Roadmap to Sustainable Finance: A Bibliometric Analysis of Socially Responsible Investment in Financial Institutions

Zahid Bashir1*, Sabeeh Iqbal2, and Muhammad Aamir2

1Department of Commerce, University of Gujrat, Pakistan

2Hailey College of Commerce, University of the Punjab, Pakistan

Abstract

The current study aims to examine the role of Socially Responsible Investment (SRI) in Financial Institutions (FIs), as well as research gaps and future directions. A bibliometric analysis is conducted using the Elsevier Scopus database and 658 relevant documents were identified through advance searches. The current study used performance analysis and scientific mapping method to achieve the objectives. The results show that the international collaboration exists in the discipline. It includes the evidenced from the prominent journals and the names of authors with extensive co-authorship among countries, such as China, the UK, the USA, Spain, India, Italy, Germany, and France. The keyword co-occurrences shed light on the most emerging topics in this domain, such as mutual funds, sustainable development, and the factors that integrate Environment, Society, and Governance (ESG) for financial decision-making process. Additionally, the study focused to emphasize SRI in FIs between 2011 and 2023. Therefore, the emerging significant themes point towards interdisciplinary and worldwide collaboration. This study came up with its findings in the light of new perspectives not only through an in-depth analysis of SRI within FIs but also by capturing the emergence of interdisciplinary and collaborative efforts worldwide.

JEL Codes:C80, G20, O16, Q56

1. Introduction

Socially Responsible Investment (SRI) has gained importance as global concerns pertaining to Environmental, Social, and Governance (ESG) issues have grown. Financial Institutions (FIs) are leading the growing need for ethical and sustainable business practices. FIs have incorporated investment decisions pertaining to social and environmental factors which has also driven the FIs to change the money-keeping responsibilities. The research conducted on SRI is relevant for FIs to be able to align with stakeholder values, mitigate risks, support long-term performance, and promote responsible corporate activity. Therefore, it addresses the global issues in an effective way, facilitating a sustainable future. The act of including social and environmental factors in making investment decisions has changed the face of financial sector. It is encouraging for firms to reconsider their roles as custodians of financial resources. SRI research compliments stakeholder values; helps mitigate risks, supports long-term performance, and fosters responsible corporate activity which is important for FIs. This effectiveness would ensure a sustainable future at targeting and resolving global issues.

Recent researches have observed a remarkable engagement of the policymakers, the researchers, and the practitioners towards environmental issues and sustainable development, with particular attention paid to SRI for FIs (Arjalies et al., 2023; Sciarelli et al., 2021). SRI is an investment strategy that not only considers financial returns, however, also the broader social, environmental, and ethical impacts of investments (Chiapello, 2023). It can be summed up by choosing an investment that observes particular ESG criteria or moral principles. SRI strategies are aimed at bringing social and environmental change while ensuring it meets its financial objectives as well (Revelli, 2017). Moreover, SRI strategies can either involve investing in companies that highly practice ESG standards, promoting technologies for sustainability, avoiding investments in industries with adverse impacts, or exerting pressure through shareholder activism to make a positive contribution to the company's behavior (Barko et al., 2022; Crifo & Forget, 2013; Dawkins, 2018; Wagemans et al., 2013).

This research provided novel perspectives through a comprehensive analysis of SRI within the FIs, while also highlighting the emergence of interdisciplinary and worldwide collaborative efforts. Therefore, the role of SRI was examined in FIs by considering the research gaps and future directions using bibliometric analysis.

Moreover, this study followed the centrality of SRI in FIs and provided a bibliometric analysis of academic contributions to this burgeoning topic. The researcher used bibliometric tools to uncover patterns, trends, and significant themes in SRI research. The bibliometric analysis comprised influential articles, names of authors, and countries that assessed the impact of SRI on FIs. Furthermore, the study aimed to understand the main developments of SRIs' financial integration, knowledge gaps, and future opportunities through published data and collaborative networks.

Historical ethical movements led to the development of SRI in the 18th century with the Quakers who avoided morally doubtful investments (Richardson, 2013). The modern SRI movement started in 1971 following the establishment of Pax World Fund (Renneboog et al., 2008). Furthermore, the seminal academic research conducted by Moskowitz (1972) discovered the financial benefits of SRI. The UN' Principles for Responsible Investments (PRI) in 2006 took SRI to the international platform (Puaschunder, 2016). As a result of increased awareness about environmental and social issues and the relevance of ethical portfolios, SRI has become a mainstream research concern (Revelli, 2017). Presently, it is an essential leader in responsible investment policies creating a positive environmental and social impact.

Consequently, in the face of stakeholder scrutiny concerning operations that are both ethical and sustainable, SRI is increasingly relevant to all organizations and institutions (Ullah et al., 2014). Recent studies have further proved that a robust set of ESG factors strongly enhances an organization's financial performance. This would motivate an institution to add ESG factors to minimize risk and improve profitability (Moskowitz, 1972). The PRI of UN has played a vital role in promoting SRI by facilitating institutions to contribute positively toward societal and environmental objectives and seeking financial returns (Puaschunder, 2016). Furthermore, SRI enables institutions to differentiate themselves competitively through making more clients and enhancing their brand reputations (Louche & Hebb, 2014). A number of firms have already intended to adopt the required ESG disclosures and others in near future (Scholtens & Sievänen, 2013). This initiative has motivated other firms to adopt SRI as well. Adopting SRI may enable the financial institutions to demonstrate responsible investment practices, encourage long-term sustainability, and contribute to a more equitable and environmentally-conscientious global economy (Arco Castro et al., 2023; Rehman et al., 2021; Risi, 2018).

The remaining part of this study comprises three sections. The second section of the current study discusses methodology which comprises the framework applied from data collection for analysis. Significant findings in the form of highly cited articles, names of authors, journals, and countries contributed to SRI-related research, contextual to financial institutions across the world. The fourth section covers a comprehensive discussion. Lastly, the fifth section comprises conclusion.

Data and Methodology

This section includes the detail about data and information sources, selection of sample data, and some details about bibliometric analysis as a part of methodology of this study.

Data and Information Source

In this study, the primary source for bibliometric analysis is the Elsevier Scopus Database. Scopus is preferred over other databases, such as Web of Science (WOS), due to its global reputation for quality and reliability (Nobanee et al., 2021). The utilization of this particular record provides a more thorough and uniform dataset, rendering it a suitable option for performing bibliometric analysis (Tunger & Eulerich, 2018).

Selection of Sample Data/Information

Data was retrieved from Elsevier-Scopus on November 29th 2023. The current study limited its search to titles and abstracts comprising the word 'SRI' and 'FIs'. This is because the review was aimed at updating the studies representing the point of intersection of the previously mentioned two key concepts. 'SRI' is a core topic in that the study is concerned with sustainable investment practices, while 'FIs' are central in the sense that they represent those mechanisms through which such strategies are applied. These are also keywords of choice to collect the relevant literature in line with the objective of this study pertaining to the role of FIs in promoting SRI. The author first used the advance search option in Scopus to include 12 alternative phrases for "SRI" and 17 for "FIs" to maximize the search procedure (Figure 1). Finally, 3571 materials were produced as results of articles, review papers, books, and conference papers. These resources were generated from 11 subjects. Afterwards, the search term was extended into business, management, accounting, economics, econometrics, finance, and social sciences in conjunction with the environmental sciences. This produced 3238 documents. These documents covered 70% of the publications on this research domain. Thirdly, the researcher analyzed "articles" as the document type, yielding 2364 articles. Afterwards, the search was restricted to the "Top 10 ABCD" journals. It yielded 658 publications for this study's detailed bibliometric analysis. The reason for not using 'Sustainable Finance' as a keyword was that it is a broader term and might include areas outside of the specific scope of this study. This is done to gather literature that directly relates to the integration of SRI within FIs for a more congruent dataset.

Figure 1

Flow Chart of Final Sample Data for Analysis

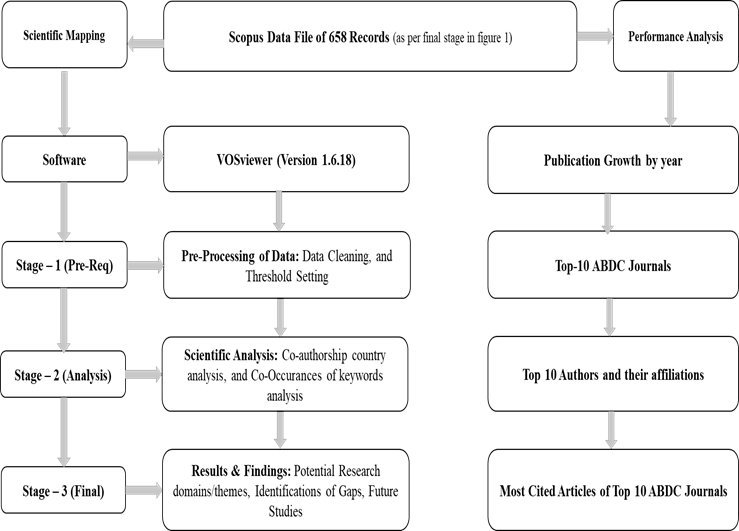

Bibliometric Analysis

Bibliometric analysis utilizes mathematical and statistical techniques to comprehend the interconnections of journal citations and to provide a concise overview of research subjects (Abdelwahab et al., 2023). Data can be acquired from citation indexes, such as Scopus and WOS which may act as data sources. The current study utilized two primary methodologies, namely performance analysis and scientific mapping, as discussed by Nobanee et al. (2021). Figure 2 indicates the overall flow of analysis (performance analysis and scientific mapping).

Figure 2

Flow Chart of Bibliometric Analysis

Results and Interpretations

Bibliometric Performance Analysis

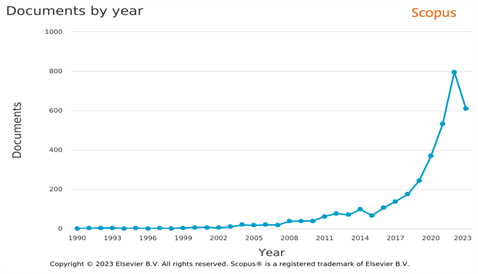

Scientific publications and citations are used to evaluate individuals, organizations, journals, and countries in bibliometric performance analysis (Nobanee et al., 2021). This method is useful in decision-making and performance comparisons. The increase in time-series analysis research papers has shown an advancement towards sustainable finance and SRI since 1990. Figure 3 shows three stages including a considerably increasing trend between 1990 and 2010, indicating a growing recognition of the subject matter. Interconnected research has increased steadily between 2011 and 2019, driven by climate change concerns. This research boom has necessitated sustainable financial practices and SRI techniques. Research activity increased between 2019 and 2023 which led to the production of 800 articles. The growing importance of sustainability and social responsibility in finance explains this research rise.

Figure 3

Yearly Publication Growth

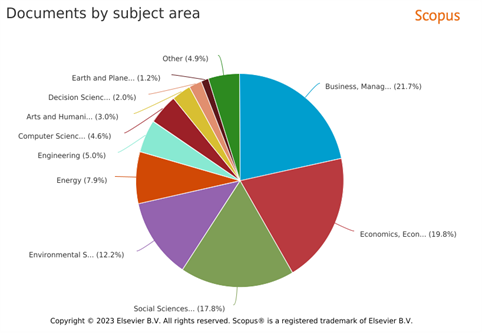

Figure 4 provides significant insights regarding the distribution of publications within the specific study domain under consideration. Data analysis indicates that scholarly articles pertaining to SRI, sustainable finance, impact investment, and other pertinent subjects are distributed throughout the 11 distinct sub-domains. In order to conduct a comprehensive analysis of the multifaceted subject matter, the researchers directed their attention on four principal domains. These domains include business, management, and accounting (21.7%); economics, econometrics, and finance (19.8%); social science (17.8%); and environmental science (12.2%). Significantly, these four domains jointly account for more than 70% of the documents within the specified research field. Therefore, it is essential to conduct a multidisciplinary analysis that encompasses various disciplines in order to achieve a thorough comprehension of the research issue.

Figure 4

Subject Distribution

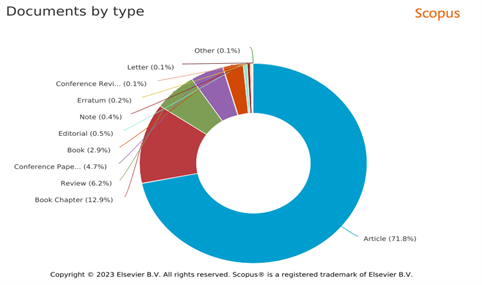

Figure 5 provides significant findings on the distribution of documents across several categories, encompassing articles (71.8%), book chapters (12.9%), reviews (6.2%), conference papers (4.7%), books (2.9%), and other forms. Considering that most of the documents within the designated research areas may be classified as articles, the researchers determined it suitable to employ the sample data to analyze the study.

Journal productivity is measured by publication count and average citations (Small, 1999). Table 1 shows that sustainable finance and SRI research are multidisciplinary, with the top 10 journals focusing on sustainability or the environment. MDPI's Sustainability Switzerland leads 2023 with 250 articles (38% of total) and a 5.8 cite score. Springer's Journal of Business Ethics has a solid cite score of 12 (14% publications). Elsevier's Journal of Cleaner Production has 61 articles (9% of total) with a cite score of 18.5. Business strategy and the environment, sustainable development, and corporate social responsibility (CSR) and environmental management have cite scores of 15.2 to 17.8, providing 5% to 6% of total publications. These periodicals demonstrate the influence of sustainable finance and SRI research.

Figure 5

Document Type

Table 1

Summary of Top 10 Journals with Total Publications and Cite Score

|

Source Title |

ABDC Category |

Number of Publications |

Cite Score (2022) |

Publisher |

|

Sustainability Switzerland |

N/A |

250/658 = 38% |

5.8 |

MDPI |

|

Journal Of Business Ethics |

A |

89/658 = 14% |

12 |

Springer |

|

Journal Of Sustainable Finance and Investment |

N/A |

74/658 = 11% |

7.4 |

Tylor & Francis |

|

Journal Of Cleaner Production |

A |

61/658 = 9% |

18.5 |

Elsevier |

|

Business Strategy and The Environment |

A |

40/658 = 6% |

17.8 |

Wiley Blackwell |

|

Sustainable Development |

C |

38/658 = 6% |

15.2 |

Wiley Blackwell |

|

Corporate Social Responsibility and Environmental Management |

C |

32/658 = 5% |

15.6 |

Wiley Blackwell |

|

Environmental Science and Pollution Research |

N/A |

32/658 = 5% |

7.9 |

Springer |

|

Finance Research Letters |

A |

23/658 = 3.5% |

10.8 |

Elsevier |

|

Sustainability Accounting Management and Policy Journal |

B |

19/658 = 3% |

7 |

Emerald |

Table 2 showcases the ten top journals together with their highly cited papers, offering unique insights into the prevailing subjects within the domains of sustainability, CSR, finance, and environmental management. Significantly, there has been a considerable scholarly interest in investigating the effects of the COVID-19 epidemic on students in higher education. This is evident by the substantial citation count of 3841 for the study published in the esteemed journal "Journal of Cleaner Production". Additional noteworthy subjects encompass ideas on CSR in the "Corporate Social Responsibility and Environmental Management" with a total of 2153 citations, as well as the "Journal of Business Ethics" with a total of 2106 citations.

Table 2

Influential Journals and their Articles

|

Journal Name |

Most Cited Article |

Time Cited |

|

Journal Of Cleaner Production |

From a literature review to a conceptual framework for sustainable supply chain management |

3841 |

|

Corporate Social Responsibility Environmental Management |

How corporate social responsibility is defined: An analysis of 37 definitions |

2153 |

|

Journal Of Business Ethics |

Corporate social responsibility theories: Mapping the territory |

2106 |

|

Business Strategy and The Environment |

Beyond the business case for corporate sustainability |

2080 |

|

Environmental Science and Pollution Research |

Eutrophication of freshwater and coastal marine ecosystems: A global problem |

1531 |

|

Sustainable Development |

Sustainable development: Mapping different approaches |

1234 |

|

Finance Research Letters |

Financial markets under the global pandemic of COVID-19 |

1163 |

|

Journal Of Sustainable Finance and Investment |

ESG and financial performance: aggregated evidence from more than 2000 empirical studies |

855 |

|

Sustainability Switzerland |

Impacts of the COVID-19 pandemic on life of higher education students: A global perspective |

803 |

|

Sustainability Accounting Management and Policy Journal |

What are the drivers of sustainability reporting? A systematic review |

208 |

Table 3 shows the rankings of ten most influential researchers in the domain of sustainable finance and SRI research, covering the time period from 1990-2023. Aibar-Guzman and Garcia-Sanchez, from Spain, have achieved prominence in their field with a total of 8 articles each in the field of sustainable finance and SRI. In close pursuit is Scholtens, from the Netherlands, who has contributed significantly with 7 publications. Additionally, Garcia-Snchez, I.M. are distinguished by their remarkable H-index of 52, which serves as a strong indicator of significant influence and acknowledgement within their respective area of research.

Bibliometric Scientific Mapping

Bibliometric scientific mapping uses statistical and mathematical methodologies to examine scientific literature, thereby uncovering research trends and identifying key authors, countries, and keywords (Abdelwahab et al., 2023; Nobanee et al., 2021; Tanwar et al., 2022; Tunger & Eulerich, 2018).

Table 3

Influential Authors

|

Rank |

Author Name |

No of Doc in SRI |

Scopus Author Id |

Year Of 1st Publication |

Total Publication |

Document H-Index |

Total Citation |

Current Affiliation |

Country |

|

1 |

Aibar-Guzman, B. |

8 |

36241172000 |

1999 |

41 |

16 |

784 |

Universidad de Santiago de Compostela,Santiago de Compostela |

Spain |

|

2 |

García-Sánchez, I.M. |

8 |

57193363767 |

2006 |

209 |

52 |

5851 |

Universidad de Salamanca, Salamanca |

Spain |

|

3 |

Scholtens, B. |

7 |

17344623500 |

1992 |

124 |

39 |

4515 |

Rijksuniversiteit Groningen, Groningen |

Netherlands |

|

4 |

Aibar-Guzmán, C. |

6 |

56819011400 |

2004 |

26 |

13 |

373 |

Universidad de Santiago de Compostela, Santiago de Compostela |

Spain |

|

5 |

Escrig-Olmedo, E. |

5 |

55450203500 |

2013 |

21 |

10 |

534 |

Universidad Jaume I, Castellon de la Plana |

Spain |

|

6 |

Weber, O. |

5 |

7004486571 |

1998 |

90 |

28 |

1850 |

University of Waterloo, Waterloo |

Canada |

|

7 |

Klein, C. |

4 |

35734464800 |

2005 |

30 |

11 |

649 |

Universität Kassel, Kassel |

Germany |

|

8 |

Moneva, J.M. |

4 |

14119993400 |

1996 |

54 |

25 |

2367 |

Universidad de Zaragoza, Zaragoza |

Spain |

|

9 |

Muñoz-Torres, M.J. |

4 |

15751052500 |

2006 |

45 |

19 |

1124 |

Universidad Jaume I, Castellon de la Plana |

Spain |

|

10 |

Orsato, R.J. |

4 |

8727661100 |

2002 |

31 |

20 |

1682 |

Università Bocconi, Milan |

Italy |

Co-author Country Analysis

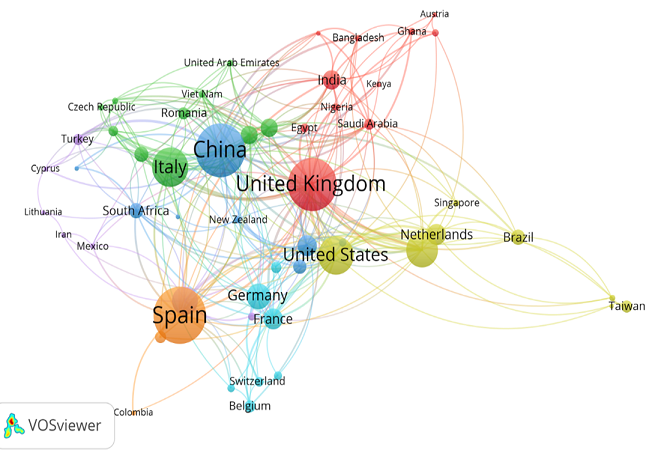

Bibliometric co-author country analysis examines global research collaboration (Fu et al., 2022). VOS viewer graphs countries' collaboration networks to show co-authorship (Gao et al., 2022; Guleria & Kaur, 2021; Shahmoradi et al., 2021). The data shows connected nations and cooperative groups. More nations with larger nodes indicate stronger co-authorship relationships in Figure 6(a). China, the UK, the USA, Spain, India, Italy, Germany, and France collaborate heavily. The author created Table 4 using VOS viewer to rank co-author countries by connections, connection strength, papers, and citations for complete analysis. This table shows detailed analysis of joint research and collaboration among significant nations in the study's topic.

Figure 6 (a)

Co-author Country Analysis (Network Visualization)

Table 4 shows nations ranked by SRI research co-authorship. China has 33 collaborations and a substantial influence (82 link strength) and has published 86 papers with 1334 citations. The UK has 32 links, 84 strength, 84 documents, and 2044 citations. The US ranks third with 26 links, 48 link strength, 56 publications, and 1660 citations. Spain has 23 links, 46 link strength, and 2391 citations from 92 sources, ranking fourth. With 19 links, 30 link strength, 23 documents, and 743 citations, India ranks sixth. Malaysia ranks sixth with 19 connections, 33 link strength, 22 documents, and 331 citations. Italy ranks sixth with 18 links, 33 link strength, 57 documents, and 1263 citations. A total of 49 documents and 1197 citations match Italy's metrics in Australia. France ranks tenth with 17 links, 32 strength, and 906 citations. Germany ranks 10th with 16 links, 19 link strength, 34 documents, and 1613 citations.

Table 4

Co-author Countries' Rankings

|

Ranks |

Countries |

Links |

Total Link Strength |

Documents |

Citations |

|

1 |

China |

33 |

82 |

86 |

1334 |

|

2 |

United Kingdom |

32 |

84 |

84 |

2044 |

|

3 |

United States |

26 |

48 |

56 |

1660 |

|

4 |

Spain |

23 |

46 |

92 |

2391 |

|

5 |

India |

19 |

30 |

23 |

743 |

|

6 |

Malaysia |

19 |

33 |

22 |

331 |

|

7 |

Italy |

18 |

33 |

57 |

1263 |

|

8 |

Australia |

18 |

33 |

49 |

1197 |

|

9 |

France |

17 |

32 |

26 |

906 |

|

10 |

Germany |

16 |

19 |

34 |

1613 |

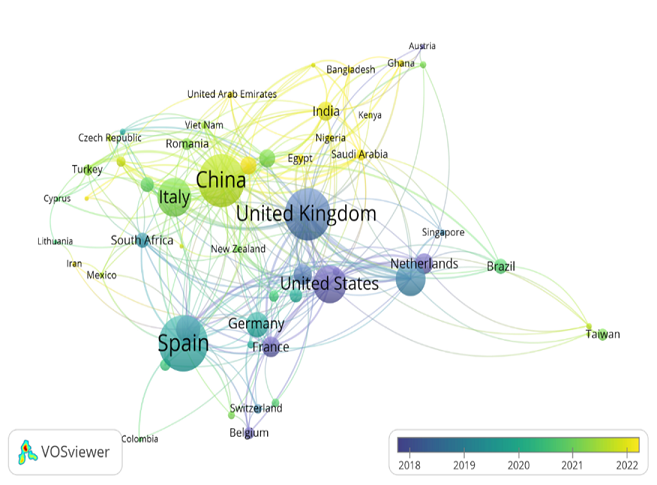

Table 4 overlays VOS viewer's bibliometric data with geographical nation representation, based on publications or citations (Huang et al., 2017; Oladinrin et al., 2023). This helps evaluate nation contributions to various scientific fields (Guleria & Kaur, 2021). In this study, co-author country analysis has been shown in Figure 6(b). The darker nodes, such as the USA, France, Belgium, Canada, the UK, and Netherlands have more citations than publications. In SRI, sustainable finance, allied topics, and lighter-colored nodes, such as Pakistan, Saudi Arabia, Egypt, Iran, Hungary, Sri Lanka, India, Bangladesh, and Ghana, suggest more collaborative research with lower citations.

Figure 6 (b)

Co-author Country Analysis (Overlay Visualization)

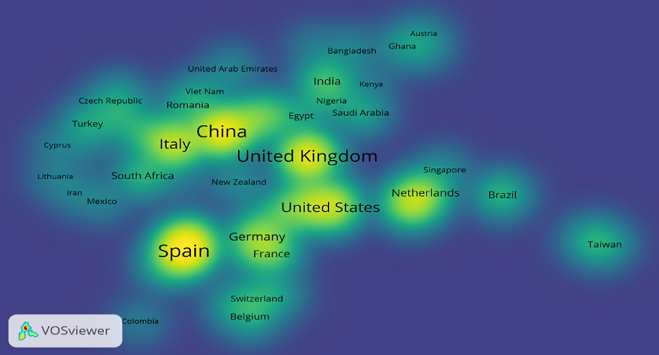

Figure 6 (c)

Co-author Country Analysis (Density Visualization)

The use of density visualization, specifically density maps, within VOS-viewer software facilitates the depiction of geographical arrangement of scientific collaboration among nations (Cobo et al., 2011; Moral-Muñoz et al., 2020). This tool facilitates the analysis of international research collaborations by identifying clusters of nations that exhibit significant levels of collaborative activities (Markscheffel & Schroter, 2021). Figure 6(c) indicates the density visualization of co-author country analysis of this study. It indicates that the countries, such as Spain, Italy, China, the UK, as well as the USA, France, Germany, and Netherlands are exhibiting a greater concentration of co-authorship on SRI and FIs.

Co-occurrences of Keyword Analysis

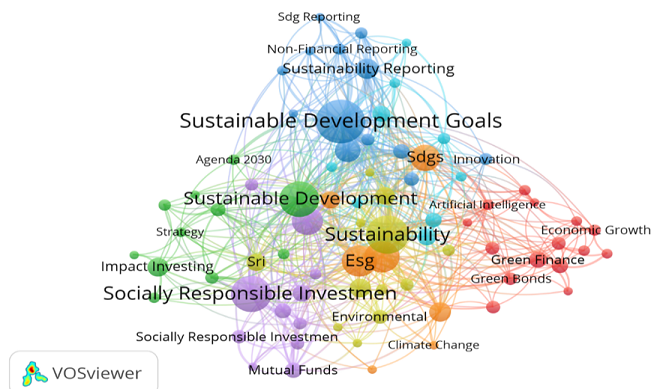

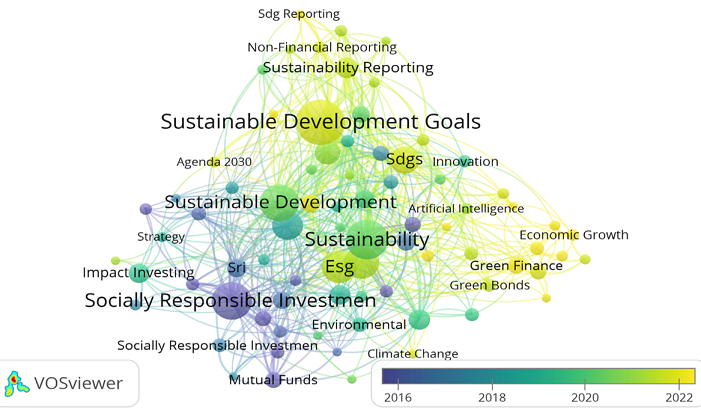

Figure 7(a) indicates top 5 nodes as per their size on the basis of co-occurrences of keywords as: SDGs, sustainability, SRI, sustainable finance, and ESG. It indicates that SDGs co-occurred 86 times with 45 other words, significantly. Additionally, sustainability co-occurred 69 times with 47 other words, significantly. Moreover, SRI co-occurred 61 times with 25 other words, significantly. The current study aimed to identify the role of SRI in FIs, therefore, it is needed to identify that how many times the SRI has co-occurred with FIs as per Scopus database.

Figure 7 (a)

Keywords Co-occurrence Analysis (Network Visualization)

The keyword co-occurrence analysis in Table 5 is noteworthy. The strongest correlation is between SRI and CSR in FIs. SRI subjects include "mutual funds," "sustainable development," "responsible investment," and "SDGs," emphasizing financial ethics and sustainability. The current study aimed to examine SRI's ESG impact, financial market impact, and performance assessment. "Impact investing", "ethical investing", "pension funds", "governance", and "environmental performance" highlight SRI's financial aspects. The report shows SRI's interaction with financial sectors, emphasizing sustainability and responsibility.

Table 5

SRI Links with other Keywords and Domains

|

Ranks |

SRI Links with |

Link Strength |

Ranks |

SRI Links with |

Link Strength |

|

1 |

CSR |

9 |

14 |

Impact Investing |

1 |

|

2 |

Mutual Funds |

6 |

15 |

Social Finance |

1 |

|

3 |

Sustainable Development |

5 |

16 |

Strategy |

1 |

|

4 |

Responsible Investment |

4 |

17 |

Institutional theory |

1 |

|

5 |

SDG |

3 |

18 |

Institutional Investors |

1 |

|

6 |

Financial Markets |

3 |

19 |

Pension funds |

1 |

|

7 |

Sustainable Investment |

3 |

20 |

Sustainability Reporting |

1 |

|

8 |

Performance Evaluation |

2 |

21 |

Governance |

1 |

|

9 |

Responsible Investing |

2 |

22 |

Corporate Sustainability |

1 |

|

10 |

Sustainability |

2 |

23 |

Environmental |

1 |

|

11 |

ESG |

2 |

24 |

Environmental Performance |

1 |

|

12 |

Fiduciary Duty |

2 |

25 |

CSR |

1 |

|

13 |

Ethical Investing |

2 |

Figure 7(b) shows darker-colored nodes with higher citations than publications for SRI, responsible investment, ethical investment, ethical investing, mutual funds, financial markets, and CSR. The lighter nodes imply lesser citations than publications for SDGs, ESG, green finance, AI, Agenda 2030, green bonds, economic growth, green innovation, financial development, and Fintech.

Figure 7 (b)

Keywords Co-occurrence Analysis (Overlay Visualization)

Figure 7 (c)

Keywords Co-occurrence Analysis (Density Visualization)

Table 6

Keywords Co-occurrence Analysis

|

Cluster & Color |

Keywords |

Links |

Total Link Strength |

Occurrences |

Cluster & Color |

Keywords |

Links |

Total Link Strength |

Occurrences |

|

1. Red |

Green Finance |

15 |

22 |

15 |

4. Yellow |

Sustainability |

47 |

109 |

69 |

|

Renewable Energy |

13 |

20 |

13 |

|

Corporate Social Responsibility |

22 |

35 |

17 |

|

|

Artificial Intelligence |

11 |

16 |

7 |

|

Sri |

20 |

29 |

17 |

|

|

Sdg |

13 |

16 |

10 |

|

Sustainable Investment |

18 |

24 |

20 |

|

|

Economic Growth |

10 |

15 |

8 |

|

Environmental |

16 |

22 |

12 |

|

|

Financial Development |

11 |

15 |

10 |

|

Socially Responsible Investing (Sri) |

9 |

14 |

9 |

|

|

Green Bonds |

11 |

14 |

10 |

|

Financial Institutions |

13 |

13 |

5 |

|

|

Emissions |

9 |

11 |

6 |

|

Corporate Social Performance |

10 |

12 |

5 |

|

|

Fintech |

10 |

11 |

5 |

|

Covid-19 Pandemic |

9 |

10 |

8 |

|

|

Financial Inclusion |

7 |

10 |

7 |

|

Risk |

7 |

7 |

7 |

|

|

Sustainable Investments |

7 |

8 |

10 |

|

Circular Economy |

6 |

6 |

5 |

|

|

Financial Literacy |

7 |

7 |

5 |

|

Performance |

4 |

4 |

5 |

|

|

Technological Innovation |

3 |

7 |

6 |

5. Purple |

Socially Responsible Investment |

29 |

75 |

61 |

|

|

Carbon Emissions |

4 |

6 |

5 |

|

Corporate Social Responsibility |

36 |

66 |

38 |

|

|

Green Innovation |

6 |

6 |

7 |

|

Ethical Investment |

18 |

31 |

13 |

|

|

2. Green |

Sustainable Development |

47 |

93 |

60 |

|

Mutual Funds |

13 |

28 |

14 |

|

Pension Funds |

20 |

29 |

11 |

|

Socially Responsible Investing |

15 |

24 |

16 |

|

|

Responsible Investment |

13 |

22 |

9 |

|

Institutional Investors |

18 |

21 |

9 |

|

|

Impact Investing |

12 |

16 |

19 |

|

Ethical Investing |

10 |

19 |

9 |

|

|

Strategy |

15 |

16 |

6 |

|

Fiduciary Duty |

11 |

16 |

9 |

|

|

Agenda 2030 |

8 |

13 |

7 |

|

Socially Responsible Investments |

10 |

14 |

11 |

|

|

Finance |

12 |

13 |

7 |

|

Financial Markets |

11 |

13 |

7 |

|

|

Responsible Investing |

8 |

11 |

8 |

|

Performance Evaluation |

7 |

11 |

5 |

|

|

Esg Investing |

8 |

9 |

5 |

6. Sky-Blue |

Corporate Social Responsibility |

18 |

29 |

16 |

|

|

Social Finance |

6 |

8 |

7 |

|

Corporate Sustainability |

15 |

22 |

15 |

|

|

Social Entrepreneurship |

3 |

4 |

5 |

|

Stakeholder Theory |

16 |

22 |

8 |

|

|

3. Blue |

Sustainable Development Goals |

45 |

123 |

86 |

|

Socially Responsible Investment (Sri) |

11 |

19 |

13 |

|

Sustainability Reporting |

23 |

49 |

22 |

|

Environment |

13 |

14 |

6 |

|

|

Sustainable Development Goals (Sdgs) |

26 |

34 |

27 |

|

Stakeholder Engagement |

12 |

13 |

6 |

|

|

Governance |

16 |

23 |

9 |

|

Gri |

9 |

12 |

6 |

|

|

Non-Financial Reporting |

15 |

21 |

8 |

|

Sustainability Performance |

10 |

12 |

6 |

|

|

2030 Agenda |

11 |

18 |

8 |

|

Legitimacy Theory |

7 |

11 |

5 |

|

|

Corporate Governance |

12 |

17 |

13 |

7. Orange |

Esg |

40 |

85 |

47 |

|

|

Sdg Compass |

9 |

17 |

5 |

|

Sdgs |

29 |

59 |

35 |

|

|

Stakeholders |

13 |

16 |

5 |

|

Sustainable Finance |

29 |

56 |

48 |

|

|

Institutional Theory |

12 |

15 |

6 |

|

Financial Performance |

19 |

34 |

21 |

|

|

Sdg Reporting |

8 |

14 |

5 |

|

Covid-19 |

13 |

26 |

17 |

|

|

Sustainable Investing |

11 |

14 |

11 |

|

Climate Change |

6 |

7 |

5 |

|

|

Innovation |

10 |

12 |

9 |

|

Environmental Performance |

5 |

5 |

5 |

Figure 7(c) shows keyword co-occurrence density. SRI, SDGs, sustainable development, sustainability, and ESG are more concentrated on sustainable finance. Mutual funds, AI, green finance, green bonds, climate change, non-financial reporting, sustainability reporting, financial innovation, impact investing, and Agenda 2030 are less concentrated in sustainable finance.

Keywords Cluster Analysis

Based on the co-occurrence analysis of author keywords as provided in Table 6, it is possible to discern the primary themes associated with the function of SRI within FIs.

Cluster-1 (Red) Green Finance and Sustainability. This cluster focuses on "green finance" and sustainable financial practices. The words emphasize environmentally-friendly investments, sustainable technologies, and financial strategy that incorporates SDGs. It indicates a growing preference for sustainable financing, renewable energy, and cutting-edge technologies to boost economic growth and address environmental challenges.

Cluster-2 (Green) Sustainable Development and Responsible Investment. This cluster emphasizes "sustainable development" and responsible investing. Moreover, it emphasizes aligning investing strategies with sustainability goals. It explores how pension funds integrate ESG issues into sustainable and responsible investing. The concepts of "Agenda 2030" and "ESG investing" emphasize sustainability and ESG concerns in investing decisions.

Cluster – 3 (Blue) SGDs and Reporting. This cluster focuses on SDGs and FIs' reporting criteria. It evaluates how financial firms integrate UN SDGs and report ESG performance. Furthermore, it explores how governance structures and institutional frameworks affect sustainability initiatives and stakeholder involvement. It suggests finance industry's transparency and responsibility to increase sustainable practices.

Cluster – 4 (Yellow) Sustainable CSR and SRI. This cluster examines sustainable CSR and SRI in FIs, focusing on ethical practices in their operations. The text focuses on "sustainable investment" and "environmental" dimensions, evaluates financial organizations' corporate social performance, and examines how the pandemic affected sustainable finance. The uncertainty of sustainable investment is addressed in relation to "risk".

Cluster -5 (Purple) Socially Responsible Investment (SRI). This cluster covers SRI, CSR, and ethical investments. The strategy emphasizes socially and ethically responsible investing. The areas of "mutual funds" and "financial markets" examine SRI in financial environments. The terms "institutional investors" and "fiduciary duty" refer to institutional investors' SRI and ethical practices. SRI performance is assessed by "performance evaluation".

Cluster - 6 (Sky-Blue) Sustainable CSR and Stakeholder Engagement. This cluster focuses on sustainability, CSR, and stakeholder engagement. "Corporate reporting," "corporate sustainability," and "stakeholder theory" explain how companies engage stakeholders and meet social and environmental goals. "SRI" invests with CSR in mind. "Stakeholder engagement" and "Global Reporting Initiative" (GRI) study sustainable reporting and stakeholder interaction for GRI. "Sustainability performance" and "legitimacy theory" evaluate firms' sustainability and credibility through responsible practices.

Cluster – 7 (Orange) Environment, Social, and Governance (ESG). This cluster examines ESG, sustainable finance, and financial performance. The key phrases include "ESG," "SDGs," and "sustainable finance," emphasizing ESG and sustainability in capital markets. "Financial performance" examines how sustainable finance affects businesses and FIs' finances. " COVID-19' explores the pandemic's impact on ESG and sustainable financing. "Climate change" and "environmental performance" discuss corporate and financial institutions' climate change strategies and ecological footprints.

The co-occurrence analysis of author keywords shows FIs' SRI themes. It emphasizes "green finance" and sustainable investments, technologies, and financial methods that incorporate sustainable development. Moreover, it emphasizes "sustainable development" and responsible investing, aligning strategies with sustainability goals and pension fund involvement. SDG integration, sustainability reporting, and governance's influence are examined. Furthermore, it emphasizes ethical inclusion, "sustainable investment," and pandemic repercussions in CSR and SRI. Likewise, it explores SRI's broad scope through "mutual funds" and "financial markets". Additionally, it emphasizes CSR, sustainability, stakeholder involvement, and "sustainability performance". Moreover, it focuses on "ESG," "SDGs," "sustainable finance", "financial performance", "COVID-19 pandemic", and "climate change". These clusters illustrate SRI's significance in financial institutions' sustainability, responsible practices, stakeholder engagement, and ESG integration.

Discussion

Bibliometric Performance Analysis

This bibliometric analysis illuminates SRI and sustainable finance research. The studies conducted during the time period (1990–2023) show climate change and finance research's relevance. A total of 11 subdomains examined SRI, sustainable finance, and impact investment, focusing on business, economics, social science, and environmental science. Especially, transdisciplinary understanding is important. Journal of Cleaner Production dominates publications and citations. Comparing prolific Spanish scholars, Aibar-Guzman and Garcia-Sanchez stand out. This analysis sheds light on sustainable finance and SRI research.

Bibliometric Scientific Mapping

The inter-country co-authorship relationships in the field of SRI within FIs. The data demonstrates a greater incidence of co-authorship relationships in countries, such as China, the UK, the USA, Spain, India, Italy, Germany, and France. These countries are ranked according to co-authorship metrics, wherein China holds the highest position in terms of link count (33) and link strength (82), followed by the UK and the USA. The findings demonstrate substantial collaboration and influence exerted by these nations in the field of SRI inside FIs. Exploring keyword co-occurrences revealed five critical nodes linking SRI, sustainability, and other pertinent words. It stressed "mutual funds," "sustainable development," and "SDGs". FIs' SRI and CSR were strongly linked. The study addresses green finance, responsible investing, SDGs, sustainability reporting, and stakeholder engagement. It emphasizes incorporating ESG factors into financial choices and evaluating sustainable finance's success. The study highlighted SRI's importance and ethical practices in financial institutions' sustainability.

Knowledge Gap

The discussion section highlighted sustainable finance and SRI research gaps. It analyzed temporal patterns, however, did not investigate the causes of these trends, indicating a need for more research. The predominance of some nations raises doubts regarding their geographical causes. Promoting multidisciplinary inquiry shows a knowledge gap in transdisciplinary issues. The publication metrics debate emphasizes the necessity to evaluate research's practical impact. Measurement frameworks for aligning investments with sustainability goals, ethical financial decision-making, and COVID-19's long-term influence on sustainable finance need to be explored.

Directions for Future Research

The current bibliometric study suggested several possible sustainable finance and SRI research directions. Understanding research trends, country collaborations, and multidisciplinary contributions are crucial. Moreover, developing stronger research impact assessments and studying ethical issues in sustainability financing are crucial. Technology, macroeconomics, and COVID-19's consequences provide valuable research insights. Assessing practical challenges to sustainable financial solutions and ethical decision-making demands detailed exploration. Addressing these gaps may help academia, industry, and policymakers comprehend sustainable finance, societal values, and economic dynamics.

Limitations

The debate highlighted many shortcomings pertaining to the study. It analyzed bibliometric data to identify sustainable finance and SRI patterns and relationships, however, it did not analyze the underlying factors, which may restrict its answers. The study did not investigate contextual factors that boost some countries' popularity. Using publication metrics and citations alone may not accurately reflect research quality and impact. Although, admitting the need for multidisciplinary inquiry, the study did not thoroughly discuss interdisciplinary collaboration problems and rewards. A confined temporal scope, reliance on a single data source possibly adding bias, absence of qualitative insights, such as interviews, and static analysis not capturing the subject's dynamic character are other drawbacks.

Conclusion

The current study aimed to investigate the role of SRI in FIs through a thorough bibliometric analysis, in accordance with the objectives of the research. The findings revealed a dynamic ecosystem in which research on SRI has undergone evolutionary changes throughout time. Discernible changes have arisen, specifically the escalating focus on climate change investigation between 2011 and 2019, indicating the increasing significance of SRI in tackling present-day difficulties. The increasing emphasis on sustainability and social responsibility in the field of finance has been observed through a notable rise in finance research from 2019-2023. The research highlighted multidisciplinary role of SRI, which encompasses several subdomains, such as business, management, economics, and environmental science. This stresses the importance of employing interdisciplinary methodologies.

Research Implications

The research gaps that have been explored have significant implications for the advancement of knowledge within the discipline. The study shed light on temporal patterns, indicating a strong necessity to delve deeper into the fundamental factors driving these changes. The examination of contextual factors that contribute to the popularity of some nations in the study of SRI is of utmost importance. This investigation revealed geographical intricacies that play an important role in their leadership. Furthermore, the study highlighted the importance of interdisciplinary inquiry, hence offering a research opportunity to explore the intricacies and obstacles of collaborative endeavors within many fields of study.

Conflict of Interest

The author of the manuscript has no financial or non-financial conflict of interest in the subject matter or materials discussed in this manuscript.

Data Availability Statement

The data associated with this study will be provided by the corresponding author upon request.

Finding details

This research did not receive grant from any funding source or agency.

Bibliography

Abdelwahab, S. I., Taha, M. M. E., Moni, S. S., & Alsayegh, A. A. (2023). Bibliometric mapping of solid lipid nanoparticles research (2012–2022) using VOSviewer. Medicine in Novel Technology and Devices, 17, Article e100217. https://doi.org/https://doi.org/10.1016/j.medntd.2023.100217

Arco Castro, M. L., Macias Guillen, A., Lopez Perez, M. V., & Rodriguez Ariza, L. (2023). The role of socially responsible investors in environmental performance: An analysis of proactive and reactive practices. Journal of Cleaner Production, 419, Article e138279. https://doi.org/https://doi.org/10.1016/j.jclepro.2023.138279

Arjalies, D.-L., Chollet, P., Crifo, P., & Mottis, N. (2023). The motivations and practices of impact assessment in socially responsible investing: The French case and its implications for the accounting and impact investing communities. Social and Environmental Accountability Journal, 43(1), 1–29. https://doi.org/10.1080/0969160X.2022.2032239

Barko, T., Cremers, M., & Renneboog, L. (2022). Shareholder engagement on environmental, social, and governance performance. Journal of Business Ethics, 180(2), 777–812. https://doi.org/10.1007/s10551-021-04850-z

Chiapello, E. (2023). Impact finance: How social and environmental questions are addressed in times of financialized capitalism. Review of Evolutionary Political Economy, 2023(2), 199–220. https://doi.org/10.1007/s43253-023-00104-y

Cobo, M. J., López-Herrera, A. G., Herrera-Viedma, E., & Herrera, F. (2011). Science mapping software tools: Review, analysis, and cooperative study among tools. Journal of the American Society for Information Science and Technology, 62(7), 1382–1402. https://doi.org/https://doi.org/10.1002/asi.21525

Crifo, P., & Forget, V. D. (2013). Think global, invest responsible: Why the private equity industry goes green. Journal of Business Ethics, 116(1), 21–48. https://doi.org/10.1007/s10551-012-1443-y

Dawkins, C. E. (2018). Elevating the role of divestment in socially responsible investing. Journal of Business Ethics, 153(2), 465–478. https://doi.org/10.1007/s10551-016-3356-7

Fu, Y. C., Marques, M., Tseng, Y.-H., Powell, J. J. W., & Baker, D. P. (2022). An evolving international research collaboration network: Spatial and thematic developments in co-authored higher education research, 1998–2018. Scientometrics, 127(3), 1403–1429. https://doi.org/10.1007/s11192-021-04200-w

Gao, J., Nyhan, J., Duke-Williams, O., & Mahony, S. (2022). Gender influences in digital humanities co-authorship networks. Journal of Documentation, 78(7), 327–350. https://doi.org/10.1108/JD-11-2021-0221

Guleria, D., & Kaur, G. (2021). Bibliometric analysis of ecopreneurship using VOSviewer and RStudio Bibliometrix, 1989–2019. Library Hi Tech, 39(4), 1001–1024. https://doi.org/10.1108/LHT-09-2020-0218

Huang, Y., Zhu, D., Lv, Q., Porter, A. L., Robinson, D. K. R., & Wang, X. (2017). Early insights on the Emerging Sources Citation Index (ESCI): An overlay map-based bibliometric study. Scientometrics, 111(3), 2041–2057. https://doi.org/10.1007/s11192-017-2349-3

Louche, C., & Hebb, T. (2014). SRI in the 21st century: Does it make a difference to society? In socially responsible investment in the 21st century: Does it make a difference for society? Emerald Group Publishing Limited. https://doi.org/10.1108/S2043-905920140000007011

Markscheffel, B., & Schröter, F. (2021). Comparison of two science mapping tools based on software technical evaluation and bibliometric case studies. COLLNET Journal of Scientometrics and Information Management, 15(2), 365–396. https://doi.org/10.1080/09737766.2021.1960220

Moral-Muñoz, J. A., Herrera-Viedma, E., Santisteban-Espejo, A., & Cobo, M. J. (2020). Software tools for conducting bibliometric analysis in science: An up-to-date review. Profesional de la información, 29(1), Article e290103. https://doi.org/10.3145/epi.2020.ene.03

Moskowitz, M. (1972). Choosing socially responsible stocks. Business Society Review, 1(1), 71–75.

Nobanee, H., Al Hamadi, F. Y., Abdulaziz, F. A., Abukarsh, L. S., Alqahtani, A. F., AlSubaey, S. K., . . . Almansoori, H. A. (2021). A bibliometric analysis of sustainability and risk management. Sustainability, 13(6), Article e3277. https://doi.org/10.3390/su13063277

Oladinrin, O. T., Arif, M., Rana, M. Q., & Gyoh, L. (2023). Interrelations between construction ethics and innovation: A bibliometric analysis using VOSviewer. Construction Innovation, 23(3), 505–523. https://doi.org/10.1108/CI-07-2021-0130

Puaschunder, J. M. (2016). On the emergence, current state, and future perspectives of Socially Responsible Investment (SRI). Consilience, 16, 38–63.

Rehman, A., Ullah, I., Afridi, F.-e.-A., Ullah, Z., Zeeshan, M., Hussain, A., & Rahman, H. U. (2021). Adoption of green banking practices and environmental performance in Pakistan: A demonstration of structural equation modelling. Environment, Development and Sustainability, 23(9), 13200–13220. https://doi.org/10.1007/s10668-020-01206-x

Renneboog, L., Ter Horst, J., & Zhang, C. (2008). Socially responsible investments: Institutional aspects, performance, and investor behavior. Journal of Banking & Finance, 32(9), 1723–1742. https://doi.org/10.1016/j.jbankfin.2007.12.039

Revelli, C. (2017). Socially responsible investing (SRI): From mainstream to margin? Research in International Business and Finance, 39, 711–717. https://doi.org/10.1016/j.ribaf.2015.11.003

Richardson, B. J. (2013). Socially responsible investing for sustainability: Overcoming its incomplete and conflicting rationales. Transnational Environmental Law, 2(2), 311–338. https://doi.org/10.1017/S2047102513000150

Risi, D. (2018). Time and business sustainability: Socially responsible investing in swiss banks and insurance companies. Business & Society, 59(7), 1410–1440. https://doi.org/10.1177/0007650318777721

Scholtens, B., & Sievänen, R. (2013). Drivers of socially responsible investing: A case study of four nordic countries. Journal of Business Ethics, 115(3), 605–616. https://doi.org/10.1007/s10551-012-1410-7

Sciarelli, M., Cosimato, S., Landi, G., & Iandolo, F. (2021). Socially responsible investment strategies for the transition towards sustainable development: The importance of integrating and communicating ESG. The TQM Journal, 33(7), 39–56. https://doi.org/10.1108/TQM-08-2020-0180

Shahmoradi, L., Ramezani, A., Atlasi, R., Namazi, N., & Larijani, B. (2021). Visualization of knowledge flow in interpersonal scientific collaboration network endocrinology and metabolism research institute. Journal of Diabetes & Metabolic Disorders, 20(1), 815–823. https://doi.org/10.1007/s40200-020-00644-8

Small, H. (1999). Visualizing science by citation mapping. Journal of the American Society for Information Science, 50(9), 799–813. https://doi.org/10.1002/(SICI)1097-4571(1999)50:9<799::AID-ASI9>3.0.CO;2-G

Tanwar, A. S., Chaudhry, H., & Srivastava, M. K. (2022). Trends in influencer marketing: A review and bibliometric analysis. Journal of Interactive Advertising, 22(1), 1–27. https://doi.org/10.1080/15252019.2021.2007822

Tunger, D., & Eulerich, M. (2018). Bibliometric analysis of corporate governance research in German-speaking countries: Applying bibliometrics to business research using a custom-made database. Scientometrics, 117(3), 2041–2059. https://doi.org/10.1007/s11192-018-2919-z

Ullah, S., Jamali, D., & Harwood, I. A. (2014). Socially responsible investment: Insights from Shari'a departments in Islamic financial institutions. Business Ethics: A European Review, 23(2), 218–233. https://doi.org/10.1111/beer.12045

Wagemans, F. A. J., Koppen, C. S. A. v., & Mol, A. P. J. (2013). The effectiveness of socially responsible investment: A review. Journal of Integrative Environmental Sciences, 10(3–4), 235–252. https://doi.org/10.1080/1943815X.2013.844169