Influence of International Standards of Internal Auditing on the Proficiency of Internal Audit Mechanism in Public Sector Universities of Pakistan

Zahid Qadeer*, Sammar Abbas, and Tanveer Ahmed

Institute of Business Studies, Kohat University, Pakistan

Abstract

The current study aims to explore how the International Standards of Internal Auditing (ISIA) impact the proficiency of Internal Audit (IA) mechanism in the public sector of Pakistan. The study targets the public sector Higher Education Institutes (HEIs) of Pakistan which are the recipients of hefty financial resources from government. A questionnaire was distributed to 250 employees working in Internal Audit and Finance Department besides the members of statutory bodies of public sector HEIs of all five provinces (stratum) across Pakistan by using the purposive sampling. One hundred and fifty (150) valid responses were received back. The Institute of Internal Auditors (IIA) has framed two broader categories of ISIA, for instance (i) Attribute Standards (IAS) (ii) Performance Standards (IPS.) By deploying SPSS version 22.0, the results of regression analysis amongst ISIA and IA mechanism reveals that in the category of attribute standards of internal auditing, 3 out of 4 standards have a significant positive impact on the proficiency of (IA) mechanism in public sector HEIs of Pakistan. While, in the category of performance standards of internal auditing; only 3 out of 6 standards have a significant positive impact on the proficiency of (IA) mechanism. The findings would be useful in strengthening the Internal Audit Functions (IAFs) in public sector of Pakistan. Policymakers are recommended to implement the international standards of internal auditing which may lead towards enhanced proficiency of IA mechanism in public sector.

1. Introduction

Public sector internal auditing consists of a comprehensive set of procedures and rules to numerate, tabulate, and identify the functions and activities in public organizations (Mattei et al., 2021). In the context of government organizations, internal audit facilitates the senior management by providing them with the independent and constant input on the soundness and accuracy of universities" financial system which makes public sector internal auditing as an obligatory function in those organizations (Christopher, 2015). These public sector entities are established as a traditional public administration or bureaucratic setup which provides services (Bednarek, 2018). Presently, internal audit has been integrated as a mandatory function in the majority of public sector organizations to make recommendations for taking corrective measures (Eltweri, 2015).

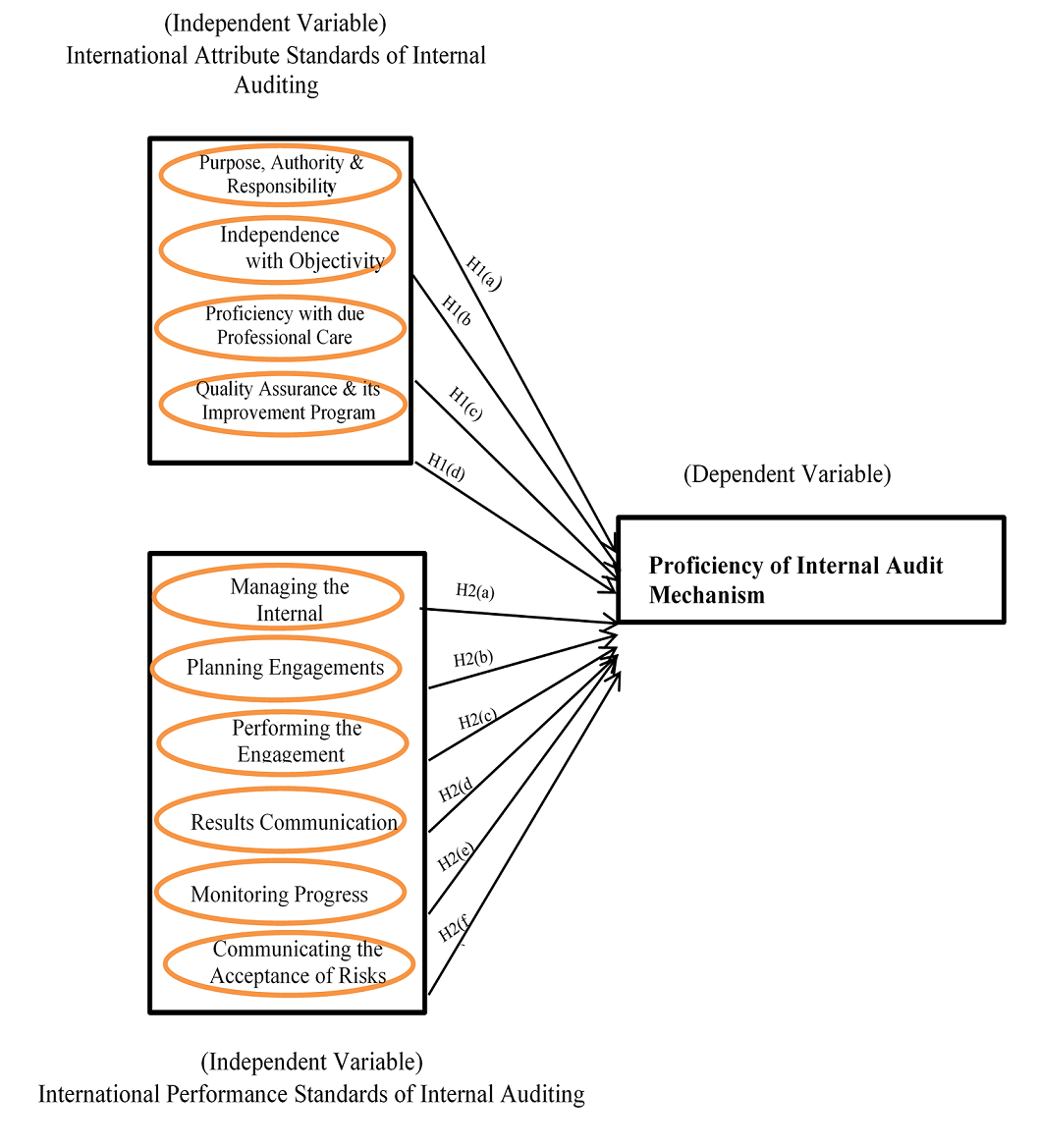

The standards for professional practicing of internal auditing, as framed by the Institute of Internal Auditing (IIA), comprise of the guiding principles which help for advancement of techniques in the field of internal auditing (Alqudah et al., 2019). These standards comprise two broader categories, for instance (a) Attribute Standards and, (b) Performance Standards. The former is more concerned with the attributes of organizations and the individual who is entrusted to perform internal auditing. Whereas, the latter deals with the nature of internal auditing activities while providing quality criteria against which the performance is determined (Institute of Internal Auditors [IIA], 2017). These standards provide comprehensive guidelines to promote and perform a broader scope of value-added services for the organization (Bailey et al., 2018).

Attribute standards are made up of 1000 series and consist of four sub-standards, that is, (i) Purpose, Authority, and Responsibility (1000), (ii) Ind pendence with Obj ctivity (1100), (iii) Profici ncy with D e Prof ssional Care (1200), and (iv) Q ality Assur nce and its Improvement Program (1300). While, Performance Standards are made-up of codes starting with series 2000 and consist of 6 sub-standards, that is, (i) Managing the Int rnal A dit Activity (2000), (ii) Pl nning Engagem nts (2200), (iii) P rforming the Engagements (2300), (iv) Res lts Communication (2400), (iv) M0nitoring Progress (2500), and (vi) C0mmunicating the Acceptance of Risks (2600) (IIA, 2017).

In public sector organizations, an effective internal control system is necessary for guidance pertaining to these standards in order to provide recommended practice consultancies and advisories, although not mandatory for all professionals of internal auditing (Marais et al., 2009). Public sector organizations are founded under a specific legal framework and enjoy the status of complete or semi-autonomy. They are founded with the aim to provide services or goods to general public on a subsidize, partial or self-financing basis, while the state contribute towards its share through budgetary support (Hassen & Altman, 2010; Poonan, 2019; Rabie & Goldman, 2014). The public sector entities play a significant role in both developing and developed countries (Organisation for Economic Co-operation and Development [OECD], 2021). Higher Education Institutes (HEIs) in both public and private sector receive federal and provincial grants for research in routine. Other stakeholders providing funds to HEIs include alumni, private donors, taxpayers, local governments, students and commercial and corporate sector, as well as patent filing and other research organizations (DeSimone & Rich, 2020).

In the last two decades, a spur growth has been witnessed in the newly established universities in public sector across the country. Keeping in view the latest legislation across Pakistan in general, while in Khyber Pakhtunkhwa (KPK) and Balochistan in particular, the mandatory role of internal audit has been given statutory cover in all public sector univeristies of these provinces between the years 2012 and 2022, respectively. Wherein, the internal audit function has replaced the traditional role of resident auditors who are mostly deputed by the government from outside the organisation. Moreover, the current study explored the prons and cones pertaining to internal audit in order to deal with the challenges and diffculties faced during the operations. Moreover, the study also attempted to plug loopholes in the field of internal auditing, particularly in the context of public sector HEIs.

The current study is significant in the context of public sector universities in Pakistan to ensure accountability, transparency, and effective governance needed to maintain trust in public sector organizations. This is because internal audit standards facilitate universities to mitigate risks and comply with relevant policies, laws, and regulations in financial management. This is crucial for public sector universities to manage their resources efficiently and to aid management for decision-making purposes. Moreover, the research is critical for the practitioners of internal auditors to make internal auditing functions more effective in order to enhance the value of money by adopting and complying with the International Standards of Internal Auditing (ISIA).

In the context of public sector, internal auditing mainly emphasizes on the compliance of rules, regulations, and the optimum utilization of public financial resources as well as to evaluate the accuracy and reliability of financial statements of organizations. According to Wiesel and Modell (2014), the public sector organizations utilize considerable taxpayer funds, therefore, a public sector auditing is more focused to determine if accounting processes were transparent, fair enough, and adhered to the law. Alazzabi et al. (2023) emphasized the need of auditing to resolve all pertinent issues which may affect the reliability of accounting records. Despite the vibrant function of internal auditing in corporate sector, many scandals in recent times have elevated apprehensions regarding risk management and effectiveness of internal audit profession (Chan et al., 2021).

The current study attempted to answer the following research questions:

- What is the impact of International Attribute Standards of internal auditing on the proficiency of IA mechanism in public sector universities of Pakistan?

- What is the impact of International Performance Standards of internal auditing on the proficiency of IA mechanism in public sector universities of Pakistan?

Literature Review

The emergence of ISIA introduced by the IIA in the last decades of twentieth century has attracted the attention of most of the practitioners and academic scholars causing a large number of publications.

Polizzi et al. (2022) recommends that the head of audit executive maintains and develops a program for quality assurance and improvement, covering both dimensions of external and internal assessments of internal audit activities; however, the findings of the study lack empirical analysis. Chambers (2014) built the conceptual framework on the procedures used which comprised meticulous preparation by experts in the field, public consultation, and revised final guidelines. Nevertheless, the conceptual framework was built on the processes followed by the parties and lacked empirical data.

Leung and Cooper (2009) conducted a study in New Zealand, Australia, and Japan. The results reported that all the countries are using international internal auditing standards with a moderately high degree. However, the majority of responders claim to be in complete compliance with the standards. It was discovered that the IIA standards fill the partial void created in public sector. Yet, the findings did not mention cultural or country-specific issues and results provided only an overview of internal audit in specific countries.

Alwan and Bougatef (2024) conducted research on Iraqi General Tax Authority to determine the relationship between international internal audit standards, comprising Attribute Standards and Performance Standards (independent variables) and the quality of tax accounting (dependent variable). The study lamented that exercising the necessary professional care, internal audit quality control has a statistical significance through its impact on the dependent variable. Though, research has been conducted on public sector entities, still no intervention of moderating variable has been employed to achieve robust results.

Christopher (2015) conducted a research to determine the relationship of internal audit activities in public banks in Turkey in terms of conformance to international standards. The results showed a significant connection among the Internal Audit Functions (IAFs) in financial institutions; however, the results were not generalized. Moreover, Shaban and Barakat (2023) claimed that in corporate sector, the majority of internal auditing standards are being met to a larger extent with a considerable focus on the maintenance of high-quality standards. This delivers results and improves the overall organizational performance; however, findings were more relevant with the corporate sector.

Alzeban and Sawan (2015) conducted research in the municipal committees of Saudia Arabia which emphasized to examine the impact of ISIA on other public sector domains, using 4 indicators for the measurement of audit committee construct. The findings showed that the audit committee's features affect internal audit compliance. Rönkkö et al. (2023) implied that the internal auditing performance evaluation systems have not advanced while the efficacy of internal auditing should significantly be refocused and broadened. Additionally, Roussy (2022) studied the Internal Audit Function (IAF) in Malaysian public sector and termed it mandatory for all the entities to prepare a summary of the internal audit activities in order to explain how internal auditing activities are discharged.

Vadasi et al. (2020) predicted that the parameters linked to internal audit professionalization are correlated with the internal audit's commitment to corporate governance and internal auditors holding professional certifications. While, empirical results showed that the internal audit professionalization impacts the internal audit effectiveness. The findings are based on secondary data and the study suggested to conduct analysis based on primary data as well. Anojan (2022) conducted a study on Sri Lankan public sector which identified that accountability and openness have a significant impact on the effectiveness of internal audit reporting and independence.

Shuwaili et al. (2023) emphasized on the interaction between internal and external auditors, giving internal auditors authority by providing them with specialized human resources, management support, bolstering organizational culture, giving technological resources, and creating audit plans. The research focused to assess the effectiveness of internal auditing in the public sector of Iraq. Secondly, the sample size of the study was relatively small, examining internal audit effectiveness. Lenz and O"Regan (2024) reiterates that the elusive epistemology of internal auditing does not merely mean that the international standards of internal audit have no systematic foundations, rather just an activity for the accumulation of concepts or an inventory of theories for body of knowledge.

Van Gils (2012) accomplished the findings in tertiary education sector of USA. The study stated that IAFs are comparatively less mature as compared to publicly listed trading firms, however, the IAF construct was measured with limited indicators. Mihret and Yismaw (2007) conducted a study on IAFs in the higher educational sector of Ethiopia. The study described the support of top management as one of the most important elements affecting internal audit quality. The existing theories and recent extent of literature rely on the development and testing of hypothesis as well as explaining the relationship among different constructs. These constructs include ISIA in relation with the proficiency of IA mechanism in a holistic manner.

Figure 1

Theoretical Framework

Methodology

The mandatory statutory role of internal audit exists in 54 public sector universities across Pakistan by virtue of the legislation by the respective provincial assemblies which have been carefully identified by exploring and checking the promulgated assemblies Act and ordinances. These include 32 universities from Khyber Pakhtunkhwa province, 11 from Balochistan province, 4 from Punjab province, 2 public sector universities from Sindh province while only 01 from Gilgit Baltistan wherein the mandatory function of Internal Audit exists. The detail is given in Table 1:

Table 1

Detail of Participants within Public Sector HEIs

|

S# |

Provinces |

Selected universities based on the mandatory role of IA |

Sample drawn |

|

1 |

Khyber Pakhtunkhwa |

32 |

32 x 2 = 64 |

|

2 |

Balochistan |

11 |

11 x 4 = 44 |

|

3 |

Punjab |

4 |

4 x 6 = 24 |

|

4 |

Sindh |

2 |

2 x 6 = 12 |

|

5 |

Gilgit Baltistan |

1 |

1 x 6 = 6 |

|

Total |

54 |

150 |

For this purpose, purposive sampling technique was used for collection of data from the relevant stakeholders of finance and audit personnel as well as members of statutory body within public sector universities of Pakistan. Total 250 questionnaires were distributed by means of Google forms and in-person efforts while 150 valid responses (60%) were received from the 54 selected public sector universities across all provinces of Pakistan. These details have been presented in Table 2. Job experience of the study experience has been presented in table 3. A 5-point Likert scale questionnaire was adapted based on the existing literature review. According to Invernizzi and Parrinello (2020), approximately, 30-200 sample size is regarded sufficient where the attribute is present in sub-groups.

Table 2

Participants Belonging to Different Deptartments/Sections in Public Sector HEIs

|

S# |

Groups |

Frequency |

Percent |

|

1 |

Finance Section |

99 |

66 |

|

2 |

Internal Audit Section |

33 |

22 |

|

3 |

Statutory bodies" Members |

18 |

12 |

|

|

Total |

150 |

100 |

Table 3

Job Experiences of Employees in Public Sector Universities

|

S# |

Experience of Respondents |

Frequency |

Percent |

|

1 |

Less than 5 years |

24 |

16 |

|

2 |

5 years > but < 10 years |

46 |

31 |

|

3 |

10 years > but < 15 years |

52 |

35 |

|

4 |

15 years > but < 20 years |

22 |

15 |

|

5 |

< 20 years |

06 |

03 |

|

Total |

150 |

100 |

Model Specifications

In order to test the research hypothesis, the model is formulated by following equation:

IA = 𝛽0+ 𝛽1PAR +𝛽2 IO+𝛽3PPC+𝛽4QAIP+𝛽5MIAA+𝛽6PLE+𝛽7PE +𝛽8RC+ 𝛽9MP+𝛽10CAR + 𝜀

Table 4

Description of Variables

|

S# |

Variables |

Measures |

Reference/Source |

|

1. |

Purpose, authority and responsibility |

The purpose and authority of the internal audit along with responsibility defined in financial charter |

(Mahzan et al., 2012) |

|

Independence with objectivity |

The internal audit function must be independent |

(Stewart & Subramaniam, 2010) |

|

|

Proficiency with due professional care |

Internal auditors should have knowledge, skills, and proficiency in terms of qualification |

(Yazid & Wiyantoro, 2018) |

|

|

Quality assurance and improvement program |

On-going evaluation and monitoring of performance for the routine internal audit activity |

(Polizzi et al., 2022) |

|

|

2. |

Managing the internal audit activities. |

Emerging tendencies and issues in the organization |

(Asare, 2009) |

|

Planning engagements |

The defined priorities of the internal audit activity |

(Coetzee & Lubbe, 2013) |

|

|

Performing the engagement |

Plan for audit engagements, its scope, timings, and allocated resources |

(Vallabhaneni, 2005) |

|

|

Results communication |

Communication should be clear, accurate, concise, complete, timely, and constructive |

(Farkas et al., 2019) |

|

|

Monitoring progress |

Follow-up mechanism for effective implementation |

(Dascalu et al., 2016) |

|

|

Communicating the acceptance of risks |

Internal auditor must discuss the risk level with senior management |

(Calvin, 2021). |

|

|

3 |

Audit committee |

Size of committee |

(Aryan, 2015) |

|

Frequency of meetings |

(Rashid et al., 2021) |

||

|

Independence |

(Zaman & Sarens, 2013) |

||

|

Tenure of members |

(Nipper, 2021) |

||

|

Experience |

(He et al., 2017) |

||

|

4 |

Proficiency of internal audit mechanism |

Internal audit report |

(Izedonmi & Olateru-Olagbegi, 2021) |

|

Management support |

(Asaolu et al., 2016) |

||

|

Regulatory requirement |

(Horvat & Zvorc, 2017) |

||

|

Internal control system |

(Chang et al., 2019) |

||

|

Liaison with external auditor |

(Yusof et al., 2018) |

||

|

Risk management |

(Shakeel et al., 2020) |

Testing Assumptions of Regression Analysis

There are a few certain assumptions related to study variables (Osborne & Waters, 2019). The testing of these basic assumptions of regression analysis is a practice in a systems framework which provides a comprehensive plan and guidelines step-by-step to determine the optimal statistical model for a certain dataset (Flatt & Jacobs, 2019). These are discussed and elaborated one by one as follows:

In the current study, variables were tested to determine the normality using Kolmogorov-Smirnov and Shapiro-Wilk test in SPSS 22.0 and transformed the variables into normal before performing regression. All p-value > 0.05, so the null hypothesis was accepted that it is a normal distribution for all variables in the model.

According to Alin (2010), where two or more predictors are considerably correlated with each other or when it is possible to forecast one variable with the help of another predictor, then this situation is called "multicollinearity". Resultantly, regression model findings generate skewness due to duplicate information. The results given in Table 5 show that the value of VIF for each predictor is less than 10. Hence, no multicollinearity exists in dataset.

Table 5

Multicollinearity

|

S# |

Model |

VIF |

|

|

(Constant) |

|

|

1 |

PAR |

2.551 |

|

2 |

IO |

2.102 |

|

3 |

PPC |

3.104 |

|

4 |

QAIP |

3.050 |

|

5 |

MIAA |

2.140 |

|

6 |

PLE |

2.520 |

|

7 |

PE |

2.145 |

|

8 |

RC |

3.025 |

|

9 |

MP |

3.015 |

|

10 |

CAR |

2.094 |

Note. PAR=purpose, authority and responsibility; IO= Independence and Objectivity; PPC= Proficiency and due professional care; QAIP= Quality assurance and its improvement programme; MIAA= Managing the internal audit activity; PLE= Planning engagements; PE= Performing engagements; RC= Results communication; MP= Monitoring progress CAR= Communicating the acceptance risk

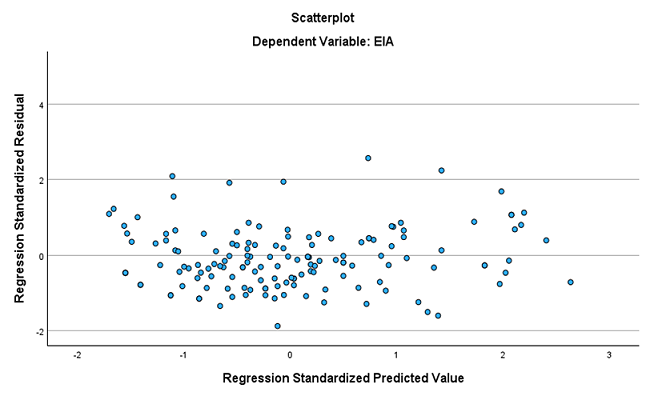

In regression analysis, the uneven spread of residuals or error terms is called heteroscedasticity. In heteroscedasticity, the residuals" distribution remains uneven throughout the wide range of measured values and reflects a systematic change. Figure 2 shows a graphical method approach and non-cone shaped data. Hence, no heteroscedasticity problem exists in the data.

Figure 2

Regression Standardized Predicted Value

Results and Discussion

The descriptive data in Table 2 reveals key characteristics of respondents of the survey carried out in public sector universities of Pakistan. Majority of the respondents belonged to finance section (66%), thereafter personnel from internal audit sections (22%). While, the rest of respondents (12%) were members of statutory bodies in public sector universities including Vice Chancellor, Registrar, Director Planning, Director Works, and Provost. Data was also segregated based on working experiences of employees in public sector universities of Pakistan, summarized in Table 3.

Regression Analysis and Hypotheses Testing

SPSS version 22.0 was used for regression anylasis for the testing of ten hypothesis. Table 6 shows impact of ISIA on the proficiency of Internal Audit (IA) mechanism in public sector universities of Pakistan. These standards belong to two broader categories of ISIA (i) Attribute Standards (ii) Performance Standards. The results of each hypothesis are tabulated as follows:

Table 6

Regression Results

|

Hypotheses |

Relationship |

Beta |

S.E |

t |

p |

Decision |

Rankede |

|

H1(a) |

PAR---> IA |

.035 |

.078 |

.442 |

.658 |

Rejected |

4 |

|

H1(b) |

IO--->IA |

.227 |

.068 |

3.343 |

.000 |

Supported |

2 |

|

H1(c) |

PPC--->IA |

.178 |

.058 |

3.055 |

.002 |

Supported |

3 |

|

H1(d) |

QAIP--->IA |

.304 |

.053 |

5.785 |

.000 |

Supported |

1 |

|

H2(a) |

MIAA--->IA |

.194 |

.080 |

2.422 |

.015 |

Supported |

3 |

|

H2(b) |

PLE--->IA |

.031 |

.060 |

.509 |

.611 |

Rejected |

5 |

|

H2(c) |

PE--->IA |

.303 |

.093 |

3.268 |

.001 |

Supported |

1 |

|

H2(d) |

RC--->IA |

.085 |

.089 |

.951 |

.342 |

Rejected |

4 |

|

H2(e) |

MP--->IA |

.196 |

.081 |

2.411 |

.016 |

Supported |

2 |

|

H2(f) |

CAR--->IA |

-.001 |

.076 |

-.007 |

.995 |

Rejected |

6 |

Note. PAR=purpose, authority and responsibility; IO= Independence and Objectivity; PPC= Proficiency and due professional care; QAIP= Quality assurance and its improvement programme; MIAA= Managing the internal audit activity; PLE= Planning engagements; PE= Performing engagements; RC= Results communication; MP= Monitoring progress CAR= Communicating the acceptance risk

International Attribute Standards of Internal Auditing and Proficiency of IA Mechanism

The IIA has exclusively designed the internal auditing standards to provide guidelines and to lay down the conceptual framework for performing and promoting internal auditing activities. One of the broader category, that is, International Attribute Standards of internal auditing address the attributes of an organization and individual, performing the function of internal auditing. These Attribute Standards start with the series of 1000, and comprise four sub-standards namely Purpose, A thority and Responsibility (1000), Ind pendence with Obj ctivity (1100), Profici ncy with D e Prof ssional Care (1200), and Q ality Assur nce and its Improvement Program (1300).

According to results mentioned in Table-6, the first hypotheses H1(a), was rejected that the Purpose, Authority and Responsibility (1000) standard has no impact on the proficiency of IA mechanism in public sector universities. Mahzan et al. (2012) argued that IAF is struggling to maintain its purpose and identity as the organizations undergo drastic changes. These constant changes evolve spanning from risk, control, and reviewing governance. The results postulated that boards and policymakers should have effective legistation for existing as well as new public sector HEIs to have a strong role of internal auditing. Moreover, its mandatory role should be governed by legal status of each HEIs.

The hypotheses H1(b) confirm significant impact between Independence and Objectivity (1100) Standard on the proficiency of IA mechanism in public sector universities. The current study aligns with the results of the previous study conducted by Sawan (2013) which described that the independence and objectivity are paramount to internal auditing. This implies that the Department of Internal Audit should have direct access to senior management and board while imposing strict conditions on the appointment and removal of the head of internal audit.

The hypotheses H1(c) also confirmed significant impact between Proficiency with Due Professional Care (1200) Standard on the capability of IA mechanism in public sector universities. The results are supportive in the findings by Marwa (2023) that the variables of competence, due professional care, and integrity significantly affect the audit quality, leading towards effective functions of internal auditing in public sector. The findings urge that public sector entities should comply with the guidelines of IIA to the maximum for best internal audit practices.

The hypotheses H1(d) proved a significant impact between Quality Assurance and its Improvement Program (1300) Standard on the proficiency of IA mechanism in public sector universities. Ali and Ali (2022) statistically tested and emphasized the significant association between internal control quality and internal auditing. Moreover, most of the previous findings are consistent with the results of current study. This supports that the function of assurance, compliance mechanisms, and financial audits are typical responsibilities of IAF which involves the supervision and improvement of risk management processes.

International Performance Standards of Internal Auditing and Proficiency of IA Mechanism

Another category of ISIA, as described by the IIA, is Performance Standards. These standards deal with the nature of internal auditing and lay down the quality criteria against which the performance of internal auditing is determined. The Performance Standards are made-up of code starting with series 2000. These standards consist of 6 sub-standards, for instance Managing the Int rnal A dit Activity (2000), Pl nning Engagem nts (2200), P rforming the Engagement (2300), Res lts Communication (2400), M0nitoring Progress (2500), and C0mmunicating the Acceptance of Risks (2600). The relevant results of each hypotheses pertaining to Performance Standards are discussed as follows:

The findings mentioned in Table 6 confirm the significant positive effect of Managing Internal Audit Activity (2000) Standard on the proficiency of IA mechanism in public sector HEIs in Pakistan. Hence, the hypotheses H2(a) is accepted. The findings are supported by findings of Hegazy and Farghaly (2021). They stated that “managing internal audit activity” standard demands the chief internal auditor to effectively manage the audit activity while ensuring that it contributes to the value addition for the organization to enhance the effectiveness and efficiency of governance processes as well as providing relevant assurance services.

The hypotheses H2(b) did not confirm the results that Planning Engagements (2200) Standards effect the proficiency of IA mechanism. Horvat and Zvorc (2017) advocated that due to lack of financial planning and checking its adherence to these plans, it does not have a substantial impact on the organizational performance of internal auditors in larger entities.

The hypotheses H2(c) testify the findings that Performing Engagements (2300) positively affect the proficiency of IA mechanism. Cular et al. (2020) also confirmed the positive relationship between audit engagement duration for the promotion of effective internal as well as external audit activities in entities with lower auditing compensation, especially at the initial phase of a business when it is hard to have profitability at this stage.

The results of the current study align with the hypothesis H2(d) that Results Communications (2400) Standards do not have any impact on the effectiveness of IAFs. This shows alignment with a study conducted by Abdullah et al. (2018) that the degree of cooperation and coordination amongst stakeholders, for instance auditee, internal auditors, management, and external auditors in organizations is not up to the satisfactory level.

The results obtained from the analysis indicate that the hypotheses H2(e) was accepted, that is, Monitoring Progress (2500) Standards have a positive and significant impact on the proficiency of IA mechanism in public sector HEIs. This argument is supported by Tang et al. (2017) that continuous monitoring process in real-time risk identification may support fraud detection and improve internal control effectiveness.

The hypotheses H2(f) do not confirm the results that Communicating the Acceptance of Risks (2600) Standards impact the proficiency of IA mechanism. These results are also in line with the existing literature. Rensberg and Coetzee (2016) also measured the perception about the risk management in governance structure and rejected the study hypothesis that there is any contribution of the IAF to risk management activities. The results are according to the expectation that high levels of non-compliance in respect of Communicating the Acceptance of Risks Standards (2600) lead towards ineffective IA mechanism.

Conclusion

The current study aimed to determine the influence of International Standards of Internal Auditing on the proficiency of IA mechanism in public sector universities of Pakistan. In the context of HEIs of Pakistan, wherein the mandatory function of internal auditor exists by vurture of the legal provision promulgated through Ordinance/Acts of respective universities passed by provincial asemblies. Similar to other public sector entities, the function of internal audit has widely been recognised to be pivotal, however, the research gap exists in HEIs in the previous literature.

The existing theories along with the recent extent of literature rely upon the development and testing of ten hypotheses. The current study initially tested the developed theoretical framework and explained the relationship among different constructs, for instance ISIA in relation with the ISIA in a holistic manner.

To achieve the objective, the hypotheses were tested to justify them empirically by employing SPSS version 22.0. The data for the current study was gathered using mixed multiple techniques, that is, self-administrated, internet-based, and telephonic-based survey.

The current study stipulated evidence to accept H1(b), H1(c), and H1(d) in the broader category of International Attribute Standards of internal auditing. Moreover, it also ranked them as 2, 3, and 1 in terms of their impact on the dependent variable, that is, Proficiency of IA mechanism in public sector universities of Pakistan as shown in Table 6. Additionally, the results in Table 6 also show that H2(a), H2(c), and H2(e) were accepted that these standards of Performance category of internal audit impact the proficiency of IA mechanism and ranked them as 3, 1, and 2 in terms of their strength of impact.

Theoretical and Managerial Implications

The current study contributed by developing a holistic model to measure the proficiency of IA mechanism in the context of public sector universities of Pakistan. Moreover, sub-standards encompassing the broader categories of both Attribute Standards as well as Performance Standards of ISIA were tested distinctively, showing its impact on the proficiency of internal audit. This study also identified those public sector universities across Pakistan wherein the function of internal audit exists by virtue of legislation.

The current study offered critical managerial implications for practitioners of internal auditors, top management as well as policymakers of public sector in general, and board of trustees (syndicate, senate, and other statutory bodies) in particular to make the internal auditing functions more effective. It would enhance the value of money by adopting and complying with the ISIA for improved finanial management and governance. Moreover, this study also provided legislatures of other provinces to gain deeper insights and to introduce afresh legislations in their respective provinces. This would make the role of internal auditing mandatory by relying less on the traditional role of resident auditors of the government. Additionally, this study also highlighted the periodical professional training opportunities to reshape the IAFs within public sector HEIs to cope with the new challenges and to meet the demands of the profession.

Despite handful results and insights, the current research still has some limitations. This study included only a few relavent stakeholders of public sector HEIs. Future studies should include other employees within the universities. Furthermore, future studies should also include private HEIs as well. Moreover, a comparative study is also recommended under this domain. The model developed and tested in the current study was holistic and the same may be tested in the corporate sector setting as well. The model may also be tested by adding some moderating or mediating variable(s).

Conflict of Interest

The author of the manuscript has no financial or non-financial conflict of interest in the subject matter or materials discussed in this manuscript.

Data Availability Statement

The data associated with this study will be provided by the corresponding author upon request.

FUNDING DETAILS

This research did not receive grant from any funding source or agency.

Bibliography

Abdullah, R., Ismail, Z., & Smith, M. (2018). Audit committees' involvement and the effects of quality in the internal audit function on corporate governance.International Journal of Auditing,22(3), 385–403. https://doi.org/10.1111/ijau.12124

Ali, S. I., & Ali, A. (2022). Internal auditing practices and internal control quality in state-owned enterprises: Evidence from Pakistan. Sarhad Journal of Management Sciences, 8(2), 139–162.

Alin, A. (2010). Multicollinearity. Wiley Interdisciplinary Reviews: Computational Statistics, 2(3), 370–374. https://doi.org/10.1002/wics.84

Alazzabi, W. Y. E., Mustafa, H., & Karage, A. I. (2023). Risk management, top management support, internal audit activities and fraud mitigation. Journal of Financial Crime, 30(2), 569–582. https://doi.org/10.1108/JFC-11-2019-0147

Alqudah, H. M., Amran, N. A., & Hassan, H. (2019). Factors affecting the internal auditors" effectiveness in the Jordanian public sector: The moderating effect of task complexity. EuroMed Journal of Business, 14(3), 251–273. https://doi.org/10.1108/EMJB-03-2019-0049

Alzeban, A., & Sawan, N. (2015). The impact of audit committee characteristics on the implementation of internal audit recommendations. Journal of International Accounting, Auditing and Taxation, 24, 61–71. https://doi.org/10.1016/j.intaccaudtax.2015.02.005

Anojan, V. (2022). Factors affecting internal audit reporting on public sector in Sri Lanka, Journal of Accounting and Business Education, 6 (2), 22–33. http://dx.doi.org/10.26675/jabe.v6i2.21265

Alwan, A. H., & Bougatef, K. (2024). The quality of tax accounting in accordance with international internal auditing standards: The case of Iraq. Tec Empresarial, 19(1), 29–48.

Aryan, L. A. (2015). The relationship between audit committee characteristics, audit 153 firm quality and companies" profitability. Asian Journal of Finance & Accounting, 7(2), 215–226. http://dx.doi.org/10.5296/ajfa.v7i2.8530

Asare, T. (2009). Internal auditing in the public sector: Promoting good governance and performance improvement. International Journal on Governmental Financial Management, 9(1), 15–28.

Asaolu, T. O., Adedokun, S. A., & Monday, J. U. (2016). Promoting good governance through internal audit function (IAF): The Nigerian experience. International Business Research, 9(5), 196–204. http://dx.doi.org/10.5539/ibr.v9n5p196

Bailey, C., Collins, D. L., & Abbott, L. J. (2018). The impact of enterprise risk management on the audit process: Evidence from audit fees and audit delay. Auditing: A Journal of Practice & Theory, 37(3), 25–46. http://dx.doi.org/10.2308/ajpt-51900

Bednarek, P. (2018). Factors affecting the internal audit effectiveness: A survey of the Polish private and public sectors. In Efficiency in Business and Economics: Proceedings from the 7th International Conference on Efficiency as a Source of the Wealth of Nations (ESWN), Wrocław 2017 (pp. 1-16). Springer International Publishing.

Calvin, C. G. (2021). Adherence to the internal audit core principles and threats to internal audit function effectiveness. Auditing: A Journal of Practice & Theory, 40(4), 79–98. https://doi.org/10.2308/AJPT-19-072

Christopher, J. (2015). The adoption of internal audit as a governance control mechanism in Australian public universities: Views from the CEOs. Journal of Higher Education Policy and Management, 34(5), 529–541. https://doi.org/10.1080/1360080X.2012.716001

Chan, K. C., Chen, Y., & Liu, B. (2021). The linear and non-linear effects of internal control and its five components on corporate innovation: Evidence from Chinese firms using the COSO framework. European Accounting Review, 30(4), 733–765. https://doi.org/10.1080/09638180.2020.1776626

Chang, Y. T., Chen, H., Cheng, R. K., & Chi, W. (2019). The impact of internal audit attributes on the effectiveness of internal control over operations and compliance. Journal of Contemporary Accounting & Economics, 15(1), 1–19. https://doi.org/10.1016/j.jcae.2018.11.002

Coetzee, P., & Lubbe, D. (2013). The use of risk management principles in planning an internal audit engagement. Southern African Business Review, 17(2), 113–139.

Cular, M., Slapničar, S., & Vuko, T. (2020). The effect of internal auditors" engagement in risk management consulting on external auditors" reliance decision. European Accounting Review, 29(5), 999–1020. https://doi.org/10.1080/09638180.2020.1723667

Chambers, D. A. (2014). New guidance on internal audit: An analysis and appraisal of recent developments. Managerial Auditing Journal, 29(2), 196–218. https://doi.org/10.1108/MAJ-08-2013-0925

Dascalu, E. D., Marcu, N., & Hurjui, I. (2016). Performance management and monitoring of internal audit for the public sector in Romania. Amfiteatru Economic Journal, 18(43), 691–705.

DeSimone, S., & Rich, K. (2020). Determinants and consequences of internal audit functions within colleges and universities. Managerial Auditing Journal, 35(8), 1143–1166. https://doi.org/10.1108/MAJ-10-2019-2444

Eltweri, A. M. E. H. (2015). An investigation into the auditing profession regulatory framework and the factors influencing the adoption of ISAs in the Libyan context. Liverpool John Moores University.

Farkas, M., Hirsch, R., & Kokina, J. (2019). Internal auditor communications: An experimental investigation of managerial perceptions. Managerial Auditing Journal, 34(4), 462–485. https://doi.org/10.1108/MAJ-06-2018-1910

Flatt, C., & Jacobs, R. L. (2019). Principle assumptions of regression analysis: Testing, techniques, and statistical reporting of imperfect data sets. Advances in Developing Human Resources, 21(4), 484–502. https://doi.org/10.1177/1523422319869915

Mattei, G., Grossi, G., & Guthrie AM, J. (2021). Exploring past, present and future trends in public sector auditing research: A literature review. Meditari Accountancy Research, 29(7), 94–134.

Mihret, D. G, & Yismaw, A. W. (2007). Internal audit effectiveness: An Ethiopian public sector case study. Managerial Auditing Journal, 22(5), 470–484. https://doi.org/10.1108/02686900710750757

Hassen, E. K., & Altman, M. (January, 2010). Public service employment and job creation in South Africa. Centre for Employment, Poverty and Growth, HSRC. https://miriamaltman.com/wp-content/uploads/2016/09/GOV_EMP031_HassenAltman_public_service_employment_scenarios_jan10.pdf

He, X., Pittman, J. A., Rui, O. M., & Wu, D. (2017). Do social ties between external auditors and audit committee members affect audit quality? The Accounting Review, 92(5), 61–87. https://doi.org/10.2308/accr-51696

Hegazy, M., & Farghaly, M. (2021). External and internal auditors" perceptions on compliance with internal audit standards and practices: Spirit versus letters. Corporate Ownership & Control, 18(3), 31–45. https://doi.org/10.22495/cocv18i3art3

Horvat, T., & Zvorc, B. (2017, May 24–27). The impact of internal auditing on financial planning in public educational institutions [Paper presentation]. Management of International Conference, Venice, Italy.

Institute of Internal Auditors. (2017, January 1). International standards for the professional practice of internal auditing (standards). https://www.theiia.org/en/content/guidance/mandatory/standards/international-standards-for-the-professional-practice-of-internal-auditing/

Invernizzi, M., & Parrinello, M. (2022). Exploration vs convergence speed in adaptive-bias enhanced sampling. Journal of Chemical Theory and Computation, 18(6), 3988–3996. https://doi.org/10.1021/acs.jctc.2c00152

Izedonmi, F. I. O., & Olateru-Olagbegi, A. (2021). Internal audit quality and public sector management in Nigeria. European Journal of Social Sciences Studies, 6(5), 10–33. https://doi.org/10.46827/ejsss.v6i5.1101

Janse van Rensburg, J. O., & Coetzee, P. (2016). Internal audit public sector capability: A case study. Journal of Public Affairs, 16(2), 181–191. https://doi.org/10.1002/pa.1574

Lenz, R., & O"Regan, D. J. (2024). The global internal audit standards: Old wine in new bottles? The EDP Audit, Control, and Security Newsletter, 69(3), 1–28. https://doi.org/10.1080/07366981.2024.2322835

Leung, P. & Cooper, B. J. (2009). Internal audit: An Asia-Pacific profile and the level of compliance with Internal Auditing Standards. Managerial Auditing Journal, 24(9), 861–882. https://doi.org/10.1108/02686900910994809

Mahzan, N., Zulkifli, N., & Umor, S. (2012). Role and authority: An empirical study on internal auditors in Malaysia. Asian Journal of Business and Accounting, 5(2), 69–98.

Marais, M., Burnaby, P. A., Hass, S., Sadler, E., & Fourie, H. (2009). Usage of internal auditing standards and internal auditing activities in South Africa and all respondents. Managerial Auditing Journal, 24(9), 883–898. https://doi.org/10.1108/02686900910994818

Marwa, B. J. (2023). Effect of I-tax Implementation on Revenue Collection in Kenya [Doctoral dissertation, University of Nairobi].

Mattei, G., Grossi, G., & AM, J. G. (2021). Exploring past, present and future trends in public sector auditing research: A literature review. Meditari Accountancy Research, 29(7), 94–134. https://doi.org/10.1108/MEDAR-09-2020-1008

Nipper, M. (2021). The role of audit committee chair tenure: A German perspective. International Journal of Auditing, 25(3), 716–732. https://doi.org/10.1111/ijau.12245

Organisation for Economic Co-operation and Development [OECD], (2021). Ownership and Governance of State-Owned Enterprises: A Compendium of National Practices. https://www.oecd.org/corporate/Ownership-and-Governance-of-State-Owned-Enterprises-A-Compendium-of-National-Practices-2021.pdf

Osborne, J. W., & Waters, E. (2019). Four assumptions of multiple regression that researchers should always test. Practical Assessment, Research, and Evaluation, 8(1), Article e2. https://doi.org/10.7275/r222-hv23

Poonan, U. U. (2019). The transformation of the South African national parks with special reference to the role of the Social Ecology Directorate 1994-2004 (Doctoral dissertation).

Polizzi, S., Lupo, F., & Testella, S. (2022). Quality assurance and improvement program: Some considerations for central banks. The TQM Journal, 35(8), 2203–2227. https://doi.org/10.1108/TQM-05-2021-0128

Rabie, B., & Goldman, I. (2014). The context of evaluation management. In Evaluation Management in South Africa and Africa, Sun Press. 1–214.

Rashid, A., Salim, B., & Ahmad, H. N. (2021). Internal Audit Effectiveness and Audit 166 Committee Characteristics: Empirical Evidence from Pakistan. iRASD Journal of Management, 3(1), 1–13. https://doi.org/10.52131/jom.2021.0301.0021

Ronkko, J., Lilja, M., & Oulasvirta, L. (2023). Voluntary adoption of the International Standards on Auditing (ISA) in local government audits: Empirical evidence from Finland. Public Money & Management, 43(3), 277–284. https://doi.org/10.1080/09540962.2022.2131290

Roussy, M. (2022). Engaging in internal audit research in the public sector no less: A Hara‐kiri for your academic career? Canadian Journal of Administrative Sciences/Revue Canadienne des Sciences de l'Administration, 39(3), 347–352. https://doi.org/10.1002/cjas.1661

Sawan, N. (2013). The role of internal audit function in the public sector context in Saudi Arabia. African Journal of Business Management, 7(6), 443–454.

Shaban, O. S., & Barakat, A. I. (2023). Evaluation of internal audit standards as a foundation for carrying out and promoting a wide variety of value-added tasks-evidence from emerging market. Journal of Risk and Financial Management, 16(3), Article e185. https://doi.org/10.3390/jrfm16030185

Shakeel, A., Rasheed, B., Ahmed, M., & Bakhsh, A. (2020). Effectiveness of the role of internal audit function: A perception of external auditors of Pakistan. Paradigms, SI(1), 75–80.

Shuwaili, A. M. J., Hesarzadeh, R., & Bagherpour Velashani, M. A. (2023). Designing an internal audit effectiveness model for public sector: Qualitative and quantitative evidence from a developing country. Journal of Facilities Management, 1(2), 25–60. https://doi.org/10.1108/JFM-07-2022-0077

Stewart, J., & Subramaniam, N. (2010). Internal audit independence and objectivity: Emerging research opportunities. Managerial Auditing Journal, 25(4), 328–360. https://doi.org/10.1108/02686901011034162

Tang, F., Norman, C. S., & Vendrzyk, V. P. (2017). Exploring perceptions of data analytics in the internal audit function. Behaviour & Information Technology, 36(11), 1125–1136. https://doi.org/10.1080/0144929X.2017.1355014

Vadasi, C., Bekiaris, M., & Andrikopoulos, A. (2020). Corporate governance and internal audit: An institutional theory perspective. Corporate Governance: The International Journal of Business in Society, 20(1), 175–190. https://doi.org/10.1108/CG-07-2019-0215

Vallabhaneni, S. R. (2005). Wiley CIA exam review, conducting the internal audit engagement. John Wiley & Sons.

Van Gils, D. (2012). The development of internal auditing within Belgian public entities: A Neo-institutional and new public management perspective [Doctoral Dissertation, Faculty of Social and Political Science, Université Catholique de Louvain].

Wiesel, F., & Modell, S. (2014). From new public management to new public governance? Hybridization and implications for public sector consumerism. Financial Accountability & Management, 30(2), 175–205. https://doi.org/10.1111/faam.12033

Yazid, H., & Wiyantoro, L. S. (2018). The effect of work experience, internal auditor competence, independence to due professional care and implications in internal audit quality. Advanced Science Letters, 24(4), 2565–2568. https://doi.org/10.1166/asl.2018.11006

Yusof, N. A. Z. M., Haron, H., Ismail, I., & Chambers (2018), A. Internal audit capability levels in Malaysian public sector organizations: The perceived role of management support and cooperation with external auditors. Journal of Governance and Integrity, 1(2), 25–60.

Zaman, M., & Sarens, G. (2013). Informal interactions between audit committees and internal audit functions: Exploratory evidence and directions for future research. Managerial Auditing Journal, 28(6), 495–515. https://doi.org/10.1108/02686901311329892