| Review | Open Access |

|---|

Determinants Affecting Systematic Risk in Pakistan’s Oil and Gas Sector |

|

|---|

![]() Muhammad Shoaib Hassan1*, Gul Mehak2 , and Waqas Mehmood1

Muhammad Shoaib Hassan1*, Gul Mehak2 , and Waqas Mehmood1

1Hailey College of Commerce, University of Punjab, Lahore, Pakistan

2School of Accounting, Zhongnan University of Economics and Law, Wuhan, China

The current study aimed to investigate the effect of different determinants on systematic risk in Pakistan’s oil and gas sector. In this study, the data of six systematic risk determinants, namely liquidity, firm size, operating efficiency, profitability, growth, and leverage, was collected from Pakistan Stock Exchange (PSX). Moreover, the firm’s monthly stock return and Karachi Stock Exchange (KSE) 100 index return data for the period of 2018-2022 was obtained from the website of ZHV Securities. Random effect regression analysis was performed to test hypothesis based on the Hausman test to validate the absence of multicollinearity, heteroskedasticity, and serial autocorrelation. Regression results showed that liquidity, profitability, operating efficiency, and leverage had a negative and significant effect. On the other hand, size and growth had a negative but insignificant effect on systematic risk regarding oil and gas companies in Pakistan. The obtained results were consistent with the existing literature and Capital Market Theory (CMT) and Capital Asset Pricing Model (CAPM). Policymakers are recommended to consider implementing measures in order to improve access to finance for companies in the sector, improve operational efficiency, and diversify sources of financing. Furthermore, the researchers are recommended to conduct comparative studies between different sectors to provide more valuable insights considering other determinants as per their country, industry, and sector dynamics.

1. INTRODUCTION

The oil and gas industry is a cornerstone of the global economic system, playing a crucial role in energy production, industrial operations, and transportation (2024). The global oil and gas market is worth over 2 trillion US dollars. Many countries depend on its performance for their Gross Domestic Product (GDP) and employment. For instance, (2017) highlighted that it contributes about 3.8% of the worldwide GDP and helps millions of people find employment, proving its role in energy markets. In recent times, the Asia-Pacific region has become a significant consumer of oil and gas, with developing countries leading the way in rapidly increasing their oil consumption (2019). The increase in oil demand not only leads to higher oil prices, affecting both producers and consumers by reducing disposable income, however, also increases uncertainty and risk. This negatively affects stock market prices and discourages investments (2020) which, in turn, leads to inflationary pressures on the economy and prompts central banks to adjust interest rates. This is particularly evident in rapidly developing countries in the Asia-Pacific region, such as China, India, and Pakistan, where GDP and oil consumption are rising (2023; 2020). Therefore, in an effort to achieve economic growth as well as balance the energy requirements of these nations, understanding factors that define systematic risks may help policymakers make better decisions. Pakistan's reliance on oil imports, coupled with its growing industrial demand, positions its oil and gas sector as a critical component of the economy, making it susceptible to systematic risk driven by global oil price dynamics (2023).

Although, the oil and gas sector is crucial to every economy, the impact of rising oil and gas prices varies between developed and developing countries. (2021) implies that developing economies are more affected by changes in oil prices which have significant implications for stock market prices and profits. While developed countries tend to be more energy-efficient and diversify their energy sources, making them less vulnerable to oil price fluctuations. In this regard, literature has revealed that the interconnection between energy usage, the economy, and financial markets is evident, as they are intricately linked to a country's economic growth (2021; 2023). Moreover, globalization has intensified the interdependence among economies, making them more sensitive to changes in oil and gas prices. This is evident by the OPEC oil embargo in 1973 which caused a significant increase in oil prices and the oil price shock in 1979, leading to a global recession. These events demonstrated how such shocks had severe consequences, particularly for developing countries (2024; 2023).

Previous research has examined the relationship between oil price volatility and financial performance globally, limited studies have focused on the determinants of systematic risk specific to Pakistan's oil and gas sector, an industry vital to the country's economic progress (2019; 2020; 2022). Additionally, different studies have produced varying conclusions about which financial variables affect systematic risk (2018; 2020). The current study aimed to address this gap by studying the effect of six systematic risk determinants, namely liquidity, firm size, operating efficiency, profitability, growth, and leverage, on the systematic risk of Pakistan's oil and gas sector (exploration and marketing). This provided implications for policymakers in the oil and gas industry, providing recommendations to analyze and anticipate future systematic risks to make informed decisions.

This study focused exclusively on the oil and gas sector due to its strategic importance in Pakistan's economy and its heightened exposure to global economic fluctuations, particularly oil price volatility, currency devaluation, and geopolitical uncertainty. Moreover, the sector is heavily reliant on imports and foreign investments, making it more susceptible to external shocks than other industries. By narrowing the scope, the research provided deeper, sector-specific insights that are more actionable for policymakers and investors. The six determinants, that is, liquidity, firm size, operating efficiency, profitability, growth, and leverage were selected based on their consistent appearance in empirical finance literature as primary financial indicators influencing systematic risk. These variables are measurable, relevant to investor decision-making, and have theoretical grounding in the Capital Asset Pricing Model (CAPM) and Capital Market Theory (CMT). While many other factors may influence market risk, this study limits its scope to these six for analytical clarity, data availability, and to ensure robust statistical testing.

The significance of this study lies in the fact that it aimed to fill a notable academic gap by investigating the financial determinants that influence systematic risk in Pakistan's oil and gas sector. This is a key industry for the country's economic stability, energy security, and industrial productivity, as emphasized by (2023). In a context where international oil prices are volatile, foreign exchange markets are unstable and energy imports are a critical necessity. Understanding how internal financial metrics, such as liquidity, leverage, and profitability affect firms' exposure to market-wide risk is not only timely but essential. By empirically evaluating how key financial indicators influence beta, the established proxy for systematic risk, this study contributed not only to the academic literature but also to practical risk management frameworks. In contrast to general studies that examined systematic risk across broader financial sectors (2024; 2023), this research provided sector-specific evidence that is more actionable for corporate managers, policymakers, and investors operating within the high-risk, capital-intensive oil and gas industry. The oil and gas sector, by its very nature, involves long project gestation periods, high capital intensity, and heightened exposure to geopolitical and regulatory uncertainty. Considering this, (2024) and (2024) highlighted the importance of studying systematic risk in this sector. It was contended that any changes in global oil prices, interest rates, or fiscal policies could have disproportionately large effects on firms, making them particularly vulnerable to external shocks.

By identifying which financial factors increase or mitigate this exposure, this study equipped firms with insights to build robust investment, financing, and operational strategies. Moreover, the study holds practical relevance for policymakers, who may use its findings to identify key areas where fiscal or regulatory reforms could enhance sectoral stability and attract long-term investment. In a broader context, the findings support efforts towards economic sustainability by helping the oil and gas sector manage market volatility and reduce its vulnerability to external shocks. Moreover, this research enhanced the ability of Pakistan's energy sector to adapt to the increasing uncertainties of the global energy landscape while contributing to the stable development of the national economy.

The present research proceeded by reviewing previous literature in section 2, data collection, and model development after hypothesis development. Then, data analysis and a discussion of the results are presented in section 4. Lastly, the study concluded by discussing results, their implications, and future research areas.

Literature Review

Recent studies specific to Pakistan's oil and gas sector underscore the unique financial challenges faced by firms operating in this volatile industry. For instance, (2023) applied quantitative risk assessment methods and found that financial risks including liquidity constraints and operational inefficiencies significantly impair project performance in oil and gas construction ventures. Similarly, (2022) highlighted the sensitivity of Pakistan's energy sector firms to macroeconomic shocks, particularly foreign exchange volatility and commodity price fluctuations, which exacerbate systematic risk exposure. While (2018) also found that in resource-intensive industries, such as sugar and oil and gas, profitability and leverage are critical determinants of market-based risk metrics. These insights reinforce the importance of focusing research within a specific sectoral and national context.

Theoretical UnderpinningThe success of equity capital depends largely on the issuance of stock timing, which is why determining the value of the stocks is so critical. In order to determine the value of the stocks, the CAPM proposed by Sharpe-Lintner and some of the models are widely used to estimate the cost of capital (2008). The CAPM calculates the expected asset's return based on its systematic risk, measured by the beta value which shows the existence of systematic risk and also tells us about the sensitivity of the individual stock returns to the returns of the portfolio stocks. Two types of risks associated with a firm include unsystematic risk and systematic risk, according to the model and returns, which are the functions of a company's systematic risk (2020). The risk specifies the expected rate of return that an investor wants from his investment in the company's stock. Systematic risk is associated with macroeconomic factors affecting all firms, making it undiversifiable. Whereas unsystematic risk is firm-specific and can be mitigated through portfolio diversification. (2022) concluded that changes in a firm's investing, financing, and operating activities may have an impact on its return and risk characteristics, especially in systematic risk. If systematic risk increases, the firm's value would decrease. This is because systematic risk directly impacts the investors' required returns and, consequently, stock prices. Unsystematic risk is related to the firm-specific event that reflects the stock price of the firm (i.e., strike, poor quality of the product, and mismanagement), and it may influence an investor's buying and selling perception of the stocks (2020). Not all investors have diversified stock portfolios, so systematic risk significantly impacts the stock return (2020).

(2022) found that liquidity should be negatively correlated with systematic risk, contending that if a firm is more liquid, it would be less sensitive to the market. This means that high liquidity makes the firm less sensitive to general movements in the market and therefore, provides more certainty of returns. (2020) conducted research to reexamine the relationship between systematic risk and its liquidity and found a negative relationship. This contended that variability in relative stock liquidity does not positively affect stock return. It was also stressed that the variability of liquidity exerts a weak impact on stock returns, leading to the conclusion that firms' liquidity helps to protect against fluctuations in the market. Besides these scholars, (2020) and (2024) also found a negative relationship. This highlighted that liquidity plays a critical role in mitigating systematic risk, as firms with higher liquid assets tend to exhibit lower market sensitivity.

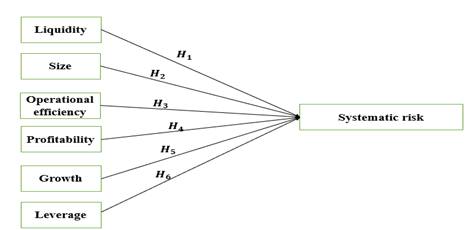

H1: Liquidity and systematic risk are inversely related.

Previous research indicated that there is a positive relationship between systematic risk and size (2020; 2020). This contended that firms with large sizes consider that their security is rapidly traded in the market and could be easily converted into cash being highly marketable. Therefore, these securities are considered less risky and have lower level of systematic risk. Large companies produce goods on a large scale and these companies avail themselves of economies of scale and become more profitable. These firms have less chance of bankruptcy and lower systematic risk levels (2020). This perspective suggests that the higher marketability and liquidity of securities associated with larger firms make them more resilient to market fluctuations. Moreover, their ability to manage and withstand external shocks, such as economic and political changes, positions them as less risky investments (2020).

H2: Size and systematic risk are inversely related.

Several studies showed negative relationship between operating efficiency and systematic risk (2020; 2018). This contended that those firms which are utilizing their resources efficiently generate more revenues than their competitors. Furthermore, these firms may lower down possible losses that could occur. Resultantly, these firms have a low level of systematic risk. The argument was also supported by (2017) who reexamined restaurant systematic risk determinants. It was found that firms that are highly efficient in generating revenue would have to face low systematic risk. The study concluded that efficient resource utilization not only improves profitability but also cushions firms against potential risks. (2016) researched determinants affecting systematic risk and their findings suggested that operating efficiency is negatively correlated with systematic risk. Firms with higher operating efficiency are considered to make high profits, and there are fewer failure chances for those firms thus, associated with lower systematic risk.

H3: Operating efficiency and systematic risk are inversely related.

Earlier studies showed a negative relationship between profitability and systematic risk (2021; 2021). This contended that firms with high profitability ratios have a lower chance of failure; thus, there is less systematic risk. This perspective highlights that consistent profitability strengthens a firm's financial health, making it less vulnerable to external shocks. Other scholars also found a negative relationship, arguing that cash flow stability reduces systematic risk. If cash flow from the operation is stable, the business is less likely to fail and vice versa (2019; 2021).

H4: Profitability and systematic risk are inversely related.

(2021) argued that fast-growing organizations face more competition than stable ones and are more sensitive to economic fluctuation. The argument was supported by (2021) who researched the chain restaurant industry. They also argued that rapidly growing firms require more resources from external financing, making them sensitive to any economic fluctuation. Another school of thought showed that rapidly growing firms need to invest more in human resource training and education and require more funds. These funds cause firms to have high leverage, which means that they are at high risk. Some other researchers also reported a negative relationship, arguing that firms with rapid growth face increased leverage and economic fluctuations, leading to higher systematic risk (2021; 2019). This implies that firms experiencing rapid growth may face higher financial risk and economic volatility due to increased leverage and resource demands.

H5: Growth and systematic risk are inversely related.

Most studies theoretically and empirically investigated the relationship between leverage and beta. For instance, (2020) and (2021) suggested that leverage has a positive significant relationship. Both studies contended that an increase in leverage would lower the investor's perceptions related to systematic risk and cash flow would remain unchanged. It was also suggested that decrease in leverage would not affect beta. (2020) also found a positive relationship between leverage and systematic risk, arguing that a positive change in leverage leads to a positive change in systematic risk. This study concluded that leverage plays a significant role in determining risk, particularly in sectors with high debt-equity ratios.

H6: Leverage and systematic risk are positively related.

Figure 1 Conceptual Framework

Methodology

In this study, the data of independent variables (financial ratios) was collected from Pakistan Stock Exchange (PSX) and the firm’s monthly stock return. Karachi Stock Exchange (KSE) 100 index return data of the oil and gas sector (exploration and marketing) of Pakistan for the period of 2018-2022 was obtained from the website of ZHV Securities. In this study, data from the PSX refers to firm-specific financial data including the six independent variables. These variables include liquidity, firm size, operating efficiency, profitability (ROA), growth, and leverage. These were derived from the financial statements of the oil and gas companies listed on PSX. In contrast, the KSE-100 index data represents the market return used to calculate the systematic risk (beta coefficient) reflecting the overall performance of the top 100 companies listed on the PSX by market capitalization and serves as a benchmark for the broader market. The monthly returns of each firm were compared with the monthly returns of the KSE-100 index to compute their beta values, indicating their sensitivity to overall market movements. Table 1 shows the operational definitions of the study variables.

Table 1 Operational Definition of Study Variables| Variable | Proxy | Source |

|---|---|---|

| Liquidity | Current assets/current liabilities | Maghyereh and Abdoh (2020) |

| Size | Natural Log of total assets | (Hassan, 2023), Hassan et al. (2022) |

| Operating Efficiency | Net sales/total assets | Jiayi (2016), (Nawaz et al., 2017) |

| Profitability (ROA) | Net income/total assets | Hassan et al. (2022) |

| Growth | Percentage increase in EBIT | Nugroho and Halik (2021) |

| Leverage | Total debt/total assets | (Cincinelli et al., 2021), Hassan (2023) |

| Systematic Risk (Beta coefficient) | The ratio of monthly return to total stock market return | (Sukrianingrum & Manda, 2020) |

A total of 13 firms are registered in Pakistan’s oil and gas sector (exploration and marketing). However, 9 of these firms are considered final companies, excluding 4 firms with negative net income. Random effect regression analysis based on the Hausman test as suggested by Hausman (1978) to test the hypothesis. As per Table 3, the Hausman test statistics reveal chi² = 22.27 and P-value = 0.619 greater than 0.05. Therefore, the random effect model was suitable for this study considering the following econometric model.

(1)

Before running the chosen regression model, the absence of multicollinearity measured by Value Inflation Factor (VIF) score, heteroskedasticity, and serial autocorrelation was ensured to have reliable results (Hassan, 2023; Hassan et al., 2022). Furthermore, descriptive statistics and correlation analysis were also performed. For the robustness analysis, the researchers also provided results of fixed effects and pooled analysis in appendix consistent with Alrwashdeh et al. (2023).

Results and Discussion

Descriptive StatisticsDescriptive statistics in Table 2 hold particular significance. The mean measurement of the beta for Pakistan’s oil and gas sector is 0.73, with a standard deviation of 0.45. This shows that the systematic risk of the sampled oil and gas sector is less than the market average one, and the investors could view the stock of the oil and gas sector as less risky. The arithmetic mean of liquidity, profitability, and growth is 1.76, 6.63, and 20.23, with the STD of 0.91, 4.87, and 2.21, respectively.

Table 2 Descriptive Statistics| Minimum | Maximum | Mean | SD | |

|---|---|---|---|---|

| Liquidity | 0.84 | 4.01 | 1.76 | 0.91 |

| Size | 16.66 | 26.63 | 22.65 | 1.58 |

| Operating efficiency | 0.28 | 7.02 | 2.88 | 1.83 |

| Profitability (ROA) | 1.96 | 22.93 | 5.63 | 6.87 |

| Growth | 17.34 | 22.59 | 20.23 | 2.21 |

| Leverage | 0.17 | 3.90 | 0.99 | 0.73 |

| Beta | 0.09 | 1.25 | 0.73 | 0.45 |

Meanwhile, the arithmetic mean of leverage and operating efficiency is 0.99 and 2.88, respectively with STDs of 0.73 and 1.83. Descriptive statistics reveal that the less risky sector is profitable for investors.

Regression AnalysisTwo main classical regression assumptions, heteroskedasticity and serial autocorrelation, of which the results are presented in Table 3, are tested to choose the preferable panel data analysis model.

Table 3Diagnostic Tests for Panel regression| Test | Statistic | Value | p | Decision |

|---|---|---|---|---|

| Breusch-Pagan Test for Heteroskedasticity | c²(1) | 0.39 | 0.53 | No heteroskedasticity |

| Wooldridge Test for Autocorrelation | F(1, 51) | 18.38 | 0.10 | No autocorrelation |

| Hausman Test for Model Selection | c² | 22.27 | 0.61 | Random effects model |

The heteroscedastic and serial autocorrelation issue is absent in the econometric model and the insignificant Hausman test statistic leads to random effect model selection.

Table 4 shows that liquidity has a negative (β = -0.3785) but significant (p<0.05) effect on systematic risk. This leads to the acceptance of H1 being consistent with (Maghyereh & Abdoh, 2020; Shafique et al., 2022). He contended that if a firm is more liquid, then it would be less sensitive to market, and variability in relative stock liquidity does not affect stock return positively. This result supports the CMT which emphasizes the importance of liquidity in reducing market risks by enabling firms to adjust more easily to market conditions, thus lowering their exposure to systematic risk. Considering this, it can be contended that the companies in Pakistan’s oil and gas sector are less sensitive to the market being more liquid, which negatively affects systematic risk.

Furthermore, profitability has a negative (β = -0.221) but significant (p<0.01) effect on systematic risk. This leads to the acceptance of H2 being consistent with (Sukrianingrum & Manda, 2020; Yang et al., 2020). He contended that firms with large size consider that their security is rapidly traded in the market and can easily convert into cash being highly marketable. So, these securities are considered as less risky and have lower level of systematic risk. Considering this, it can be contended that the securities of companies in Pakistan’s oil and gas sector could easily be converted into cash and be less risky, which has a lower level of systematic risk being aligned with the CAPM. This suggests that companies with high profitability and liquidity experience less volatility in their returns, leading to a lower exposure to systematic risk.

Similarly, operating efficiency has a negative (β = -0.853) but significant (p<0.1) effect on systematic risk. This leads to the acceptance of H3 being consistent with (Jaafar et al., 2020; Kamran & Malik, 2018). He contended that firms utilizing their resources efficiently generate more revenues than their competitors. Furthermore, these firms may lower down possible losses that could occur and as a result, these firms have a low level of systematic risk. Considering this, it can be contended that the companies in the Pakistan’s oil and gas sector have higher operating efficiency and are considered to generate high profits. Furthermore, there are less chances of failure of those firms and thus, associated with lower systematic risk. This result is supported by the CMT. This theory suggests that firms with higher operating efficiency are better positioned to withstand market volatility and reduce exposure to risks, leading to lower systematic risk.

Table 4Hypothesis Testing| Variables | β (SE) | VIF | Decision |

|---|---|---|---|

| Liquidity | -0.3785** | 2.58 | Supported |

| (0.158) | |||

| Profitability | -0.221*** | 3.81 | Supported |

| (0.007) | |||

| Operating Efficiency | -0.853* | 2.48 | Supported |

| (0.483) | |||

| Growth | -0.006 | 1.03 | Supported |

| (0.00723) | |||

| Size | -0.124 | 1.21 | Supported |

| (0.215) | |||

| Leverage | -0.104*** | 1.75 | Supported |

| (0.00549) | |||

| Constant | 4.37 | ||

| (0.273) | |||

| Prob >c² | 0.000 | ||

| R2 | 0.2422 |

Table 4 shows that growth has a negative (β = -0.006) but insignificant effect on systematic risk. This leads to the acceptance of H4 being consistent with (Lasmana & Wahyudin, 2021; Nugroho & Halik, 2021). The study contended that firms with high profitability ratio have less chances of failure; thus, there is less systematic risk. The CAPM also suggests that while growth may lower risk in some instances, its impact is not as significant without considering factors, such as profitability, which plays a more direct role in reducing exposure to systematic risk. This implies that the companies in Pakistan’s oil and gas sector have stable cash flow from operation, and there are fewer chances of failure or risk.

Similarly, size has a negative (β = -0.124) but insignificant effect on systematic risk. This leads to the acceptance of H5 being consistent with (Muhammad et al., 2021; Narayan et al., 2019). The study argued that rapidly growing firms require more resources and these resources are obtained from external financing which makes them sensitive if there is any fluctuation in the economy. According to CAPM, the size effect on systematic risk is not straightforward, as large firms may still face substantial market risks if they rely heavily on external financing or are subject to market fluctuations.

Moreover, leverage has a negative (β = -0.104) but significant (p<0.01) effect on systematic risk. This leads to the acceptance of H6 being consistent with (Bratis et al., 2020; Pagano & Sedunov, 2016). The study contended that an increase in leverage would lower down investors’ perceptions related to systematic risk and cash flow would remain unchanged. The CAPM suggests that higher leverage may alter the risk-return profile for investors, leading them to perceive the firm as having lower systematic risk, even if the underlying risks remain. Considering this, it can be contended that the companies in Pakistan’s oil and gas sector have high leverage that leads investors to assume more risk.

Although, the results align with much of the existing literature, its novelty lies in its contextual focus of examining systematic risk determinants specifically within Pakistan’s oil and gas sector. Previous studies largely concentrated on broader industries or different economic environments. Whereas, the current study offered sector-specific insights into a developing economy with distinct macroeconomic and geopolitical factors. The findings highlighted critical financial determinants influencing systematic risk in Pakistan’s oil and gas sector. The negative impact of liquidity, profitability, operating efficiency, and leverage on systematic risk suggests that firms with stronger internal financial controls and operational stability are better insulated from market volatility. This aligns with global trends where firms in resource-dependent economies exhibit heightened sensitivity to macroeconomic shocks, such as global oil price fluctuations, interest rate changes, and geopolitical instability. For instance, rising US interest rates or OPEC+ production decisions often impact global energy prices, affecting the systematic risk exposure of oil and gas firms in emerging markets (Quint & Venditti, 2023). Furthermore, the ongoing global shift towards renewable energy and net-zero emission targets introduces long-term uncertainty, compelling oil-reliant firms to adapt or face increased risk. A divergence from prior literature is noted in the negative and significant effect of leverage, which contrasts with several studies that report a positive correlation. This suggests that, in the Pakistani context, higher leverage may reflect cautious financial structuring rather than heightened risk exposure. Overall, these results underscore the importance of strategic risk management and financial resilience in volatile environments. For policymakers, it reinforces the need to foster fiscal and regulatory stability and promote investment in technological upgrades and risk diversification strategies to buffer firms against global shocks.

The VIF values shown in Table 4 are all below 5, indicating no significant multicollinearity among the independent variables and Prob > c² less than 0.05 affirms that the model is statistically significant. This affirms that each predictor contributes uniquely to the model without redundancy, enhancing the reliability of regression results. The R2 value of 0.2422, while moderate, is acceptable given the nature of panel data and the complexity of systematic risk influenced by both observed and unobserved variables. It suggests that approximately 24.22% of the variance in systematic risk is explained by the selected determinants. While higher R-squared values are ideal, in financial and economic studies this level is considered sufficient when backed by theoretical justification and robustness checks (El Tamamy, 2014).

Robustness AnalysisIn order to determine the stability of the results, additional regression tests were run through the fixed effects and pooled OLS models. Such additional techniques are used to check and verify the consistency and accuracy of the results obtained by various estimation procedures. The results are reported in Appendix (Table 5), suggesting that the coefficients of the independent variables and the dependent variable are consistent irrespective of the regression techniques employed.

The fixed effects model analysis results showed that liquidity, profitability, operating efficiency, and leverage are statistically significant with the dependent variable as in the main analysis. For instance, liquidity has a negative and significant correlation (β = -0.395, p < 0.05) and profitability was also found to have a negative relationship (β = -0.231, p < 0.01) thereby, supporting actual results. The analysis of the pooled OLS model also supports the findings of the random effects model. Liquidity (β = -0.365, p < 0.05) and profitability (β = -0.216, p < 0.01) retain its negative relationship. However, the coefficient of operating efficiency (β = -0.393) was found to be only significant at 10% level, implying that there might be some cross-sectional heterogeneity in the strength of the relationship depending on the model used. Interestingly, growth and size did not have substantial correlations in either model as identified in the primary analysis. This further strengthens the main findings. Furthermore, it can be observed from both models, leverage stands out as a consistent and robust determinant with negative effects estimated at -0.099 in fixed effects (p < 0.01) and -0.106 in pooled OLS (p < 0.01). The significance of the constant term and the fairly stable R-squared values (fixed effects = 0.238 and pooled OLS = 0.252) show how well the models explain the relationship variations.

Conclusion

The current study aimed to investigate the effect of different determinants on the systematic risk in Pakistan’s oil and gas sector. In this study, the data of independent variables (financial ratios) was collected from PSX and the firm’s monthly stock return. KSE-100 index return data from 2018-2022 was obtained from the website of ZHV Securities. The study used six systematic risk determinants: liquidity, firm size, operating efficiency, profitability, growth, and leverage. A total of 13 firms are registered in Pakistan’s oil and gas sector (exploration and marketing). However, 9 of these firms are considered final companies, excluding 4 firms with negative net income. Random effects regression analysis based on the Hausman test was performed to test the hypothesis validating the absence of multicollinearity, heteroskedasticity, and serial autocorrelation.

Descriptive statistics revealed that the systematic risk of the sampled oil and gas sector is less than the market average. Therefore, investors could view the oil and gas sector stock as less risky. The correlation matrix revealed that liquidity, profitability, size, and leverage positively relate to systematic risk, while operating efficiency and growth are inversely related. The VIF score of all variables was less than five, which showed the absence of a multicollinearity issue, and the model was statistically significant as Prob > chi2 was less than 0.05. Regression results showed that liquidity, profitability, operating efficiency, and leverage had a negative and significant effect. While, size and growth had a negative but insignificant effect on systematic risk regarding oil and gas companies in Pakistan. The obtained results are consistent with the existing literature. Overall, the results revealed that companies in Pakistan’s oil and gas sector are less sensitive to the market being more liquid, can easily be converted into cash, have high operating efficiency, have stable cashflows, and have less chance of failure, ultimately leading to lower systematic risk.

The results are not generalized to other economies due to the unique structural and economic characteristics of Pakistan’s oil and gas sector. Factors, such as reliance on imports, regulatory frameworks, energy infrastructure, and financial market maturity differ significantly from those in developed or resource-rich countries. Resultantly, the systematic risk determinants identified in this context may not behave similarly elsewhere, necessitating caution when applying these findings to other economies without further contextual analysis.

Future Research Implications

The negative relationship between liquidity and systematic risk suggests that companies in the sector may face financial constraints. This could hinder their ability to invest in new projects for which policymakers are recommended to adopt measures in order to improve access to finance. Furthermore, the negative relationship between profitability and systematic risk suggests that companies in the sector may struggle to generate sufficient profits to invest in growth. For this purpose, companies should consider improving operational efficiency and diversifying their revenue streams. Moreover, the negative relationship between operating efficiency and systematic risk suggests that oil and gas sector may be struggling to operate efficiently. So, it is recommended to invest in new technologies and upgrade their infrastructure. Finally, the negative relationship between leverage and systematic risk suggests that companies in the sector may be over-relying on debt financing, which could put them at risk of financial distress. Therefore, companies are recommended to consider reducing their debt levels and diversifying their financing sources.

This study provides a valuable theoretical contribution to the existing body of knowledge on systematic risk. It extended the application of the CAPM and CMT to a developing economy’s energy sector, specifically Pakistan’s oil and gas industry. While previous studies have largely focused on developed economies or generalized industry-level analyses, this research isolated a vital sector within a volatile economic environment. By empirically examining six financial determinants, that is, liquidity, size, operating efficiency, profitability, growth, and leverage, the study validated the traditional risk-return assumptions in CAPM. This demonstrates that variables often assumed to reduce risk (e.g., firm size and growth) may have insignificant effects in developing contexts. Furthermore, the study revealed that firms with strong liquidity and operating efficiency are less sensitive to market movements. This reinforces the importance of firm-level financial health in mitigating systematic risk. These insights bridge a gap in literature by showing how macroeconomic instability, sector-specific dynamics, and emerging market characteristics influence the predictive power of traditional financial models. Thus, the study enhanced the understanding of how theoretical models operate under non-ideal, real-world conditions, making it relevant for academics, analysts, and policymakers in emerging markets.

Limitations and Future Research

The study’s first limitation is its generalizability to only Pakistan’s oil and gas sector. Corresponding to this limitation, future researchers are recommended to analyze systematic risk determinants in different industries and segments of the economy. More precisely, future research should expand beyond the oil and gas sector to examine other critical industries within Pakistan and comparable developing economies to assess the consistency of systematic risk determinants. A cross-country comparative approach may also be employed to evaluate how different macroeconomic environments influence the behavior of financial risk factors. Undoubtedly, this study considered a comprehensive set of determinants affecting systematic risk. However, future researchers are recommended to consider other factors based on their country, industry, and sector dynamics. For instance, future studies could incorporate qualitative variables, such as corporate governance, regulatory policy, or geopolitical risks to enrich the quantitative framework. In this study, ROA was used as a proxy for profitability. Further studies should be carried out using other proxies, such as ROE and EPS. Longitudinal studies tracking post-pandemic economic recovery or energy transition trends may also offer deeper understanding of how systemic changes affect firm-level risk exposure in the medium to long term.

CONFLICT OF INTEREST

The authors of the manuscript have no financial or non-financial conflict of interest in the subject matter or materials discussed in this manuscript.

DATA AVAILABILITY STATEMENT

The data associated with this study will be provided by the corresponding author upon request.

FUNDING DETAILS

No funding has been received for this research.

REFERENCES

- Adekoya, O., Oliyide, J., Akinseye, A., & Al-Faryan, M. A. S. (2024). Risk spillovers among global oil & gas firms. Investment Analysts Journal, 54, 1–19. https://doi.org/10.1080/10293523.2024.2347714

- Alam, S. M. I. (2022). The capital market theory: Markowitz, cml, and separation theorem. https://www.researchgate.net/publication/363639593_The_Capital_Market_Theory_Markowitz_CML_and_Separation_Theorem

- Alrwashdeh, N. N. F., Ahmed, R., Danish, M. H., & Shah, Q. (2023). Assessing the factors affecting the liquidity risk in Jordanian commercial banks: A panel data analysis. International Journal of Business Continuity and Risk Management, 13(1), 84–99. https://doi.org/10.1504/IJBCRM.2023.10055478

- Alrwashdeh, N. N. F., Umara, N., Hassan, D. M., & and Ahmed, R. (2024). Bank capital and risk in emerging banking of Jordan: A simultaneous approach. Cogent Economics & Finance, 12(1), Article e2322889. https://doi.org/10.1080/23322039.2024.2322889

- Alsagr, N., & Van Hemmen, S. (2021). The impact of financial development and geopolitical risk on renewable energy consumption: Evidence from emerging markets. Environmental Science and Pollution Research, 28, 25906–25919. https://doi.org/10.1007/s11356-021-12447-2

- Arezki, M. R., Jakab, Z., Laxton, M. D., Matsumoto, M. A., Nurbekyan, A., Wang, H., & Yao, J. (2017). Oil prices and the global economy. International Monetary Fund. https://www.imf.org/en/Publications/WP/Issues/2017/01/27/Oil-Prices-and-the-Global-Economy-44594

- Arora, L. (2019, June 21–23). Firm performance and systematic risk [Paper presentation]. 2nd International Conference on Business, Management and Economics, Vienna, Austria.

- Bratis, T., Laopodis, N. T., & Kouretas, G. P. (2020). Systemic risk and financial stability dynamics during the Eurozone debt crisis. Journal of Financial Stability, 47, Article e100723. https://doi.org/10.1016/j.jfs.2020.100723

- Cincinelli, P., Pellini, E., & Urga, G. (2021). Leverage and systemic risk pro-cyclicality in the Chinese financial system. International Review of Financial Analysis, 78, Article e101895. https://doi.org/10.1016/j.irfa.2021.101895

- Dai, Z., & Wu, T. (2024). The impact of oil shocks on systemic risk of the commodity markets. Journal of Systems Science and Complexity, 37, 2697–2720. https://doi.org/10.1007/s11424-024-3224-y

- Durrani, O., & Zeeshan, Q. (2023). An assessment of risks in oil and gas construction projects in Pakistan: A quantitative approach using failure modes & effects analysis. Journal of Engineering Management and Systems Engineering, 2(3), 180–195. https://doi.org/10.56578/jemse020305

- El Tamamy, M. (2014). Investigating the explanatory power of economic profits (Eva®) versus accounting profits on stock returns as a measure of shareholders wealth creation. An empirical study of the FTSE 100. An Empirical Study of the FTSE, 100 [Master's thesis, London School of Business and Finance]. Social Science Research Network. https://dx.doi.org/10.2139/ssrn.2507191

- Hausman, J. A. (1978). Specification tests in econometrics. Econometrica: Journal of the Econometric Society, 46(6), 1251–1271. https://doi.org/10.2307/1913827

- Hassan, M. S. (2023). Dynamics of corporate governance and tax avoidance in Pakistan family-owned firms. KASBIT Business Journal, 16(4), 1–13.

- Hassan, M. S., Ahmad, A., & Qadeer, A. (2022). Dynamics of intellectual capital, corporate governance, and firm performance in family-owned companies in Pakistan. NUML International Journal of Business & Management, 17(2), 1–17. https://doi.org/10.52015/nijbm.v17i2.133

- Islam, S., Raihan, A., Ridwan, M., Rahman, M. S., Paul, A., Karmakar, S., Paul, P., Tanchangya, T., Rahman, J., & Al Jubayed, A. (2023). The influences of financial development, economic growth, energy price, and foreign direct investment on renewable energy consumption in the BRICS. Journal of Environmental and Energy Economics, 2(2), 17–28. https://doi.org/10.56946/jeee.v2i2.419

- Jaafar, M. N., Muhamat, A. A., Basri, M. F., & Alwi, S. F. S. (2020). Determinants of systematic risk: Empirical evidence from Shariah compliants firms listed on Bursa Malaysia. International Business Education Journal, 13(1), 71–82. https://doi.org/10.37134/ibej.vol13.1.6.2020

- Jiayi, L. (2016). Systematic risk, financial indicators and the financial crisis: A risk study on international airlines [Unpublished master's thesis]. Uppsala University.

- Kamran, M., & Malik, Q. (2018). Do financial variables affect the systematic risk in sugar industry? Pakistan Administrative Review, 2(2), 234–242.

- Kraidi, L., Shah, R., Matipa, W., & Borthwick, F. (2019). Analyzing the critical risk factors associated with oil and gas pipeline projects in Iraq. International Journal of Critical Infrastructure Protection, 24, 14–22. https://doi.org/10.1016/j.ijcip.2018.10.010

- Lasmana, S. A., & Wahyudin, A. (2021). Profitability as a moderating variable of systematic risk in mining companies. Accounting Analysis Journal, 10(2), 131–137. https://doi.org/10.15294/aaj.v10i2.47343

- Liu, J. H., Huang, L.-L., & McFedries, C. (2008). Cross-sectional and longitudinal differences in social dominance orientation and right wing authoritarianism as a function of political power and societal change. Asian Journal of Social Psychology, 11(2), 116–126. https://doi.org/10.1111/j.1467-839X.2008.00249.x

- Maghyereh, A., & Abdoh, H. (2020). Asymmetric effects of oil price uncertainty on corporate investment. Energy Economics, 86, Article e104622. https://doi.org/10.1016/j.eneco.2019.104622

- Maiti, M. (2021). Efficient frontier and portfolio optimization. In M. Maiti (Ed.), Applied financial econometrics: Theory, method and applications (pp. 89–111). https://doi.org/10.1007/978-981-16-4063-6_4

- Mittal, S., Bhattacharya, S., & Mandal, S. (2022). Characteristics analysis of behavioural portfolio theory in the Markowitz portfolio theory framework. Managerial Finance, 48(2), 277–288. https://doi.org/10.1108/MF-05-2021-0208

- Muhammad, B., Khan, M. K., Khan, M. I., & Khan, S. (2021). Impact of foreign direct investment, natural resources, renewable energy consumption, and economic growth on environmental degradation: Evidence from BRICS, developing, developed and global countries. Environmental Science and Pollution Research, 28(17), 21789–21798. https://doi.org/10.1007/s11356-020-12084-1

- Nahar, N., Alrwashdeh, N., Ahmed, R., Danish, M., & Shah, Q. (2023). Assessing the factors affecting the liquidity risk in Jordanian commercial banks: A panel data analysis. International Journal of Business Continuity and Risk Management, 13(1), 84–99. https://doi.org/10.1504/IJBCRM.2023.10055478

- Narayan, S., Le, T.-H., Rath, B. N., & Doytch, N. (2019). Petroleum consumption and economic growth relationship: Evidence from the Indian States. Asia-Pacific Sustainable Development Journal, 26(1), 21–65. https://doi.org/10.18356/348f0f5e-en

- Nawaz, R., Imran, S., Arshad, M., Rani, T., & Khan, A. (2017). Financial variables and systematic risk. Chinese Business Review, 16(1), 36–46. https://doi.org/10.17265/1537-1506/2017.01.004

- Nguyen, T. C., Vu, T. N., Vo, D. H., & McAleer, M. (2020). Systematic risk at the industry level: A case study of Australia. Risks, 8(2), Article e36. https://doi.org/10.3390/risks8020036

- Nugroho, M., & Halik, A. (2021). The effect of growth and systematic risk on the firm's value: Profitability as a mediating variable. Journal of Economics, Business, & Accountancy Ventura, 23(3), 466–476. https://doi.org/10.14414/jebav.v23i3.2468

- Pagano, M. S., & Sedunov, J. (2016). A comprehensive approach to measuring the relation between systemic risk exposure and sovereign debt. Journal of Financial Stability, 23, 62–78. https://doi.org/10.1016/j.jfs.2016.02.001

- Quint, D., & Venditti, F. (2023). The influence of OPEC+ on oil prices: A quantitative assessment. The Energy Journal, 44(5), 173–186.

- Shafique, A., Hassan, M. U., Shahzad, A., Ali, Q. M., & Saqlain, M. (2022). Exchange rate volatility and its relationship with macroeconomic variables in Pakistan. Bulletin of Business and Economics (BBE), 11(1), 121–131.

- Sukrianingrum, D. R., & Manda, G. S. (2020). The effect of systematic risk and unsystematic risk on expected return of optimal portfolio. SAR (Soedirman Accounting Review): Journal of Accounting and Business, 5(2), 181–195. https://doi.org/10.20884/1.sar.2020.5.2.3772

- Tache, I. (2024). OPEC and the 1970s oil crises: Lessons for the 2021 global energy crisis. In H.-D. Yan, O. Bajo-Rubio, D. S. Kwan, & F.-L. T. Yu (Eds.), Conflicts and challenges in the middle east: religious, political and economic perspectives (pp. 61–77). Springer.

- Wang, Y., Bouri, E., Fareed, Z., & Dai, Y. (2022). Geopolitical risk and the systemic risk in the commodity markets under the war in Ukraine. Finance Research Letters, 49, Article e103066. https://doi.org/10.1016/j.frl.2022.103066

- Wiyono, E. R., & Mardijuwono, A. W. (2020). Leverage, profitability, firm size, exchange rate, and systematic risk: Evidence from the manufacturing industry in Indonesia. Cuadernos de Economía, 43, 442–448. https://doi.org/10.32826//cude.v4i123.402

- Yang, L., Wang, Y., Wang, R., Klemeš, J. J., Almeida, C. M. V. B. d., Jin, M., Zheng, X., & Qiao, Y. (2020). Environmental-social-economic footprints of consumption and trade in the Asia-Pacific region. Nature Communications, 11(1), Article e4490. https://doi.org/10.1038/s41467-020-18338-3

- Zaman, S. u. (2023). Arab oil embargo. In M. Ustaoğlu & C. Çakmak (Eds.), The palgrave encyclopedia of islamic finance and economics (pp. 1–8). springer.

- Zhao, X.-h., & Zhang, Z.-h. (2020). Risk factors for postpartum depression: An evidence-based systematic review of systematic reviews and meta-analyses. Asian Journal of Psychiatry, 53, Article e102353. https://doi.org/10.1016/j.ajp.2020.102353