| Review | Open Access |

|---|

Nexus between Financial Reporting Fraud and Delegated Investments: Mediating role of Emotions and Delegated Investments Decisions |

|

|---|

![]() Rukhshinda Begum*, and Danish Ahmed Siddiqui

Rukhshinda Begum*, and Danish Ahmed Siddiqui

Karachi University Business School, University of Karachi, Pakistan

Financial reporting fraud is an important area of study in finance. However, reporting this fraud encounters new challenges with the changes in time and the state of affairs. Hence, this study is envisioned to investigate the mediating role of emotions and investment decisions in between financial reporting fraud and the performance of investment professionals under the delegated investment mechanism. The research is based on the responses collected through a self-administered questionnaire from 248 investment professionals in Pakistan selected through judgmental sampling. The proposed relationship was analyzed through the application of Partial Least Square Structure Equation Modeling (PLS-SEM) by using Smart PLS 4. The study discovered the full mediation of both emotions and short- and long-term investment decisions in the relationship between financial reporting fraud and investment performance. Cognizant to the fact that emotions and investment decisions mediate between fraudulent financial reporting and the performance of investment professionals; real investors may have a better understanding about who to hire to manage their investments. A well-selected competitive professional, at one end, is expected to safeguard the investors’ interest in the times of crises. While, at the other end, these professionals would bring economic stability by strengthening the investors’ trust on the financial market mechanisms as a result of their resilient professional support.

1. INTRODUCTION

“Fraudulent financial reporting involves intentional misstatements, including omissions of amounts or disclosures in financial statements, to deceive financial statement users” (International Auditing and Assurance Standards Board, 2023, p. 17). Approximately 5% of the total revenues of firms vanish due to fraud, which actually has been a global concern since long. Financial statement frauds are among the frauds that cause huge losses for firms and make the continuation of their businesses and even their existence doubtful. These frauds commonly include the over/under statement of revenues, over/under statement of expenses, and over/under valuation of assets and liabilities. Financial reporting frauds are usually executed either by the management or the ones responsible for the governance and control of the companies (Zenzerović, Šajrih, 2023). A virtuous corporate governance mechanism is imperative to avert managers from fraudulent reporting. Moreover, financial statements are the only source of information for stakeholders in developing economies and may lose their trustworthiness in case of the occurrence of a fraud (Ebaid, 2023).

Financial reporting is considered as significant in making investment decisions (Kawugana et al., 2019). Investor decisions are greatly influenced by the financial statements of the investee companies. On the basis of these statements, investors decide whether to invest in a business or not (Mohammed et al., 2016). The ability of SMEs to attract investments and enjoy optimal allocation of resources in productive ways is interlinked with the quality of their financial reporting. All financial statements were found to have a significant positive effect on investment decisions in Nigeria (Akinadewo et al., 2023). Moreover, a significant relationship was also observed between financial statements and decisions made by the financial decision-makers in KSA. The lack of credibility in financial information results in the lost trust of investors and hinders them from making sound investment decisions (Abdulshakour, 2020). The poor quality of financial reporting adversely affects investor confidence and ultimately investor decisions (Mesioye & Bakare, 2024).

Several researches have been conducted to study the relationship between financial reporting quality and investment efficiency. In this regard, a positive association was observed between financial reporting quality and investment efficiency in the manufacturing companies of Vietnam (Le et al., 2024), in the companies listed on the Indonesia Stock Exchange (Ardianto et al., 2020), and in the companies listed with the Pakistan Stock Exchange (Shahzad & Rehman, 2019). Manipulation in the valuation of assets and recognition of expenses negatively affect the profits of the manufacturing firms (a basis for the productive sector of economy) in the long-run. Researchers contend that it harms creditors and investors by providing misleading financial information. Such information adversely affects the reliability of profit as being a measure of performance. Hence, it should be considered on a priority in order to attain economic growth (Agbaje & Oloruntoba, 2018).

Revelation of fraud related to financial reporting destroys investors’ trust and lessens their participation in capital markets. However, studies about the influence of such frauds over the behavior of investment professionals remain scarce. Nevertheless, the consequences of these frauds are important for fiduciary investments because a significant volume of investments in today’s capital markets is being executed through these intermediaries. Hence, the analysis of financial reporting fraud, in preference to other forms of corporate misconduct, has been performed in this study. The purpose of this analysis is to test specifically how accounting fraud affects delegated portfolio management, rather than enumerating the cumulative cost of fraud for capital markets (Davidson et al., 2021).

The current study capitalizes on the opportunity provided by Agbaje and Oloruntoba (2018) to test the impact of financial reporting fraud on the decisions of investment professionals on behalf of all types of investors, rather than being specific to the investors of the manufacturing sector only. Taking the benefit of the study by Akinadewo et al. (2023), this study was conducted in Pakistan to see whether comparable business settings produce similar results regarding the effect of financial reporting on investment decisions. It also provides an opportunity for future research guided by the clues provided by Abdulshakour (2020), Kawugana et al. (2019), Mohammed et al. (2016), and pertaining to the effects of financial reporting on investment decisions by focusing on fraudulent financial reporting. This is achieved by using a larger sample size, applying recent statistical techniques, and covering the geographical area of Pakistan in the perspective of delegated investment decisions.

Theoretical FrameworkPakistan is particularly threatened by the emergence of accounting scandals worldwide. This is due to weak internal controls which create the risk for the misappropriation of investor money. This situation persuades investors to acquire services from professional analysts and managers to better analyze the financial health of target firms. Nevertheless, the acquisition of such services and making investments on behalf of the actual investors may cause agency conflicts.

Agency TheoryAgency theory refers to the conflict of interest between the principal (who assigns the task) and the agent (to whom any task is assigned on behalf of the principle) (Safiq & Seles, 2018). Delegated investments comprise an agency relationship where investment professionals serve as the agents of the real investors (the principle) and make investment decisions on their behalf. Hence, it is important to know the factors that may have an effect over the behavior and decisions of investment professionals.

Financial statement frauds cause damage to the reputation thus having major influence over the market of the product (Xin et al., 2018). Such frauds damage the industry as well as the economy on the whole. Therefore, there is a need for careful selection of portfolio while making investment decisions (Omidi et al., 2019).

Any delay in detecting scam makes it impossible to avoid the same. Therefore, some researchers have produced theories that make it possible to detect such scams at their early stages in order to timely prevent them from happening and causing huge losses (Maulidiana & Triandi, 2019). The fraud pentagon theory and the signaling theory are relevant in this regard.

Fraud Pentagon TheoryFraud pentagon theory developed by Marks (2012) is a modified form of fraud triangle developed earlier by Donald R. Cressey (1953). This theory contends that there are five reasons behind the occurrence of fraud in any organization including pressure, rationale, opportunity, capability, and arrogance. Fraud theories have been demonstrated to explain the reasons or stimulations of fraud in organizations (Christian & Basri, 2019). Since investment professionals make investment decisions on behalf of investors, hence it is important to know whether these stimulations of fraud are considered by professionals while managing delegated investments.

Signaling TheoryThe signaling theory is useful in transmitting the signals regarding the financial health of the company to investors. The application of the signaling theory in finance has been revealed to boost investors' inclination to invest, which consequently improves the company's profitability (Elwisam et al., 2024).

Signaling theory, initially introduced by Spence (1973), discusses the behavior of two parties when they are in possession of different information. The sender of information decides on how to communicate a particular information or signal and the receiver selects how to interpret that information. It goes on to affect the decisions made on its basis. Two types of information more important in this regard comprise the information about quality and the information about intention (Connelly et al., 2011). Hence, it is important to understand how these information signals are used by investment professionals to interpret the quality of the financial information being provided. Moreover, it is also important for investors to understand the information signals regarding the quality and intent of the investment professionals they hire to manage their investments

Literature Review and Hypotheses Development

Financial Reporting Fraud and Investment PerformanceAmalia and Triwacananingrum (2022) postulated that the financial reporting quality, which actually communicates detailed information about a company’s operations and reduces asymmetries in that information, has a direct influence on the efficiency of investments. Hence, investors need to carefully evaluate the reporting quality of financials in order to ascertain fraud free information while making investment decisions. This is because such information would resultantly affect the performance of their investments in the form of reduced returns. The assessment of financial information and making investment decisions is the responsibility of investment managers under delegated investments. This calls for the investigation of whether these professionals also find a relationship between the financial reporting fraud in the target firms and the performance of investments they are making on behalf of actual investors.

H1: Financial reporting frauds have a significant effect on the performance of investment professionals under delegated investments in Pakistan.

Financial Reporting Fraud and Investment DecisionsNumerous factors may result in imprudent decisions by investors (Gill et al., 2018). Financial information is one such factor that allows the users to forecast future cash flows while making investment decisions. Moreover, the unavailability or inaccuracy of this information may result in ineffective investment decisions by stakeholders (Berthilde & Rusibana, 2020).

Bamidele et al. (2018) evaluated the effects of financial reporting quality on investment decisions in the deposit money banks of Nigeria. The results supported the positive effects of financial reporting quality on investment decisions. It infers that the investors are more interested to invest in companies that report their financial position to stakeholders fairly. Angela and Aryancana (2017) also studied the effect of financial reporting quality on financing and investment in 15 Indonesian companies with the highest market capitalization. The results uncovered that the quality of financial reporting leads to efficient investments by reducing over and under investment. These reflections about the effects of financial reporting quality on investor decisions is of prime concern in the current study, which aims to test them for the decisions of investment professionals under delegated investments.

H2: Financial reporting frauds have a significant effect on the investment decisions of investment professionals under delegated investments in Pakistan.

Financial Reporting Fraud and the Emotions of Investment ProfessionalsFinancial fraud results in not just losing money; it also harms the trust of the victim. The emotional facet of the fraud has not been given much attention in the literature as yet. However, psychiatrists and psychologists point toward these aspects. Fraudsters play with the emotions of individuals because they consider these emotions as an influential tool to achieve their target. The feelings of distrust, guiltiness for being irresponsible, excitement, and anxiety are some of the emotional consequences of fraud. The stress gets intensified due to the fear of more frauds in the future (BioCatch, 2024).

H3: Financial reporting frauds have a significant effect on the emotions of investment professionals under delegated investments in Pakistan.

Investment Decisions and Investment Performance of Investment ProfessionalsHaidari (2023) investigated the relationship between investment decision-making and its outcomes. The outcome in the form of the success or failure of an investment depends upon the investment decisions made after a careful consideration of the available alternatives by the investors. The decision-making process becomes more difficult in the presence of various internal and external challenges and requires an evaluation of the probable outcomes that investment decisions may generate. Hence, a complex relationship has been observed between investment decisions and performance.

This research, as part of the investigation about the impact of financial reporting fraud on investment performance, also makes an attempt to test the effects of investment decisions on the performance of investment professionals in terms of risk management, cost curtailment, and returns generation.

H4: Investment decisions have a significant effect on the performance of investment professionals under delegated investments in Pakistan.

Emotions and Investment Decisions of Investment ProfessionalsIn normal circumstances, people make selections based on logic. However, the involvement of emotions can change their decisions accordingly (BioCatch, 2024). Lerner et al. (2015) analyzed the works addressing the relationship between emotions and decision-making over a period of 35 years. The findings of their study revealed that emotions help to develop vital influencers during decision-making. However, they contended that several areas pertaining to the relationship between emotions and decision-making still remain uncultivated. Sander (2024) also confirmed the role of emotions in decision-making. This study evaluates the relationship between emotions and investment decisions in the framework of delegated investments.

H5: Emotions of investment professionals have a significant effect on their investment decisions under delegated investments in Pakistan.

Emotions and Performance of Investment ProfessionalsThe environment of asset management industry is supposed to be highly emotional. This is because professional managers often face extreme pressure from their clients to outperform relative to their competitors. This pressure may result in uninformed decisions by these professionals. Conviction is an emotional determinant that encourages money managers to take decisions in stressed circumstances. It directs them towards speculative decisions that deviate greatly from the respective benchmarks and result in unstable returns. Thus, too much conviction on behalf of fund managers has been found to result in their deteriorated performance and increased risks for their respective funds (Jin et al., 2019).

The advocates of behavioral finance claim that investment decisions and the performance of investors are influenced by various behavioral factors. Numerous studies have been conducted to test the impact of behavioral factors on investment decisions and performance; however, developing economies like Pakistan still lag behind in this area (Bokhari et al., 2023). Therefore, the current study explores the influence of emotions on the performance of investment professionals in the setup of delegated investments in Pakistan.

H6: Emotions of investment professionals have a significant effect on their performance under delegated investments in Pakistan.

Mediating Effects of Emotions and Investment DecisionsInvestors’ feelings have been found to affect investment decisions and performance. Koech at al. (2020) evaluated and confirmed the significant mediating effect of investment decisions in between behavioral heuristics and financial performance in SMEs. It infers that behavioral characteristic influence investment decisions that resultantly influence investment performance. Irfan et al. (2023) also revealed that emotions influence investment decision-making and resultantly affect investment performance. This is because performance, whether return or risk, is the outcome of investment decisions. Hence, if emotional decisions are made by investment professionals, then such decisions may deviate the actual performance from the one that would have been the result of a rational decision.

H7: Investment decisions significantly mediate the relationship emotions and the performance of investment professionals under delegated investments in Pakistan

Song et al. (2024) examined and found the moderating effect of emotional intelligence on the relationship between financial literacy and financial behavior of investors. Fear, excitement, embarrassment, and stress are some of the emotional stimuli used by the those who commit fraud. If the fraudsters are able to successfully stimulate emotions, then the decision-making process becomes apprehensive and demands extra vigilance, failing which enables the scammers to get their desired outcomes (BioCatch, 2024). These outcomes may not necessarily be in the best interest of investors, thus result in the adverse performance of money managers.

Gill et al. (2018) suggested to conduct future research on the factors affecting investment decisions with the mediating effects of attitudes, biases, and emotions. Hence, this research investigates the effect of financial reporting fraud on short-term and long-term investment decisions with the mediating influence of emotions.

H8: Emotions of investment professionals significantly mediate the relationship between financial reporting frauds and investment decisions under delegated investments in Pakistan.

H8(a): Emotions of investment professionals significantly mediate the relationship between financial reporting frauds and short-term investment decisions under delegated investments in Pakistan.

H8(b): Emotions of investment professionals significantly mediate the relationship between financial reporting frauds and long-term investment decisions under delegated investments in Pakistan.

H9: Emotions of investment professionals significantly mediate the relationship between financial reporting frauds and the performance of investment professionals under delegated investments in Pakistan.

H10: Emotions and investment decisions of investment professionals simultaneously and significantly mediate the relationship between financial reporting frauds and the performance of investment professionals under delegated investments in Pakistan.

Amahalu et al. (2020) discovered that the quality of financial statements has a significant and positive effect on investment performance, measured through return on equity (ROE) by the researchers. Financial statements’ quality is essential to avoid frauds in reporting that may result in irrational investment decisions and suboptimal allocation of resources.

H11: Investment decisions significantly mediate the relationship between financial reporting frauds and the performance of investment professionals under delegated investments in Pakistan.

Research Methodology

This research is conducted to evaluate the effects of financial reporting frauds on investment decisions and the performance of investment professionals in Pakistan, with the mediating effects of the emotions of these investment professionals.

Figure 1

The above conceptual model is formed to test the causal relationship between financial reporting fraud and the performance of investment professionals in Pakistan. Davidson et al. (2021) determined the implications of the revelation of financial reporting frauds for the decisions of professional portfolio managers. The findings of the study reveals that the behavior of money managers changes as they lose their trust in those issuers of financial securities against which fraud is revealed. The above study was performed on the basis of secondary data, whereas the current study is based on primary data, that is, a survey conducted from investment professionals in Pakistan. Moreover, in the proposed framework, investment performance is the ultimate dependent variable that absorbs the effects of financial reporting fraud, emotions, and decisions of investment professionals in Pakistan.

SamplingDelegated investments are executed by investment professionals. Therefore, these professionals comprise the main source of data in the current study. The total population of this study comprises a complex blend of investment professionals serving in portfolio management, fund management, investment banking, security brokerage, and investment analysis. Therefore, their exact population in Pakistan could not be determined. Hence, a non-probability sampling technique was applied and the authors relied upon the judgmental sampling technique to extract the representative of the total population. Around 450 investment professionals working in Pakistan were approached through social media platforms, specifically LinkedIn. A total of 265 of them responded. Upon a critical analysis of the respondents by their functional titles, it was found that 248 met the criteria for inclusion.

Research InstrumentsA close-ended questionnaire comprising questions related to the study variables, including financial reporting fraud, emotions of investment professionals, investment decisions, and the performance of investment professionals in the delegated investments setup in Pakistan was used to collect data from the respondents.

The questionnaire items are structured on a five-degree Likert scale with the responses ranging over strongly disagree (1), disagree (2), neither agree nor disagree/neutral (3), agree (4), and strongly agree (5). The items for all the constructs are adopted from existing researches. Financial reporting fraud (the independent variable) is evaluated through eight questions from FF1 to FF8. These questions are adopted from Attah and Jindal (2017). The six questions used to test emotions from EMO1 to EMO6 are taken from Brundin and Gustafsson (2013). While, the questions for investment decisions taken from Ahmad (2021) were originally adapted from Mayfield et al. (2008). The items used to measure the performance of investment professionals are adopted from Fairbank et al. (2006).

Responses received through the questionnaire were then analyzed with Structure Equation Modeling (SEM) using SmartPLS4.

Respondents’ DemographicsThe demographic depiction of 248 investment professionals (respondents) included in the study provides that 94% of them are male and 6% are female. As far as risk tolerance of these professionals is concerned, 61% reported medium risk tolerance, 33% reported high risk tolerance, whereas a minimal number, that is, 6% reported low risk tolerance. Other details regarding the demographics of the respondents may be found in an earlier study conducted over the same respondents (Begum & Siddiqui, 2024).

Table 1 Descriptive Statistics and Confirmatory Factor Analysis (CFA)| Variables / Factors | Item Code | Questions | Me | SD | Outer Loadings | t | p |

|---|---|---|---|---|---|---|---|

| Financial Reporting Fraud | FF1 | I prefer to check if there is an overstatement of revenues by the company, I am intending to invest in | 3.871 | 0.870 | 0.840 | 28.628 | 0.000 |

| FF2 | I prefer to check if there is an understatement of expenses by the company, I am intending to invest in | 3.786 | 0.893 | 0.828 | 24.023 | 0.000 | |

| FF3 | I prefer to check if there is an overstatement of assets by the company, I am intending to invest in | 3.798 | 0.963 | 0.882 | 49.960 | 0.000 | |

| FF4 | I prefer to check if there is an understatement of liabilities by the company, I am intending to invest in | 3.815 | 0.910 | 0.872 | 37.006 | 0.000 | |

| FF5 | I prefer to check if there is an improper use of reserves by the company, I am intending to invest in | 3.831 | 0.891 | 0.839 | 30.774 | 0.000 | |

| FF6 | I prefer to check if there is a mischaracterization as one-time expense by the company, I am intending to invest in | 3.851 | 0.892 | 0.752 | 16.990 | 0.000 | |

| FF7 | I prefer to check if there is a misapplication of accounting rules by the company, I am intending to invest in | 3.819 | 0.922 | 0.700 | 11.145 | 0.000 | |

| FF8 | I prefer to check if there is a misrepresentation by the company, I am intending to invest in | 3.883 | 0.958 | 0.764 | 18.602 | 0.000 | |

| Emotions | EMO1 | The project makes me feel certain that it will turn out well and that I will have the ability to manage it | 3.750 | 0.731 | 0.767 | 11.851 | 0.000 |

| EMO2 | The project makes me feel that the goals will finally be met | 3.859 | 0.690 | 0.739 | 9.184 | 0.000 | |

| EMO3 | The project makes me feel energized and it offers future opportunities for success, rewards, and personal growth | 3.911 | 0.818 | 0.842 | 16.991 | 0.000 | |

| Short Term Decisions | STD2 | I engage in portfolio management activities at least twice per week | 3.407 | 1.070 | 0.751 | 11.609 | 0.000 |

| STD3 | I put at least half of my investment money into the stock market | 3.210 | 1.176 | 0.600 | 4.975 | 0.000 | |

| STD4 | I perform my own investment research instead of using outside advice | 3.637 | 0.957 | 0.769 | 14.176 | 0.000 | |

| Long Term Decisions | LTD1 | I save at least 10% of my gross earnings for investing/saving/retirement purposes | 3.669 | 1.006 | 0.735 | 14.555 | 0.000 |

| LTD2 | I have a portfolio that focuses on multiple asset classes (i.e., stocks, bonds, cash, real estate, etc.) | 3.645 | 1.045 | 0.773 | 16.773 | 0.000 | |

| LTD3 | I invest some money in long-term assets where my money will be tied up and inaccessible for years | 3.625 | 1.044 | 0.813 | 23.344 | 0.000 | |

| Performance of Investment Professionals | PERF1 | Compared to other investment professionals, I am performing better in terms of service quality | 3.532 | 0.818 | 0.683 | 11.525 | 0.000 |

| PERF2 | Compared to other investment professionals, I am performing better in terms of customer responsiveness | 3.593 | 0.832 | 0.758 | 17.086 | 0.000 | |

| PERF3 | Compared to other investment professionals, I am performing better in terms of asset liability matching | 3.488 | 0.818 | 0.745 | 13.883 | 0.000 | |

| PERF4 | Compared to other investment professionals, I am performing better in terms of risk management | 3.613 | 0.854 | 0.734 | 11.625 | 0.000 | |

| PERF5 | Compared to other investment professionals, I am performing better in terms of cost containment | 3.540 | 0.827 | 0.703 | 10.464 | 0.000 | |

| PERF6 | Compared to other investment professionals, I am performing better in terms of investment performance | 3.649 | 0.763 | 0.758 | 17.253 | 0.000 | |

| PERF7 | Compared to other investment professionals, I am performing better in terms of customer satisfaction | 3.661 | 0.817 | 0.760 | 18.203 | 0.000 |

Results

Descriptive StatisticsTable 1 illustrates the descriptive statistics and confirmatory factor analysis (CFA) of the questionnaire responses. For mean values, ‘5’ represents the maximum value, that is, ‘strongly agree’ and ‘1’ depicts the minimum value, that is, ‘strongly disagree’. The values of ‘2’, ‘3’, and ‘4’ represent ‘disagree’, ‘neither agree nor disagree/neutral’, and ‘agree’, respectively.

On average, the respondents recorded their agreement with all seven statements concerning investment performance, eight statements related to financial reporting frauds, three statements related to the emotions of investment professionals, and one item related to short-term investment decisions. Nevertheless, two items of short-term decisions received neutral responses from investment professionals. For all statements, item loadings > 0.5 reveal indicator reliability (Hulland, 1999).

Appended below are the results and analysis of the measurement model and the structural model of the study.

Table 2 Construct Reliability and Validity| Variables Factors | Items | Loadings | AVE | CR(Rho C) | Rho A |

|---|---|---|---|---|---|

| Financial Reporting Fraud | FF1 | 0.840 | 0.659 | 0.939 | 0.942 |

| FF2 | 0.828 | ||||

| FF3 | 0.882 | ||||

| FF4 | 0.872 | ||||

| FF5 | 0.839 | ||||

| FF6 | 0.752 | ||||

| FF7 | 0.700 | ||||

| FF8 | 0.764 | ||||

| Emotions | EMO1 | 0.767 | 0.615 | 0.827 | 0.750 |

| EMO2 | 0.739 | ||||

| EMO3 | 0.842 | ||||

| Short Term Decisions | STD2 | 0.751 | 0.505 | 0.752 | 0.541 |

| STD3 | 0.600 | ||||

| STD4 | 0.769 | ||||

| Long Term Decisions | LTD1 | 0.735 | 0.600 | 0.818 | 0.666 |

| LTD2 | 0.773 | ||||

| LTD3 | 0.813 | ||||

| Performance of Investment Professionals | PERF1 | 0.683 | 0.540 | 0.891 | 0.860 |

| PERF2 | 0.758 | ||||

| PERF3 | 0.745 | ||||

| PERF4 | 0.734 | ||||

| PERF5 | 0.703 | ||||

| PERF6 | 0.758 | ||||

| PERF7 | 0.760 |

Indicator items with loadings below 0.5 were removed. These items included EMO1, EMO2, EMO3, STD1, and LTD4. All item loadings > 0.5 point toward indicator reliability (Hulland, 1999). All average variance extracted (AVE) values > 0.5 indicate convergent validity (Bagozzi & Yi, 1988; Fornell & Larker, 1981). All composite reliability (CR) values > 0.7 indicate internal consistency (Gefen et al., 2000). Rho A > 0.7 for most of the constructs indicate indicator reliability except short-term decisions and long-term decisions (Henseler et al., 2015). However, these two constructs meet reliability criteria as per Chin (1998), according to which Rho C is the closer approximation assuming that parametric estimates are accurate for reflective measures.

Table 3 Discriminant Validity via HTMT Results| EMO | FF | LTD | PERF | STD | |

|---|---|---|---|---|---|

| EMO | |||||

| FF | 0.326 | ||||

| LTD | 0.329 | 0.286 | |||

| PERF | 0.256 | 0.233 | 0.443 | ||

| STD | 0.273 | 0.298 | 0.385 | 0.569 |

All values in the above HTMT results are below 0.85, thus ensuring discriminant validity.

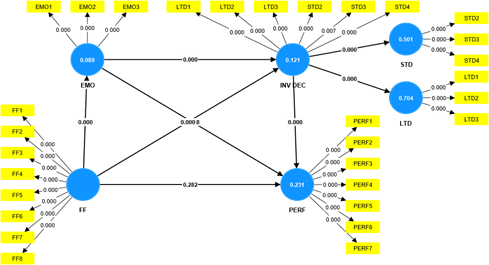

This study explores the relationship of financial reporting frauds and performance under delegated investments with the mediating effect of the emotions of investment professionals. PLS-SEM model for the current study is presented below.

Figure 2PLS Model

The tests reveals that the direct path from financial fraud to investment performance is insignificant, as indicated in Table 4 below.

Table 4 Path Coefficients| M | SD | t | p | Decision | |

|---|---|---|---|---|---|

| EMO → INV DEC | 0.208 | 0.057 | 3.577 | 0.000 | H5 Accepted |

| EMO → PERF | 0.064 | 0.068 | 0.845 | 0.398 | H6 Rejected |

| FF → EMO | 0.307 | 0.060 | 4.969 | 0.000 | H3 Accepted |

| FF → INV DEC | 0.230 | 0.063 | 3.641 | 0.000 | H2 Accepted |

| FF → PERF | 0.072 | 0.065 | 1.076 | 0.282 | H1 Rejected |

| INV DEC → PERF | 0.436 | 0.065 | 6.650 | 0.000 | H4 Accepted |

The direct path in Table 4 discloses that neither the revelation of financial fraud nor the emotions of investment professionals affect the performance of these professionals in delegated investments setup (H1). However, significant relationships can be observed between financial fraud and emotions (H3), emotions and investment decisions (H5), investment decisions and performance (H4), and financial fraud and investment decisions.

Contrary to the results of the direct path between financial fraud and performance, specific indirect effects reveal that there is full mediation of emotions and both long- and short-term investment decisions in between financial fraud revelation and the performance of investment professionals (H10), as per Zhao et al. (2010).

Table 5 Specific Indirect Effects| M | SD | t | p | Decision | |

|---|---|---|---|---|---|

| EMO → INV DEC → PERF | 0.091 | 0.029 | 3.058 | 0.002 | H7 Accepted |

| FF → EMO → INV DEC | 0.065 | 0.023 | 2.599 | 0.009 | H8 Accepted |

| FF → EMO → INV DEC → STD | 0.046 | 0.017 | 2.461 | 0.014 | H8(a) Accepted |

| FF → EMO → INV DEC → LTD | 0.054 | 0.020 | 2.567 | 0.010 | H8(b) Accepted |

| FF → INV DEC → PERF | 0.100 | 0.032 | 3.113 | 0.002 | H11 Accepted |

| FF → EMO → PERF | 0.019 | 0.022 | 0.792 | 0.428 | H9 Rejected |

| FF → EMO → INV DEC → PERF | 0.028 | 0.011 | 2.326 | 0.020 | H10 Accepted |

The recent fraud scandals have negatively affected investors’ trust over financial statements (Okike, 2011). Davidson et al. (2021) asserted that ample number of investments are being made through intermediaries. However, the effects of financial reporting fraud on the behavior of investment professionals, though an important area of study, has not been discussed in sufficient detail as yet. Therefore, this study is intended to test how the information related to the financial reporting fraud affects the decision-making and performance of investment professionals in Pakistan.

The current study reflects two types of agency layers in delegated investments. The first layer reflects the agency relationship between the company and real investors. The second layer exists between investment professionals and the real investors. This study is concerned with the second. These professionals may intentionally miscommunicate to real investors about the capability of the target firms. Moreover, they can also come under the influence of their behavioral characteristics while making investment decisions for their clients after the revelation of financial reporting fraud by the target firms.

The results of the current study confirm the findings of Shakespeare (2020), Akinadewo et al. (2023), and Kapellas and Siougle (2017), according to which financial reporting affects investment decisions. The current findings also corroborate the findings of Davidson et al. (2021) indicating that financial reporting frauds have an influence over investment decisions under delegated investments, as well as the findings of Haidari (2023) which state that investment decisions affect investment performance. The outcomes of this study do not directly support the findings of Amahalu et al. (2020), and Amalia and Triwacananingrum (2022), which expound that the quality of financial reporting affects investment performance. This is because the direct relationship between financial reporting fraud and investment performance is not significant in the current study.

Furthermore, this study adds some more findings to the existing literature indicating that financial reporting fraud has conditional influence over the performance of investment professionals under delegated investments if their relationship is mediated by emotions and short- and long-term investment decisions. It infers that the revelation of financial reporting fraud affects the investment outcomes only if the investment decisions of investment professionals are influenced by their emotions. Hence, emotions play a key role in affecting investment performance. In this way, this study also supports the outcomes of Sander (2024) and Sutejo et al. (2023) that uncovered the effects of emotions on investment decisions.

Moreover, the findings of the current study are in line with those of Irfan et al. (2023). They discovered that emotions affect investment decision-making and resultantly investment performance. These findings are helpful for actual investors because the information about fraudulent financial reporting may provide a different signal to investment professionals from what is apprehended by real investors, according to the signaling theory. Hence, the investors need to know how various information signals are being interpreted by the professionals for onward dissemination to their clients. A clear understanding of the factors that may influence investment decisions and their outcomes by real investors would provide a guideline for them to select competent professionals to manage their investments. It would also provide reasonable satisfaction to them that their funds would not be wasted.

Conclusion

Financial statistics have a significant effect on financial decisions. Investors may suffer huge losses as a result of an unhealthy investment decision made on the basis of false information. Such outcomes have been observed in the cases of Enron and WorldCom. Hence, it is necessary for the users to be able to better interpret the available financial information and identify if there are any manipulations in the given information. Manipulations in financial reporting comprise an abuse of accounting standards. Fair information helps users to make rational decisions, thus enhances the quality of capital markets in the economy. Weaker internal controls, the structure of a company’s management, flexibility in the application of accounting standards, and accrual accounting are some of the triggers behind fraudulent reporting. The inducements behind the manipulations in financial reporting include moving the share price, meeting debt covenants, and acquiring financial benefits in the form of low-cost resources and higher salaries. Financial statement frauds costs higher and are difficult to detect. Although new regulations have been introduced to prevent fraudulent reporting, however, these regulations remain inefficient, ultimately causing inappropriate allocation of resources by investors (Isa, 2011).

The results of the current study suggest the actual investors to first investigate if the manager/advisor of their funds considers the revelation of fraud in financial statements as an important aspect in making investment decisions. Investors are also advised to inquire if the manager of their funds acts under the influence of emotions while making investment decisions. This is because the investment performance of professional money managers is the combined effect of the financial reporting fraud revelation about the investee firms, the emotions of professional money managers, and the investment decisions they make for their clients.

Limitations and Future Directions

This study is limited to investment professionals working in Pakistan. More studies can be carried out in other developing countries and a comparative study may also be conducted between the developed and developing countries of the world. It is survey-based research executed via a structured questionnaire. On the other hand, conducting detailed interviews with investment professionals may also add some important qualitative insights in this regard.

CONFLICT OF INTEREST

The authors of the manuscript have no financial or non-financial conflict of interest in the subject matter or materials discussed in this manuscript.

DATA AVAILABILITY STATEMENT

The data associated with this study will be provided by the corresponding author upon request.

FUNDING DETAILS

No funding has been received for this research.

REFERENCES

- Abdulshakour, S. (2020). Impact of financial statements on financial decision-making. Open Science Journal, 5(2), 1–31. https://doi.org/10.23954/osj.v5i2.2260

- Agbaje, W. H., & Oloruntoba, S. R. (2018). An assessment of impact of financial statement fraud on profit performance of manufacturing firm in Nigeria: A study of food and beverage firms in Nigeria. European Journal of Business and Management, 10(9), 1–16.

- Ahmad, M. (2021). Does underconfidence matter in short-term and long-term investment decisions? Evidence from an emerging market. Management Decision, 59(3), 692–709. https://doi.org/10.1108/MD-07-2019-0972

- Akinadewo, I., Al-Amen, S., Dagunduro, M., & Akinadewo, J. (2023). Empirical assessment of the effect of financial reporting components on investment decisions of small and medium enterprises in Nigeria. Archives of Business Research, 11(9), 30–49. https://doi.org/10.14738/abr.119.15449

- Amahalu, N, N., & Chinyere, O. (2020). Effect of financial statement quality on investment decisions of quoted deposit money banks in Nigeria. International Journal of Management Studies and Social Science Research, 2, 99–109.

- Amalia, D. R., & Triwacananingrum, W. (2022). The disclosure effect of sustainability reporting and financial statements on investment efficiency: Evidence in Indonesia. Indonesian Journal of Sustainability Accounting and Management, 6(1), 82–93. https://doi.org/10.28992/ijsam.v6i1.512

- Angela, W., & Aryancana, R. (2017). The effect of financial reporting quality on financing and investment. Etikonomi, 16(1), 81–92. https://doi.org/10.15408/etk.v16i1.4600

- Ardianto, H., Harymawan, I., Paramitasari, Y., & Nasih, M. (2020). Financial reporting quality and investment efficiency: Evidence from Indonesian stock market. Economics and Finance in Indonesia, 66(2), 112–122. https://doi.org/10.47291/efi.v66i2.702

- Attah, M., & Jindal, P. (2017). Impact of misstatement in financial statements on investment decision making. International Journal of Scientific and Research Publications, 7(5), 145–150.

- Bagozzi, R., & Yi, Y. (1988). On the evaluation of structural equation models. Journal of the Academy of Marketing Science, 16(1), 74–94. https://doi.org/10.1007/BF02723327

- Bamidele, M., Ibrahim, J., & Omole, I. (2018). Financial reporting quality and its effect on investment decisions by Nigerian deposit money banks. European Journal of Accounting, Auditing and Finance Research, 6(4), 23–34.

- Begum, R., & Siddiqui, D. A. (2024). Corporate social responsibility disclosures & delegated investment decisions: The role of religiosity. International Journal of Social Science and Entrepreneurship, 4(2), 111–138. https://doi.org/10.58661/ijsse.v4i2.270

- Berthilde, M., & Rusibana, C. (2020). Financial statement analysis and investment decision making in commercial banks: A case of bank of Kigali, Rwanda. Journal of Financial Risk Management, 9, 355–376. https://doi.org/10.4236/jfrm.2020.94019

- BioCatch. (2024). AI, fraud & financial crime survey: AI's role in perpetrating and fighting financial crime. https://www.biocatch.com/ai-fraud-financial-crime-survey

- Bokhari, U., Sulehri, F. A., Hassan, N., & Aziz, B. (2023). Impact of allied factors on investment performance, mediating role of investment decision: Evidence from investors in Lahore. Journal of Education and Social Studies, 4(1), 27–46. https://doi.org/10.52223/jess.20234103

- Brundin, E., & Gustafsson, V. (2013). Entrepreneurs' decision making under different levels of uncertainty: the role of emotions. International Journal of Entrepreneurial Behaviour & Research, 19(6), 568–591. https://doi.org/10.1108/IJEBR-07-2012-0074

- Chin, W. W. (1998). Issues and opinion on structural equation modeling. MIS Quarterly, 8(2), 7–16.

- Christian, N., & Basri, Y. (2019). Analysis of fraud triangle, fraud diamond and fraud pentagon theory to detecting corporate fraud in Indonesia. The International Journal of Business Management and Technology, 3(4), 1–6.

- Connelly, B., Certo, S., Ireland, R., & Reutzel, C. (2011). Signaling Theory: A review and assessment. Journal of Management, 37(1), 39–67. https://doi.org/10.1177/0149206310388419

- Cressey, D. R. (1953). Other people's money: A study of the social psychology of embezzlement. Free Press.

- Davidson, R., Pirinsky, C., & Zhang, H. (2021). Financial reporting fraud and delegated investment. http://dx.doi.org/10.2139/ssrn.3763194

- Ebaid, I. S. (2023). Board characteristics and the likelihood of financial statements fraud: Empirical evidence from an emerging market. Future Business Journal, 9(47), 1–12. https://doi.org/10.1186/s43093-023-00218-z

- Elwisam, Muhani, Ria, Digdowiseiso, K., Kartini, Juliandi, D., & Saputra, D. (2024). Implementation of signaling theory in financial management: A bibliometric analysis. RGSA – Revista de Gestão Social e Ambiental, 18(3), 1–13. https://doi.org/10.24857/rgsa.v18n3-092

- Fairbank, J., Labianca, G., Steensma, H., & Metters, R. (2006). Information processing design choices, strategy, and risk management performance. Journal of Management Information Systems, 23(1), 293–319. http://dx.doi.org/10.2753/MIS0742-1222230110

- Fornell, C., & Larcker, D. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 18(1), 39–50.

- Gefen, D., Straub, D., & Boudreau, M.-C. (2000). Structural equation modeling and regression: Guidelines for research practice. Communications of the Association for Information Systems, 4(7), 1–77. https://doi.org/10.17705/1CAIS.00407

- Gill, S., Khurshid, M. K., Mahmood, S., & Ali, A. (2018). Factors effecting investment decision making behavior: The mediating role of information searches. European Online Journal of Natural and Social Sciences, 7(4), 758–767.

- Haidari, M. N. (2023). Impact of decision-making on investment performance: A comprehensive analysis. Journal of Asian Development Studies, 12(4), 980–990. https://doi.org/10.62345/jads.2023.12.4.78

- Henseler, J., Ringle, C., & Sarstedt, M. (2015). A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science, 43, 115–135. https://doi.org/10.1007/s11747-014-0403-8

- Hulland, J. (1999). Use of partial least squares (pls) in strategic management research: A review of four recent studies. Strategic Management Journal, 20, 195–204. https://doi.org/10.1002/(SICI)1097-0266(199902)20:2<195::AID-SMJ13>3.0.CO;2-7

- International Auditing and Assurance Standards Board. (2023, October 13). Handbook of international quality management, auditing, review, other assurance, and related services pronouncements. https://www.iaasb.org/publications/2022-handbook-international-quality-management-auditing-review-other-assurance-and-related-services

- Irfan, M., Adeel, R., & Malik, M. S. (2023). The impact of emotional finance, and market knowledge and investor protection on investment performance in stock and real estate markets. SAGE Open, 13(4), 1–18. https://doi.org/10.1177/21582440231206900

- Isa, T. (2011). Impacts and losses caused by the fraudulent and manipulated financial information on economic decisions. Review of International Comparative Management, 12(5), 929–939.

- Jin, L., Taffler, R., Eshraghi, A., & Tosun, O. (2019). Fund manager conviction and investment performance. International Review of Financial Analysis, 71, 1–15. https://doi.org/10.1016/j.irfa.2020.101550

- Kapellas, K., & Siougle, G. (2017). Financial reporting practices and investment decisions: A review of the literature. Industrial Engineering & Management, 6(4), 1–9. https://doi.org/10.4172/2169-0316.1000235

- Kawugana, A., Johnson, A., & Ade, F. A. (2019). Role of financial statement in investment decision making. International Journal of Management Science Entrepreneurship, 9(5), 123–139.

- Koech, A., Cheboi, J., & Koske, N. (2020). Mediating effect of investment decisions between overconfidence heuristic and financial‐performance of small, and medium enterprises in Nairobi, Kenya. Journal of Business Management and Economic Research, 4(2), 186–198. https://doi.org/10.29226/TR1001.2020.193

- Le, H., Lai, C.-P., Phan, V., & Pham, V. (2024). Financial reporting quality and investment efficiency in manufacturing firms: The role of firm characteristics in an emerging market. Journal of Competitiveness, 16(1), 62–78. https://doi.org/10.7441/joc.2024.01.04

- Lerner, J., Li, Y., Valdesolo, P., & Kassam, K. (2015). Emotion and decision making. Annual Review of Psychology, 66(1), 799–823. https://doi.org/10.1146/annurev-psych-010213-115043

- Marks, J. (2012, June 17–22). The mind behind the fraudsters crime: Key behavioral and environmental elements [Discussion Session]. 23rd ACFE Global Fraud Conference, Orlando, The USA.

- Maulidiana, S., & Triandi, T. (2019). Analysis of fraudulent financial reporting through the fraud pentagon theory. Advances in Economics, Business and Management Research, 143, 214–219. https://doi.org/10.2991/aebmr.k.200522.042

- Mayfield, C., Perdue, G., & Wooten, K. (2008). Investment management and personality type. Financial Services Review, 17, 219–236. https://doi.org/1057-0810/08/$

- Mesioye, O., & Bakare, I. (2024). Evaluating financial reporting quality: metrics, challenges, and impact on decision-making. International Journal of Research Publication and Reviews, 5(10), 1144–1156. https://doi.org/10.55248/gengpi.5.1024.2735

- Mohammed, A., Abubakar, H., & Lawal, M. D. (2016). The effects of financial reporting on investment decision making by banks In Nigeria. International Journal of Research in Finance and Marketing, 6(4), 21–51

- Okike, E. (2011). Financial reporting and fraud. In S. Idowu & C. Louche (Eds.), Theory and practice of corporate social responsibility (pp. 229–262). Springer.

- Omidi, M., Min, Q., Moradinaftchali, V., & Piri, M. (2019). The efficacy of predictive methods in financial statement fraud. Discrete Dynamics in Nature and Society, 2019 (1), 1–12. https://doi.org/10.1155/2019/4989140

- Safiq, M., & Seles, W. (2018, August 8–9). The effects of external pressures, financial targets and financial distress on financial statement fraud [Paper presentation]. 5th Annual International Conference on Accounting Research (AICAR 2018), Manado, Indonesia.

- Sander, J. C. (2024). The role of emotions in investment decisions: The effects of vividness of a crowdfunding campaign video [Master's thesis, Leopold-Franzens-Universität Innsbruck]. -Universität Innsbruck Repository. https://digital.obvsg.at/9479661

- Shahzad, F., & Rehman, I. (2019). The influence of financial reporting quality and audit quality on investment efficiency: Evidence from Pakistan. International Journal of Accounting & Information Management, 27(4), 600–614. http://dx.doi.org/10.1108/IJAIM-08-2018-0097

- Shakespeare, C. (2020). Reporting Matters: The real effects of financial reporting on investing and financing decisions. Accounting and Business Research, 50(5), 425–442. https://doi.org/10.1080/00014788.2020.1770928

- Song, C., Pan, D., Ayub, A., & Cai, B. (2024). The interplay between financial literacy, financial risk tolerance, and financial behaviour: The moderator effect of emotional intelligence. Psychology Research and Behavior Management, 16, 535–548. https://doi.org/10.2147/PRBM.S398450

- Spence, M. (1973). Job market signaling. The Quarterly Journal of Economics, 87(3), 355–374. https://doi.org/10.2307/1882010

- Sutejo, B. S., Sumiati, Wijayanti, R., & Ananda, C. F. (2023, March 15–16). Five basic human emotions and investment decisions on generation Z in Surabaya-Indonesia [Paper presentation]. Proceedings of the 20th International Symposium on Management (INSYMA 2023), Bangkok, Thailand. https://doi.org/10.2991/978-94-6463-244-6_3

- Xin, Q., Zhou, J., & Hu, F. (2018). The economic consequences of financial fraud: Evidence from the product market in China. China Journal of Accounting Studies, 6(1), 1–23. https://doi.org/10.1080/21697213.2018.1480005

- Zenzerović, R., & Šajrih, J. (2023). Financial statements fraud identifiers. Economic Research-Ekonomska Istraživanja, 36(3), 1–13. https://doi.org/10.1080/1331677X.2023.2218916

- Zhao, X., Lynch Jr, J., & Chen, Q. (2010). Reconsidering Baron and Kenny: Myths and truths about mediation analysis. Journal of Consumer Research, 37(2), 197–206. https://doi.org/10.1086/651257