Aribah Aslam*, and Ghulam Ghouse

Department of Economics, University of Lahore, Pakistan

*Corresponding Author: [email protected]

Abstract

Trust in financial institutions (ToF) is considered essential for an effective financial system, yet, little has been explored regarding what determines them, particularly in the case of Pakistan. By using World Values Survey data (wave 7), large cross-provincial differences are observed for the trust on banks, which confirmed the influence of several socio-demographic indicators. The findings indicate that men tend to trust banks more than women in most cases and trust in banks tends to increase with income, but not in every province. However, it decrease with age in provinces like Balochistan, and media and internet access bring novel results for the trust in financial institutions. Additionally, trusting religious and political institutions, such as trust in government or civil wars, and economic values may affect the trust in financial institutions too. Therefore, the current study suggests policymakers that a uniform strategy may not work equally well in boosting trust on financial institutions (ToF) across all provinces of Pakistan. However, media literacy and financial education can be prioritized, particularly in areas with lower educational attainment, which could be instrumental in fostering confidence in banks.

Keywords: financial inclusion policies, Trust Financial institutions (ToF), regional variation, economic development, determinants

In contemporary banking and finance, establishing and maintaining trust within financial institutions assumes paramount significance (Zulfiqar et al., 2016). It is a foundational cornerstone upon which the nation's financial stability rests. This interdependence between the cultivation of trust and the integrity of financial systems underscores a complex mechanism of different social, political, economic, and cultural elements (Gillespie & Hurley, 2013). Beyond capital flows, trust shapes investor sentiments, streamlines interbank operations, and overall enables people’s engagements that constitute fiscal stability. This relationship between trust in financial institutions, financial inclusion, and financial institutions becomes inextricably linked with the socio-political stabilities of the country. The trust in financial institutions, hereafter referred to as ToF, is contingent upon diverse determinants that extend beyond the confines of mere financial parameters, such as marital status, gender, media, education, varying age groups, income stratifications, religiosity most importantly, the influence of the historical contexts like civil war or confidence in the government. A recent example of this incident could be the global financial crises of 2007 and the recent upheavals caused by the COVID-19 pandemic that underscore the vital role of ToF plays in these crucial times (Amagoh, 2008; Ghouse et al., 2021). During the global financial crisis of 2008, the mortgage crisis in the United States led to a series of events that significantly eroded public trust in financial institutions (Aslam et al., 2020). ToF forms the basis of financial inclusion and stability, with far-reaching implications for economic growth.

Inclusive growth is a new growth theory which is determined by financial inclusion (Zulfiqar et al., 2016). Inclusive growth is the new drive of modern economic development that talks about caring for each member of society. Pakistan, one of the most populous countries, not only in South Asia but also in the world, requires particular interest due to its demographic heft and belonging to lower-middle-income countries.

The province of Punjab is relatively more stable and developed as compared to other provinces of Pakistan, having all of its four sectors much developed. Sindh province comes second, with relatively economic performance slowed down in recent years and this impacting financial inclusion and thus inclusive growth. The urban center of Sindh like Karachi might hinder access to financial services for low income populations. Thirdly, remittance-driven economy of the province Khyber-Pakhtunkhwa’s (KPK) lead to a higher need for financial services to manage remittances and related transactions (Ali et al., 2012). However, the need for higher financial inclusion is persistent in all provinces, especially in rural areas. The insurgency and security concerns might hinder the expansion of formal financial services, particularly in least developed province i.e. Baluchistan (Hassan et al., 2020).

Similarly, social elements, such as marital status and being a female also links with ToF on a global scale, these elements are likely to take on unique manifestations within the provinces of Punjab, Sindh, Khyber Pakhtunkhwa, and Baluchistan, which should be a scope for future research (Shirazi & Ashraf, 2018). Moreover, the role of media sources in shaping trust is expected to be amplified within Pakistan's media frame, which recently got much independent, playing a significant role in shaping public perceptions (DiMaggio, 2009; Saleem, 2007). Moreover, the interrelationship between trust in financial institutions, trust in various governmental and justice systems, and society after conflicts becomes even more complex when examined within different regional contexts (Filipiak, 2016).

This study brings novelty by investigating trust in financial institutions in Pakistan's four culturally diverse provinces. It uncovers gender disparities, varying income effects, and age-related trends, challenging conventional assumptions. Additionally, the study explores the impact of media and internet access and considers the influence of values and external factors on trust in financial institutions.

We extend the research discourse on ToF by delving into the four regional intricacies of trust dynamics in Pakistan. By doing so, this study aims to provide novel insights for policymakers, financial institutions, and researchers to increase financial inclusion by escalating peoples’ ToF. We seek to shed light on ToF, which can be fortified within the distinctive societal fabric of Pakistan's provinces. In the ensuing sections, we undertake a comprehensive analysis of these determinants of trust, leveraging the insights gained from Figure 1 (see conceptual Linkages). We aim to enrich our understanding of trust in financial institutions within the intricate mosaic of Pakistan's provincial contexts, which has been hardly done in literature by now. The empirical exploration of these objectives relies on the latest iteration (Wave 7) of the World Values Survey, the most recent wave 7. The remainder of the article is structured as follows: Section 2 delves into the literature review, and later, establishes the conceptual foundation of ToF in Section 3. Section 4 outlines the methodology for measuring trust and provides a data description. Section 4 presents trust determinants within Pakistan and its four provinces. Finally, Section 5 concludes the research paper, providing policy guidelines.

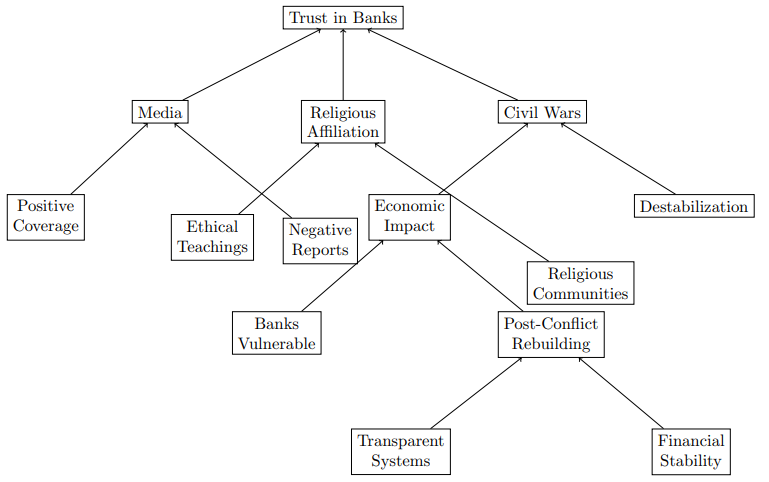

The importance of maintaining trust in financial institutions ToF for short, cannot be overstated (Zulfiqar et al., 2016), as it serves as the bedrock upon which a nation's financial stability is built. It is built through a complex interplay of social, political, economic, and cultural factors (Gillespie & Hurley, 2013). Trust in financial institutions influences investor sentiment, streamlines interbank operations, and underpins the financial interactions that collectively contribute to fiscal stability. This intricate relationship between trust in financial institutions, financial inclusion, and the overall well-being of a country becomes inseparable from its socio-political stability. Trust in financial institutions is shaped by a number of determinants that reach beyond conventional financial metrics. These determinants include marital status, gender, media exposure, education, age groups, income levels, religiosity, and notably, the influence of historical events such as civil wars or public confidence in the government. A recent example underscores the pivotal role ToF plays in times of crisis (Amagoh, 2008). The mortgage crisis in the United States, for instance, triggered a series of events that severely eroded public trust in financial institutions. Trust in financial institutions forms the very foundation of financial inclusion and stability, with implications for a nation's economic growth. Without this trust, the entire banking system is not only compromised but ultimately at risk of collapse. Considering the above Figure 1 elucidates the multifaceted interplay of factors that influence trust in banks, which is used as a proxy of trust in financial institutions. So, trust in financial institutions is centered around "Trust in Banks," (Flavian et al., 2004; Luo et al., 2010; Miremadi et al., 2012). Figure 1 showcases how direct and indirect connections impact various elements and determinants. First, positive and negative media coverage, coupled with the influence of religious teachings, can significantly impact trust in financial institutions.

Furthermore, it is crucial to recognize the impact of religious communities and people’s beliefs or people's perceptions, and attitudes toward financial institutions. Religious teachings often emphasize principles related to financial ethics, savings, and the acceptance or rejection of interest-based economies (Alam, 2017; Badshah et al., 2013; Erol & El‐Bdour, 1989; Hayat & Malik, 2014; Hidayah, 2014; Islam et al., 2023; Lewis, 2001; Pratiwi et al., 2020; Su'un, 2018). These teachings are deeply rooted in the cultural and social fabric of communities that can significantly influence individuals' trust in banking systems (Pratiwi et al., 2020; Su'un, 2018). For instance, in Islamic finance, the prohibition of riba (interest) is a fundamental principle, and this prohibition can lead individuals to seek alternative financial institutions that align with their religious beliefs, potentially eroding trust in conventional banks, and in most extreme forms trust in Islamic banking too. Hence, as an idiosyncratic school of thought it is still believed that even the Islamic banks are not based on Islamic teachings(Usman et al., 2017). Moreover, civil wars and conflicts can have far-reaching consequences on the stability of financial institutions within a country (Baddeley, 2008; Bremmer & Roubini, 2011; Collier, 2000; Jones & Sugden, 2001; Kijewski & Freitag, 2018; Klayman, 1995). The economic destabilization resulting from such conflicts can weaken the foundations of trust in financial systems (Collier, 2000; Kijewski & Freitag, 2018). People may become cautious of placing their financial assets in banks that they perceive as vulnerable to the repercussions of such conflicts.

Figure 1

Conceptual Linkages

In addition to these factors, religious and ethical considerations play an important role in shaping trust in financial institutions (Hayat & Malik, 2014). Religious teachings such as those embedded in islamic shariah, encompass ethical guidelines that influence individuals' financial choices and behaviors. Moreover, institutional structure plays an important role too. AN open access social order; characterized by trust in the government's ability to ensure equitable wealth and income distribution play pivotal role in trust in financial institutions (Badshah et al., 2013; Blind, 2007). Thus, corruption in government or financial systems can hinder the trust on financial institutions, making it challenging to regain public trust. Figure 1 shows how important factors such as social (media), religion, conflicts, ethics may share a strong bond with trust in financial institutions.

The aim of the current study is to explore the dynamics of these linkages within the context of Pakistan.

The main variable of interest is trust in financial institutions measure by " confidence_banks", on a scale of 1 to 4. If someone rates it as 1, it means they have low confidence, while a 4 rating indicates high confidence in banks.

Now, diving into the other variables:

- "Married" is a straightforward one variable; it simply tells us whether someone is married (1) or not (0).

- "Male" and "Female" distinctions help us to understand the gender breakdown, with 0 representing males and 1 representing females.

- "Newspaper," "TV," and "Internet" are all about where people get their information, which was also rated on a scale from 1-5.

- When it comes to education, "Lower_Education," "Middle_Education," and "High_Education" categorize individuals into different education levels, using 0 to signify not having achieved that level and 1 to represent those who have.

- "Age" is quite straightforward; it tells us the age of respondents, ranging from 16-103 years. "Age_Square," on the other hand, is a bit more complex – it's the age squared, likely included to explore potential non-linear relationships between age and confidence in banks.

- Moving to income, "Low_Income," "Middle_Income," and "High_Income" classify respondents based on their income level, using binary values of 0 and 1.

- "Religious" measured how religious someone is on a scale from 1-3.

- "Press" and "Confidence_Government" gauge confidence in the press and government, respectively, on a scale from 1-4.

- Family size is captured by "No_children," "Two_or_less_children," and "Three_or_more_children."

- Lastly, "Justice" evaluates confidence in the justice system, and "Civil_war" reflects concerns about the possibility of a civil war.

Utilizing the aforementioned variables, the equation to be estimated via ordinal logistic regression is as follows: Please note that in equation (1), the coefficients from β0 to β16 correspond to the independent variables for each individual. The error term accounts for the unique variability or random factors specific to each individual.

confidence_banks i = β0 + β1 married i + β2 female i + β3 newspaper i + β4 TV i + β5 internet i + β6 lower_education i + β7 middle_education i + β8 high_education i + β9 age i + β10 age_square i + β11 low_income i + β12 middle_income i + β13 high_income i + β14 religious i + β15 Confidence_government i + β16 justicei + β16 Civil_wari + β16 Two_or_less_children i + β16 Three_or_more_children i i + β16 No_children i + β16 pressi i + εi … (1)

This data is sourced from the World Value Survey (WVS), specifically from the latest wave of Wave 7 spanning the years 2017-2022. Given that the dependent variable, such as "confidence in banks," is measured on an ordinal scale, the choice of using ordinal logistic regression is appropriate for modeling and analyzing the relationship between this ordinal outcome and the predictor variables. Considering that ordinal logistic regression (O-Logit) is employed to analyze the determinants of Trust on Financial Institutions. The use of an ordered logistic model is most appropriate due to several reasons. Firstly, the dependent variable is measured in ordinal scale, meaning that has multiple ordered categories rather than a simple binary outcome. Secondly, the independent variables in the model encompass a mix of categorical and continuous variable, such as marital status (respondent is married or not), gender (respondent is female or not), different income levels, and different educational levels. Ordered logit regression offers versatile and accommodates both types of predictors efficiently. Thirdly, the data is taken from the World Value Survey (WVS- wave 7), a well reputed source for cross-cultural and cross-national studies at a global level since 1980s. Lastly, given the temporal aspect (timely affect) of the survey data from Wave 7, spanning several years, the ordered logit model is robust in handling longitudinal or time-series data, making it a suitable choice for examining how confidence in banks or trust in financial institutions may have evolved over this time period.

Across the four provinces of Pakistan, the sign of the "married" variable may vary, however, the significance remains same (see Tables 1 and 2). In Punjab, being married has a negative impact on ToF, suggesting that it reduces trust in financial institutions (ToF) significantly. In Balochistan, being married reduces confidence in banks. These findings indicate that the influence of marital status on ToF differs between provinces (different for Sindh and KPK), highlighting the importance of regional context. This may be due to increased financial pressure and provincial differences that comes with marriage, as well as the influence of cultural and economic factors specific to the province (Lachance & Tang, 2012). In Sindh and KPK, being married positively influences ToF and this impact is statistically insignificant (too). Now, this possibly could be due to the financial stability and better standard of life (comparatively) associated with marriage in these regions. Additionally, socio-economic factors like income and education may interact with marital status to reinforce this positive impact in these two provinces as indicated by statistically significant findings (Soumare et al., 2016). The mixed results make it difficult to have some conclusive understandings.

Interestingly, gender reveals interesting results too. The "male" variable consistently displays a negative sign across all provinces (except Sindh), indicating that males tend to have higher confidence in banks than females in Sindh only (Goh & Sun, 2014; Heyert & Weill, 2023; Ndubisi, 2006; Wang et al., 2020). The results can be explained by three significant reasons; firstly, Males exhibit higher confidence in banks due to being more involved in the financial sector, secondly, cultural roles, specific to gender position them as financial decision-makers, and thirdly, gender-related challenges faced by women, including discrimination and limited access to financial education opportunities make them trust banks in three provinces where this variable is negative.

Table 1

Empirical Results

|

Variables |

(1) |

(2) |

(3) |

(4) |

(5) |

|

Pakistan |

Punjab |

Sindh |

KPK |

Baluchistan |

|

|

Married |

-0.0882 |

-0.167 |

0.452 |

0.276 |

-1.009 |

|

|

(0.195) |

(0.248) |

(0.452) |

(0.523) |

(2.882) |

|

Male |

0.0835 |

-0.0871 |

0.431* |

-0.0320 |

-0.128 |

|

|

(0.107) |

(0.147) |

(0.224) |

(0.353) |

(0.889) |

|

Newspaper |

0.0669* |

0.0510 |

0.150* |

0.130 |

0.446** |

|

|

(0.0371) |

(0.0492) |

(0.0826) |

(0.114) |

(0.225) |

|

TV |

0.150*** |

0.131*** |

0.146** |

-0.0703 |

0.147 |

|

|

(0.0342) |

(0.0504) |

(0.0720) |

(0.0923) |

(0.239) |

|

Internet |

0.0576 |

0.0348 |

0.174** |

0.106 |

-0.0214 |

|

|

(0.0359) |

(0.0473) |

(0.0856) |

(0.101) |

(0.189) |

|

Lower_Education |

-0.165 |

-0.288 |

-0.214 |

0.421 |

-1.252 |

|

|

(0.170) |

(0.226) |

(0.356) |

(0.526) |

(1.253) |

|

Middle_Education |

-0.0260 |

-0.111 |

-0.498 |

0.838* |

-0.536 |

|

|

(0.165) |

(0.216) |

(0.367) |

(0.495) |

(1.254) |

|

High_Education |

- |

- |

- |

- |

- |

|

Age |

-0.0157 |

-0.0104 |

-0.0930 |

-0.0649 |

-0.358 |

|

|

(0.0248) |

(0.0313) |

(0.0592) |

(0.0872) |

(0.279) |

|

Age_Square |

0.000192 |

0.000153 |

0.00114 |

0.00094 |

0.00359 |

|

|

(0.00029) |

(0.00036) |

(0.00071) |

(0.0011) |

(0.00329) |

|

Low_Income |

-0.225 |

0.134 |

-0.664** |

0.782 |

-1.508 |

|

|

(0.180) |

(0.336) |

(0.331) |

(0.597) |

(1.111) |

|

Middle_Income |

0.0320 |

0.201 |

-0.0457 |

0.909 |

-0.678 |

|

|

(0.166) |

(0.329) |

(0.256) |

(0.564) |

(0.855) |

|

High_Income |

- |

- |

- |

- |

- |

|

Religious |

-0.0660 |

-0.0576 |

-0.278 |

0.821 |

0.465 |

|

|

(0.133) |

(0.214) |

(0.204) |

(0.516) |

(1.593) |

|

Press |

0.212*** |

0.181*** |

0.275*** |

0.201** |

-0.164 |

|

|

(0.0404) |

(0.0515) |

(0.104) |

(0.100) |

(0.350) |

|

Civil_War |

0.375*** |

0.325*** |

0.383*** |

0.242 |

0.564 |

|

|

(0.0536) |

(0.0753) |

(0.105) |

(0.204) |

(0.410) |

|

Confidence_government |

0.501*** |

0.462*** |

0.509*** |

0.63*** |

0.670** |

|

|

(0.0480) |

(0.0624) |

(0.103) |

(0.150) |

(0.306) |

|

No_Children |

0.215 |

0.204 |

-0.108 |

-0.185 |

2.162 |

|

|

(0.233) |

(0.296) |

(0.519) |

(0.701) |

(2.066) |

|

Two_Or_Less_Children |

0.523*** |

0.288 |

0.597 |

0.367 |

2.767 |

|

|

(0.198) |

(0.253) |

(0.435) |

(0.543) |

(1.976) |

|

Three_Or_More_Children |

0.496** |

0.321 |

0.522 |

-0.454 |

3.457* |

|

|

(0.214) |

(0.279) |

(0.451) |

(0.642) |

(1.994) |

|

/Cut1 |

2.466*** |

2.263*** |

1.760* |

3.771** |

-6.454* |

|

|

(0.537) |

(0.736) |

(1.181) |

(1.702) |

(5.592) |

|

/Cut2 |

4.170*** |

3.823*** |

3.920*** |

5.450*** |

-2.671* |

|

|

(0.544) |

(0.743) |

(1.195) |

(1.728) |

(5.568) |

|

/Cut3 |

5.211*** |

4.910*** |

4.987*** |

6.39*** |

-1.281* |

|

|

(0.550) |

(0.751) |

(1.204) |

(1.742) |

(5.562) |

|

|

|

|

|

|

|

|

Observations |

1,665 |

993 |

383 |

208 |

81 |

Note. Standard errors in parentheses

*** p<0.01. ** p<0.05. * p<0.1.

Another important understandings from results are indicated by the role of social factors such as media exposure, which significantly boosts confidence in financial institutions in all provinces (DiMaggio, 2009; Mullainathan & Shleifer, 2002). These results are mostly statistically significant and positive in majority of cases, emphasizing the role of media in shaping trust in the banking sector, regardless of any province. Moreover, just like the role of media is important, the role of Internet is worthwhile too in embracing the trust in financial institutions. The table shows that Internet provides individuals with (easy) access to information about financial institutions and their financial investment options, services of financial institutions, and customer experiences, too. This allows for more informed decision-making and fostering trust on financial institutions. Secondly, online banking or E-commerce provides a platform for more convenience and transparency, enhancing trust in their financial interactions. In Balochistan only, internet usage has a negative effect, although it is not statistically significant. These disparities underline the regional differences in how internet affect ToF (Bayar et al., 2021).

It is important to highlight that in countries like Pakistan, religion plays a very important role even in their financial decisions. The "religious" variable displays varying significance and signs across provinces. In all provinces, religiosity does not have a statistically significant effect on ToF (Aggarwal et al., 2014; Kaur & Kaur, 2022; Sharma, 2017). In KPK, being religious has a positive and statistically significant effect on ToF. In Balochistan, religiosity negatively impacts ToF and is statistically insignificant, too. However, religiosity is closely linked with income levels and education, which makes people more rigid or flexible (in contrast) in their decision-making. These disparities highlighted how the influence of religiosity/religion on ToF differs between provinces all across Pakistan.

Moreover, another important variable is "civil_war" variable, which display varying significance and signs across all provinces, particularly owing to the different security conditions in each province. In Punjab, Sindh, and Pakistan (full sample), the presence of a civil war have a statistically insignificant effect on ToF (Badshah et al., 2013; Blind, 2007; Islam et al., 2023).

The impact of family size on ToF varies across all provinces of Pakistan in terms of significance. In all provinces (independently), family size does not have statistically significant effects on ToF, however, it is significant in borth cases for overall sample of Pakistan. It is important to note that these two provinces of Punjab and Sindh have relatively educated populations, are more concerned about family size and education, while having higher income levels comparatively. Note that having no children or having a small family (two or fewer children) may negatively impact ToF due to a perception of greater financial stability among individuals with larger families after marriage (Furstenberg & Kaplan, 2004; Olson et al., 2003). These effects are statistically significant, suggesting that family size plays a meaningful role in shaping ToF within the socio-cultural context of all provinces.

Table 2

OLOGIT Regression (Eform)

|

Variables |

(1) |

(2) |

(3) |

(4) |

(5) |

|

Pakistan |

Punjab |

Sindh |

KP |

Balochistan |

|

|

Married |

0.8513 |

0.7766 |

1.5349 |

1.4172 |

0.8789 |

|

|

(0.1655) |

(0.1921) |

(0.6901) |

(0.7560) |

(2.5364) |

|

Male |

1.0047 |

0.8347 |

1.5492* |

0.8341 |

0.3539 |

|

|

(0.1070) |

(0.1208) |

(0.3474) |

(0.2949) |

(0.2672) |

|

Newspaper |

1.0636* |

1.0486 |

1.1235 |

1.1285 |

1.3523 |

|

|

(0.0394) |

(0.0515) |

(0.0935) |

(0.1290) |

(0.3130) |

|

TV |

1.1782*** |

1.134** |

1.2008** |

0.9164 |

1.3631 |

|

|

(0.0400) |

(0.0570) |

(0.0864) |

(0.0849) |

(0.2884) |

|

Internet |

1.0584 |

1.0307 |

1.1955** |

1.0765 |

0.9803 |

|

|

(0.0381) |

(0.0487) |

(0.1029) |

(0.1097) |

(0.1845) |

|

Religious |

0.8685 |

0.9503 |

0.6732* |

1.7901 |

1.6842 |

|

|

(0.1165) |

(0.2034) |

(0.1383) |

(0.9432) |

(2.7194) |

|

Press |

1.2497*** |

1.19*** |

1.432*** |

1.245** |

0.8734 |

|

|

(0.0502) |

(0.0609) |

(0.1477) |

(0.1264) |

(0.3030) |

|

Civil_War |

0.9112*** |

0.946** |

0.856*** |

0.85*** |

1.0730 |

|

|

(0.0157) |

(0.0221) |

(0.0314) |

(0.0447) |

(0.1232) |

|

Confidence_government |

1.7037*** |

1.62*** |

1.690*** |

1.89*** |

2.0675** |

|

|

(0.0812) |

(0.1010) |

(0.1747) |

(0.2835) |

(0.6198) |

|

No_Children |

1.2050 |

1.3016 |

0.7450 |

0.7302 |

7.7610 |

|

|

(0.2810) |

(0.3837) |

(0.3860) |

(0.5213) |

(16.1316) |

|

Two_Or_Less_children |

1.6883*** |

1.3798 |

1.6922 |

1.3776 |

13.8085 |

|

|

(0.3338) |

(0.3475) |

(0.7462) |

(0.7585) |

(27.1082) |

|

Three_Or_More_children |

1.6397** |

1.3790 |

1.5885 |

0.6666 |

21.5135 |

|

|

(0.3492) |

(0.3830) |

(0.7269) |

(0.4308) |

(42.4116) |

|

Lower_Education |

0.8565 |

0.7221 |

0.7787 |

1.7132 |

0.2386 |

|

|

(0.1453) |

(0.1623) |

(0.2804) |

(0.9029) |

(0.2982) |

|

Middle_Education |

0.9437 |

0.8727 |

0.5512 |

2.2496 |

0.3100 |

|

|

(0.1555) |

(0.1871) |

(0.2034) |

(1.1143) |

(0.3903) |

|

O.High_Education |

- |

- |

- |

- |

- |

|

Age |

0.9966 |

0.9964 |

0.9167 |

0.9330 |

0.6643 |

|

|

(0.0246) |

(0.0311) |

(0.0539) |

(0.0808) |

(0.1845) |

|

Age_Square |

1.0000 |

1.0001 |

1.0011 |

1.0010 |

1.0043 |

|

|

(0.0003) |

(0.0004) |

(0.0007) |

(0.0011) |

(0.0033) |

|

Low_Income |

0.6730** |

1.1972 |

0.389*** |

1.9306 |

0.2797 |

|

|

(0.1194) |

(0.4031) |

(0.1253) |

(1.1000) |

(0.3031) |

|

Middle_Income |

0.8250 |

1.2211 |

0.6972 |

1.8247 |

0.6630 |

|

|

(0.1358) |

(0.4023) |

(0.1765) |

(0.9797) |

(0.5439) |

|

O.High_Income |

- |

- |

- |

- |

- |

|

/Cut1 |

3.1313** |

4.0395* |

0.8597 |

4.3164 |

0.0005 |

|

|

(1.7210) |

(3.0395) |

(1.0427) |

(7.6425) |

(0.0025) |

|

/Cut2 |

16.896*** |

18.8*** |

7.5489* |

24.592* |

0.0194 |

|

|

(9.3498) |

(14.254) |

(9.1800) |

(43.904) |

(0.1061) |

|

/Cut3 |

47.59*** |

55.8*** |

22.283** |

64.34** |

0.0783 |

|

|

(26.5451) |

(42.612) |

(27.2077) |

(115.52) |

(0.4276) |

|

Observations |

1,665 |

993 |

383 |

208 |

81 |

Note. Se-Eform in parentheses

*** p<0.01. ** p<0.05. * p<0.1.

The "age" variable displays same significance and signs across provinces. In Punjab, Sindh, and KPK, age does not have a statistically significant effect on ToF (Wood & Lichtenberg, 2017; Zeng & Li, 2023). Similar results are seen in terms of Age_square variable too.

Concluding the above discussion, these variables significance and sign vary across all four provinces of Pakistan, reflecting regional differences, socio-economic dynamics, and regional inconsistencies. At the same time, it is also observed that some variables, such as gender and media exposure, exhibit significant and consistent effects on ToF. Other variables including marital status and income levels, show regional disparities in ToF. The findings of this study underscore the importance and relevance of considering provincial context when analyzing the determinants of ToF in Pakistan.

A key question is how to regain Trust in Financial Institutions (ToF) after a crisis or even during or after the pandemic, such as COVID-19, struck the world in most unexpected ways. After the crisis, unforeseen global impacts, such as high inflation, low incomes, recession, or bank failures left a lasting impression on financial systems. During and after the crisis, the role of authorities became crucial for financial institutions that contribute to rebuilding trust and stability in the financial sectors. However, before answering this question it is useful to emphasize that ToF is dependent upon other array of factors that need to be scrutinized at provincial levels in Pakistan. Considering this, the goal of the current study is to enhance financial inclusion by strengthening people's trust in Financial Institutions (ToF). Through the exploration, this study uncovered how ToF can be enhanced within the diverse national social contexts of Pakistan. Ultimately, contributing to more effective financial strategies and practices using ordered logit modeling (O-Logit). The analysis of ToF across the four provinces of Pakistan revealed regional variations in the significance and signs of determinants. While gender and media exposure consistently influenced ToF positively and significantly in all provinces, other factors exhibited diverse effects. Marital status, education levels, and income levels impact ToF differently across regions. For instance, being married enhances ToF in Sindh and Khyber Pakhtunkhwa (KPK) but reduced in Punjab and Balochistan. Similarly, education plays a significant role in Punjab and KPK but this was relatively lower in Sindh and Balochistan. Income levels have varying impacts, it was observed that higher incomes reduced ToF in Balochistan but did not significantly affect other provinces. Markedly, religiosity and family size also display divergent effects. While the presence of a civil war significantly reduced ToF in Balochistan.

These findings underscored the importance of tailoring financial inclusion policies to suit each province’s specific socio-economic and cultural dynamics. Policymakers should recognize that a one-size-fits-all approach may not effectively enhance ToF across different provinces of Pakistan. Therefore, emphasis on media literacy and financial education, especially in regions with lower education levels, could promote confidence in banks (ToF). Furthermore, addressing regional economic disparities and security concerns is crucial for bolstering ToF in conflict-affected areas like Balochistan. By and large, understanding the nuanced provincial determinants of ToF is essential for crafting targeted policies that foster financial inclusion and inclusive growth across Pakistan.

Aggarwal, N., Gupta, M., & Singh, S. (2014). Financial literacy among farmers: Empirical evidence from Punjab. Pacific Business Review International, 6(7), 36–42.

Alam, N. (2017). Islamic finance a practical perspective. Springer.

Ali, K., Khalid, U., & Khalid, Z. (2012). Promoting financial inclusion and literacy in Pakistan via G2P payment programs. Pakistan Microfinance Network for the World Bank. https://tinyurl.com/zmd78wdp

Amagoh, F. (2008). Perspectives on organizational change: Systems and complexity theories. The Innovation Journal: The Public Sector Innovation Journal, 13(3), 1–14.

Aslam, A. (2020). The hotly debate of human capital and economic growth: Why institutions may matter? Quality & Quantity, 54(4), 1351–1362. https://doi.org/10.1007/s11135-020-00989-5

Baddeley, M. (2008). Poverty, armed conflict and financial instability. University of Cambridge. https://doi.org/10.17863/CAM.5596

Badshah, I., Mellemvik, F., & Timoshenko, K. (2013). Accounting from a religious perspective: A case of the central government accounting in Islamic Republic of Pakistan. Asian Economic and Financial Review, 3(2), 243–258.

Bayar, Y., Gavriletea, M. D., & Păun, D. (2021). Impact of mobile phones and internet use on financial inclusion: Empirical evidence from the EU post-communist countries. Technological and Economic Development of Economy, 27(3), 722–741. https://doi.org/10.3846/tede.2021.14508

Blind, P. K. (2007, June 26–29). Building trust in government in the twenty-first century: Review of literature and emerging issues. 7th global forum on reinventing government building trust in government, Expert Associate UNDESA Vienna, Austria. https://www.almendron.com/tribuna/wp-content/uploads/2016/11/building-trust-in-government-in-the-twenty-first-century.pdf

Bremmer, I., & Roubini, N. (2011, January 31). AG-zero world: The new economic club will produce conflict, not cooperation. Foreign Affairs, https://www.foreignaffairs.com/world/g-zero-world

Collier, P. (2000). Economic causes of civil conflict and their implications for policy. World Bank. https://gsdrc.org/document-library/economic-causes-of-civil-conflict-and-their-implications-for-policy/

DiMaggio, A. (2009). When media goes to war: Hegemonic discourse, public opinion, and the limits of dissent. NYU Press.

Erol, C., & El‐Bdour, R. (1989). Attitudes, behaviour, and patronage factors of bank customers towards Islamic banks. International Journal of Bank Marketing, 7(6), 31–37. https://doi.org/10.1108/02652328910132060

Filipiak, U. (2016). Trusting financial institutions: Out of reach, out of trust? The Quarterly Review of Economics and Finance, 59(C). 200–214. https://doi.org/10.1016/j.qref.2015.06.006

Flavian, C., Torres, E., & Guinaliu, M. (2004). Corporate image measurement: A further problem for the tangibilization of Internet banking services. International Journal of Bank Marketing, 22(5), 366–384. https://doi.org/10.1108/02652320410549665

Furstenberg, F. F., & Kaplan, S. B. (2004). Social capital and the family. In J. Scott, J. Treas, & M. Richards, (Eds.), The blackwell companion to the sociology of families (pp. 218–232). Blackwell Publishing. https://doi.org/10.1002/9780470999004.ch13

Ghouse, G., Aslam, A., & Bhatti, M. I. (2021). Role of islamic banking during COVID-19 on political and financial events: Application of impulse indicator saturation. Sustainability, 13(21), 116–119. https://doi.org/10.3390/su132111619

Gillespie, N., & Hurley, R. (2013). Trust and the global financial crisis. In R. Bachmann & A. Zaheer (Eds.), Advances in trust research (pp 177–204). Edward Elgar. https://doi.org/10.4337/9780857931382.00019

Goh, T.-T., & Sun, S. (2014). Exploring gender differences in Islamic mobile banking acceptance. Electronic Commerce Research, 14, 435–458. https://doi.org/10.1007/s10660-014-9150-7

Hassan, J., Muhammad, N., Sarwar, B., & Zaman, N. U. (2020). Sustainable development through financial inclusion: The use of financial services and barriers in Quetta-Pakistan. European Online Journal of Natural and Social Sciences, 9(4), 691–707.

Hayat, U., & Malik, A. (2014). Islamic finance: Ethics, concepts, practice. Practice CFA Institute Research Foundation L2014-3. https://ssrn.com/abstract=2616257

Heyert, A., & Weill, L. (2023). The gender gap in trust in banks. Research in International Business and Finance, 66, Article e102032. https://doi.org/10.1016/j.ribaf.2023.102032

Hidayah, N. (2014). Religious compliance in Islamic financial institutions [Doctoral dissertation]. Aston University. https://publications.aston.ac.uk/id/eprint/24762/1/Hidayah_Nunung_N._2014.pdf

Islam, Y., Mindia, P. M., Farzana, N., & Qamruzzaman, M. (2023). Nexus between environmental sustainability, good governance, financial inclusion, and tourism development in Bangladesh: Evidence from symmetric and asymmetric investigation. Frontiers in Environmental Science, 10, Article e1056268. https://doi.org/10.3389/fenvs.2022.1056268

Jones, M., & Sugden, R. (2001). Positive confirmation bias in the acquisition of information. Theory and Decision, 50, 59–99. https://doi.org/10.1023/A:1005296023424

Kaur, S., & Kaur, K. (2022). An evaluation of availability of financial inclusion services in Punjab. International Journal of Early Childhood Special Education, 14(4), 1815–1823.

Kijewski, S., & Freitag, M. (2018). Civil war and the formation of social trust in Kosovo: Posttraumatic growth or war-related distress? Journal of Conflict Resolution, 62(4), 717–742. https://doi.org/10.1177/0022002716666324

Klayman, J. (1995). Varieties of confirmation bias. Psychology of Learning and Motivation, 32, 385–418. https://doi.org/10.1016/S0079-7421(08)60315-1

Lachance, M.-E., & Tang, N. (2012). Financial advice and trust. Financial Services Review, 21(3), 209–226.

Lewis, M. K. (2001). Islam and accounting. Accounting Forum, 25(2), 103–127. https://doi.org/10.1111/1467-6303.00058

Luo, X., Li, H., Zhang, J., & Shim, J. P. (2010). Examining multi-dimensional trust and multi-faceted risk in initial acceptance of emerging technologies: An empirical study of mobile banking services. Decision Support Systems, 49(2), 222–234. https://doi.org/10.1016/j.dss.2010.02.008

Miremadi, A., Ghalamakri, S., & Ramezani, A. (2012). Challenges in trust and security by implementation of E-CRM among banks and financial institution: A case study of e-banking in Iran. International Journal of Information Science and Management, 10(1), 99–118.

Mullainathan, S., & Shleifer, A. (2002). Media bias (National Bureau of Economic Research Working Paper No. 9295). https://doi.org/10.3386/w9295

Olson, P. D., Zuiker, V. S., Danes, S. M., Stafford, K., Heck, R. K., & Duncan, K. A. (2003). The impact of the family and the business on family business sustainability. Journal of Business Venturing, 18(5), 639–666. https://doi.org/10.1016/S0883-9026(03)00014-4

Ndubisi, N. O. (2006). Effect of gender on customer loyalty: A relationship marketing approach. Marketing Intelligence & Planning, 24(1), 48–61. https://doi.org/10.1108/02634500610641552

Pratiwi, E. K., Medias, F., & Janah, N. (2020). Perception of non-muslim religious leaders to Islamic financial institutions (Conference session). 1st Borobudur International Symposium on Humanities, Economics and Social Sciences (BIS-HESS 2019). https://doi.org/10.2991/assehr.k.200529.188

Saleem, N. (2007). US media framing of foreign countries image: An analytical perspective. Canadian Journal of Media Studies, 2(1), 130–162.

Sharma, R. (2017). Financial inclusion in Punjab: An inter district analysis. SAARJ Journal on Banking & Insurance Research, 6(4), 36–42.

Shirazi, N. S., Javed, S. A., & Ashraf, D. (2018). The interlinkage between social exclusion and financial inclusion: Evidence from Pakistan.. http://dx.doi.org/10.2139/ssrn.3183623

Soumare, I., Tchana, F. T., & Kengne, T. M. (2016). Analysis of the determinants of financial inclusion in Central and West Africa. Transnational Corporations Review, 8(4), 231–249. https://doi.org/10.1080/19186444.2016.1265763

Su'un, S. U. Possumah, B. T., Appiah, M. K., & Hilmiyah, N. (2018). Determinants of Islamic banking adoption across different religious groups in Ghana: A panoptic perspective. Journal of International Studies, 11(4), 138–154. https://doi.org/10.14254/2071-8330.2018/11-4/10

Usman, H., Tjiptoherijanto, P., Balqiah, T. E., & Agung, I. G. N. (2017). The role of religious norms, trust, importance of attributes and information sources in the relationship between religiosity and selection of the Islamic bank. Journal of Islamic Marketing, 8(2), 158–186. https://doi.org/10.1108/JIMA-01-2015-0004

Wang, X., Cai, L., Zhu, X., & Deng, S. (2020). Female entrepreneurs’ gender roles, social capital and willingness to choose external financing. Asian Business & Management, 21, 432–457. https://doi.org/10.1057/s41291-020-00131-1

Wood, S., & Lichtenberg, P. A. (2017). Financial capacity and financial exploitation of older adults: Research findings, policy recommendations and clinical implications. Clinical Gerontologist, 40(1), 3–13. https://doi.org/10.1080/07317115.2016.1203382

Zeng, Y., & Li, Y. (2023). Understanding the use of digital finance among older internet users in urban China: Evidence from an online convenience sample. Educational Gerontology, 49(6), 477–490. https://doi.org/10.1080/03601277.2022.2126341

Zulfiqar, K., Chaudhary, M. A., Aslam, A. (2016). Financial inclusion and its implications for inclusive growth in Pakistan. Pakistan Economic and Social Review, 54(2), 297–325.