2016). Sharī‘ah legitimacy of Islamic banking practices in Pakistan: An evaluation. Journal of Islamic Business and Management, 6(1), 76–96.

Kholidah, H. (2018). The Effect of social performance to the profitability of Islamic banks. The International Journal of Applied Business, 2(2), 58–68. http://dx.doi.org/10.20473/tijab.V2.I2.2018.58-68

Laldin, M. A., & Furqani, H. (2013). Developing Islamic finance in the framework of maqasid al-Shari'ah: Understanding the ends (maqasid) and the means (wasa'il). International Journal of Islamic and Middle Eastern Finance and Management, 6(4), 278–289. https://doi.org/10.1108/IMEFM-05-2013-0057

Laldin, M. A., & Furqani, H. (2016). Innovation versus replication: Some notes on the approaches in defining shariah compliance in Islamic finance. Al-Jami'ah: Journal of Islamic Studies, 54(2), 249–272. https://doi.org/10.14421/ajis.2016.542.249-272

Maqbool, S., & Zameer, M. N. (2018). Corporate social responsibility and financial performance: An empirical analysis of Indian banks. Future Business Journal, 4(1), 84–93. https://www.sciencedirect.com/science/article/pii/S2314721017300543

Moqbel, T., & Ahmed, H. (2021). Flexibility and Sharīʿah compliance of Islamic financial contracts: An evaluative framework. Arab Law Quarterly, 35(1-2), 92–115.

Nasution, A. A., Lubis, A. F., & Fachrudin, K. A. (2018). Sharia compliance and Islamic social reporting on financial performance of the Indonesian sharia banks. Advances in Social Science, Education and Humanities Research, 292(1), 640–644. https://doi.org/10.2991/agc-18.2019.96

Nidyanti, A., & Siswantoro, D. (2022). Shariah compliance level of Islamic Banks in Asia and its implications on financial performance and market share. European Journal of Islamic Finance, 9(1), 15–21. https://doi.org/10.13135/2421-2172/6025

Okumus, H. S. (2015). Customers’ bank selection, awareness and satisfaction in Islamic banking: Evidence from Turkey. International Journal of Business and Social Science, 6(4), 41–54.

Ongera, F. K., & Ndede, F. (2019). Shariah banking and financial performance of selected commercial banks in Kenya. International Journal of Current Aspects, 3(6), 50–66. https://doi.org/10.35942/ijcab.v3iVI.78

Platonova, E., Asutay, M., & Dixon, R. (2018). The impact of corporate social responsibility disclosure on financial performance: Evidence from the GCC Islamic banking sector. Journal of Business Ethics, 151(2), 451–471. https://doi.org/10.1007/s10551-016-3229-0

Romadhonia, S., & Kurniawati, S. L. (2022). The effect of Islamic corporate governance, sharia compliance, Islamic social responsibility on the profitability of sharia banks. Journal of Economic Studies, 6(1), 90–104. http://dx.doi.org/10.30983/es.v6i1.5566

Saeed, A. (2004). Islamic banking and finance: In search of a pragmatic model. In V. Hooker & A.Saikal (Eds.), Islamic perspectives on the new millennium (pp. 113–129). Institute of Southeast Asian Studies.

Saleem, S., Baig, U., & Kavaliauskiene, I. M. (2022). Attaining standardization in Islamic banking institutions in Pakistan: Analysis on Ijarah financing. Journal of Risk and Financial Management, 15(10), Article e430. https://doi.org/10.3390/jrfm15100430

Sari, D. N., Fakhruddin, I., Pramono, H., & Pratama, B. C. (2023). The role of sharia compliance, Islamic corporate governance and company size in preventing internal fraud. Jurnal Ekonomi, 12(01), 335–344.

Shaikh, S. A. (2023). Some observations on contemporary financial proposals. International Journal of Ethics and Systems, 39(2), 464–480. https://doi.org/10.1108/IJOES-03-2021-0067

Siswanti, I., Sharif, S. M., & Indrajaya, S. (2021). The role of corporate social responsibility and sharia compliance on Islamic banks performance in Indonesia and Malaysia. The Journal of Asian Finance, Economics and Business, 8(6), 983–992.

Suhartanto, D., Farhani, N. H., & Muflih, M. (2018). Loyalty intention towards Islamic bank: The role of religiosity, image, and trust. International Journal of Economics & Management, 12(1), 137–151.

Suhartanto, D., Gan, C., Sarah, I. S., & Setiawan, S. (2019). Loyalty towards Islamic banking: Service quality, emotional or religious driven? Journal of Islamic Marketing, 11(1), 66–80. https://doi.org/10.1108/JIMA-01-2018-0007

Sutrisno, & Widarjono, A. (2018). Maqasid sharria index, banking risk and performance cases in Indonesian Islamic banks. Asian Economic and Financial Review, 8(9), 1175–1184.

Tegambwage, A. G., & Kasoga, P. S. (2023). Determinants of customer loyalty in Islamic banking: The role of religiosity. Journal of Islamic Marketing, ahead of printing. https://doi.org/10.1108/JIMA-12-2021-0396

Usman, H., Widowati, N., & Haque, M. G. (2022). The exploration role of sharia compliance in technology acceptance model for e-banking (Case: Islamic bank in Indonesia). Journal of Islamic Marketing, 13(5), 1089–1110. https://doi.org/10.1108/JIMA-08-2020-0230

Usmani, M. M. T. (2021). An introduction to Islamic finance: Brill.

Waluyo, B., & Rozza, S. (2020). A model for minimizing problems in salam financing at Islamic banks in Indonesia. International Review of Management and Marketing, 10(2), 1–7. https://doi.org/10.32479/irmm.9149

Zaki, A., Sholihin, M., & Barokah, Z. (2014). The association of Islamic bank ethical identity and financial performance: Evidence from Asia. Asian Journal of Business Ethics, 2(3), 97–110. https://doi.org/10.1007/s13520-014-0034-7