Naila Sadiq*, Ummul Baneen, and Syeda Fizza Abbas

Department of Accounting and Finance, Kinnaird College for Women, Lahore, Pakistan

*Corresponding Author: [email protected]

This study aims to analyze how the six variables, such as perceived legal risk, perceived performance risk, perceived cyber risk, perceived financial risk, perceived economic benefit, ease of use, and monetary benefit affects the adoption of financial technology, with the moderating effect of gender and education. Additionally, it explores the impact of fintech adoption on economic, environmental, and social sustainability of Pakistan. For this purpose, a quantitative researchapproach has been employed by using a well-designed questionnaire. Moreover, the sample size of 312 was considered and the responses were collected through Google forms. The data collected was then analyzed using SPSS.The study’s findings revealed that the perception of the advantages of using fintech has a positive impact on its adoption. The perception of risk has a negative impact, however, this impact is much lesser than the benefits. Risk perception negatively impacts sustainability while benefits perception impacts sustainability positively.Thus, this study can provide policymakers in emerging economies with valuable insights into the perceived risks and benefits of Fintech adoption for sustainable development. This study gives insight to the practitioners and researchers on how perceived risk and benefit can impact Fintech adoption and how its adoption, in turn, impacts sustainability. The research can contribute to informed policy decisions, support the development of robust regulatory frameworks, advance knowledge, and promote inclusive growth in emerging economies.

Keywords: financial technology, fintech adoption, risk benefit, sustainability, technology adoption

Financial services, manufacturing, and other industries have all been severely disrupted by Industry 4.0 technologies. Industry 4.0 is the fourth generation of industrial insurgence. It heralds an innovative integration of robotics and information interchange in production environments, which is known as a “digital factory”(Bartodziej & Bartodziej, 2017). Thesetechnologies aim to increase manufacturing efficiencies, which is a crucial competitive edge in today's globalized marketplace. Industry 4.0technologies can serve as agents of change for environmental, economic, and socialsustainability as well asfor sustainable development because they combine productivity-driven characteristics with digital structure (Khan et al., 2022; Meiling et al., 2021).

Fintech used to describe any novel concepts that propose technological solutions to various business problems in order to enhance financial service procedures (Leong & Sung, 2018). It includes a broad range of financial operations, including crypto-currency, mobile banking, and Internet payments. The use of fintech has many advantages, among which convenience is at the top. The services of fintech are available online on mobile phones and other electronic devices, in which the users do not need to put in effort unlike traditional banking, where the users have to go to banks to perform financial and monetary activities. This has a positive impact on financial inclusion, along with the increased financial services given to individual users and businesses as well, which were deprived of convenient financial services (Goswami et al., 2022; Kumari & Devi, 2022).

The increasing use of Fintech supports the Disruptive Innovation Theory (DIT). According to this theory, emerging technology may undermine traditional business paradigms and cause disruption in traditional financial services (Anshari et al., 2020). It's not unexpected that professionals and scholars both have grown quite interested in disruptive innovations and want to know more about how they affect businesses and sectors (Christensen et al., 2018). According to a study by Suprun et al. (2020), traditional banks and new fintech businesses compete in their domains like transactions and transfers of money. Nowadays, a large number of people are using Fintech than traditional finance due to factors like ease of use, convenience, and services with lower costs (Schueffel, 2020).

The innovation of the banking sector with the advent of fintech is supported by the Technology Acceptance Theory (TAM). Perceived utility and simplicity of use are the two key factorsthat influence a person's desire to utilize new technology, in accordance with the technology adoption paradigm(Singh et al., 2020). Hence, people choose innovative technology (Fintech) because it offers ease and efficiency with less effort. A study by Singh et al. (2020) has revealed that the user-friendliness of fintech services is a driver of the initial adoption of fintech, and the seamless transaction is a driver of the later adoption of fintech by users. Furthermore, studies have shown that the perceived benefit and user-friendliness of fintech positively and firmly impact the adoption of financial technology more than the impact of perceived risk on avoiding fintech (Ali et al., 2021; Razzaque et al., 2020).

Despite all the advantages of Fintech, users are often reluctant to utilize fintech because of the risks associated with using this technology for monetary purposes. While some researchers have proclaimed that the perception of risk does not significantly impact Fintech adoption, and individuals' perception of benefits has a more positive influence onthe adoption of fintech than the potential negative impact of perceived risk on its adoption (Al-Nawayseh, 2020). This paper aims to explore the impact of perceived risks and perceived benefits on the adoption of Fintech and its impact on social, economic, and environmental sustainability.

Despite the existing literature on Fintech Adoption (FA), further exploration is still required to unleash the impact of perceived risks and perceived benefits on FA as well as the impact of FA on sustainability, especially for developing countries like Pakistan. The study also aims to identify the types of potential risks that users of Fintech face. This insight can help companies and monetary institutions to identify potential obstacles in fintech adoption and address user concerns; thereby, promoting the adoption of fintech in fostering sustainable financial practices.

The adoption of fintech has a positive association with sustainability because it can reduce transaction costs, increase excess to financial services, and enhance transparency (Chen, 2018; Zhang et al., 2021). Fintech adoption, according to Zhang et al. (2021), can aid in lowering information asymmetry; however, it also involves legal risks (Nakamura et al., 2019). Several studies have demonstrated that legal risk has a detrimental effect on FA (Chen et al., 2018; He et al., 2020).

Prior studies have shown a favorable and strong correlation between financial stability and fintech, indicating that the use of fintech contributes to financial stability; subsequently, impacting economic sustainability (Daud et al., 2022). Shang and Niu (2023), closely examined the slighter aspects of the digital transformation of the banks. It became clear that increasing the level of digitization in bank management fosters the growth of green credit. Implementing Fintech and following the strategies of G20 and better than cash alliance, financial inequalities can be reduced and more inclusivity can also be created for economies. This approach is crucial in achieving the Sustainable Development Goals (SDGs) by encouraging digital payment methods and involving a larger population in financial initiatives. Collaboration among key stakeholders is pivotal in bringing meaningful change and fulfilling these goals (Danladi et al., 2023).

The intention to adopt Finetch is the bigger factor that influence fintech services offered by banks. The association indicated above is more significant than perceived behavioral control, possibly because certain Fintech businesses provide the user-friendly apps that prioritizes the user experience in their business strategies. However, organizations are motivated to use these services more by the reputation and image of their clients, service providers, and rivals, rather than the resources accessible to employ Fintech services (Irimia-Diéguez et al., 2023).

A bibliometric analysis of Fintech in the banking Industry by Asif et al. (2023) has been conducted to provide in depth insights into the current and future research directions of Fintech. In this analysis, the authors reviewed 1,135 Scopus Indexed research papers to drawinteresting statistics, indicating that China is the leading country in conducting research on Fintech in the banking industry, and the majority of the research has been conducted in the year 2021.

As the use of technology is increasing day by day, it is considered easy and convenient for the users to use FA. Only a small percentage of people have had a bad experience with the use of technology which made them reluctant users of technology(Sjöberg & Fromm, 2001).

The use of fintech or any technology is associated with electricity and internet connections. However, emerging or developing economies have uncertainty and risk associated with FA due to unreliable electricity and Internet sources(Lukonga, 2018). When client information isutilizedfor discrimination against consumer groups, the societal dangers of FinTech intersect with or occur simultaneously withtechnological issues (Horn et al., 2020).

The Perceived Risk (PR) of FA has many indicators, such as regulatory risk, financial risk, and cyber risk associated with FA(Abdul-Rahim et al., 2022; Ryu & Ko, 2020). Another factor impacting FA in relation to the PR is the performance risk of fintech. FA is impacted by the performance risks as well. People perceive that the performance of mobile banking and the working of online platforms would not be efficient, and it may lead to potential monetary loss(Xie et al., 2021). In the fintech business, performance risk alludes to the potential for disappointment or functional issues (Nakamura et al., 2019). Numerous studies have also revealed that performance risk has a detrimental effect on the adoption of fintech (Chen et al., 2018; He et al., 2020). A study by Ryu (2018), studied the effect of perception of risk in the adoption of fintech and found out that the users of fintech are skeptical regarding the use of financial technology. Several studies have demonstrated that legal risk has a detrimental effect on the adoption of fintech (Chen et al., 2018; He et al., 2020).

Nakamura et al. (2019) discovered that both legal risk and performance risk had a detrimental effect on the adoption of fintech, with legal risk having a more detrimental effect when performance risk was potentially higher.According to Ali et al. (2021), the perception of customers that financial technology would be risky or disadvantageous for us would have an adverse consequence on the FA. PR does not straightforwardly influence the use of fintech however trust can have a significant influence (Al-Nawayseh, 2020). Users of fintech are apprehensive about payment security because of the poor quality of the systemand are hesitant to use fintech further. The most important aspect of information quality for fostering trust in the application of fintech is its credibility (Ryu & Ko, 2020). According to Zhou (2012), the reliability of service providers is reflected in the quality of their information.Similar research conducted on the adoption behavior of fintech by the farmers showed that risk perception did influence the use of fintech by the farmers (Mathur, 2022).

The individual’s perception of the benefits of FA has a significant impact on the overall FA of people. This has made the banking system more efficient and easier rather than replacing it(Murinde et al., 2022). The individual’s positive perception of the benefits of fintech has a favorable impact e on FA. Fintech instills the trust of people in financial services, attracting more people to use fintech for a longer time(Ali et al., 2021).

Established technology adoption theories influence how the perceived benefits of fintech are regarded, including the economic, usability, and monetary benefits (Abdul-Rahim et al., 2022). According to Granić and Maranguni (2019), the TAM framework explains why fintech is being adapted based on convenience and usability. The study's findings emphasized the influence of perceived utility and usability on the use of fintech. TAM helps with user retention and recruitment initiatives. Studies show that FA is very beneficial as it reduces time, effort, and uncertainty. Feyen et al. (2021) has studied the adoption of fintech in different countries emphasizing factors, such as high price of conventional banking, a favourable regulatory climate, and additional variables, particularly macroeconomics, linked to fintech uptake in other nations. Adopting fintech can improve the financial system's accessibility and effectiveness, leading to positive economic effects(Nangin et al., 2020).Only a few studies have examined different aspects of Fintech adoption in the marineand seaport industries across Africa and elsewhere(Antwi-Boampong et al., 2022). A study by Mathur (2022) revealed that the ease of use and other benefits of Fintech result in farmers using fintech in their transactions.

Regulatory challenges include maximizing FinTech's benefits, while balancing its inherent dangers with banking safety. In the coming decade, AI applications will significantly benefit customers and businesses, offering banks a competitive edge through readily available AI systems and custom services built on extensive data (Murinde et al., 2022). According to studies (Ali et al., 2021; Ryu, 2018), the advantages of FinTech, such as lower prices, efficiency, trustworthiness, and ease of use, influence its acceptance.

The main goal of Sustainable Development Goals is the reduction of poverty, maintenance of peace, and protection of the environment. There is a need for knowledge of the SDGs as many people are unaware of them(Zamora-Polo et al., 2019). All stakeholders including the government, private businesses, andnon-governmental organizations, etc must be involvedto meet the Sustainable Development Goals(Velenturf & Purnell, 2021).

The SDGs are of three kinds economic, social and environmental. Adopting fintech supports all three kinds of goals environmental, social and economic. Fintech has been viewed as a catalyst for long-term economic growth(Ryu & Ko, 2020). Studies have found that technology use may also result in more income and lower costs(Khan et al., 2022). It also contributes to the environment and to accomplish social, financial, and ecological supportability, it is essential to use FinTech(Ziemba, 2019). Even though numerous studies haveemphasizedthe significance of technology in Fintech, a research study on how IT affects Fintech usage has not yet been conducted(Khan et al., 2022). The SDGscould be considered the paramount objective. An adequate global banking system is required today to fulfill its responsibility to encourage themobilizationof private capital to foster sustainable development and consistent economic growth(Hoang et al., 2022).

It is debatable if fintech will have an impact on sustainable economic growth, although it may have positive effects on financial services and technical development (Haddad & Hornuf, 2019). Although FinTech encourages social equity and inclusion, further research is necessary to fully understand its impact (Zhang et al., 2021). It promotes economic growth, empowers neglected groups, and advances the SDGs(Al-Hammadi & Nobanee, 2019; Al-Nawayseh, 2020). Sustainable financing and green investments are made possible by cutting-edge analytics, blockchain, and AI (Lau et al., 2020). However, problems with energy use and power concentration could arise (Chen, 2018; Lau et al., 2020).

Fintech adoption should be improved through both public and private sector collaboration in order to increase financial inclusion, which would also help the SDGs to be achieved. The achievement of the SDG aim of eradicating extreme poverty is in part attributable to the increased availability of financial services, including in rural areas (Danladi, 2023). The categories of digital innovation are categorized in an article from the standpoint of value creation, as well as the realization paths of digital finance innovation are distilled in green manufacturing companies from the standpoint of smart servitization and cooperative capacities (Chang et al., 2022).

Researchers have shown that distinctions in sexual orientation exist in fintech reception, with women being somewhat less inclined to embrace fintech administrations as compared to men(Jin et al., 2019). Research has revealed that men generally have a higher usage rate of fintech applications compared to women(Chen et al., 2023). Nonetheless, it means a lot to take note of that distinction in sexual orientation in fintech adoption might shift across various social settings and explicit fintech administrations advertised(Nurlaily et al., 2021). Study has shown that age gender and education do significantly impact the use of Fintech among the farmers (Mathur, 2022). A study has revealed that gender does not directly impact the adoption of fintech (Sakhare et al., 2023). A study by Tripathi and Reejay (2023), revealed that the impact of gender on fintech adoption also depends on the financial condition of the country. They found that in developed and financially stable countries, women use fintech more than women in underdeveloped or struggling countries.

A study revealed that the use of Fintech is more common among the literate population as compared to illiterate people or the ones with lesser formal education (Aggarwal et al., 2023). On the other hand, a study by Ahmad and Yahaya (2023), showed contradictory results concluding that people can use fintech equally in Malaysia regardless of their educational background because facilities like mobile banking, are easy to use and user-friendly, which allow their convenient usage.

The following hypotheses have been proposed in this study that are as follows:

H1: Perceived risk has a negative impact on the Adoption of fintech.

H2: Perceived risk has a negative impact on sustainability.

H3: Fintech adoption has a significant impact on sustainability.

H4: The adoption of fintech completely or partially mediates the relationship between perceived risk and sustainability.

H5a: Gender moderates the relationship between PR and sustainability.

H5b: Education has a moderating impact on the relationship between PR and FA.

H6: Perceived benefits have a positive impact on the adoption of fintech.

H7: Perceived benefits have a positive impact on sustainability.

H8: Adoption of fintech has a positive impact on sustainability.

H9: FA completely or partially mediates the relationship between PB and sustainability.

H10a: Gender moderates the relationship between PB and FA.

H10b: Education moderates the relationship between PB and FA

On one hand, Fintech adoption plays a crucial role in the convenient and efficient flow of money; however, it also includes risk perception towards the use of technology since there’s always room for error. A study showed that a lot of people avoid Fintech due to perceived risk (Sjoberg & Fromm, 2001). So, the aim of the study is to identify if perceived risk impacts FA or sustainability or not.

Similarly, is it crucial to study if there is any impact of gender and education on the adoption behavior of Fintech. According to a study, age and gender do have an impact on FA (Aggarwal et al., 2023), on contrary to this research a researcher revealed that gender and education have no significant impact on FA (Ahmad & Yahaya, 2023; Sakhare et al., 2023). How Perceived benefit can impact FA and in turn, sustainable growth will be studied in hypotheses H7, H8, and H9.

The following sections demonstrate how data has been collected, measured, and analyzed in this study.

Data Measurement

The data for the study has been collected using a survey questionnaire that included questions regarding each variable. The factors are PR, PB, FA, and sustainability. The perceived risk has four dimensions that are cyber risk, performance risk, legal risk, and financial risk, while the perceived benefits have three dimensions that are economic benefits, ease of use, and monetary benefit. Similarly, sustainability has three dimensions that are economic, environmental, and social sustainability (Abdul-Rahim et al., 2022).

The targeted population for this study comprises users of mobile banking and fintech services. The survey was distributed among individuals who actively or frequently use digital finance services. The participants included in were both men and women. The sampling method employed for the study was snowballing and the distribution of online surveys to several people to collect multiple responses. The survey was distributed among 350 people out of which 312 responded (with a response rate of 89%) which was then used as a sample for the study.

The tool used for the analysis is SPSS. The descriptive are run through SPSS and the hypotheses are analyzed using the Hayes model on SPSS.

Questionnaire

Table 1

Questionnaire Items

|

Constraints |

Code |

Questionnaire |

Reference |

|

Fintech adoption |

FA1 |

I always use the internet/online banking |

Venkatesh et al. (2003) |

|

FA2 |

I always use a mobile banking app (using a smartphone, jazz cash, easy paisa) |

||

|

FA3 |

I always use contactless debit/credit/prepaid cards (NBP, HBL) |

||

|

Performance risk |

PR1 |

When financial problems happen or financial data leakage occurs, financial technology companies are unwilling to address the problems. |

Ryu (2018) |

|

PR2 |

When financial problems or financial data leakage occur, financial technology companies' organizational reactions are too delayed. |

||

|

PR3 |

It is concerning to me how Fintech businesses react to monetary losses or financial data leaks. |

||

|

Cyber risk |

CR1 |

I believe that FinTech poses a considerably greater cyber-security risk than using conventional banking services. |

Abdul-Rahim et al. (2022) |

|

CR2 |

Using FinTech makes me concerned that someone might steal my account data and information. |

||

|

CR3 |

I worry about the misuse of my financial records when using FinTech. |

||

|

Financial risk |

FR 1 |

When using fintech I am prone to payment frauds and financial frauds. |

Abdul-Rahim et al. (2022) |

|

FR2 |

I could lose money with FinTech because of exchange rate changes. |

||

|

FR3 |

I might lose money via FinTech as a result of crypto-currency price swings. |

||

|

Legal risk |

LR1 |

Using Fintech is uncertain due to many regulations. |

Ryu (2018) |

|

LR2 |

It is not easy to use a Fintech due to the government regulation |

||

|

LR3 |

There is a legal uncertainty for Fintech users. |

||

|

Monetary savings |

MS1 |

Using FinTech allows me to save money. |

Abdul-Rahim et al. (2022) |

|

MS2 |

Using FinTech allows me to expect financial gains (e.g., cashback, higher interest, vouchers, rewards). |

||

|

MS3 |

Using FinTech allows me to use various financial services at a low cost. |

||

|

Economic benefit |

EB1 |

Using Fintech is cheaper than using traditional financial services. |

Ryu (2018) |

|

EB2 |

I can save money when I use Fintech. |

||

|

EB3 |

I can use various financial services at a low cost when I use Fintech. |

||

|

Ease of use |

EU1 |

It is easy for me to become skillful at looking for information with mobile Internet. |

(Okazaki, 2013) |

|

EU2 |

It is easy to browse a search engine with mobile Internet. |

||

|

EU3 |

Learning how to find information with a mobile device is easy for me. |

||

|

Sustainability |

S1 |

FinTech adoption could reduce energy consumption (e.g., fuel) and increase the protection of the environment through FinTech. |

Abdul-Rahim et al. (2022) |

|

S2 |

FinTech adoption could reduce social exclusion due to age, education, place of residence, or disability, which causes difficult participation in banking and finance and limited or difficult access to financial services. |

||

|

S3 |

FinTech adoption could reduce costs (for instance, through lower purchase prices of goods/services on the internet, eliminating travel expenses, and lower costs of communication over the internet than telephone or personal communication). |

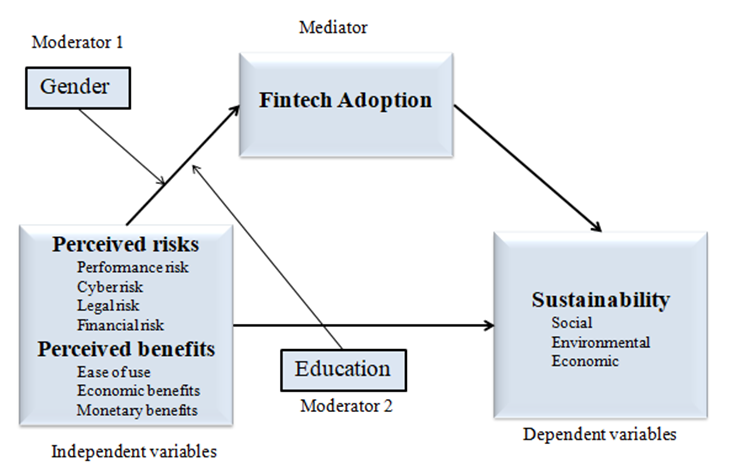

Figure 1

Conceptual Model

Table 2

Demographics Operationalization

|

Variables |

Characteristics |

Sources |

|

Gender |

Male Female |

|

|

Education |

No Formal Education High school Diploma Graduate Post Graduate Ph.D |

(Jain & Raman, 2023) |

The data has been collected to study the impact of perceived risk and perceived benefit on FA and the impact of FA on economic, environmental, and social sustainability. After data collection, the data was analyzed using IBM SPSS 26. The demographic, descriptive, and Hayes model has been performed in this section.

Table 3

Statistics

|

Gender |

Education |

||

|

N |

Valid |

312 |

312 |

|

Missing |

0 |

0 |

|

Table 4

Demographics of Gender

|

Frequency |

Percent |

Valid Percent |

Cumulative Percent |

||

|

Valid |

Female |

166 |

53.2 |

53.2 |

53.2 |

|

Male |

146 |

46.8 |

46.8 |

100.0 |

|

|

Total |

312 |

100.0 |

100.0 |

|

|

The questionnaire was distributed among 350 people, and 312 individuals responded. Among the survey respondents, 166 (53.20%) were women, 124 (39.7%) were men, while 22 (7.1%) respondents did not prefer to disclose their gender. In terms of age, 166 (58.6%) respondents fell within the age bracket of 21 to 30. Regarding the education level, most of the respondents were literate while only a few percent (16%) had no formal education.

Table 5

Demographics of Education

|

|

Frequency |

Percent |

Valid Percent |

Cumulative Percent |

|

|

Valid |

Diploma |

40 |

12.8 |

12.8 |

12.8 |

|

Graduate |

104 |

33.3 |

33.3 |

46.2 |

|

|

High school |

16 |

5.1 |

5.1 |

51.3 |

|

|

no formal education |

50 |

16.0 |

16.0 |

67.3 |

|

|

PhD |

28 |

9.0 |

9.0 |

76.3 |

|

|

Post Graduate |

74 |

23.7 |

23.7 |

100.0 |

|

|

Total |

312 |

100.0 |

100.0 |

|

|

Descriptive statistics are presented in table 1 below, including standard deviations (σ), means (µ), maximum parameter values, minimum parameter values, and the number of observations taken.

Table 6

Descriptive Statistics

|

|

N |

Mean |

Std. Deviation |

Skewness |

Kurtosis |

||

|

Statistic |

Std. Error |

Statistic |

Std. Error |

||||

|

Edu |

312 |

3.71 |

1.51 |

-.54 |

.14 |

-.65 |

.28 |

|

Gender |

312 |

1.47 |

0.50 |

.13 |

.14 |

-2.00 |

.28 |

|

FA |

312 |

3.9599 |

1.064 |

-.40 |

.14 |

-.67 |

.28 |

|

S |

312 |

3.9812 |

0.96 |

-.31 |

.14 |

-.61 |

.28 |

|

Perceived risk |

312 |

3.3849 |

1.01 |

-.08 |

.14 |

-.91 |

.28 |

|

Perceived benefit |

312 |

3.8495 |

0.88 |

-.68 |

.14 |

-.17 |

.28 |

|

Valid N (listwise) |

312 |

|

|

|

|

|

|

There are a total of 312 observations for each variable. Most of the individuals surveyed predominantly use fintech services like mobile banking, cash apps, contactless debit and credit cards, etc. Most of the fintech users are indecisive about the performance risk of FA. The users of fintech have a moderate leveled concern regarding the risk related to fintech adoption. The PR has a mean value of 3.38 with a standard deviation of 1.013. The Variable PB has a mean of 3.84 with an SD of 0.8826, which means that the values can go above and below the mean values by 0.8826. Finally, the variable S has a mean value of 3.98 indicating that most of the respondents agree that FA has a positive impact on S (sustainability).

The reliability test is applied to identify if the questionnaire used to conduct the research is reliable or not. The Cronbach alpha should be greater than 0.7 less than 0.95. The Cronbach’s Alpha of the questionnaire is 0.857 which indicates that the questionnaire is reliable, and we can rely on the results derived from it..

Table 7

Reliability Statistics

|

Cronbach's Alpha |

N of Items |

|

.857 |

35 |

Correlation Matrix also shows that the items are valid. Pairwise correlations among variables used in the evaluation are represented by the correlation matrix. It is observed that the correlation values for all the variables are below than 0.8, which suggests that no high level of correlation exists among the variables.

Table 8

Correlation Matrix

|

|

S |

FA |

Perceived risk |

Perceived benefit |

Gender |

Edu |

|

|

S |

Pearson Correlation |

1 |

.404** |

-.495** |

.749** |

.020 |

.179** |

|

Sig. (2-tailed) |

|

.000 |

.000 |

.000 |

.730 |

.001 |

|

|

N |

312 |

312 |

312 |

312 |

312 |

312 |

|

|

FA |

Pearson Correlation |

.404** |

1 |

-.287** |

.563** |

.118* |

.380** |

|

Sig.(2-tailed) |

.000 |

|

.000 |

.000 |

.037 |

.000 |

|

|

N |

312 |

312 |

312 |

312 |

312 |

312 |

|

|

Perceived risk |

Pearson Correlation |

-.495** |

-.287** |

1 |

-.621** |

-.194** |

-.261** |

|

Sig. (2-tailed) |

.000 |

.000 |

|

.000 |

.001 |

.000 |

|

|

N |

312 |

312 |

312 |

312 |

312 |

312 |

|

|

Perceived benefit |

Pearson Correlation |

.749** |

.563** |

-.621** |

1 |

.031 |

.377** |

|

Sig. (2-tailed) |

.000 |

.000 |

.000 |

|

.589 |

.000 |

|

|

N |

312 |

312 |

312 |

312 |

312 |

312 |

|

|

Gender |

Pearson Correlation |

.020 |

.118* |

-.194** |

.031 |

1 |

.085 |

|

Sig. (2-tailed) |

.730 |

.037 |

.001 |

.589 |

|

.133 |

|

|

N |

312 |

312 |

312 |

312 |

312 |

312 |

|

|

Edu |

Pearson Correlation |

.179** |

.380** |

-.261** |

.377** |

.085 |

1 |

|

Sig. (2-tailed) |

.001 |

.000 |

.000 |

.000 |

.133 |

|

|

|

N |

312 |

312 |

312 |

312 |

312 |

312 |

|

|

Note. **. Correlation is significant at the 0.01 level (2-tailed). |

|||||||

|

*. Correlation is significant at the 0.05 level (2-tailed). |

|||||||

Impact of PR on Sustainability with Mediation of FA and Moderation of Education and Gender

With a 20.02% explained variance, the study revealed that public relations (PR) significantly predict the mediating variable (FA) in the connection. However, PR had a negligible direct effect on FA. Education and gender had non-significant effects on FA. In addition to that indirect effects of education and gender on the PR-FA connection were also non-significant. Sustainability (S) was considerably impacted by both PR and FA, with PR having a negative impact and FA having a favorable impact. Sustainability was linked to FA, while sustainability suffered from higher risk perception. For instance, the first line of the chart represents the situation where gender and education are both 1. A one-unit rise in PR is correlated with a -0.0857unit drop in S, indirectly through FA, for these specific levels of education &gender, according to effect estimation regarding the indirect impact of PR on the sustainability (S)through FA, that is -.0857. Hence, the PR impacts dependent variables (sustainability) with the mediation of FA.

Table 9

Direct Impact of PR, Gender and Education on FA

|

|

b |

se |

t |

p |

LLCI |

ULCI |

|

Constant |

4.2644 |

0.8005 |

5.3273 |

0.0000 |

2.6893 |

5.8395 |

|

Perceived risk (PR) |

-.3824 |

.2221 |

-1.7214 |

.0862 |

-.8194 |

.0547 |

|

Gender |

.1529 |

.3905 |

.3915 |

.6957 |

-.6156 |

.9214 |

|

Int_1 |

-0.0046 |

0.1113 |

-0.0410 |

0.9673 |

-0.2235 |

.2144 |

|

Edu |

0.0438 |

0.1337 |

0.3279 |

0.7432 |

-0.2192 |

0.3068 |

|

Int_2 |

.0515 |

.0359 |

1.4346 |

.1524 |

-.0191 |

.1221 |

Table 10

Conditional Effects of the Focal Predictor at Values of the Moderator(s)

|

Gender |

Edu |

Effect |

se |

t |

p |

LLCI |

ULCI |

|

1.0000 |

1.0800 |

.5285 |

.1196 |

4.4195 |

.0000 |

.2932 |

.7638 |

|

1.0000 |

4.0000 |

.7067 |

.0920 |

7.6807 |

.0000 |

.5257 |

.8878 |

|

1.0000 |

5.0000 |

.7678 |

.1079 |

7.1132 |

.0000 |

.5554 |

.9801 |

|

2.0000 |

1.0800 |

.4140 |

.1054 |

3.9276 |

.0001 |

.2066 |

.6214 |

|

2.0000 |

4.0000 |

.5922 |

.0816 |

7.2607 |

.0000 |

.4317 |

.7527 |

|

2.0000 |

5.0000 |

.6532 |

.1015 |

6.4342 |

.0000 |

.4535 |

.8530 |

Table 11

Impact of PR, FA, Edu and Gender on Sustainability

|

|

b |

se |

t |

p |

LLCI |

ULCI |

|

Constant |

4.2850 |

0.2713 |

15.7951 |

0.0000 |

3.7512 |

4.8188 |

|

Perceived Risk (PR) |

-0.3923 |

0.0465 |

-8.4288 |

.0000 |

-.4838 |

-0.3007 |

|

FA |

.2586 |

.0444 |

5.8287 |

.0000 |

.1713 |

.3459 |

Table 12

Indirect Effect

|

Indirect effect: Perceived Risk→ Fintech adoption → Sustainability |

|||||

|

Gender |

Edu |

Effect |

BootSE |

BootLLCI |

BootULCI |

|

1.0000 |

1.0800 |

-.0857 |

.0337 |

-.1585 |

-.0265 |

|

1.0000 |

4.0000 |

-.0468 |

.0186 |

-.0868 |

-.0127 |

|

1.0000 |

5.0000 |

-.0335 |

.0210 |

-.0759 |

.0076 |

|

2.0000 |

1.0800 |

-.0869 |

.0377 |

-.1748 |

-.0275 |

|

2.0000 |

4.0000 |

-.0480 |

.0300 |

-.1150 |

.0023 |

|

2.0000 |

5.0000 |

-.0347 |

.0330 |

-.1073 |

.0248 |

Table 13

Indices of Partial Moderated Mediation

|

|

Index |

BootSE |

BootLLCI |

BootULCI |

|

Gender |

-.0012 |

.0295 |

-.0672 |

.0495 |

|

Edu |

.0133 |

.0097 |

-.0034 |

.0337 |

Impact of PB on Sustainability with Mediation of FA and Moderation of Education and Gender

On the next path, the variable PB is taken as independent and the impact of PB is studied on the sustainability with the mediating impact of FA and moderation of education and gender. First, the impact of PB, gender, and education is studied on the variable FA (fintech adoption). In the model summary, the value of R-squared is 0.3657 which means that 36.57% of the variation in FA is explained by the independent variable. The benefit perception which is denoted by P has a significant impact on FA (adoption of fintech) because p=0.0110 (p<0.05). It can be seen that the value of the coefficient is 0.5771, which indicates that the PB positively impacts the FA.

The education and gender have no direct significant impact on FA but the main concern is to study the indirect impact of education and gender on the relationship between the variables FA and PB. The b value of PB is positive (0.5771) which indicates that PB has a positive relationship with FA. This indicates that if the PB increase appreciates by 1 point then the FA will also appreciate by 0.5771. The p-value is less than 0.05, which means that the PB does positively impact FA. Now the moderating impact of gender and education on the relationship between PB and FA is to be analyzed. The direct impact of education and gender on FA is insignificant because, for both, the p-value is less than 0.05. The main objective is to study the interaction terms of both moderators (gender and education). The b=-0.1145 for the interaction between (PB*Gender) and FA and the p-value is less than 0.05 which means that there is no significant impact of gender and PB collectively on FA. Similarly, the interaction impact of PB along with education on the mediating variable FA is not significant (p>0.05).

The model for the direct impact of variables on the dependent variable S has an R-squared value of 0.5614% which means that 56.14% of the variances in the S are explained by the independent variable while p=0.000, which means that the given model is significant in order to analyze the impact of PB and FA on S. The PB has b value of 0.8334 which indicates that PB positively impacts the dependent variable S in such a way that if the PB goes up by 1 point the S will go up by 0.8334. The p-value is 0.00 which indicates that PB significantly impacts S. FA has a b value of -0.0235 which means that if the FA goes up by 1 point the S will go down by 0.0235 which indicates a negative impact, and p=0.5704 which means that FA does not significantly impacts S.

Table 14

Impact of PB, Gender and Education on FA

|

|

b |

SE |

t |

p |

LLCI |

ULCI |

|

Constant |

0.9420 |

0.8632 |

1.0914 |

0.2760 |

-0.7565 |

2.6406 |

|

Perceived benefit (PB) |

0.577 |

0.2255 |

2.5591 |

0.0110 |

0.1333 |

1.0208 |

|

Gender |

0.606 |

0.4415 |

1.3718 |

0.1711 |

-0.2631 |

1.4745 |

|

Int_1 |

-.114 |

.1118 |

-1.0246 |

.3063 |

-.3344 |

.1054 |

|

Edu |

-.093 |

.1386 |

-.6722 |

.5020 |

-.3660 |

.1796 |

|

Int_2 |

.0610 |

.0364 |

1.6790 |

.0942 |

-.0105 |

.1326 |

Table 15

Impact of FA, PB on S

|

Impact on Sustainability |

||||||

|

|

b |

Se |

t |

p |

LLCI |

ULCI |

|

Constant |

0.8661 |

0.1717 |

5.0454 |

0.0000 |

0.5283 |

1.2038 |

|

Perceived benefit (PB) |

0.8334 |

0.0498 |

16.7498 |

0.0000 |

0.7355 |

0.9313 |

|

FA |

-0.024 |

0.0413 |

-0.5681 |

0.0074 |

-0.1047 |

0.0578 |

Table 16

Indirect effect of PB, FA and S

|

Indirect effect: Perceived benefit → Fintech adoption → Sustainability |

|||||

|

Gender |

Edu |

Effect |

BootSE |

BootLLCI |

BootULCI |

|

1.0000 |

1.0800 |

-.0124 |

.0255 |

-.0631 |

.0391 |

|

1.0000 |

4.0000 |

-.0166 |

.0344 |

-.0885 |

.0509 |

|

1.0000 |

5.0000 |

-.0180 |

.0377 |

-.0975 |

.0546 |

|

2.0000 |

1.0800 |

-.0097 |

.0200 |

-.0509 |

.0311 |

|

2.0000 |

4.0000 |

-.0139 |

.0288 |

-.0732 |

.0414 |

|

2.0000 |

5.0000 |

-.0153 |

.0320 |

-.0822 |

.0454 |

Table 17

Indices of Partial Moderated Mediation

|

Indices of partial moderated mediation |

||||

|

|

Index |

BootSE |

BootLLCI |

BootULCI |

|

Gender |

.0027 |

.0078 |

-.0114 |

.0223 |

|

Edu |

-.0014 |

.0036 |

-.0107 |

.0046 |

Table 18

Hyotheses Testing

|

Hypotheses |

V |

p-value |

Coefficient |

Significance |

Reject H0 / Accept H0 |

|

H1 |

PR→FA |

0.0862 |

-0.3824 |

Insignificant |

Accept H0 |

|

H2 |

PR→S |

0.000 |

-0.3923 |

Significant |

Reject H0 |

|

H3 |

FA→S |

0.000 |

0.2586 |

Significant |

Reject H0 |

|

H5a |

(PR*gender) → FA |

.9673 |

-.0046 |

Insignificant |

Accept H0 |

|

H5b |

(PR*education) →FA |

.1524 |

.0515 |

Insignificant |

Accept H0 |

|

H6 |

PB→FA |

0.0110 |

0.5771 |

Significant |

Reject H0 |

|

H7 |

PB→S |

0.0000 |

0.8334 |

Significant |

Reject H0 |

|

H8 |

FA→S |

0.0074 |

-0.0235 |

Significant |

Reject H0 |

|

H10a |

(Gender*PB) →FA |

0.3063 |

-0.1145 |

Insignificant |

Accept H0 |

|

H10b |

(Education*PB) →FA |

0.0942 |

0.0610 |

Insignificant |

Accept H0 |

Table 19

Results of Mediation

|

Hypotheses |

V |

Significance |

Reject H0/ Accept H0 |

|

H4 |

FA partially mediates (PB→S) |

Significant |

Reject H0 |

|

H9 |

FA partially mediates (PR→S) |

Significant |

Reject H0 |

From the analysis, it is concluded that the adoption of fintech is impacted by the risk perception of individual users. Risk perception has a negative impact on the fintech adoption which means that an increase in risk perception would put a downward impact on the adoption of fintech. Although it has a negative impact on the trust of users, it does not impact the overall adoption behavior of fintech (Abdul-Rahim et al., 2022). Furthermore, it has been analyzed that perceived risk has a negative impact on sustainability, which means that the more people are reluctant to use fintech the more negative impact it would have on sustainability (economic, environmental, and social) (Abdul-Rahim et al., 2022).

The study showed that fintech adoption has a positive impact on sustainability which is supported by Yan (2022). The study indicates that there is no impact of gender or education on the relationship between PR and FA and the relationship between PB and FA. According to the study performed by Ferdaous and Rahman (2021), the behavior of individuals can be different in different regions, and different people in different areas of the world respond differently to technology, so if gender and education influence fintech adoption in one region, it can have no influence in other regions of the world. The results of mediating the impact of fintech on the relationship between PR and sustainability showed that there is a partial indirect significance among these variables.

Moving on to the results of the impact of perceived benefit on the adoption of fintech and sustainability. The perceived benefits were found to have a significant impact on the adoption of fintech. It has been found that the impact of PB is positive on FA and S. And the variable FA has a significant positive impact on sustainability (Jain & Raman, 2023). Like other studies, this study also concludes that the adoption of fintech has a significant impact on sustainability (economic, social, and environmental). This is because fintech is a means of financial inclusion, and environmentally friendly paper-free transactions. The findings coincide with past literature that came up with the same results that FA impacts S (Museba et al., 2021).

As it has been already indicated sustainability (in this research) has been studied with three further indicators; economic sustainability, social sustainability, and environmental sustainability. If we talk about environmental sustainability, Fintech assists companies in measuring the sustainability of their portfolios and finding ESG-friendly investing possibilities. It helps by reducing pollution and promoting green innovation (Taylor, 2023). From an economic point of view, Fintech helps in reducing transaction costs and the cost of transport since all the transactions are a click away. As far as social sustainability is concerned Fintech promotes social inclusion. People living in remote areas can also practice online banking as well as people who are disabled and cannot travel can also use Fintech (Cambaza, 2023).

Age or gender does not seem to have a direct or moderating impact on the relationship between PB and FA. This means that the trust in fintech and adoption of fintech does not depend on the gender in the region where the study has been taken. Studies have revealed that the demographic or other results may vary because people in different regions respond to technology differently (Ferdaous & Rahman, 2021).

The results indicate that the FA partially mediates the relationship between the variables PB and S. This indicates that the mediating impact of FA is partial, and there can be other reasons as well that influence the sustainability (Guang-Wen & Siddik, 2023). Partial mediation exists when there is a significant relationship between the dependent and mediating variables, but also a direct relation between the dependent and independent variable. In the present case, there is a direct significant relationship between perceived risk/benefit and sustainability as well as a significant relationship between FA and sustainability (Maxwell et al., 2011).

The current study analyzed the impact of the adoption of fintech on the sustainable development of Pakistan. The study investigated the risk and benefit perception of users of fintech and how it impacts the actual adoption of technology for several financial transactions. The perceived risk was studied using four indicators (legal risk, cyber risk, financial risk, and performance risk). The results indicated that people were more influenced by the perception of financial, cyber, and performance risks than by the legal risk. Overall, the results implied that people are reluctant to use fintech, but it does not significantly impact the adoption behavior of fintech, which means that the negative impact of risk perception is less than the positive impact that the benefit perception has on the adoption of fintech. Similarly, as the individuals benefit perception towards fintech increases people tend to have more trust in technologies like financial technology which act as a driver of FA. The FA, in turn, impact sustainability. If people use technology to perform day-to-day transactions, there would be less reliance on paper and other materials that negatively impact the environment. Similarly, with the use of technology tasks can be performed in mobile areas and this way financial inclusion is promoted. On the contrary, conventional banking requires physical presence, posing challenges for old and special people and for bank users in rural areas where banking facilities are not available. Higher benefit perception fosters more trust among individual users, resulting in increased adoption of fintech.

The research conducted on fintech can assist regulators and decision makers in formulating new policies that would help in further sustainability and policies promoting technology for SDGs. The study also specifies the types of potential risks that users of fintech usually fear or face. This will help companies and monetary institutes identify potential problems in fintech adoption and overcome the problem of fear among the users that would put upward pressure on the adoption of fintech leading to further sustainable financial practices. This research aims to create awareness, among the readers, about the use of fintech and how its adoption can bring about ease and sustainability in the environment.

The study focuses on examining the impact of PB and PR on S with the mediating impact of FA and moderating impacts of education and gender.

Abdul-Rahim, R., Bohari, S. A., Aman, A., & Awang, Z. (2022). Benefit–risk perceptions of fintech adoption for sustainability from bank consumers’ perspective: The moderating role of fear of COVID-19. Sustainability, 14(14), Article e8357. https://doi.org/10.3390/su14148357

Aggarwal, M., Nayak, K. M., & Bhatt, V. (2023). Examining the factors influencing fintech adoption behaviour of gen Y in India. Cogent Economics & Finance,11(1), Article e2197699. https://doi.org/10.1080/23322039.2023.2197699

Ahmad, K., & Yahaya, M. H. (2023). Islamic social financing and efficient zakat distribution: Impact of fintech adoption among the asnaf in Malaysia.Journal of Islamic Marketing,14(9), 2253–2284. https://doi.org/10.1108/JIMA-04-2021-0102

Ali, M., Raza, S. A., Puah, C., & Amin, H. (2021). How perceived risk, benefit and trust determine user Fintech adoption: A new dimension for Islamic finance. Foresight, 23(4), 403–420. https://doi.org/10.1108/FS-09-2020-0095

Anshari, M., Almunawar, M. N., & Masri, M. (2020). Financial technology and disruptive innovation in business: Concept and application.International Journal of Asian Business and Information Management,11(4), 29–43. https://doi.org/10.4018/IJABIM.2020100103

Antwi-Boampong, A., Boison, D. K., Agbedoawu, J., Doumbia, M. O., & Blay, A. (2022). Factors affecting port users’ behavioral intentions to adopt financial technology (fintech) in ports in Sub-Saharan Africa: A case of ports in Ghana. FinTech, 1(4), 362–375. https://doi.org/10.3390/fintech1040027

Asif, M., Sarwar, F., & Lodhi, R. N. (2023). Future and current research directions of fintech: A bibliometric analysis.Audit and Accounting Review,3(1) 19–51. https://doi.org/10.32350/aar.31.02

Azeez, A. N., Akhtar, S. M., & Banu, N. M. (2021). Role of education on financial literacy of Rural India.Asian Journal of Research in Banking and Finance,11(5), 1–11. https://doi.org/10.5958/2249-7323.2021.00007.9

Bartodziej, C. J., & Bartodziej, C. J. (2017).The concept industry 4.0(pp. 27–50). Springer Fachmedien Wiesbaden.

Cambaza, E. (2023). The role of fintech in sustainable healthcare development in Sub-Saharan Africa: A narrative review. FinTech,2(3), 444–460. https://doi.org/10.3390/fintech2030025

Chang, L., Zhang, Q., & Liu, H. (2022). Digital finance innovation in green manufacturing: A bibliometric approach.Environmental Science and Pollution Research, 30, 61340–61368. https://doi.org/10.1007/s11356-021-18016-x

Chen, X., Chen, W., & Lu, K. (2023). Does an imbalance in the population gender ratio affect FinTech innovation?Technological Forecasting and Social Change,188, Article e122164. https://doi.org/10.1016/j.techfore.2022.122164

Chen, Y. (2018). Fintech and sustainable development. Journal of Sustainable Finance & Investment, 8(3), 218–232.

Christensen, C. M., McDonald, R., Altman, E. J., & Palmer, J. E. (2018). Disruptive innovation: An intellectual history and directions for future research.Journal of Management Studies,55(7), 1043–1078. https://doi.org/10.1111/joms.12349

Danladi, S., Prasad, M. S. V., Modibbo, U. M., Ahmadi, S. A., & Ghasemi, P. (2023). Attaining sustainable development goals through financial inclusion: Exploring collaborative approaches to fintech adoption in developing economies.Sustainability,15(17), Article e13039. https://doi.org/10.3390/su151713039

Daud, S. N. M., Khalid, A., & Azman-Saini, W. N. W. (2022). FinTech and financial stability: Threat or opportunity? Finance Research Letters, 47, Article e102667. https://doi.org/10.1016/j.frl.2021.102667

Do, N., Tham, J., Azam, S., & Khatibia, A. (2020). Analysis of customer behavioral intentions towards mobile payment: Cambodian consumer’s perspective.Accounting,6(7), 1391–1402. https://doi.org/10.5267/j.ac.2020.8.010

Ferdaous, D. J., & Rahman, M. N. (2021). Banking goes digital: Unearthing the adoption of fintech by Bangladeshi households.Journal of Innovation in Business Studies,1, 7–42.

Feyen, E., Frost, J., Gambacorta, L., Natarajan, H., & Saal, M. (2021). Fintech and the digital transformation of financial services: implications for market structure and public policy (Bank of International Settlements Working Paper No. 117). https://www.bis.org/publ/bppdf/bispap117.pdf

Goswami, S., Sharma, R. B., & Chouhan, V. (2022). Impact of financial technology (Fintech) on financial inclusion (FI) in Rural India. Universal Journal of Accounting and Finance, 10(2), 483–97. https://doi.org/10.13189/ujaf.2022.100213

Granić, A., & Marangunić, N. (2019). Technology acceptance model in educational context: A systematic literature review. British Journal of Educational Technology, 50(5), 2572–2593. https://doi.org/10.1111/bjet.12864

Guang-Wen, Z., & Siddik, A. B. (2023). The effect of fintech adoption on green finance and environmental performance of banking institutions during the COVID-19 pandemic: The role of green innovation.Environmental Science and Pollution Research,30(10), 25959–25971. https://doi.org/10.1007/s11356-022-23956-z

Haddad, C. & L. Hornuf (2019). The emergence of the global fintech market: Economic and technological determinants. Small Business Economics, 53(1), 81–105. https://doi.org/10.1007/s11187-018-9991-x

Al-Hammadi, T. & Nobanee, H. (2019). FinTech and sustainability: A mini-review. SSRN. http://dx.doi.org/10.2139/ssrn.3500873

He, X., Li, Y., & Li, H. (2020). Consumer adoption of fintech services in China: Perceived risks and their mitigation strategies. Journal of Business Research, 108, 290–299.

Hoang, T. G., Nguyenet, G., & Le, D. (2022). Developments in financial technologies for achieving the sustainable development goals (SDGs): FinTech and SDGs. In U. Akkucuk (Ed.), Disruptive technologies and eco-innovation for sustainable development (pp. 1–19). IGI Global. https://doi.org/10.4018/978-1-7998-8900-7.ch001

Horn, M., Oehler, A., & Wendt, S. (2020). Fintech for consumers and retail investors: Opportunities and risks of digital payment and investment services. In T. Walker, D. Gramlich, M. Bitar & P. Fardnia (Eds.), Ecological, Societal, and Technological Risks and the Financial Sector (pp. 309–327). Springer International Publishing. https://doi.org/10.1007/978-3-030-38858-4_14

Irimia-Diéguez, A., Velicia-Martín, F., & Aguayo-Camacho, M. (2023). Predicting fintech innovation adoption: The mediator role of social norms and attitudes.Financial Innovation,9(1), 1–23. e36. https://doi.org/10.1186/s40854-022-00434-6

Jain, N., & Raman, T. V. (2023). The interplay of perceived risk, perceive benefit and generation cohort in digital finance adoption.EuroMed Journal of Business,18(3), 359–379. https://doi.org/10.1108/EMJB-09-2021-0132

Jin, C. C., Seong, L. C., & Khin, A. A. (2019). Factors affecting the consumer acceptance towards fintech products and services in Malaysia.International Journal of Asian Social Science,9(1), 59–65. https://doi.org/10.18488/journal.1.2019.91.59.65

Khan, H. U. R., Zaman, B., Zaman, K., Nassani, A. A., Haffar, M., & Muneer, G. (2022). The impact of carbon pricing, climate financing, and financial literacy on COVID-19 cases: Go-for-green healthcare policies. Environmental Science and Pollution Research, 29(24), 35884–35896. https://doi.org/10.1007/s11356-022-18689-y

Kumari, A., & Devi, N. C. (2022). The impact of fintech and blockchain technologies on banking and financial services.Technology Innovation Management Review,12(1/2). Article e22010204. http://doi.org/10.22215/timreview/1481

Lau, H. C., Li, Y., & Wong, G. K. (2020). The impact of fintech on sustainable finance. Journal of Cleaner Production, 260, Article e121102.

Leong, K., & Sung, A. (2018). FinTech (Financial Technology): What is it and how to use technologies to create business value in fintech way?International Journal of Innovation, Management and Technology,9(2), 74–78. http://doi.org/10.18178/ijimt.2018.9.2.791

Lukonga, M. I. (2018). Fintech, inclusive growth and cyber risks: Focus on the MENAP and CCA regions. International Monetary Fund.

Mathur, H. P. (2022). Conceptual development of factors driving fintech adoption by farmers.Purushartha: A Journal of Management, Ethics and Spirituality,15(1), 39–50. https://doi.org/10.21844/16202115103

Maxwell, S. E., Cole, D. A., & Mitchell, M. A. (2011). Bias in cross-sectional analyses of longitudinal mediation: Partial and complete mediation under an autoregressive model. Multivariate Behavioral Research, 46(5), 816–841. https://doi.org/10.1080/00273171.2011.606716

Meiling, L., Yahya, F., Waqas, M., Shaohua, Z., Ali, S. A., & Hania, A. (2021). Boosting sustainability in healthcare sector through fintech: Analyzing the moderating role of financial and ICT development. Inquiry: The Journal of Health Care Organization, Provision, and Financing. 58, 1–11. https://doi.org/10.1177/00469580211028174

Murinde, V., Rizopoulos, E., & Zachariadis, M. (2022). The impact of the FinTech revolution on the future of banking: Opportunities and risks. International Review of Financial Analysis, 81, Article e102103. https://doi.org/10.1016/j.irfa.2022.102103

Museba, T. J., Ranganai, E., & Gianfrate, G. (2021). Customer perception of adoption and use of digital financial services and mobile money services in Uganda.Journal of Enterprising Communities: People and Places in the Global Economy,15(2), 177–203. https://doi.org/10.1108/JEC-07-2020-0127

Nakamura, M., Matsuo, M., & Kajiwara, K. (2019). Fintech adoption: The impact of legal and performance risks. Journal of Business Research, 98, 365–378.

Nangin, M. A., Barus, I. R. G., & Wahyoedi, S. (2020). The effects of perceived ease of use, security, and promotion on trust and its implications on fintech adoption. Journal of Consumer Sciences, 5(2), 124–138. https://doi.org/10.29244/jcs.5.2.124-138

Al-Nawayseh, M. K. (2020). Fintech in COVID-19 and beyond: What factors are affecting customers’ choice of fintech applications? Journal of Open Innovation: Technology, Market, and Complexity, 6(4), Article e153. https://doi.org/10.3390/joitmc6040153

Nurlaily, F., Aini, E. K., & Asmoro, P. S. (2021). Understanding the FinTech continuance intention of Indonesian users: The moderating effect of gender.Business: Theory and Practice,22(2), 290–298.

Okazaki, S., & Mendez, F. (2013). Exploring convenience in mobile commerce: Moderating effects of gender. Computers in Human Behavior, 29(3), 1234–1242. https://doi.org/10.1016/j.chb.2012.10.019

Razzaque, A., Cummings, R. T., Karolak, M., & Hamdan, A. (2020). The propensity to use FinTech: Input from bankers in the Kingdom of Bahrain.Journal of Information & Knowledge Management,19(1), Article e2040025. https://doi.org/10.1142/S0219649220400250

Ryu, H. S., & Ko, K. S. (2020). Sustainable development of Fintech: Focused on uncertainty and perceived quality issues.Sustainability,12(18), Article e7669. https://doi.org/10.3390/su12187669

Ryu, H.-S. (2018). What makes users willing or hesitant to use Fintech? The moderating effect of user type. Industrial Management & Data Systems, 118(3), 541–569. https://doi.org/10.1108/IMDS-07-2017-0325

Sakhare, C. A., Somani, N. N., Patel, B. L., Khorgade, S. N., & Parchake, S. (2023). What drives FinTech adoption? A study on perception, adoption, and constraints of FinTech services.European Economic Letters,13(3), 1216–1230.

Schueffel, P. (2020). The fintech book: The financial technology handbook for investors, entrepreneurs, and visionaries. John Wiley & Sons.

Shang, X., & Niu, H. (2023). Does the digital transformation of banks affect green credit?Finance Research Letters,58(B), Article e104394. https://doi.org/10.1016/j.frl.2023.104394

Singh, S., Sahni, M. M., & Kovid, R. K. (2020). What drives FinTech adoption? A multi-method evaluation using an adapted technology acceptance model.Management Decision,58(8), 1675–1697. https://doi.org/10.1108/MD-09-2019-1318

Sjöberg, L. and J. Fromm (2001). Information technology risks as seen by the public. Risk Analysis, 21(3), 427–442. https://doi.org/10.1111/0272-4332.213123

Suprun, A., Petrishina, T., & Vasylchuk, I. (2020, May 20–22). Competition and cooperation between fintech companies and traditional financial institutions (Conference Session). The International Conference on Sustainable Futures: Environmental, Technological, Social and Economic Matters (ICSF 2020), Kryvyi Rih, Ukraine. https://doi.org/10.1051/e3sconf/202016613028

Taylor, H., (2023, May 11). How fintech is helping build a more sustainable financial future. Cryptomathic. https://www.cryptomathic.com/news-events/blog/how-fintech-is-helping-build-a-more-sustainable-financial-future#:~:text=FinTech%20solutions%20can%20help%20businesses,in%20attaining%20global%20environmental%20objectives

Tripathi, S., & Rajeev, M. (2023). Gender-inclusive development through fintech: Studying gender-based digital financial inclusion in a cross-country setting.Sustainability,15(13), Article e10253. https://doi.org/10.3390/su151310253

Velenturf, A. P. & Purnell, P. (2021). Principles for a sustainable circular economy. Sustainable Production and Consumption, 27, 1437–1457. https://doi.org/10.1016/j.spc.2021.02.018

Venkatesh, V., Morris, M. G., Davis, G. B., & Davis, F. D. (2003). User acceptance of information technology: Toward a unified view. MIS Quarterly, 27(3), 425–478. https://doi.org/10.2307/30036540

Xie, J., Ye, L., Huang, W., & Ye, M. (2021). Understanding fintech platform adoption: Impacts of perceived value and perceived risk. Journal of Theoretical and Applied Electronic Commerce Research, 16(5), 1893–1911. https://doi.org/10.3390/jtaer16050106

Yan, C., Siddik, A. B., Yong, L., Dong, Q., Zheng, G-W., Rahman, M. N., (2022). A two-staged SEM-artificial neural network approach to analyze the impact of FinTech adoption on the sustainability performance of banking firms: The mediating effect of green finance and innovation. Systems, 10(5), Article e 148.https://doi.org/10.3390/systems10050148

Zamora-Polo, F., Sánchez-Martín, J., Corrales-Serrano, M., & Espejo-Antúnez, L. (2019). What do university students know about sustainable development goals? A realistic approach to the reception of this UN program amongst the youth population. Sustainability, 11(13), Article e3533. https://doi.org/10.3390/su11133533

Zhang, Y., Liu, C., Cao, Y., & Yang, Z. (2021). The effect of fintech adoption on sustainability: Evidence from China. Sustainability, 13(5), Article e2925.

Zhou, T. (2012). Understanding users’ initial trust in mobile banking: An elaboration likelihood perspective.Computers in Human Behavior,28(4), 1518–1525. https://doi.org/10.1016/j.chb.2012.03.021

Ziemba, E. (2019). Synthetic indexes for a sustainable information society: Measuring ICT adoption and sustainability in Polish government units. In E. Ziemba (Ed.), Information technology for management: emerging research and applications. Springer.