Zahid Bashir1*, Muhammad Aamir2, and Sabeeh Iqbal2

1Department of Commerce, University of Gujrat, Pakistan

2Hailey College of Commerce, University of Punjab, Lahore, Pakistan

* Corresponding Author: [email protected]

The current study aims to investigate boardroom diversity and its varying characteristics by using agency theory to examine the effect of debt and agency costs in the manufacturing sector of Pakistan. Precisely, it seeks to examine how board size, independence, and gender diversity affect the financial matrices of a firm’s profitability. Therefore, the study utilized an imbalanced panel of 105 manufacturing companies that were listed on the Pakistan Stock Exchange (PSX) 2003 to 2022. Furthermore, the study utilized static and dynamic panel models to examine and evaluate the proposed hypotheses. The findings of this study indicated that there is a positive relationship between board size, gender diversity, and debt and agency costs for manufacturing enterprises in Pakistan. Conversely, it was observed that board independence has a negative impact on the debt and agency costs of firms. Future research can use experimental or longitudinal approaches, including varied businesses, to investigate qualitative research for deeper insights. Cross-cultural comparisons would support the findings. Consequently, this study highlighted the importance of exercising caution when evaluating the influence of board composition on debt and agency costs. The results of the study also prompted inquiries regarding the financial ramifications of initiatives aimed at promoting gender diversity.

Keywords: agency cost, board’s characteristics, debt cost, GMM, manufacturing industry

JEL Codes: C23, G32, J16, L67, M12

Debt cost, commonly known as the cost of debt or interest cost, denotes the financial outlays borne by a corporation to fulfil its debt responsibilities (Brockman & Unlu, 2009). This encompasses the payments of interest made on loans, bonds, or other types of borrowed capital. Furthermore, the assessment of loan expenses holds significant importance for enterprises as it immediately influences their fiscal well-being and potential to generate profits (Brüggen et al., 2017). Moreover, Suhadak et al. (2019) argued that excessive debt expenses can exert pressure on a company's liquidity and diminish its capacity to allocate resources towards expansion prospects or deliver dividends to stakeholders. Hence, it is imperative to comprehend and handle the expenses associated with debt to ensure financial viability, which may optimize the allocation of capital.

According to Dirzka and Acciaro (2021), the concept of agency cost pertains to the financial burdens and operational inefficiencies that usually arise as a result of the principal-agent relationship within a corporate setting. This particular association encompasses stockholders or principals, who entrust managers or executives, known as agents, with the responsibility of making decisions and overseeing the company’s operations on their behalf. Furthermore, agency expenses arise when there is a divergence of interests between principals and agents (Hill & Jones, 1992). Moreover, agency costs encompass various factors that can potentially hinder the alignment of interests between managers and shareholders (Murray et al., 2019). These factors, include managerial self-interest, the issue of excessive executive compensation, inefficient decision-making, and the monitoring expenses borne by shareholders to ensure that managers act in the best interests of their shareholders.

The focus of this study inquiry pertains to the examination of the impact of distinct board features, including size, independence, and diversity, on the cost of debt and agency costs within the manufacturing sector of Pakistan. It also aims to investigate the specific attributes, which might alleviate inefficiencies, conflicts of interest, and poor decision-making in the companies. In particular, the study examines how board size, independence, and diversity reduce debt and agency costs in the manufacturing sector of Pakistan. The research aims to investigate the impact of board characteristics of manufacturing companies in Pakistan on their debt cost, and agency cost during the study period 2003-22.

This study adds to the body of knowledge and provide suggestions to improve corporate governance by investigating board size independence and gender diversity. The findings of this study will be helpful for the manufacturing industries of Pakistan to make better financial decisions. These findings may also boost stakeholder confidence and lower these companies' borrowing rates. The research may also help in shaping policy by illuminating governance laws tailored to the industrial industry. Examining gender diversity on corporate boards promotes inclusivity in governance systems, improving decision-making, and potentially lowering agency costs. The longitudinal approach provides valuable insights into regional governance practices and financial outcomes over time.

The examination of the impact of board characteristics on debt cost as well as on agency cost is commonly approached through agency theory.

Agency theory suggests that improved monitoring and control of the board could lower debt financing costs (Bathala & Rao, 1995). In a likewise manner, better governance and reduced perceived risk may allow creditors to offer better finance, including lower interest rates to companies with larger and more effective boards (Bonazzi & Islam, 2007). Moreover, a larger board allows more people to analyze administrative decisions and hold managers accountable (Roberts et al., 2005). This improved control can lessen agency problems and managers' self-serving interests at the expense of shareholders; thereby, decreasing agency costs.

According to Trinh et al. (2020), agency theory says independent directors on a company's board can eliminate agency conflicts, increase supervision, boost credibility, manage risks, and align board interests with creditors. Thus, creditors may view companies with independent boards as safer debtors, resulting in better debt financing terms. The firm ultimately leads to a reduction in both borrowing as well as agency costs. Agency theory does not address board diversity; however, it does address its principles for effective governance, risk management, and accountability that can be aligned with the potential benefits of a diverse board (Kovermann & Velte, 2019; Luciano et al., 2020). Furthermore, diverse boards can improve decision-making, risk management, and responsibility (Gaio & Gonçalves, 2022; Peng et al., 2021; Shakil, 2021). All these factors are significant in reducing creditor risk perceptions. Thus, creditors may view diverse boards as lower-risk borrowers, resulting in better debt financing terms. This reduces corporate and agency borrowing costs.

A larger board can provide more knowledge and supervision, reducing the information asymmetry between managers and external creditors. For example, improved information flow may reduce creditors' perceived risk, lowering interest rates, and loan costs (Trinh et al., 2020). Furthermore, Pekovic and Vogt (2021) found that a larger board may also boost a firm's governance legitimacy and effectiveness. Moreover, a larger board may indicate strong governance and receptivity to lenders, improving loan terms and lowering debt costs (Kim et al., 2022). Additionally, a larger board of directors can also help in resolving conflicts and by making significant decisions that may benefit the company in the future (Aksoy & Yilmaz, 2023; Rixom et al., 2023). Implementing this measure has the potential to decrease the probability of conflicts that may have adverse effects on the company's credit rating and borrowing costs. Therefore, the study tested the following hypothesis.

H1a: : A larger board reduces debt costs.

A larger board of directors can better oversee and control managerial behavior. Zhang et al. (2020), proclaimed that more directors may scrutinize CEO decisions and decrease agency costs from managerial opportunism. Furthermore, a larger board can also bring more skills and experiences to the decision-making process, by significantly increasing the overall board diversity (Pekovic & Vogt, 2021). Moreover, board diversity can reduce group thinking and boost the board's ability to solve agency problems (Huynh et al., 2022). However, a large board may diminish decision-making efficiency, causing delays and inefficiencies (Chaudhary, 2022). Likewise, directors may struggle to coordinate and disseminate information, which may increase agency costs (Roy & Chakraborty, 2023). Therefore, the study tested the following hypothesis.

H1b: A larger board reduce agency cost.

A board that exhibits a greater level of independence is frequently regarded as indicative of robust corporate governance. For example, increased trustworthiness may reduce creditors' perceived risk, improve financing conditions, and lower the company's loan cost (Bacha et al., 2021). In a similar vein, Chen et al. (2022) found that independent directors are less likely to have conflicts of interest with management, which may improve their supervisory effectiveness. Furthermore, the ability of individuals to question managerial choices and promote openness can improve corporate governance, reducing loan risk, and debt expenses (Chaudhary, 2022; Chen et al., 2023). Therefore, the study tested the following hypothesis.

H2a : Increasing the board’s independence reduces the debt cost.

Independent directors serve as a mechanism to mitigate managerial opportunism and self-interest. The impartiality and prioritization of shareholders' interests over managerial interests might result in enhanced monitoring and control of managerial behavior; thus, mitigating agency costs (Trinh et al., 2020). Moreover, the inclusion of independent directors on the board of directors enhances decision-making processes by introducing a wide range of perspectives and specialized knowledge (Zhang et al., 2020). Furthermore, critical thinking can improve strategic decision-making by reducing agency costs associated with inferior choices (Bacha et al., 2021). Nevertheless, independent directors are responsible for ensuring that CEOs are held accountable for their conduct (Chaudhary, 2022). The presence of individuals or entities with ethical standards serves as a deterrent to unethical action; hence, decreasing the probability of engaging in misbehavior or contempt (Roy & Chakraborty, 2023). This, in turn, helps to mitigate potential damage to reputation and finances, while also reducing agency expenses. Therefore, the study tested the following hypothesis.

H2b : Increasing the board’s independence reduces agency costs.

Diverse boards may improve risk and decision-making. Diverse perspectives can help to identify and address difficulties, minimizing the firm's risk and financing cost (Pandey et al., 2020). Additionally, a diverse board can boost a firm's brand and ties with stakeholders, including creditors (Beji et al., 2021). Moreover, positive stakeholder connections may improve loan conditions and debt costs (Gaio & Gonçalves, 2022). Furthermore, board diversity may affect these costs differently for different firms (Aksoy & Yilmaz, 2023; Chen et al., 2023; Rixom et al., 2023; Roy & Chakraborty, 2023). Therefore, this study tested the following hypothesis.

H3a: The board’s diversity reduces debt costs.

H3b: Board diversity decreases agency costs.

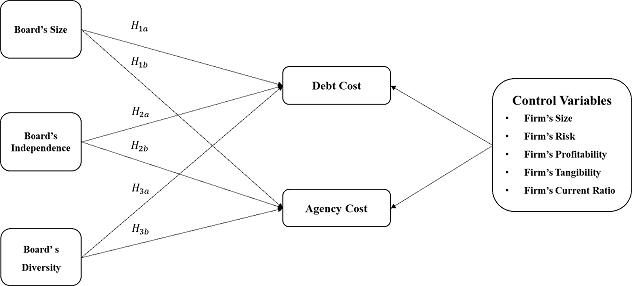

The study uses agency theory to evaluate how board size, independence, and diversity affect loan and agency costs in the manufacturing industry of Pakistan from 2003 to 2022. Figure 1 indicates the research framework of the study and the required set of hypotheses to be tested for this study.

Figure 1

Research Framework based on Agency Theory

This study used 105 manufacturing businesses listed on the Pakistan Stock Exchange (PSX) from 2003 to 2022. Financial, food, and transit companies were intentionally excluded from our sample because of their distinct governance, finance, and regulation. Furthermore, any observations that contained incomplete data were excluded from the study. Consequently, the final dataset comprises a total of 1700 observations (unbalanced panel) for combinations of firm-year. The data utilized in this study was obtained from the annual reports and financial statements accessible on the respective organizations’ official websites.

The study uses proxies, dependent variables, independent variables, and control variables. Velte (2017) argued that the empirical analysis preferred accounting-based indicators over market-based metrics due to their greater reliability, which is attributable to accounting data auditing. The study incorporates debt cost and agency cost as dependent variables in its accounting-based measurements. The research also used board characteristics, including size, independence, and diversity, as independent variables. Control factors were business size, risk level, profitability, tangibility, and current ratio. This inclusion helped construct models that examined the relationship between board characteristics, debt costs, and agency costs. Table 1 provides the detailed operationalization of the variables of the study, including the references from which the measurement of each variable was adopted.

Table 1

Variables’ Operationalization

|

Variables |

Operational Definition |

References |

|

Debt Cost (DC) |

Interest paid/total debt |

|

|

Agency Cost (AC) |

Total Sales/Total Assets ratio |

(Chaudhary, 2022; Roy & Chakraborty, 2023)

|

|

Board Size (B_size) |

Natural log of board members |

(Aksoy & Yilmaz, 2023; Chaudhary, 2022; Roy & Chakraborty, 2023) |

|

Board Independence (Bind) |

Independent board members/total board members |

|

|

Board’s Gender Diversity (B_Div)

|

Female board members/total board members |

|

|

Company’s Size (F_size) |

Natural log of total assets |

(Aksoy & Yilmaz, 2023; Canarella & Miller, 2022; Chaudhary, 2022; Dhoraisingam Samuel et al., 2022; Gao et al., 2020) |

|

Company’s Risk |

Total debt/asset ratio |

|

|

Company's Profitability |

Profit-after-tax/equity ratio |

|

|

Company's tangibleness |

Tangible asset-to-total asset ratio |

|

|

Company's Current Ratio |

Current asset-to-current liability ratio |

The study examines how board characteristics affect the debt and agency costs of 105 PSX-listed Pakistani manufacturing companies from 2003 to 2022. The study used an unbalanced panel data comprising a total number of 1700 observations. To achieve the objectives of the study, the researchers used the Pooled OLS, Fixed effect, and Random effect model’s equation as well as the GMM model.

The data which was analyzed using Pooled Ordinary Least Squares (Pooled OLS), integrated observations from different periods or groups, and applied linear regression (Wooldridge, 2021). It implies a linear relationship between dependent and independent variables but requires independence, homoscedasticity, lack of autocorrelation, endogeneity, perfect multicollinearity, and measurement errors (Baltagi et al., 2008). Furthermore, pooled OLS is used to compare variables across groups or time because of its efficiency and statistical power (Plmper & Troeger, 2007). Equations 1a and 1b used pooled OLS estimation to show how board features affect debt and agency costs.

DCDCit = β0 + ∑(j=2)nβn (Board Characteristics)it+ ∑(j=n+1)kβk (Controls)it + εit (1a)

ACit = β0 + ∑(j=2)nβn (Board Characteristics)it + ∑(j=n+1)kβk (Controls)it + εit (1b)

Here,

DC = Debt cost, AC = Agency cost, Board’s characteristics = Board’s size, Board’s independence, and Board’s diversity, Control variables, include the Firm’s size, risk, profitability, current ratio, and tangibility.

Pooled OLS may not work when assumptions are violated, and panel data analysis may benefit from fixed or random effects to account for unobserved person or time-specific effects (Baltagi et al., 2008).

Panel data analysis addresses unobservable individual or entity-specific effects on the dependent variable using the Fixed Effects (FE) model (Hsiao, 2007). Separating time-varying independent variables and accounting for individual-specific features makes the FE model suited for longitudinal data analysis and controlling unobserved heterogeneity that may distort results (Wooldridge, 2021). Equations 2a and 2b use fixed effect estimation to show how board features affect debt and agency costs:

DCit = (β0 + ui )+ ∑(j=2)nβn (Board Characteristics)it + ∑(j=n+1)kβk (Controls)it + vit (2a)

ACit = (β0 + ui )+ ∑(j=2)nβn (Board Characteristics)it + ∑(j=n+1)kβk (Controls)it + vit (2b)

Panel data analysis uses the Random Effects (RE) model to account for unobserved person or entity-specific effects on the dependent variable (Hsiao, 2007). These effects are assumed to be random variables with a normal distribution that are added as model error factors (Wooldridge, 2021). When unobservable effects change over time and entities, researchers use the RE model on panel data (Baltagi et al., 2008). Equations 3a and 3b use random effect estimation to show how board features affect debt and agency costs:

DCit = β0 + ∑(j=2)nβn (Board Characteristics)it + ∑(j=n+1)kβk (Controls)it + (ui+vit) (3a)

DCit = β0 + ∑(j=2)nβn (Board Characteristics)it + ∑(j=n+1)kβk (Controls)it + (ui+vit) (3b)

Dynamic Panel (DP) Models are advanced statistical methods used in panel data analysis to study how variables change over time in a set of entities (Bun & Sarafidis, 2015). The addition of lagged variable values to panel data models accounts for temporal dependencies and dynamic effects (Ahmad et al., 2021). DP Models are used to explore variable dynamics, to determine how previous values affect future outcomes, and to correct for endogeneity (Chaudhary, 2022). As prior literature has indicated the impact of lagged debt cost and lagged agency cost; therefore, the current study requires testing the hypotheses using this mode (Aksoy & Yilmaz, 2023; Chaudhary, 2022). Thereby, using the dynamic panel model, Equations 4a and 4b show how board features affect debt and agency costs:

DCit = βi + γ(DC)(it-1) + ∑(j=2)nβn (Board Characteristics)it + ∑(j=n+1)kβk (Controls)it + εit (4a)

ACit = βi + γ(AC)(it-1) + ∑(j=2)nβn (Board Characteristics)it + ∑(j=n+1)kβk (Controls)it + εit (4b)

The descriptive data in Table 2 reveal crucial financial and governance characteristics of manufacturing firms in Pakistan. These statistics are taken from 1700 observations. The average cost of debt is 0.12, reflecting these institutions' typical interest rates. This value depends on interest rates and corporate creditworthiness. Agency expenses, with average of 0.90, indicated governance issues. These cost differences, from 0.01 to 4.00, showed the discrepancies that exist in corporate governance. The average board size is 10.60, which implies complexity in the decision-making and governance process. The average board independence is 0.62, which emphasizes the importance of independent board members in handling organizational conflicts of interest. The average board diversity score of 0.29 shows that firms value board diversity. Firm size, profitability, risk, tangibility, and liquidity vary widely, demonstrating the industry's diversity in company size, financial performance, and risk.

Table 2

Descriptive Statistics

|

Variables |

Mean |

STD |

Kurtosis |

Skewness |

Min |

Max |

Count |

|

Debt Cost |

0.12 |

0.10 |

1.67 |

1.20 |

0.00 |

0.66 |

1700 |

|

Agency Cost |

0.90 |

0.56 |

1.66 |

0.98 |

0.01 |

4.00 |

1700 |

|

Board’s Size |

10.60 |

3.85 |

1.27 |

0.84 |

3.00 |

31.0 |

1700 |

|

Board’s Independence |

0.62 |

0.14 |

2.32 |

1.52 |

0.00 |

0.81 |

1700 |

|

Board’s Diversity |

0.29 |

0.09 |

0.24 |

0.09 |

0.00 |

0.71 |

1700 |

|

Firm’s Size |

8.18 |

1.71 |

0.32 |

0.02 |

3.10 |

13.3 |

1700 |

|

Firm’s Risk |

0.32 |

0.20 |

0.42 |

0.36 |

0.00 |

0.89 |

1700 |

|

Firm’s Profitability |

0.09 |

0.12 |

2.60 |

1.97 |

0.01 |

2.98 |

1700 |

|

Firm’s Tangibility |

0.48 |

0.23 |

0.98 |

0.24 |

0.00 |

0.90 |

1700 |

|

Firm’s Current Ratio |

1.42 |

0.97 |

3.01 |

1.75 |

0.01 |

6.00 |

1700 |

A Pearson correlation matrix shows some significant correlations between financial and corporate governance variables. First, loan cost and agency cost are positively correlated (0.3225***). Board size also has a moderately significant positive connection (0.0490**) with agency cost, indicating that larger boards come with a surcharge. Board independence has a moderately significant negative connection (-0.0507**) with debt cost, indicating that a more independent board lowers the debt costs of a firm.

Table 3

Correlation Matrix

|

Variables |

DC |

AC |

B _size |

Bind |

B_div |

F_size |

F_risk |

PRF |

TNG |

CR |

|

Debt Cost (DC) |

1 |

|

||||||||

|

Agency Cost (AC) |

0.322*** |

1 |

|

|||||||

|

(0.000) |

|

|||||||||

|

Board’s Size (B_size) |

0.007 |

0.049** |

1 |

|

|

|

|

|

|

|

|

(0.776) |

(0.0434) |

|

|

|

|

|

|

|

|

|

|

Board’s Independence (Bind) |

-0.051** |

-0.024 |

0.105*** |

1 |

||||||

|

(0.0367) |

(0.3151) |

(0.000) |

||||||||

|

Board’s Diversity (B_div) |

0.046* |

0.112*** |

-0.294*** |

-0.101*** |

1 |

|||||

|

(0.0589) |

(0.000) |

(0.000) |

(0.000) |

|||||||

|

Firm’s Size (F_size) |

0.084*** |

-0.238*** |

-0.087*** |

-0.016 |

-0.051** |

1 |

||||

|

(0.0005) |

(0.000) |

(0.0003) |

(0.5074) |

(0.0361) |

||||||

|

Firm’s Risk (F_risk) |

-0.312*** |

-0.237*** |

-0.031 |

-0.078*** |

0.024 |

0.061** |

1 |

|||

|

(0.000) |

(0.000) |

(0.2002) |

(0.0013) |

(0.3169) |

(0.0117) |

|||||

|

Firm’s Profitability (PRF) |

0.047* |

0.074*** |

0.021 |

0.022 |

-0.055** |

-0.116*** |

-0.080*** |

1 |

||

|

(0.0529) |

(0.0022) |

(0.3936) |

(0.3529) |

(0.024) |

(0.000) |

(0.001) |

||||

|

Firm’s Tangibility (TNG) |

-0.137*** |

-0.483*** |

-0.127*** |

-0.018 |

-0.008 |

0.231*** |

0.324*** |

-0.138*** |

1 |

|

|

(0.000) |

(0.000) |

(0.000) |

(0.4503) |

(0.7534) |

(0.000) |

(0.000) |

(0.000) |

|||

|

Firm’s Current Ratio (CR) |

0.157*** |

0.210*** |

0.0003 |

0.030 |

-0.049** |

-0.114*** |

-0.450*** |

0.069*** |

-0.431*** |

1 |

|

(0.000) |

(0.000) |

(0.991) |

(0.211) |

(0.0447) |

(0.000) |

(0.000) |

(0.0042) |

(0.000) |

Note. p-values in parentheses

*** p<0.01. ** p<0.05. * p<0.1.

Board diversity has a fairly significant positive connection (0.0458*) with debt cost, indicating that boards with more diversity have higher debt costs. Firm size has a highly significant positive connection (0.0845***) with debt cost, showing that larger enterprises have higher debt costs. However, the firm's risk has a highly significant inverse association (-0.3115***) with debt cost, showing that riskier enterprises have lower debt costs. Firm profitability has a highly significant positive association (0.0741***) with agency cost, indicating that more profitable enterprises have higher agency costs. The firm's tangibility has a very strong negative correlation (-0.4826***) with agency cost, indicating that enterprises with more tangible assets have lower agency costs. According to a highly significant positive association (0.1567***), enterprises with greater current ratios have higher debt costs. Therefore, the correlation matrix also shows no significant multicollinearity between the independent variables.

Table 4 displays the outcomes of four distinct regression models employing robust estimates for the impact of board characteristics on debt cost using POLS, FE, RE, and GMM

The statistical significance of at least one of the fixed effects in the FE model is indicated by the F test with F (104, 1586, and p = 0.0000). This test confirmed that the FE model is more appropriate than POLS. Additionally, the Hauseman Specification Test indicates that the RE model is more appropriate than the FE model, with a p-value of 0.0645, respectively. Furthermore, the researchers also estimated the B.P LaGrange Multiplier test to confirm the validity of the random effect model. The test confirmed that the RE model is more appropriate than the POLS model ( = 4687.94, p = 0.0000). The presence of heteroscedasticity ( (105) = 14910.60, p = 0.0000) and autocorrelation F (1, 104) = 54.317, and (p = 0.0000) made the RE model invalidated. A dynamic relationship between debt cost and explanatory factors may have rendered fixed or random effects models ineffective. Thus, the GMM estimator was used to re-evaluate board attributes and debt expense. First Semykina and Wooldridge's (2010) rigorous exogeneity test was used to find variable exogeneity. The Wooldridge stringent exogeneity test reveals significant endogeneity in the models (X^2 = 5.27794, p = 0.0216), rejecting Wooldridge's null hypothesis. Thus, Blundell and Bond's (1998) GMM approach was best for addressing potential endogeneity issues caused by our model's dynamic nature. This model allows to evaluate the relationship between board diversity and debt costs, taking into consideration the changing nature of the relationship. As shown in this study, the GMM technique was designed to analyze the panel data, which includes many enterprises and shorter periods (Roodman, 2009). Table 4 shows Windmeijer (2005) corrective model system GMM outputs. The Hansen test for overidentifying constraints (with a p-value greater than 0.1) and the Arellano-Bond test for autocorrelation (with an AR (1) p-value less than 0.01 and an AR (2) p-value greater than 0.1) show that the GMM model is well-defined.

Table 4 shows that the coefficient for debt cost from the previous year is positive and statistically significant (p < 0.05). This means that previous debt cost values significantly affected the current debt cost. The size of the board also has a statistically significant favorable effect on debt costs. It rejects H_1a and believes that larger boards raise Pakistani industrial debt costs. Larger boards may manage financial risks less efficiently due to greater communication and decision-making complexity, agency issues and lesser responsibility, coordination issues, and market viewpoints. Pakistani regulation and industry characteristics may potentially affect this connection. Board independence has a statistically significant negative influence on debt cost. It accepts H_2a and concludes that enhancing board independence in Pakistan's industrial sector can dramatically cut loan costs. It supports prior research that directors with fewer ties to management or external interests can cut borrowing costs for their firms. Gender diversity on the board has a statistically significant favorable effect on debt cost. The study contradicts H_3a and indicates that boosting gender diversity on the board can dramatically reduce loan costs in Pakistan's manufacturing industry. Market prejudices or stereotypes may encourage lenders to equate diverse boards with higher risk, raising interest rates.

Finally, control variables yield useful results. In the industrial sector of Pakistan, the firm’s size and current ratio greatly reduce debt costs. Larger companies have higher financial stability, assets, and revenue; therefore, lenders view them as safer borrowers. Thus, these organizations can negotiate lower interest rates and better credit terms. A strong current ratio, which shows a firm's ability to fulfil immediate liabilities with current assets, reassures creditors and reduces the risk of non-payment. Additionally, firm risk, profitability, and tangibly enhance target population debt costs. Finance fundamentals support the view that a corporation's risk, profitability, and tangibility affect the target population's loan cost. Lenders demand higher interest rates to offset potential losses due to financial instability, excessive debt, and business risks. This raises borrowing costs, lower profitability means less ability to meet debt obligations, prompting lenders to be cautious and raise interest rates to offset the risk. Due to increased risk exposure, interest rates rise as assets lose tangibility and lenders have less collateral to use in the event of failure.

Table 4

Regression Analysis for Cost of Debt

|

Variables |

DV = Cost of Debt |

||||

|

OLS (Robust) |

FE (Robust) |

RE (Robust) |

Sys. GMM |

||

|

L.Cost of Debt |

- |

- |

- |

0.714*** (0.0346) |

|

|

Board’s Size |

0.00822 (0.00847) |

0.00397 (0.00987) |

0.0468* (0.0095) |

0.00376* (0.0016) |

|

|

Board’s Independence |

-0.0352* (0.0177) |

-0.0729 (0.0488) |

-0.0572* (0.0269) |

-0.0919** (0.0247) |

|

|

Board’s Diversity |

0.0856** (0.0341) |

0.081* (0.0443) |

0.0878** (0.0331) |

0.1162*** (0.0411) |

|

|

Firm’s Size |

-0.0100*** (0.00173) |

-0.00130 (0.00343) |

-0.000414 (0.00313) |

-0.0062*** (0.00149) |

|

|

Firm’s Risk |

0.069** (0.0179) |

0.061* (0.0208) |

0.0653** (0.0203) |

0.0962*** (0.0216) |

|

|

Firm’s Profitability |

0.00883* (0.00386) |

0.00159 (0.00367) |

0.00783* (0.00359) |

0.00938** (0.00277) |

|

|

Firm’s Current Ratio |

-0.0389* (0.0202) |

-0.0736* (0.0413) |

-0.0698** (0.0313) |

-0.0238*** (0.00896) |

|

|

Firm’s Tangibility |

0.0325** (0.015) |

0.0386** (0.0176) |

0.0297* (0.0153) |

0.0557*** (0.0176) |

|

|

Constant |

0.372*** (0.0395) |

0.274*** (0.0465) |

0.278*** (0.0422) |

0.0487 (0.0796) |

|

|

Observations |

1,700 |

1,700 |

1,700 |

1,593 |

|

|

No of Instruments |

- |

- |

- |

78 |

|

|

Number of firms |

105 |

105 |

105 |

105 |

|

|

R2 |

0.595 |

0.527 |

0.545 |

N/A |

|

|

Diagnostics |

|

|

|||

|

F test that all ui=0 |

F(104, 1586) = 28.73, and Prob > F = 0.0000 |

||||

|

Hauseman Specification Test |

chi2(9) = 16.11, and Prob>chi2 = 0.0645 |

||||

|

BP LM test |

chibar2(01) = 4687.94, and Prob > chibar2 = 0.0000 |

||||

|

Modified Wald test for GroupWise heteroscedasticity |

chi2 (105) = 14910.60, and Prob>chi2 = 0.0000 |

||||

|

Wooldridge test for autocorrelation in panel data |

F(1, 104) = 54.317, and Prob > F = 0.0000 |

||||

|

Test of endogeneity |

chi2(1) = 5.27794, and p = 0.0216 |

||||

|

Arellano-Bond tests |

|

||||

|

AR (1) |

z = -5.72 Pr > z = 0.000 |

||||

|

AR (2) |

z = 0.34 Pr > z = 0.734 |

||||

|

Test of Over-id Restrictions |

|

||||

|

Sargan test |

chi2(1367) =1281.73 Prob > chi2 = 0.951 |

||||

|

Hansen test |

chi2(1367) = 94.41 Prob > chi2 = 1.000 |

||||

Note. Robust standard errors in parentheses

*** p<0.01. ** p<0.05. * p<0.1.

Table 5 displays the outcomes of four distinct regression models employing robust estimates for the impact of the board’s characteristics on agency cost using POLS, FE, RE, and GMM.

The statistical significance of at least one of the fixed effects in the FE model is indicated by the F test with F (104, 1586, and p = 0.0000). This test confirmed that the FE model is more appropriate than POLS. Additionally, the Hauseman Specification Test indicates that the FE model is more appropriate than the RE model, with a p-value of 0.0000, respectively. The presence of heteroscedasticity ( (105) = 4042.32, p = 0.0000), and autocorrelation F (1, 104) = 84.319, and (p = 0.0000) made the FE model invalidated. A dynamic relationship between agency cost and explanatory factors may have rendered fixed or random effects models ineffective. Thus, the GMM estimator was used to re-evaluate board attributes and debt expense. Firstly, Semykina and Wooldridge's (2010) rigorous exogeneity test was used to find variable exogeneity. After that the Wooldridge stringent exogeneity test reveals significant endogeneity in the models (X^2 = 17.3894, p = 0.0000), rejecting Wooldridge's null hypothesis. Thus, Blundell and Bond (1998)’s GMM approach was best for addressing potential endogeneity issues caused by model's dynamic nature, which was suggested in this study. This model allows to evaluate the relationship between board diversity and agency cost, taking into account the past agency cost to account for the changing relationship. The Hansen test for overidentifying constraints (with a p-value greater than 0.1) and the Arellano-Bond test for autocorrelation (with an AR (1) p-value less than 0.01 and an AR (2) p-value greater than 0.1) show that the GMM model is well-defined.

In Table 5, the coefficient for the previous year's agency showed a positive direction and statistical significance (p < 0.05). This means that previous agency cost values significantly affected the current agency costs. Board size has a statistically significant beneficial effect on agency costs. It rejects the hypothesis and concluded that a larger board size significantly increases the agency cost in the manufacturing industry of Pakistan. Inefficiency and delay from a larger board's coordination, communication, and longer decision-making processes raise agency costs. Thereby, diluting board member accountability reduces diligence and supervision, increasing agency costs. Larger boards may need more dispute-resolution capabilities, thus, increasing the costs. Compensation, expenses, and resource allocation for a larger board raise agency costs. Furthermore, the board's independence indicates a statistically significant negative impact on the agency costs. It accepts the , and concludes that increasing the independence of boards in the manufacturing industry of Pakistan can significantly reduce the agency cost in this sector. Independent boards without direct financial interests can prioritize shareholder interests and avoid conflicts. They boost efficiency and transparency through increasing governance, accountability, and fiduciary responsibility. Trust in independent boards may lessen the need for costly external monitoring and compliance. Avoid costly legal challenges and regulatory fines with compliance and legal risk mitigation. Moreover, the board’s gender diversity indicates a statistically significant and positive impact on the agency cost. It rejects ., and concludes that by increasing the gender diversity in the board, the agency cost in the manufacturing industry of Pakistan can significantly enhance. A gender-diverse board can improve decision-making by providing more perspectives. However, increased diversity may increase scrutiny and monitoring, increasing governance costs. Divergent opinions may require greater resources for management. Stakeholder expectations for diversity in governance may encourage firms to invest in programmes, training, and development; thus, increasing agency costs. Recruitment and remuneration to attract a varied pool of candidates, organizational image management, and board oversight problems might boost agency expenses.

Finally, control variables yield useful results. In the manufacturing industry of Pakistan, firm size, current ratio, and tangibility greatly reduce agency costs. Companies with higher assets and revenues inspire shareholder trust and lower default and financial distress risks due to their financial stability. A strong current ratio indicates liquidity, reducing short-term financial concerns, and the need for close monitoring or action. Companies with real assets as collateral are less hazardous to creditors and investors, cutting the overall agency costs. These financial advantages increase capital access and lower agency financing costs.

The target population's agency cost rises with company risk and profitability. A firm's high risk demands stakeholders to constantly monitor its operations and financial decisions, increasing agency costs, and resources. Agency relationship management can be complicated and costly when risk needs complex contractual conditions and risk mitigation. However, diminishing profitability suggests financial trouble or inability to meet obligations, increasing stakeholder scrutiny, and monitoring costs. Info asymmetry and data analysis to reduce the gap can enhance agency costs.

Table 5

Regression Analysis for Agency Cost

|

Variables |

DV = Agency Cost |

||||||

|

OLS (Robust) |

FE (Robust) |

RE (Robust) |

Sys. GMM |

||||

|

L. Agency Cost |

|

|

|

0.761*** (0.0428) |

|||

|

Board’s Size |

0.0567** (0.0166) |

0.0339 (0.0259) |

0.0392** (0.0125) |

0.0707*** (0.0173) |

|||

|

Board’s Independence |

-0.0100 (0.0406) |

-0.00941 (0.103) |

-0.0129 (0.0838) |

-0.0619 (0.0940) |

|||

|

Board’s Diversity |

0.138* (0.072) |

0.142** (0.061) |

0.159 (0.107) |

0.1508*** (0.0284) |

|||

|

Firm’s Size |

-0.0225*** (0.00403) |

-0.0358*** (0.0129) |

-0.0338*** (0.0113) |

-0.00732** (0.00296) |

|||

|

Firm’s Risk |

0.208*** (0.0401) |

0.219** (0.0485) |

0.218*** (0.056) |

0.115*** (0.0216) |

|||

|

Firm’s Profitability |

0.0380*** (0.00937) |

0.0282*** (0.00921) |

0.0287*** (0.00922) |

0.0137*** (0.00334) |

|||

|

Firm’s Current Ratio |

-0.0593*** (0.0223) |

-0.0649*** (0.0258) |

-0.0205 (0.0252) |

-0.0489*** (0.020) |

|||

|

Firm’s Tangibility |

-0.501*** (0.0354) |

-0.311*** (0.0888) |

-0.339*** (0.0810) |

-0.159*** (0.0575) |

|||

|

Constant |

1.611*** (0.0930) |

1.501*** (0.118) |

1.508*** (0.119) |

0.387*** (0.0913) |

|||

|

Observations |

1,700 |

1,700 |

1,700 |

1,593 |

|||

|

Instruments |

|

|

|

78 |

|||

|

Number of firms |

105 |

105 |

105 |

105 |

|||

|

R2 |

0.799 |

0.746 |

0.7574 |

N/A |

|||

|

Country FE |

|

YES |

|

|

|||

|

Diagnostics |

|

||||||

|

F test that all ui=0 |

F(104, 1586) = 31.25, and Prob > F = 0.0000 |

||||||

|

Hauseman Specification Test |

chi2(9) = 40.17, and Prob>chi2 = 0.0000 |

||||||

|

BP LM test |

Not Required |

||||||

|

Modified Wald test for GroupWise heteroscedasticity |

chi2 (105) = 4042.32, and Prob>chi2 = 0.0000 |

||||||

|

Wooldridge test for autocorrelation in panel data |

F(1, 104) = 84.319, and Prob > F = 0.0000 |

||||||

|

Test of endogeneity |

chi2(1) = 17.3894, and p = 0.0000 |

||||||

|

Arellano-Bond tests |

|

||||||

|

AR (1) |

z = -5.85 Pr > z = 0.000 |

||||||

|

AR (2) |

z = -0.51 Pr > z = 0.611 |

||||||

|

Test of Over-id Restrictions |

|

||||||

|

Sargan test |

chi2(1367) =1316.49 Prob > chi2 = 0.833 |

||||||

Note. Robust standard errors in parentheses

*** p<0.01. ** p<0.05. * p<0.1.

The study aimed to examine the impact of a board’s characteristics like board size, board independence, and board gender diversity on debt and agency costs for the manufacturing sector of Pakistan. To achieve the objectives of this study, the researcher used an unbalanced panel of 105 manufacturing companies listed in the Pakistan stock exchange (PSX) for two decades (2003-2022). The researchers employed static as well as dynamic panel models to test the hypotheses.

GMM estimations for debt cost and board characteristics show a positive and statistically significant impact of the previous year’s debt cost on the current year’s value. The industrial sector of Pakistan has lower debt costs when the board is independent, larger, and more gender diverse. In the manufacturing sector of Pakistan, risk, profitability, and tangibility increase debt cost, while the size and current ratio face a decline. However, GMM calculations for agency cost and board characteristics show a positive and statistically significant impact of the previous year’s agency cost on the current value. Increased board size, gender diversity, and independence reduced the agency cost of the manufacturing sector of Pakistan. In the manufacturing enterprises of Pakistan, agency cost grows when risk and profitability increase and control variables like size, current ratio, and tangibility decrease.

The study concludes that a larger board and a board’s gender diversity strongly increase the cost of debt. However, the board’s independence strongly decreases the debt and agency costs in the manufacturing sector of Pakistan. Furthermore, a firm’s size and current ratio also play a negative role, while a firm’s risk and profitability play a significant positive role in determining the debt cost and agency cost in the manufacturing sector of Pakistan. Finally, tangibility increases the cost of debt, while it decreases the agency cost for the firms in the manufacturing sector of Pakistan.

Larger boards and gender diversity positively correlate with debt costs, challenging board composition ideas. The strong negative link between board independence, debt levels, and agency expenses emphasizes the importance of independent directors in tackling financial inefficiencies. Therefore, managers must also be cautious when choosing board members, when considering debt costs. Although diversity is valued, it is vital to weigh the benefits against the potential increase in loan costs. Emphasizing board independence may reduce debt and agency costs. Firms should tailor their financial management practices to size, risk, profitability, and tangibility. Understanding how these components affect debt and agency expenses can help decision-makers improve their financial systems. Since they reveal unexpected consequences, the study's findings on gender diversity in boardrooms affect society. Policymakers and advocates must consider gender diversity's financial impacts while supporting diversity programmes. Thus, prioritizing board independence to save agency costs affects corporate governance norms. Furthermore, transparency and accountability depend on strong governance systems. The study of board features and manufacturing sector financial outcomes in Pakistan adds to economic growth and stability discussions. The above data may help shape policies to strengthen and resilient the business ecosystem.

Although the study shows significant association between board qualities and debt/agency cost, it does not prove causality. Experimental or longitudinal research may improve causal understanding. Within a given timeframe, the research has focused on the manufacturing sector of Pakistan. Extrapolating the findings to other sectors or geographies requires caution. The study contained control variables but unknown factors that may have affected debt and agency expenses that were not accounted. Furthermore, the limitations of the study might include data and source biases.

Future researchers should conduct long-term studies to track board qualities and their effects on debt and agency expenses. This strategy can help to identify causal relationships and assess effect persistence. Future research could also include other Pakistani businesses to compare board features and financial performance. Future studies should include qualitative research approaches alongside quantitative analysis to better understand the mechanisms behind the observed relationships, which may have an association with each other. Interviews or polls with board members and executives may reveal relevant context for further analysis. Finally, the study must compare its findings to the present international data, which will allow researchers to verify board qualifications and financial outcomes in different cultural and legal contexts.

Ahmad, N., Mobarek, A., & Roni, N. N. (2021). Revisiting the impact of ESG on financial performance of FTSE350 UK firms: Static and dynamic panel data analysis. Cogent Business & Management, 8(1), Article e1900500. https://doi.org/10.1080/23311975.2021.1900500

Aksoy, M., & Yilmaz, M. K. (2023). Does board diversity affect the cost of debt financing? Empirical evidence from Turkey. Gender in Management: An International Journal, 38(4), 504–524. https://doi.org/10.1108/GM-01-2022-0021

Bacha, S., Ajina, A., & Saad, S. B. (2021). CSR performance and the cost of debt: Does audit quality matter? Corporate Governance: The International Journal of Business in Society, 21(1), 137–158. https://doi.org/10.1108/CG-11-2019-0335

Baltagi, B. H., Bresson, G., & Pirotte, A. (2008). To pool or not to pool? In L. Mátyás & P. Sevestre (Eds.), The econometrics of panel data: Fundamentals and recent developments in theory and practice (pp. 517–546). Springer Berlin Heidelberg. https://doi.org/10.1007/978-3-540-75892-1_16

Bathala, C. T., & Rao, R. P. (1995). The determinants of board composition: An agency theory perspective. Managerial and Decision Economics, 16(1), 59–69. https://doi.org/https://doi.org/10.1002/mde.4090160108

Beji, R., Yousfi, O., Loukil, N., & Omri, A. (2021). Board diversity and corporate social responsibility: Empirical evidence from France. Journal of Business Ethics, 173(1), 133–155. https://doi.org/10.1007/s10551-020-04522-4

Blundell, R., & Bond, S. (1998). Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics, 87(1), 115–143. https://doi.org/https://doi.org/10.1016/S0304-4076(98)00009-8

Bonazzi, L., & Islam, S. M. N. (2007). Agency theory and corporate governance. Journal of Modelling in Management, 2(1), 7–23. https://doi.org/10.1108/17465660710733022

Brockman, P., & Unlu, E. (2009). Dividend policy, creditor rights, and the agency costs of debt. Journal of Financial Economics, 92(2), 276–299. https://doi.org/https://doi.org/10.1016/j.jfineco.2008.03.007

Bruggen, E. C., Hogreve, J., Holmlund, M., Kabadayi, S., & Löfgren, M. (2017). Financial well-being: A conceptualization and research agenda. Journal of Business Research, 79, 228–237. https://doi.org/https://doi.org/10.1016/j.jbusres.2017.03.013

Bun, M. J. G., & Sarafidis, V. (2015). Dynamic panel data models. In B. H. Baltagi (Ed.), The Oxford Handbook of Panel Data (pp. 76–110). Oxford University Press. https://doi.org/10.1093/oxfordhb/9780199940042.013.0003

Canarella, G., & Miller, S. M. (2022). Firm size, corporate debt, R&D activity, and agency costs: Exploring dynamic and non-linear effects. The Journal of Economic Asymmetries, 25, Article e00233. https://doi.org/https://doi.org/10.1016/j.jeca.2021.e00233

Chaudhary, P. (2022). Agency costs, board structure and institutional investors: Case of India. Asian Journal of Accounting Research, 7(1), 44–58. https://doi.org/10.1108/AJAR-12-2020-0130

Chen, G., Chen, X., & Wan, P. (2022). Naive independent directors, corporate governance and firm performance. Frontiers in Psychology, 13, Article e984661. https://doi.org/10.3389/fpsyg.2022.984661

Chen, L., Gao, F., Guo, T., & Huang, X. (2023). Mixed ownership reform and the short-term debt for long-term investment of non-state-owned enterprises: Evidence from China. International Review of Financial Analysis, 90, Article e102861. https://doi.org/https://doi.org/10.1016/j.irfa.2023.102861

Samuel, S. D., Mahenthiran, S., & Ramasamy, R. (2022). CSR disclosures, CSR awards and corporate governance as determinants of the cost of debt: Evidence from Malaysia. International Journal of Financial Studies, 10(4), Article e87. https://doi.org/10.3390/ijfs10040087

Dirzka, C., & Acciaro, M. (2021). Principal-agent problems in decarbonizing container shipping: A panel data analysis. Transportation Research Part D: Transport and Environment, 98, Article e102948. https://doi.org/https://doi.org/10.1016/j.trd.2021.102948

Gaio, C., & Gonçalves, T. C. (2022). Gender diversity on the board and firms' corporate social responsibility. International Journal of Financial Studies, 10(1), Article e15. https://doi.org/10.3390/ijfs10010015

Gao, H., Wang, J., Wang, Y., Wu, C., & Dong, X. (2020). Media coverage and the cost of debt. Journal of Financial and Quantitative Analysis, 55(2), 429–471. https://doi.org/10.1017/S0022109019000024

Hill, C. W. L., & Jones, T. M. (1992). Stakeholder-Agency Theory. Journal of Management Studies, 29(2), 131–154. https://doi.org/https://doi.org/10.1111/j.1467-6486.1992.tb00657.x

Hsiao, C. (2007). Panel data analysis: Advantages and challenges. TEST, 16(1), 1–22. https://doi.org/10.1007/s11749-007-0046-x

Huynh, K., Wilden, R., & Gudergan, S. (2022). The interface of the top management team and the board: A dynamic managerial capabilities perspective. Long Range Planning, 55(3), Article e102194. https://doi.org/https://doi.org/10.1016/j.lrp.2022.102194

Kim, J., Shon, J., & McDonald, B. D. (2022). Does school district board type affect fiscal conditions? Examining debt positions. Public Performance & Management Review, 45(1), 30–53. https://doi.org/10.1080/15309576.2021.1939738

Kovermann, J., & Velte, P. (2019). The impact of corporate governance on corporate tax avoidance: A literature review. Journal of International Accounting, Auditing and Taxation, 36, Article e100270. https://doi.org/https://doi.org/10.1016/j.intaccaudtax.2019.100270

Luciano, M. M., Nahrgang, J. D., & Shropshire, C. (2020). Strategic leadership systems: Viewing top management teams and boards of directors from a multiteam systems perspective. Academy of Management Review, 45(3), 675–701. https://doi.org/10.5465/amr.2017.0485

Murray, A., Kuban, S., Josefy, M., & Anderson, J. (2019). Contracting in the smart era: The implications of blockchain and decentralized autonomous organizations for contracting and corporate governance. Academy of Management Perspectives, 35(4), 622–641. https://doi.org/10.5465/amp.2018.0066

Pandey, R., Biswas, P. K., Ali, M. J., & Mansi, M. (2020). Female directors on the board and cost of debt: Evidence from Australia. Accounting & Finance, 60(4), 4031–4060. https://doi.org/https://doi.org/10.1111/acfi.12521

Pekovic, S., & Vogt, S. (2021). The fit between corporate social responsibility and corporate governance: The impact on a firm’s financial performance. Review of Managerial Science, 15(4), 1095–1125. https://doi.org/10.1007/s11846-020-00389-x

Peng, X., Yang, Z., Shao, J., & Li, X. (2021). Board diversity and corporate social responsibility disclosure of multinational corporations. Applied Economics, 53(42), 4884–4898. https://doi.org/10.1080/00036846.2021.1910620

Plumper, T., & Troeger, V. E. (2007). Efficient estimation of time-invariant and rarely changing variables in finite sample panel analyses with unit fixed effects. Political Analysis, 15(2), 124–139. https://doi.org/10.1093/pan/mpm002

Rixom, J. M., Jackson, M., & Rixom, B. A. (2023). Mandating diversity on the board of directors: Do investors feel that gender quotas result in tokenism or added value for firms? Journal of Business Ethics, 182(3), 679–697. https://doi.org/10.1007/s10551-021-05030-9

Roberts, J., McNulty, T., & Stiles, P. (2005). Beyond agency conceptions of the work of the non-executive director: Creating accountability in the boardroom. British Journal of Management, 16(s1), S5–S26. https://doi.org/https://doi.org/10.1111/j.1467-8551.2005.00444.x

Roodman, D. (2009). How to do Xtabond2: An introduction to difference and system GMM in Stata. The Stata Journal, 9(1), 86–136. https://doi.org/10.1177/1536867X0900900106

Roy, U., & Chakraborty, I. (2023). Market concentration, agency cost and firm performance: A case study on Indian corporate firms. Economic Change and Restructuring, 56(4), 2645–2693. https://doi.org/10.1007/s10644-023-09529-1

Semykina, A., & Wooldridge, J. M. (2010). Estimating panel data models in the presence of endogeneity and selection. Journal of Econometrics, 157(2), 375–380. https://doi.org/https://doi.org/10.1016/j.jeconom.2010.03.039

Shakil, M. H. (2021). Environmental, social and governance performance and financial risk: Moderating role of ESG controversies and board gender diversity. Resources Policy, 72, Article e102144. https://doi.org/https://doi.org/10.1016/j.resourpol.2021.102144

Suhadak, S., Kurniaty, K., Handayani, S. R., & Rahayu, S. M. (2019). Stock return and financial performance as moderation variable in influence of good corporate governance towards corporate value. Asian Journal of Accounting Research, 4(1), 18–34. https://doi.org/10.1108/AJAR-07-2018-0021

Trinh, V. Q., Aljughaiman, A. A., & Cao, N. D. (2020). Fetching better deals from creditors: Board busyness, agency relationships and the bank cost of debt. International Review of Financial Analysis, 69, Article e101472. https://doi.org/https://doi.org/10.1016/j.irfa.2020.101472

Velte, P. (2017). Does ESG performance have an impact on financial performance? Evidence from Germany. Journal of Global Responsibility, 8(2), 169–178. https://doi.org/10.1108/JGR-11-2016-0029

Windmeijer, F. (2005). A finite sample correction for the variance of linear efficient two-step GMM estimators. Journal of Econometrics, 126(1), 25–51. https://doi.org/https://doi.org/10.1016/j.jeconom.2004.02.005

Wooldridge, J. M. (2021). Two-way fixed effects, the two-way mundlak regression, and difference-in-differences estimators. SSRN.

Zhang, L., Zhang, Z., Jia, M., & Ren, Y. (2020). A tiger with wings: CEO–board surname ties and agency costs. Journal of Business Research, 118, 271–285. https://doi.org/https://doi.org/10.1016/j.jbusres.2020.06.026