Conditional Multifactor Assets Pricing Model: An Empirical Analysis of Anomalies in the State Space Framework

Abstract

Factor pricing models are commonly used to assess portfolio risk and predict returns. Factor pricing models are commonly used to assess portfolio risk and predict returns. These models establish a connection between portfolio risk and a set of common factors, which may each have multiple dimensions. The effectiveness of a factor model depends on the selection of risk factors and their perceived sensitivity. In this paper, a Kalman filter-based conditional multifactor price model is employed to examine the influence of fundamentals and macroeconomics on industry portfolios. The approach taken in this study differs from the existing literature in the sense that the time-varying sensitivity of each factor is treated as a series of random processes. In a cross-sectional setting, a sector-based factor model can be used to reduce the possibility of measurement error caused by uncontrolled variables, in particular factor sensitivities. The empirical analysis demonstrates that, with the exception of the travel and leisure industry, the market factor has a substantial impact on the returns of most industries. On the other hand, fundamental components showed statistical significance at 1%, 5%, and 10% levels in explaining sector returns across all industries. The results underline the everlasting significance of fundamental variables across all sectors and the central role of the market factor in generating profits for most enterprises.

Introduction

Several studies have been conducted to explore the many variables to be included in the asset pricing model. Several studies (Athari et al., 2023; Kostin et al., 2022; Miss et al., 2020) shows that stock returns can be predicted over time using the multifactor asset pricing model. For example, Fama and French (1993) proposed a three-factor model (FF3) designed to capture firm size and firm value, on average. Carhart (1997) proposed a four-factor model by adding Jegadeesh and Titman's (1993) momentum factor to FF3, suggesting that stock returns are a function of the momentum anomaly and the three factors advocated by FF3. Besides firm-characteristic-based risk factors, many researchers have also investigated the time series relationship between macroeconomic variables and aggregate stock market returns. Common macroeconomic variables found to be significantly impacting the stock market; include industrial production growth, term spread, credit spread, inflation (Verma & Bansal, 2021), international trade flows (Forbes & Warnock, 2012), foreign exchange rate (El-Diftar, 2023), gold prices (Arouri et al., 2015), money supply (Gunardi & Disman, 2023) and more recently, oil prices. Oil prices have gained particular attention due to their high volatility and are expected to have both direct (Jones & Kaul, 1996; Khalid & Shehzad., 2021) and indirect (Hawaldar et al., 2020) effects on stock market performance.

There is limited research available on the use of multifactor asset pricing model in Pakistan stock market. It is well documented that many firm-based and macroeconomic variables highly correlated with stock market returns, although there is no agreement regarding the number of variables or the types of variables to be included in the asset pricing model. Substantial empirical research has been conducted in developed markets, especially the US market. However, studies on the use of asset pricing models in emerging markets, especially in Pakistan are limited. Empirical studies on the multifactor pricing model have shown that anomalies related to fundamentals[1], such as size, valuation, and idiosyncratic volatility (IV), are useful in predicting returns in emerging markets like Pakistan. These factors have been found to play a significant role in understanding and forecasting the performance of various assets, highlighting their importance in the context of Pakistan's financial market.

This study examines how fundamentals (which are related to firm-specific features), momentum, and macroeconomic anomalies affect the industries and sector portfolios of businesses listed on the Pakistan Stock Exchange (PSX). It expands the current frontier of the multifactor asset pricing model by providing more elaborate specifications to account for time-varying impacts and developing a more complete set of possible fundamentals and macroeconomic variables. The conditional modelling approach employed is unique in two aspects. Firstly, time-varying factor sensitivities are explicitly modelled as individual stochastic processes. Secondly, sectors are used as dependent variables instead of single stocks. The study combines two different strands of anomalies, that is, fundamentals and macroeconomic risk factors, in a single model to evaluate the joint impact by using a unified framework.

The theoretical concept of time-varying beta, which postulates that the correlation between equity returns and various risk indicators might fluctuate over time, serves as the theoretical foundation for this study. The current modelling strategy was deliberately created to capture this occurrence. Markets are consistently organized in terms of sectors, worldwide. Hence, institutional investors are increasingly taking sector allocation into account when making investment decisions. Therefore, this study examines sector-based portfolios. Utilising sector data is primarily motivated by statistical factors. The current study attempts to minimise potential inaccuracies in the variables. It should result in more precise estimates of betas by using aggregated sector data (Chen et al., 1986).

The issue is compelling when viewed in the perspective of the current performance of PSX, which is the best in Asia and has reclaimed tiger status in the area with a 14% increase in PSX index (Mufti, 2016). PSX has been growing rapidly since it was added to the developing markets index of Morgan Stanley Capital International and has already reached a record threshold of 44,000 points. The capital of the market has now risen past eight trillion rupees, demonstrating the size of investments being made there. Foreign investors, especially those from industrialised economies, are now drawn to the marker. Indeed, The Wall Street Journal has declared Pakistan's market profitable for foreign investment.

Furthermore, CPEC has arrived at an opportune time. Billions of dollars of investment and Chinese influence in the project are bound to bring in countless investment opportunities. The project will add 2.5% to the GDP of the country and create jobs in excess of 700,000 in the next 14 years (Haq, 2016). The advances taking place as part of CPEC may be a game changer for Pakistan's economy. The magnitude of trading on PSX is a strong indication of the positivity that surrounds Pakistan at this point in time. Given its inclusion in MCSI and the opportunities under CPEC, it seems that PSX is receiving the attention of international investors.

In the context of a multifactor pricing paradigm, this study probes the practical importance of time-varying factor loadings and their potential impact. It aims to determine, on the basis of the conditional multiple beta series computed using the Kalman filter, whether or not the industrial portfolios of Pakistan require the explicit consideration of the time-varying influence of macroeconomics and fundamentals (Kostin et al., 2022).

The rest of the paper is structured as follows. Section 2 explores the literature on anomalies, with an emphasis on macroeconomic and fundamental factors, after briefly summarising the notion of factor modelling. Section 3 describes the multifactor conditional technique. The common risk factors, empirical findings and relative output are presented in Section 4. Section 5 to conclude this research.

Literature Review

Several empirical investigations have revealed elements that may be able to explain the cross-section of returns, in addition to market beta risk. Investors frequently employ the Capital Asset Pricing Model (CAPM) which uses the market's overall excess return as the main criterion to assess investments. The market beta is used by the model to determine systematic risk. A single beta model, albeit it captures a sizable percentage of the general variation in returns, may not adequately explain the variability in returns among assets (Cheung & Wong, 1992).

According to empirical research, risks related to firm-specific characteristics and macroeconomic factors have a bigger impact on asset pricing than market risk. This seriously calls into question the reliability of CAPM (Bhatti & Khan, 2022).

The most common reasons for the empirical limitations of CAPM, which are in line with these well-documented findings, comprise the lack of risk factors or an underestimation of the whole wealth portfolio. Multifactor pricing models are predicated on the idea that there are several risk factors or common components that might explain the common variance in asset returns. The standard form of a beta pricing model is as follows:

R(i,t) =αi +∑(K=1) k βi k fkt +ϵ(i,t) ϵ(i,t) ~N(0,σ2 k )

where βi k is referred to as factor loading or exposure. The sensitivity of the i-th asset

on the k-th risk factor is denoted by fkt , where for each k = 1…..,K.

The term "αi " refers to the asset-specific intercept in the context of the asset pricing model. The disturbances term, which stands for the irregular parts of the return series, is presumably unrelated to both the collection of risk variables for each time period (t) and the zero mean for all assets i = 1.......,N. It is advantageous to generate zero-mean factors as a general rule when the collection of common factors does not have a mean of zero. This makes it easier to take into account the distinctive qualities of each asset and how they relate to the underlying risk concerns. Multifactor modelling is appealing at first glance but it lacks clarity about the factors that should be included and their respective proportions. In addition to the market beta risk, other empirical studies have found other variables that might explain the cross-section of returns. Fundamental factor models, on the other hand, contend that variables such as the price-earnings ratio (PER), company leverage, or firm size can account for the cross-sectional volatility in returns (Mundi, 2023). Despite the efficacy of fundamental factor models, the precise systemic hazards they represent remains unclear. The third category's momentum models are based on the empirical finding that historical return patterns can predict future returns. These models make use of elements linked to motion. In contrast, unlike the previously described factor types, statistically created factors cannot be viewed directly. Instead, they are deduced from the return data by using statistical approaches for factor selection (Bessler & Schmidt, 2022).

The hypothesis that macroeconomic variables might be able to forecast security returns has inspired a significant quantity of written work. This work investigates whether or not it is possible to forecast stock returns by analysing macroeconomic factors. In the field of multifactor asset pricing models, the study of Chen et al. (1986) is regarded as among the most well-known studies ever conducted. Inflation (both predicted and unforeseen), industrial production, the difference between short-term and long-term interest rates, and the default premium (which is the difference in yield between bonds with good ratings and bonds with poor ratings) are all factors that are considered. This research shows that the chosen risk factors are reasonably priced. Earlier, Maysami and Koh (2000) discovered a cointegrating relationship between changes in Singapore's stock market and changes in inflation, the expansion of the money supply, interest rates, and exchange rate swings. Rjoub et al. (2009) conducted an APT analysis on Istanbul Stock Exchange in response to Tursoy et al.'s (2008) work. The results showed a statistically significant link between stock price fluctuations and the macroeconomic variables they examined. Benaković and Posedel (2010) showed that market index, followed by interest rates, oil prices, and industrial production (all of which positively correlated with market volatility) had the greatest impact on stock prices in the Croatian stock market, while inflation showed a negative correlation. Hsing (2011) examined a number of macroeconomic variables, such as real GDP, stock market growth, government bond yield, real interest rates, exchange rates, and inflation expectations to determine their related impact on the Croatian stock market index.

The second group of variables in this research consists of traits peculiar to each company, or company-specific features. Previous empirical research has shown that building portfolios based on fundamental traits can help achieve risk-adjusted returns (Kaczmarek & Perez, 2022). In a mean-variance efficient market portfolio, Basu (1977) discovered that businesses with low price-earnings ratios (PERs) typically have greater sample returns, whereas those with high PERs display lower sample returns. According to Banz (1981), the effect of size can be seen in the outperformance of small businesses with tiny market capitalization. Moreover, leverage and average returns are positively correlated, according to Bhandari (1988). Additionally, it was discovered that average returns are positively connected with the book-to-market equity ratio, which contrasts the book value and the market value of an organisation. According to Chan et al. (1991), Japanese stocks have a higher value than other stocks. The book-to-market paradox is further supported by the studies of Fama and French (1993, 1995), Lakonishok et al. (1994). The latter also examined other potential explanations for the value premium. Metrics such as return on assets (ROA), current ratio (CR), debt-to-equity ratio (DER), price-earnings ratio (PER), and price-to-book value have been identified by other studies as key determinants of stock returns (Arista & Astohar, 2012).

Research on momentum and reversal approaches started following trials conducted by DeBondt and Thaler (1985, 1987). Over the course of three to five years, they noticed price reversals where stock prices tended to overreact before settling down to their usual levels. The authors discovered that an investing strategy that extends the holding period for long-term losers, while cutting it short for long-term winners, produces higher returns than any alternative method. Jegadeesh (1990) also showed that price reversals could take place over a small amount of time. The creation and performance of investment portfolios is significantly impacted by these findings. Jegadeesh and Titman (1993) and Chan et al. (1991) revealed that the impacts of price momentum become apparent over the medium-term, which can range from three months to one year. These consequences demonstrate that prior winners continue to have an advantage over those who were unsuccessful in the past. Fama and French's three-factor model predicts that long-term price reversals follow a pattern consistent with the model (Anuno et al., 2023). This is due to the fact that stocks that underperform over a long period of time are the ones responsible for creating value premiums. It is not possible for the Fama-French model to adequately describe price momentum or short-term reversals. Some scholars make the connection between profits gained through momentum trading and structural variables, such as calendar effects or liquidity effects. Carhart (1997) illustrated that momentum and reversal techniques, which demand frequent trading, are not exploitable if taken into consideration the costs incurred to execute each trade. Hence, momentum and reversal effects cannot be taken into consideration as a result of the lack of the persuasiveness of the reasons presented above, as well as due to the findings of Grundy and Martin (2001), which suggest that momentum strategies are less appealing when applied to sectors, rather than individual stocks.

Research Methodology

In this section, a standard unconditional multifactor pricing system is analyzed to create a conditional multifactor risk model which would serve as the focal point of further empirical research. When modelling the time-varying effect of macroeconomics and fundamentals on different sectors of Pakistan's industry allocation, it is essential to consider how these factors influence the distribution and composition of industries over time and the generic multifactor beta pricing model is used as a starting point (Kostin et al., 2022). The general form of the model for different sectors of Pakistan's economy can be written as follows:

R(i,t) =β ́(i,t) ft +ϵ(i,t) ϵ(i,t)~N(0,σ2ϵt)

For =1,……,N and t=1,…….,T ; ft and βit are the K×1 vector of risk factors and corresponding factor loadings, respectively. ϵ(i,t) is the vector of normally distributed disturbances with unconditional variance σ2 t . Factor realizations are assumed to be stationary with unconditional moments

E(ft)=0

cov(ft)=Ωt

and to be uncorrelated with the error term

cov(f(k,t),ϵ(t,t))=0,

for all i, k, and t.

The Kalman filter equations can be described by observation equation and state equation as follows:

R(i,t)=αt+β(i,t) R(0,t)+ϵ(i,t)

(αt¦βt )=(C1¦C2 )+[(a1&a2a3a4 )][α(t-1)¦β(t-1) ]+[U1t¦V2t] Xt=ρ+AX(t-1)+Vt

The coefficient Xt is measured through Kalman, while the parameters and are measured through the maximum likelihood method (MLE).

The auxiliary regression which includes fundamental and macroeconomic factors is written as follows:

R(i,t)=[SIZt,HML,WML,IP,TSt ,OILt ,FXt]'

Where,

Difference in PSX large and small return

Difference between log-returns of the chosen value and growth indices

WML = Difference between winner and loser return

Change in Pakistan term structure

Log return of Brent crude oil

Log return of the synthetic US dollar to Pakistani rupee exchange rate

IP = Log return of the industrial production

Excess returns on the Pakistan industry stocks

The series turned out to be stationary by performing a unit root test on the stationarity of the time series data using an Augmented Dickey-Fuller (ADF) test. The test checks whether one unit root holds against the alternative hypothesis that the time series might be stationary.

Data Overview

The data used to estimate the Pakistani multifactor asset pricing model is discussed below. There are many other basic qualities, such as size and value, in addition to a great number of proxies for macroeconomic risks, that have been appraised as having an impact on the returns of shares. Table 1 contains a listing of the variables used in this inquiry as risk factors (Zhu et al., 2020). It is expected that all of them would capture the external variables that have an impact across all sectors. This paper focuses on risk modelling rather than the factor selection methods and employs conditional factor loadings as its primary method of analysis. As a result, components were chosen from variables that have been thoroughly investigated, can be theoretically justified, and have been successfully implemented in previously published research (Natoli & Venditti, 2022). These variables could provide an estimate of a group of unobserved factors that influence the returns on an asset. However, the chosen variables do have some theoretical validity. Each one has been broken down in the past, so that it may be used to illustrate a different component of systemic risk. In order to investigate the issues raised by this research, data on all of the firms listed on PSX was gathered for the years 1995-2022 on a monthly basis. It wasn't until the middle of the 1990s that credible market statistics for individual stocks were finally made available. Thomson Reuters DataStream is the source of information used to compile stock prices and market capitalization. The data on macroeconomic indicators and variables was taken from the International Monetary Fund (IMF), the State Bank of Pakistan (SBP), and the World Bank, respectively.

Explanation of Variables

Each variable represents a specific aspect or characteristic relevant to this study. Each variable is defined and described below, highlighting its significance and how it relates to the current research questions.

Table 1

Symbols and Definitions of Variables

|

Symbols |

Definitions |

|

Term Structure |

This is the distinction between the interest rate on a government bond with a 10-year term and the interest rate on a bond with a three-month term. |

|

Oil Prices |

Brent crude oil rate of return |

|

Exchange rate |

Log return of the US dollar to Pakistan exchange rate |

|

Industrial Production |

Used as proxy to measure the GDP of a country |

|

HML |

Difference between the specified value's log returns and growth indices |

|

SIZE |

Difference between log returns of the PSX Large index and the PSX Small index |

|

WML |

Difference between winner and loser returns |

|

Sector Return |

Excess returns on the Pakistan industry stocks |

Results and Discussion

Table 2 below contains statistical information for 8 different variables used in this study. These variables include MR, SMB, HML, WML, crude oil, exchange rate, industrial production, and term structure. The table provides information on the mean, median, maximum, minimum, standard deviation, skewness, kurtosis, Jarque-Bera, probability, sum, sum of squared deviations, observations, and Augmented Dickey-Fuller (ADF) statistic for each variable.

Table 2

Summary Statistics and Unit Root Test

|

MR |

SMB |

HML |

WML |

Crude oil Price |

Exchange Rate |

Industrial Production |

Term Structure |

|

|

Mean |

-0.704 |

0.004 |

0.023 |

-0.008 |

63.197 |

88.844 |

100.450 |

-2.342 |

|

Median |

-0.709 |

0.006 |

0.015 |

-0.001 |

60.770 |

85.288 |

101.490 |

-2.041 |

|

Maximum |

0.050 |

0.116 |

0.322 |

0.122 |

141.710 |

167.826 |

175.170 |

9.430 |

|

Minimum |

-1.486 |

-0.146 |

-0.105 |

-0.207 |

18.850 |

51.743 |

43.150 |

-14.778 |

|

Std. Dev. |

0.284 |

0.045 |

0.061 |

0.054 |

29.855 |

31.969 |

31.994 |

4.050 |

|

Skewness |

0.321 |

-0.346 |

1.656 |

-0.859 |

0.444 |

0.903 |

0.025 |

-0.415 |

|

Kurtosis |

2.900 |

3.818 |

8.146 |

4.649 |

2.192 |

2.964 |

2.217 |

5.303 |

|

Jarque-Bera |

4.635 |

12.645 |

411.980 |

62.342 |

15.849 |

35.864 |

6.779 |

65.926 |

|

Probability |

0.099 |

0.002 |

0.000 |

0.000 |

0.000 |

0.000 |

0.034 |

0.000 |

|

Sum |

-185.800 |

1.138 |

5.945 |

-1.987 |

16684.100 |

23454.800 |

26519.000 |

-618.316 |

|

Sum Sq. Dev. |

21.180 |

0.533 |

0.982 |

0.767 |

23443.100 |

26874.100 |

2691.900 |

4314.767 |

|

Observations |

264.000 |

264.000 |

264.000 |

264.000 |

264.000 |

264.000 |

264.000 |

264.000 |

|

ADF |

-2.622* |

-16.35*** |

-14.01*** |

-14.00*** |

-2.4594* |

3.468** |

-2.080* |

-5.480*** |

Note. The table presents key descriptive statistics and diagnostic test values for the fundamental and macroeconomics series. The mean is expressed in percentage terms, representing the average values of the variables. The standard deviation is also expressed in percentage terms, indicating the variability or risk of returns over time. Skewness (sk) and Kurtosis (ku) provide insights into the shape and tail behaviour of the return distribution. Positive skewness suggests a longer right tail, while negative skewness indicates a longer left tail. High kurtosis indicates a more peaked and fat-tailed distribution as compared to a normal distribution. Jarque-Bera (JB) statistic is used to test the normality of the return distribution. It assesses whether the returns follow a standard bell-shaped curve. A higher JB value suggests departure from normality. The Augmented Dickey-Fuller (ADF) test checks the stationarity of the sector return series. Stationarity is crucial in time series analysis, since it ensures that statistical properties remain constant over time. Following the name of each industry, the number of companies in the particular industry is given in parentheses.

The market risk premium, denoted by the variable MR, is the distinction between the expected return and the risk-free rate. The average market return is below the risk-free rate because the mean value of MR is negative. The distribution of returns is negatively skewed, as shown by the fact that the median value is negative. The market returns are rather erratic, as indicated by the standard deviation of MR, which is 0.283786. The variable is likely stationary, according to the ADF statistic of -2.622753. SMB stands for the small-minus-big factor which measures how well small-cap equities have performed in comparison to large-cap companies. Since both the mean and median values of SMB are positive, it may be concluded that small-cap companies generally outperform large-cap equities. In comparison to the other variables in the table, the standard deviation of SMB is 0.045024, which is quite low. The variable may be stationary because the ADF statistic for SMB is -16.35392. HML stands for the high-minus-low factor which measures how well value equities have performed in comparison to growth stocks. The positive mean value of HML indicates that value equities typically outperform growth companies. The distribution of returns is negatively skewed, as shown by the negative median value of HML. HML has a standard deviation of 0.06111, which is higher than SMB's average. The HML ADF statistic of -14.01205 indicates that the variable may be stationary. The performance of equities with high momentum as compared to stocks with low momentum is gauged by the winner-minus-loser factor or WML. Since both the mean and median values of WML are negative, it can be concluded that equities with low momentum generally beat those with high momentum. WML has a standard deviation of 0.053997, which is higher than SMB's average. The WML ADF statistic of -14.00063 indicates that the variable may be stationary.

The average price of crude oil is 63.19758, which shows that it is a relatively expensive commodity. Crude oil can range from a maximum value of 141.71 to a minimum value of 18.85, demonstrating the volatility of its price. According to the -2.459404 ADF statistic for CRUDEOIL, the variable may be stationary. The exchange rate between two currencies is shown by the symbol EXCHRATE. The average EXCHRATE value is 88.84423, which shows that one currency is stronger than the other. EXCHRATE has a range of values between 51.7429 and 167.8263, demonstrating the volatility of the exchange rate. The EXCHRATE ADF statistic is 3.468661, which indicates that the variable may not be stationary. IP stands for industrial production, which is a gauge of the economy's industrial sector's output. The average industrial production is rather high, as indicated by the IP's mean value of 100.4523.

Results and Explanation of the State Space Model

Table 3 displays the estimation outcomes for the model based on the fully stated Kalman filter. In Figure 1, the Kalman filter-derived alpha and beta values for the beverage industry exhibit fluctuations attributed to shifts in both fundamental industry-specific elements and broader macroeconomic influences. These fluctuations capture the industry's sensitivity to changes in both internal and external factors. The computed hyperparameters exhibit a wide range of significance, hence suggesting the robustness of the model. The market factor holds considerable importance across all sectors, with the exception of the travel and leisure sector. On the other hand, both fundamental factors exhibit significance at the 1%, 5%, and 10% levels across all sectors. This implies that sector performance can be significantly influenced by market and fundamental issues.

Upon the examination of the macroeconomic determinants, it becomes evident that several parameters including interest rate, term structure, industrial production, and currency rate do not hold equal relevance across all 13 sectors under investigation. The concept of the structural factor, which aims to capture systematic hazards linked to variations in the slope of the yield curve, demonstrates statistical significance in 11 sectors out of a total of 13. This observation highlights the significance of utilising this approach to elucidate hazards that are specific to a certain sector (Jardet & Meunier, 2022). It is noteworthy that the predicted sensitivities to fluctuations in oil price exhibit large deviations across 12 sectors, highlighting its significance as a systematic risk factor. Nevertheless, it is noteworthy that fluctuations in oil prices do not appear to pose a significant systemic risk to industries closely tied to energy, such as chemicals, minerals and mining, as well as travel and leisure.

Moreover, the exchange rate is identified as the primary macroeconomic determinant in elucidating the variations observed in sector return series across different time periods. Except for personal goods and general industries, as well as the telecommunication sector, the exchange rate exerts a notable influence on the remaining 11 sectors. This conclusion is substantiated by scholarly research that underscores the impact of changes in the exchange rate on the performance of various sectors.

Table 3

Parameter Estimates for the Multifactor Kalman filter Model

|

|

α0 |

βrm |

βsmb |

βhml |

βwml |

βip |

βexe |

βyield |

βoilprice |

LogL |

AIC |

|

Auto |

-0.070** |

0.157*** |

0.711*** |

0.338*** |

0.081* |

-0.028** |

-0.009*** |

0.064* |

-0.097** |

-312.442 |

2.078 |

|

Beverages |

-0.001* |

0.137** |

0.311** |

0.118** |

0.051*** |

-0.009 |

0.002** |

0.074 |

-0.077** |

-298.004 |

2.987 |

|

Chemical |

0.035** |

0.195** |

0.793*** |

0.246* |

-0.066** |

-0.023** |

0.006* |

0.066* |

-0.092 |

-299.773 |

1.999 |

|

Chemical and Mining |

0.011* |

0.199** |

0.868** |

0.181** |

-0.055* |

-0.015** |

0.008** |

0.069** |

-0.090 |

-245.469 |

2.658 |

|

Electrical |

-0.042*** |

0.213** |

0.874** |

0.117* |

-0.125** |

-0.026 |

0.001** |

0.068* |

-0.091** |

-312.493 |

2.078 |

|

Food |

0.047** |

0.199* |

0.308*** |

0.213** |

-0.046** |

-0.017 |

0.002** |

0.069** |

-0.067* |

-317.390 |

2.109 |

|

General Industries |

-0.060* |

0.165** |

0.745* |

0.258* |

-0.013*** |

-0.025* |

0.005 |

0.062* |

-0.096** |

-311.903 |

2.075 |

|

Minerals |

0.046** |

0.181** |

0.814** |

0.211*** |

0.084* |

-0.021* |

0.006*** |

0.065 |

-0.103* |

-316.301 |

2.102 |

|

Oil and Gas |

-0.018** |

0.229*** |

0.691*** |

0.228* |

0.015* |

-0.020** |

0.008* |

0.072* |

-0.107*** |

-313.024 |

2.082 |

|

Personal Goods |

0.064** |

0.153* |

0.662* |

0.318** |

-0.008* |

-0.020** |

0.004 |

0.062** |

-0.093* |

-327.365 |

5.933 |

|

Pharmaceutical |

0.076** |

0.191** |

0.754* |

0.238* |

0.013*** |

-0.016 |

0.004* |

0.065* |

-0.094** |

-311.454 |

2.072 |

|

Telecommunication |

0.044*** |

0.210** |

0.836** |

0.186** |

-0.072** |

-0.001*** |

0.003 |

0.070** |

-0.096** |

-312.583 |

2.079 |

|

Travel and Leisure |

0.150** |

0.189 |

0.810 |

0.190 |

0.070 |

-0.029 |

0.007* |

0.069* |

-0.047 |

-316.613 |

2.104 |

Note. The following table shows the estimated parameters of the multifactor specifications used by the Kalman filter based method to 13 industries in Pakistan. The state disturbance variance terms assigned to each regressor are highlighted in the calculated parameters and provide valuable information about the relationship between the variables and the sector. The degree of variability or uncertainty around the impact of each regressor on the chosen sectors is measured by predicted variances of the state disturbance. The approximate magnitude of these interruptions is indicated by numbers in these columns. At 10% level, “*” indicates statistical significance. An analysis of the calculated parameters' statistical significance and reliability is provided in the last two columns. Log-likelihood (LogL) and Akaike Information Criterion (AIC) are the statistics used to measure the model's ability to fit the observed data. A higher log-likelihood indicates a better match, as it indicates a higher probability of seeing the supplied data in the estimated model.

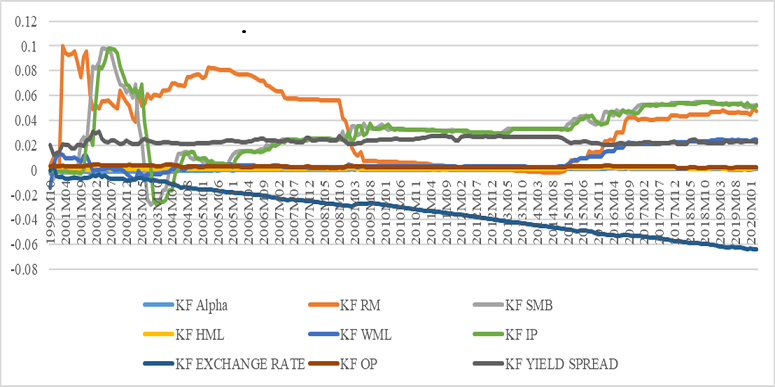

Figure 1

KF Estimates for Beverages Industry

The suggested specification, which includes a carefully chosen collection of explanatory factors, accounts for a significant amount of the variability seen in the dependent variable across the chosen sectors. The Akaike Information Criterion (AIC) was employed as a tool for model selection. AIC values are within the range 5.933-1.99, which suggests a more favourable balance between the goodness of fit of the model and its level of complexity.

The beverage industry's use of the Kalman filter to monitor variations in alpha and beta measurements is seen in Figure 1. The graph gives these shifts a visual representation, which aids in our comprehension of the fluctuations in the performance of the beverage industry and how it relates to the market as a whole. This information can give a better understanding of how the beverage industry behaves and how it's affected by the fundamental and macroeconomic factors.

Based on the findings of the estimation results, it is noteworthy that market and fundamental elements exhibit more relevance as compared to macroeconomic ones (Lan, 2020). With the exception of oil and gas, mining, and general industry sectors, it can be observed that the HML (high-minus-low) and SMB (small-minus-big) variables exhibit statistical significance, specifically at a significance level of 10%, across all sectors. This observation is consistent with other scholarly investigations that underscore the significance of these variables in elucidating stock market performance (Chen & Rancière, 2019).

In contrast to previous findings, it is evident that the term structure component serves as a systematic risk factor across all industries examined in this study. This discovery contradicts prior research that posits its restricted significance (Chen et al., 2019). The relevance of the exchange rate component is limited to the auto sector, suggesting that other variables may have a greater influence on the performance of the remaining sectors. Oil price is identified as a significant macroeconomic driver, reinforcing prior studies that emphasised its impact on sector returns.

The analysis of regime switching based multiple factor specifications reveals that the significance of market and fundamental variables is somewhat supported, although the significance of macroeconomic factors is not fully sustained. In RS specification, both the market factor and the size factor exhibit statistical significance across all 13 sectors. With the exception of certain sectors, such as drinks, personal products, and general industries, there exists a notable disparity in value-growth across all sectors, reaching statistical significance at a minimum level of 10%. In contradistinction to the preceding finding, it is noteworthy that the term structural component serves as a systematic risk factor for a total of 11 sectors. The exchange rate component exhibits a statistically significant deviation from zero only within the automotive industry. The fluctuation of oil prices emerges as the second most significant macroeconomic factor. The AIC information indicates that the alternative models provide greater explanatory power in comparison to the Kalman filter-based model, which is more flexible. The range of AIC information spans from 1.6 to 3.9, suggesting that the selected systematic risk variables account for a relatively lesser proportion of sector variance. This observation is consistent with the conclusions drawn from prior research which emphasised the inadequacies of linear factor models in comprehensively capturing the intricacies of stock returns (Chen et al., 1986).

Table 4, which shows the average errors and their related rankings across all sectors for the three specification models utilized, summarizes the mean error measurements obtained from the analysis. The betas derived using the Kalman filter demonstrate the best in-sample predicting performance in the investigated sample. The Kalman filter-based specification achieved the best results for both the evaluated error measures. This is true across all 13 sectors. When compared to the least square's alternatives, the predictive accuracy of the betas based on the Kalman filter is much higher. The average absolute inaccuracy is 5.9% to 10.4% lower across all industries. When the mean squared error criterion is considered, the benefit of the betas based on the Kalman filter becomes more obvious. The mean squared error is, on average, 14.8% less than regime switching and 21.2% less than the alternative rolling regression. These results demonstrate that as compared to the other alternative methods, the Kalman filter-based betas consistently produce more accurate in-sample forecasts. There are constantly less mean absolute errors which suggests fewer total prediction mistakes (Hepenstrick & Marcellino, 2019). Additionally, the mean squared error reductions highlight the better performance of Kalman filter-based approach and shows that it significantly enhances the accuracy of capturing the underlying dynamics of the data.

To sum up, the findings highlight how well the Kalman filter-based betas perform in producing more accurate forecasts than the alternative estimate methods in every industry.

Table 4

In-sample Estimation of MAE and MSE for all 13 Sectors

|

Sectors |

MAE |

MSE |

||||

|

Rolling |

RS |

KF |

Rolling |

RS |

KF |

|

|

Auto |

0.017 (2) |

0.017 (2) |

0.016 (1) |

0.055 (3) |

0.051 (2) |

0.047 (1) |

|

Beverages |

0.010 (2) |

0.010 (2) |

0.009 (1) |

0.021 (3) |

0.020 (2) |

0.016 (1) |

|

Chemical |

0.017 (2) |

0.017 (2) |

0.016 (1) |

0.056 (3) |

0.053 (2) |

0.050 (1) |

|

Chemical and Mining |

0.014 (1) |

0.014 (1) |

0.014 (1) |

0.031 (2) |

0.035 (3) |

0.031 (1) |

|

Electrical |

0.011 (2) |

0.011 (2) |

0.010 (1) |

0.024 (1) |

0.022 (2) |

0.020 (1) |

|

Food |

0.012 (1) |

0.011 (2) |

0.010 (1) |

0.026 (1) |

0.023 (2) |

0.019 (1) |

|

General Industries |

0.012 (1) |

0.012 (1) |

0.012 (1) |

0.031 (3) |

0.029 (2) |

0.027 (1) |

|

Minerals |

0.014 (2) |

0.013 (1) |

0.013 (1) |

0.035 (2) |

0.035 (2) |

0.038 (1) |

|

Oil and Gas |

0.010 (2) |

0.010 (2) |

0.009 (1) |

0.020 (3) |

0.019 (1) |

0.016 (2) |

|

Personal Goods |

0.015 (3) |

0.014 (2) |

0.013 (1) |

0.049 (3) |

0.042 (2) |

0.033 (1) |

|

Pharmaceutical |

0.017 (2) |

0.015 (1) |

0.015 (1) |

0.063 (3) |

0.054 (2) |

0.040 (1) |

|

Telecommunication |

0.016 (2) |

0.015 (1) |

0.015 (1) |

0.046 (3) |

0.042 (2) |

0.039 (1) |

|

Travel and Leisure |

0.017 (2) |

0.017 (2) |

0.016 (1) |

0.055 (3) |

0.050 (2) |

0.043 (1) |

Note. The estimated mean errors for three distinct multiple factor specifications are displayed in the table. The rank of a model's mean, absolute, and squared errors are shown by the values in parentheses for each sector i. The first place goes to the model with the lowest error. The estimated mean errors provide insights into the performance of the multiple factor specifications in predicting the target variable for each sector. Lower mean errors indicate better predictive accuracy and performance of the models. The relative ranking allows researchers to easily compare the models and identify the most accurate and effective specification for each sector.

Conclusion

Systematic effects on industry portfolios in Pakistan depend on certain aspects. Risk and return models often use factor models with multiple risk factors. However, only a few specifically take into account how factor sensitivities may change over time. The current empirical study uses a novel approach to cover this knowledge gap. It models the loadings on many common fundamental and macroeconomic components as individual stochastic random walk processes, which are approximated using the Kalman filter.

The main contribution of this study is its empirical analysis, which shows that how important it is to include changing factor loadings in a multifactor pricing model. This method improves the current understanding of the multifactor model's ability to predict returns in a time series setting by showing how factor sensitivity changes over time. The results have important effects. It has been identified that time-varying sensitivities have a bigger effect on the time series prediction of returns than risk analysis. This demonstrates how employing time-varying betas increases the precision of return projections and facilitates the prediction of an investment's future performance. The arguments put forth in this paper are well-supported by extensive research conducted previously.

Future Research Directions

In future research, it would be interesting to explore a multivariate approach to the previously mentioned Kalman filter-based multifactor model. This approach may effectively identify potential correlations between the analyzed series by simultaneously computing the equations for each sector. Such a study would provide a deeper understanding of the interplay between components and their loadings across different sectors. Additionally, it would offer valuable insights into the functioning of the multifactor model. Future research in this area can benefit from the insights gained through this study which shed light on the numerous factors with systematic impacts on Pakistan's industrial portfolios.

Conflict of Interest

The author of the manuscript has no financial or non-financial conflict of interest in the subject matter or materials discussed in this manuscript.

Data Availability Statement

The data associated with this study will be provided by the corresponding author upon reasonable request.

Funding Details

This research did not receive grant from any funding source or agency.

Bibliography

Al-Rjoub, S. A. (August 25, 2009). Business cycles, financial crises, and stock volatility in Jordan stock exchange.Social Science Research Network, Article e1461819. http://dx.doi.org/10.2139/ssrn.1461819

Anuno, F., Madaleno, M., & Vieira, E. (2023). Using the capital asset pricing model and the fama–french three-factor and five-factor models to manage stock and bond portfolios: Evidence from Timor-Leste.Journal of Risk and Financial Management, 16(11), Article e480. https://doi.org/10.3390/jrfm16110480

Arista, D., & Astohar, A. (2012). Analisis faktor–faktor yang mempengaruhi return saham [Analysis of factors affecting stock returns]. Jurnal Ilmu Manajemen dan Akuntansi Terapan, 3(1), 1–15.

Arouri, M., Lahiani, A., & Nguyen, D. K. (2015). World gold prices and stock returns in China: Insights from a nonlinear causality test. Economic Modelling, 44, 270–279. https://doi.org/10.1016/j.econmod.2014.10.030

Athari, S. A., Kirikkaleli, D., & Adebayo, T. S. (2023). World pandemic uncertainty and German stock market: Evidence from Markov regime-switching and Fourier based approaches. Quality & Quantity, 57(2), 1923–1936. https://doi.org/10.1007/s11135-022-01435-4

Banz, R. W. (1981). The relationship between return and market value of common stocks. Journal of Financial Economics, 9(1), 3–18. https://doi.org/10.1016/0304-405X(81)90018-0

Basu, S. (1977). Investment performance of common stocks in relation to their price-earnings ratios: A test of the efficient market hypothesis. The Journal of Finance, 32(3), 663–682. https://doi.org/10.1111/j.1540-6261.1977.tb01979.x

Benaković, D., & Posedel, P. (2010). Do macroeconomic factors matter for stock returns? Evidence from estimating a multifactor model on the Croatian market. Business Systems Research: International Journal of the Society for Advancing Innovation and Research in Economy, 1(1-2), 39–46.

Bessler, W., & Schmidt, R. H. (2022). Empirical capital market research in Germany. In W. Matiaske & D. Sadowski (Eds.), Ideengeschichte der BWL II: Produktion, OR, innovation, marketing, finanzierung, nachhaltigkeit, ÖBWL, internationales management (pp. 271–306). Springer Gabler. https://doi.org/10.1007/978-3-658-35155-711

Bhandari, L. C. (1988). Debt/equity ratio and expected common stock returns: Empirical evidence. The Journal of Finance, 43(2), 507–528. https://doi.org/10.1111/j.1540-6261.1988.tb03952.x

Bhatti, M. R., & Khan, A. A. (2022). A comparative test of multifactor asset pricing models in the dynamic regimes of financial Crisis: Evidence from emerging market regions Asia, EMEA, and Americas. Journal of Positive School Psychology, 6(5), 8985–8997.

Carhart, M. M. (1997). On persistence in mutual fund performance. The Journal of Finance, 52(1), 57–82. https://doi.org/10.1111/j.1540-6261.1997.tb03808.x

Chan, K., Chen, N. F., & Hsieh, D. A. (1991). An exploratory investigation of the firm size effect. Journal of Financial Economics, 30(2), 195–226. https://doi.org/10.1016/0304-405X(85)90008-X

Chen, J., Jiang, F., Xue, S., & Yao, J. (2019). The world predictive power of US equity market skewness risk. Journal of International Money and Finance, 96, 210–227. https://doi.org/10.1016/j.jimonfin.2019.05.003

Chen, N.-F., Roll, R., & Ross, S. A. (1986). Economic forces and the stock market. The Journal of Business, 59(3), 383–403. https://doi.org/10.1086/296344

Chen, S., & Ranciere, R. (2019). Financial information and macroeconomic forecasts. International Journal of Forecasting, 35(3), 1160–1174. https://doi.org/10.1016/j.ijforecast.2019.03.005

Cheung, Y. L., & Wong, K. T. (1992). An assessment of risk and return: Some empirical findings from the Hong Kong stock exchange. Applied Financial Economics, 2(2), 105–114. https://doi.org/10.1080/758536014

DeBondt, W. F., & Thaler, R. (1985). Does the stock market overreact? The Journal of Finance, 40(3), 793–805. https://doi.org/10.1111/j.1540-6261.1985.tb05004.x

DeBondt, W. F., & Thaler, R. (1987). Further evidence on investor overreaction and stock market seasonality. The Journal of Finance, 42(3), 557–581. https://doi.org/10.1111/j.1540-6261.1987.tb04569.x

El-Diftar, D. (2023). The impact of exchange rates on stock market performance of the Emerging 7. Journal of Capital Markets Studies, 7(2), 125–139. https://doi.org/10.1108/JCMS-03-2023-0005

Fama, E. F., & French, K. R. (1993). Common risk factors in the returns on stocks and bonds. Journal of Financial Economics, 33(1), 3–56. https://doi.org/10.1016/0304-405X(93)90023-5

Fama, E. F., & French, K. R. (1995). Size and book-to-market factors in earnings and returns. Journal of Finance, 50(1), 131–155. https://doi.org/10.1111/j.1540-6261.1995.tb05169.x

Forbes, K. J., & Warnock, F. E. (2012). Capital flow waves: Surges, stops, flight, and retrenchment. Journal of International Economics, 88(2), 235–251. https://doi.org/10.1016/j.jinteco.2012.03.006

Grundy, B. D., & Martin, J. S. M. (2001). Understanding the nature of the risks and the source of the rewards to momentum investing. The Review of Financial Studies, 14(1), 29–78. https://doi.org/10.1093/rfs/14.1.29

Gunardi, N., & Disman, M. S. (2023). The effect of money supply and interest rate on stock price. Journal of Survey in Fisheries Sciences, 10(4S), 100–111. https://doi.org/10.17762/sfs.v10i4S.659

Haq, R. (2016, October 7). Haq's musings. https://www.riazhaq.com/2016/10/china-pakistan-corridor-to-add-over-2.html

Hawaldar, I. T., Mathukutti, R., Lokesh, L., & Sarea, A. (2020). Causal nexus between the anomalies in the crude oil price and stock market. International Journal of Energy Economics and Policy, 10(3), 233–238. http://dx.doi.org/10.2139/ssrn.3556135

Hepenstrick, C., & Marcellino, M. (2019). Forecasting gross domestic product growth with large unbalanced data sets: The mixed frequency three‐pass regression filter. Journal of the Royal Statistical Society: Series A: Statistics in Society, 182(1), 69–99. https://doi.org/10.1111/rssa.12363

Hsing, Y. (2011). The stock market and macroeconomic variables in a BRICS country and policy implications. International Journal of Economics and Financial Issues, 1(1), 12–18.

Jardet, C., & Meunier, B. (2022). Nowcasting world GDP growth with high‐frequency data. Journal of Forecasting, 41(6), 1181–1200. https://doi.org/10.1002/for.2858

Jegadeesh, N. (1990). Evidence of predictable behavior of security returns. The Journal of Finance, 45(3), 881–898. https://doi.org/10.1111/j.1540-6261.1990.tb05110.x

Jegadeesh, N., & Titman, S. (1993). Returns to buying winners and selling losers: Implications for stock market efficiency. The Journal of Finance, 48(1), 65–91. https://doi.org/10.1111/j.1540-6261.1993.tb04702.x

Kones, C. M., & Kaul, G. (1996). Oil and the stock markets. The Journal of Finance, 51(2), 463–491. https://doi.org/10.1111/j.1540-6261.1996.tb02691.x

Kaczmarek, T., & Perez, K. (2022). Building portfolios based on machine learning predictions. Economic Research - Ekonomska Istraživanja, 35(1), 19–37. https://doi.org/10.1080/1331677X.2021.1875865

Khalid, R., & Shehzad, C. T. (2021). Crude oil prices, financial stability, and stock market crashes: Evidence from MENA Countries. Pakistan Journal of Commerce and Social Sciences, 15(4), 736–764.

Kostin, K. B., Runge, P., & Charifzadeh, M. (2022). An analysis and comparison of multi-factor asset pricing model performance during pandemic situations in developed and emerging markets. Mathematics, 10(1), Article e142. https://doi.org/10.3390/math10010142

Lakonishok, J., Shleifer, A., & Vishny, R. W. (1994). Contrarian investment, extrapolation, and risk. The Journal of Finance, 49(5), 1541–1578. https://doi.org/10.1111/j.1540-6261.1994.tb04772.x

Lan, C. (2020). Stock price movements: Business-cycle and low-frequency perspectives. The Review of Asset Pricing Studies, 10(2), 335–395. https://doi.org/10.1093/rapstu/raaa002

Maysami, R. C., & Koh, T. S. (2000). A vector error correction model of the Singapore stock market. International Review of Economics & Finance, 9(1), 79–96. https://doi.org/10.1016/S1059-0560(99)00042-8

Miss, S., Charifzadeh, M., & Herberger, T. A. (2020). Revisiting the monday effect: A replication study for the German stock market. Management Review Quarterly, 70(2), 257–273. https://doi.org/10.1007/s11301-019-00167-4

Mufti, F. (2016, December 30). PSX emerges as Asia's best-performing market in 2016. The Express Tribune. https://tribune.com.pk/story/1279831/year-2016-psx-emerges-asias-bestperforming-market/

Mundi, H. S. (2023). Risk neutral variances to compute expected returns using data from S&P BSE 100 firms: A replication study. Management Review Quarterly, 73(1), 215–230. https://doi.org/10.1007/s11301-021-00236-7

Natoli, F., & Venditti, F. (2022). The role of financial and macroeoconomic conditions in forecasting recession. Social Science Research Network, Article e4176581. http://dx.doi.org/10.2139/ssrn.4176581

Tursoy, T., Gunsel, N., & Rjoub, H. (2008). Macroeconomic factors, the APT and the Istanbul stock market. International Research Journal of Finance and Economics, 22(9), 49–57.

Verma, R. K., & Bansal, R. (2021). Impact of macroeconomic variables on the performance of stock exchange: A systematic review. International Journal of Emerging Markets, 16(7), 1291–1329. https://doi.org/10.1108/IJOEM-11-2019-0993

Zhu, S., Gao, J., & Sherman, M. (2020). The role of future economic conditions in the cross-section of stock returns: Evidence from the US and UK. Research in International Business and Finance, 52, Article e101193. https://doi.org/10.1016/j.ribaf.2020.101193

[1]Factors is related to firm-specific attributes like PE effect, size effect, book-to-market equity ratio and many more.