| Review | Open Access |

|---|

Exploring the Role of Fintech, Green Finance, and CSR on Environmental Performance with the Mediating Role of Green Innovation |

|

|---|

![]() Fareeha Waseem1* ,

Fareeha Waseem1* ,

![]() Veera Salman2 , and

Veera Salman2 , and

![]() Zahra Batool1

Zahra Batool1

1Hailey College of Banking & Finance, University of the Punjab, Lahore, Pakistan

2Department of Accounting & Finance, Kinnaird College for Women, Lahore, Pakistan

This study aims to investigate the influence of green finance, corporate social responsibility, and fintech on the environmental performance of banks in the context of sustainability. Additionally, it seeks to examine the mediating role of green innovation. Primary data was collected using convenience random sampling through a structured questionnaire from 400 respondents working in the banking sector of Pakistan. Through multiple linear regression, it was found that CSR, green finance, and fintech adoption play a significant role in driving the banks’ environmental performance. Additionally, Hayes Process showed that green innovation significantly but partially mediated these relationships. The outcomes support the resource-based theory, implying that possessing and implementing strategic resources can boost the performance of banks and extend the application of the above theory in the realm of environmental sustainability. Banks and policymakers can also benefit from the results of this research.

JEL Codes: Q56, G21, M48, O33

1. INTRODUCTION

Financial mechanisms, especially the ones established and adopted by banks to ensure environmental sustainability, have received considerable recognition, especially amid increasing environmental concerns. This has led policymakers around the world to focus on reconciling economic development with environmental protection (Tan et al., 2025). Theoretically, the widely discussed themes include environmental performance, green financing, green innovation, corporate social responsibility, and financial technology. At the practical level, banks have started incorporating green initiatives to boost their environmental performance (Desai & Patel, 2025). The banking sector does not contribute directly to environmental pollution. However, if it finances those who play a major role, then its effect is indirect (Aslam & Jawaid, 2023). Therefore, when they opt not to promote the polluting sector, their own reputation and environmental performance are enhanced (Riyanti et al., 2025).

Environmental performance is defined as the impact of banks’ actions on the natural environment (Klassen & Whybark, 1999). Increasing this performance is important and is carried out by adopting eco-friendly practices in banking operations. In this regard, fintech is one of the contemporary factors that help to promote effective, efficient, and sustainable financial services (Sadiq et al., 2024). These eco-friendly financial products and services aid in minimizing carbon emissions (Ashta, 2023). Employing financial technology in banking operations has led to improved performance and competitiveness in this sector (Dwivedi et al., 2021).

Fintech has been identified as a possible enabler for improving long-term growth (Subanidja et al., 2022). Several studies have explored the role of financial technologies, green financing, and green innovation, providing information about their overall impact on environmental sustainability (Liu et al., 2022). The literature also highlights the crucial role of fintech in promoting green finance (Xue et al., 2022). However, despite the presence of such significant studies, several deficiencies are found in the peer-reviewed literature which the current study seeks to address.

Green finance is a mechanism used by the banks to channelize finances to other sectors, while carrying social, economic, and ecological benefits (Wang & Zhi, 2016). Hence, when banks provide investment to eco-friendly projects, they indirectly promote environmental sustainability. This boosts their environmental and financial performance, as well as the economy’s sustainability profile (Chen et al., 2022; Indriastuti & Chariri, 2021). Whether it is in the form of impact investments, green bonds, sustainable funds, or microfinance, green finance plays a significant role in improving the environmental performance of banks (Guang-Wen & Siddik, 2022). Similar to green finance, green innovation is also a key enabler of environmental performance (Kraus et al., 2020). It encapsulates the integration of green technologies and green banking to assist operations and boost environmental performance (Dai et al., 2022). Since it minimizes the ill-effects of banking operations on the environment by reducing carbon emissions, it promotes better financial and environmental performance (Ali et al., 2021). Research suggests that significant investigation is needed into the mediated processes and particular tactics banks might use to improve their performance towards the environment via implementing fintech and green financing methodologies. In the same vein, corporate social responsibility (CSR) also helps to ensure banks’ contribution towards the environment (Dai et al., 2022). It holds banks accountable to the stakeholders and such social and regulatory pressure requires them to implement CSR initiatives to promote environmental sustainability (Guang-Wen & Siddik, 2022). While several studies have concentrated on the impact of CSR on financial performance, there is a lack of studies especially investigating the interplay of these factors within the banking industry, while addressing the deficiencies identified by Dai et al. (2022) and Zheng et al. (2021). Moreover, the existing research mostly examines the impact of these factors in industrialized economies. Hence, it is crucial to comprehend how fintech affects sustainability procedures within financial institutions of developing nations (Riyanti et al., 2025).

The integration of financial technology with the long-term viability performance of banking organizations is enhanced by extending green finance and introducing innovative green technologies (Chen et al., 2022). The current study makes three contributions to the literature. Firstly, it examines the role of financial technology adoption, green financing, corporate social responsibility, and green innovation in driving environmental performance in the banking sector. This covers the technological, environmental, and financial dimensions important for banks that aim to boost their efficiency. The banks leverage fintech and green innovation which serve as technological resources, while simultaneously achieving operational/green financing motives, i.e., the financial aspects, and fulfilling their ecological responsibility, covering the environmental dimension. Secondly, it provides a new lens by exploring the mediating role of green innovation. Green innovation is studied as a dual-dimensional construct where banks incorporate it for internal operational transformation (both product innovation and process innovation) as well as its financing/investing role; they implement it for external and environmentally responsible financing to promote such innovations in other sectors. Thirdly, it determines the aforementioned relationship in the context of a developing country’s banking sector to provide economy-specific insights. In Pakistan, the adoption of financial technology, green innovation, and green finance is still in its nascent phase. Moreover, CSR is not yet a mandatory requirement, rather it is voluntarily opted for. Technological readiness, environmental governance, and regulatory support keep evolving; therefore, under the constraints of still-developing infrastructure and awareness in users, aligning technological, financial, and environmental goals to achieve sustainability objectives serves to provide contextual and empirical insights. This would aid to extend the theoretical aspect towards how the banks of developing countries utilize their limited resources under institutional pressures. Moreover, they face a lack of awareness about green financial products and how to translate them into environmental performance. Hence, the scope of this research covers the environmentally sustainable practices and performance of the banking sector in Pakistan. Accordingly, the results offer practical insights and the stakeholders can benefit from them by incorporating sustainable practices in the banks. Doing so would lead the banks to offer financing to environmentally sustainable goods-making and services-providing industries. Moreover, they would be able to conform to international sustainability standards and support the economy’s overarching environmental objectives. So, policymakers and regulators may also play their role in promoting a banking system that works to enhance sustainable economic development.

The remaining paper is structured as follows: Section 2 reviews the literature and builds hypotheses, Section 3 outlines the research methodology, Section 4 explains and discusses the results, and Section 5 concludes the study.

Literature Review

Theoretical Framework: Resource-Based View (RBV)The resource-based view (RBV) states that organizations enjoy a competitive advantage if they use valuable, scarce, and unique resources with no existing substitutes (Barney, 1991). According to this theory, such resources translate into better performance (Bai & Lin, 2022). In this regard, this research considers fintech adoption, green finance, corporate social responsibility, and green innovation as strategic resources that improve environmental performance.

Environmental Performance of BanksThe environmental performance (EP) of banks shows their commitment to sustainable practices (Gidage & Bhide, 2024). The banking sector is considered a key stakeholder as it provides financing to all other sectors, thus it can affect their environmental performance as well (Rehman et al., 2021). EP is the ability of organizations to effectively manage their environmental impact through innovative green practices and CSR initiatives (Xu et al., 2024). Lower levels of greenhouse gas emissions, measures to reduce pollution, reduction of waste, initiatives to recycle products, training of employees towards sustainable daily practices, supplier evaluations, instances of non-compliance with environmental regulations, and the number of environmentally certified locations are some of the indicators that can be used to evaluate banks’ environmental performance (Chen et al., 2022). Measuring the environmental performance of banks is important because they play a substantial role as intermediaries between investors and borrowers in the monetary system (Bimha & Nhamo, 2017). Nevertheless, one of the most important metrics used in industry is the efficient use of resources. Hence, banks need to adopt financial technology and other green practices to reduce their negative impact on the environment (Badrous et al., 2025).

Fintech Adoption and Environmental PerformanceThe banking sector has been greatly influenced by the rise of fintech, which has brought a significant change in traditional banking operations and models (Sajid et al., 2023). Even though the integration of technology into the banking sector is not new, still significant advancements have been made only recently (Asif et al., 2023). The adoption of fintech to boost environmental performance can be widely observed in the banking sector (Naz et al., 2023). The deployment of such ecologically friendly technologies expedites their operations while ensuring better environmental performance (Yan et al., 2022). A recent study evaluated the impact of fintech adoption on the environmental performance of commercial banks and found that with the increase in the use of such technologies, environmental performance also increases (Badrous et al., 2025). Similarly, another study found a significant, positive relationship between the two using structural equation modeling (SEM) and supported the results via necessary condition analysis, which showed fintech adoption as an indispensable factor affecting environmental performance (Yuan, 2025). Another study found that banks using fintech report enhance their environmental performance, which gives them a competitive edge over non-users (Rehman et al., 2021). This is because integration technology helps to reduce paper wastage, carbon emissions, and energy consumption, thereby leading to a lesser negative impact on the environment (Dong & Yu, 2023). On the other hand, the negative effects of fintech adoption in banks have been reported as well (Lisha et al., 2023), leading to inconclusive results. Therefore, the resource-based theory posits that financial technology is a strategic resource. So, the current study aims to test the following hypothesis:

H1: Fintech adoption significantly impacts the environmental performance of banks.

Green Finance and Environmental PerformanceGreen finance encompasses financial systems, products, and services that are specifically designed to promote sustainable economic growth and development (Yu et al., 2021). According to Zheng et al. (2021), it encourages financial tools and investment techniques that facilitate environmentally sustainable initiatives. Additionally, it prioritizes environmentally-friendly initiatives that lessen the effects of climate change (Desalegn & Tangl, 2022). In contrast to polluting sectors, it may effectively distribute and modify the financial resources allocated to green businesses, enabling them to obtain better credit resources (Cao et al., 2021). Along with its role in financing climate change projects in compliance with global conventions and structures, the importance of green financing in achieving equitable social and ecological growth has been highlighted (Hu & Zheng, 2021). The reputation and environmental performance of banks increase when they provide loans for ecologically-friendly projects (Rehman et al., 2021; Zheng et al., 2021). Badrous et al. (2025) also validated these results, highlighting that banks can align their credit/lending strategies with environmental values using green finance. Thus, green finance remains a valuable resource for the banks as per the resource-based theory. So, the study aims to test the following hypothesis:

H2: Green finance significantly affects the environmental performance of banks.

Corporate Social Responsibility and Environmental PerformanceCSR entails a company’s dedication to sustainable operations, taking into account diverse stakeholders (Xu, 2025). Proper implementation of CSR initiatives results in increased business reputation and stakeholders’ confidence (Chen et al., 2022). Hence, as part of their strategic decision-making, organizations give back to the society by playing their part in resolving social and environmental challenges (Bruna & Lahouel, 2022). The banks that practice CSR tend to work on environmental issues in addition to their core businesses (Al-Ali & O’Mahony, 2025). A study found that banks fostering CSR activities tend to develop a pro-environmental behavior, which motivates them to reduce their ecological footprint, thus boosting their environmental performance (Ahmad et al., 2021). A similar study reported that CSR increases environmental performance (Dai et al., 2022). It was further explained in another study that undertaking CSR activities helps to attract investors. They invest more which increases the market share as well as the environmental performance of the banks (Gazi et al., 2025). Additionally, green finance projects implemented in parallel to the banks’ corporate social responsibility enhance their reputation as responsible corporate entities (Wang et al., 2022). Therefore, corporate social responsibility acts as a strategic resource that integrates social and environmental considerations into the banks’ lending and investment decisions. So, this study aims to assess the following hypothesis:

H3: Corporate social responsibility significantly impacts the environmental performance of banks.

Green Innovation and Environmental PerformanceGreen innovation, as defined in the context of the banking sector, is the set of activities where corporate processes are carried out while considering sustainability. It also implies the conceptualization and launching of green financing products. Furthermore, it means the use of energy-efficient technology in banking operations (Liu, 2024). Green technology, online banking, and green banking are some of the technological advancements in this regard (Dai et al., 2022). They explained that such innovations help banks to boost their environmental and financial performance. They also reported a direct and significant impact of green innovation on the environmental performance of financial institutions, along with its mediating role; hence, extending the study by Kraus et al. (2020). A review study also reported similar results and elaborated that green innovation translates into better corporate sustainability (Abbas & Shahid, 2024). Guang-Wen and Siddik (2022) found a partial mediation of green innovation between fintech adoption and the environmental performance of banking institutions. Green innovation plays the role of a strategic resource to mitigate their adverse environmental impacts. Financial institutions may facilitate green innovation by offering capital and consultancy to companies that adopt sustainable practices. Based on the previous literature, the following hypothesis is posited to evaluate it in the context of a developing country:

H4: Green innovation significantly influences the environmental performance of banks.

Research Methodology

Research DesignThis study empirically investigates the role of fintech adoption, green finance, and corporate social responsibility in determining the banks’ environmental performance, while also testing if green innovation mediates the above relationship. In this regard, a non-probability, convenience sampling technique was opted for because the study aimed to assess the implementation of fintech, green finance, CSR, and green innovation practices through those directly involved with such operations. Furthermore, due to practical challenges and confidentiality restrictions pertinent to acquiring data from all the employees, this sampling technique served as a suitable, practical option from a methodological point of view. Additionally, a diverse set of banks was considered to maintain the heterogeneity of responses. A total of 400 employees from the list of banks provided in Table 1 served as the participants of the current study.

Table 1

Sample Selection

|

Types of Banks |

Banks Under Study |

|---|---|

|

Public Sector Banks |

National Bank of Pakistan (NBP), The Bank of Punjab (BOP), Sindh Bank Limited, The Bank of Khyber (BOK) |

|

Private Sector Banks |

Habib Bank Limited (HBL), United Bank Limited (UBL), MCB Bank Limited (MCB), Allied Bank Limited (ABL), Askari Bank, Bank Alfalah, Faysal Bank, Standard Chartered Bank (Pakistan), Habib Metropolitan Bank, JS Bank, Bank of Punjab, Silk Bank, Summit Bank, Meezan Bank (Islamic Bank) |

|

Foreign Bank operating in Pakistan |

Standard Chartered Bank |

|

Islamic Banks |

Meezan Bank, Bank Islami Pakistan Limited, Al Baraka Bank, Dubai Islamic Bank Pakistan, MIB - MCB Islamic Bank |

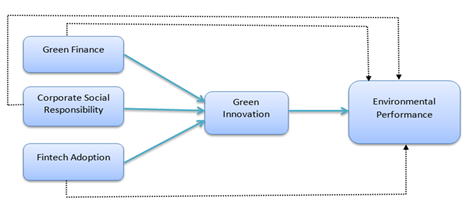

The conceptual framework of this study is shown below in Figure 1.

Figure 1

Conceptual Framework

As this study builds on explanatory research design, a five-point Likert scale-based (1: strongly agree and 5: strongly disagree) structured questionnaire was used as a tool to collect primary data, while both online and physical distribution modes were leveraged. To retain the study’s reliability and validity, questionnaire items were extracted from previous studies. However, to further ensure content clarity, a pre-test with a few employees was also conducted. Cronbach’s alpha value established high reliability as all the variables exhibited values above 0.7. Hence, as depicted by Table 2, the survey instrument consistently captured the measures under consideration.

Table 2

Reliability Test

|

Cronbach's Alpha |

N of Items |

|---|---|

|

.776 |

4 |

The Kaiser-Meyer-Olkin (KMO) test and Bartlett’s test of sphericity were conducted as part of the factor analysis, which confirmed sampling adequacy and factorability. The factor loadings grouped related items under distinct constructs, verifying fintech, CSR, green finance, and green innovation as key drivers of environmental performance. The results in Table 3 show that the value of KMO is high, implying sampling adequacy (Nkansah, 2018). While, the resulting value of Bartlett’s test is statistically significant, indicating that correlation matrix is not the identity matrix and meaningful factors can be extracted from the constructs (Bartlett, 1935). Hence, the data is suitable for analysis.

Table 3

KMO and Bartlett’s Test

|

Kaiser-Meyer-Olkin Measure of Sampling Adequacy |

.907 |

|

|---|---|---|

|

Bartlett's Test of Sphericity |

Approx. c2 |

4700.019 |

|

df |

406 |

|

|

Sig. |

.000 |

|

Statistical Package for Social Sciences (SPSS) was used to process the results. Due ethical considerations in data collection, handling, and reporting were followed.

Results

Demographic ProfileTable 4 provides the demographic profile of the respondents.

Table 4

Respondents’ Demographic Profile

|

Demographics |

Categories |

Percentages |

|---|---|---|

|

Gender |

Male |

48 |

|

Female |

52 |

|

|

Age |

Below 25 years |

16 |

|

25 – 35 years |

12 |

|

|

36 – 45 years |

56 |

|

|

Above 45 years |

16 |

|

|

Education Level |

Bachelor |

24 |

|

Masters |

40 |

|

|

PhD |

20 |

|

|

Others |

16 |

|

|

Position in Bank |

Junior Staff Member |

32 |

|

Middle Staff Member |

44 |

|

|

Senior Staff Member |

24 |

|

|

Work Experience |

Less than one year |

28 |

|

1 – 2 years |

32 |

|

|

3 – 5 years |

24 |

|

|

Above 5 years |

16 |

|

|

Monthly Income |

Below 30,000pkr |

20 |

|

30,000-55,000pkr |

36 |

|

|

56,000-81,000pkr |

28 |

|

|

Above 81,000pkr |

16 |

Descriptive statistics offer insights into the general patterns and help to understand the prevalence of fintech adoption, CSR, and green finance within the sampled banks. The results in Table 4 show that the responses of participants ranged between 1 and 5, from neutral to disagreement. This implies that in the selected sample of banks whose employees were asked about green finance, CSR, fintech adoption, green innovation, and environmental performance of their respective banks, it was found that these practices are less common in Pakistan’s banking sector. On the other hand, there is a possibility that either the staff’s perception in this regard is not supportive or they are not well aware of their respective bank’s initiatives.

Table 5

Descriptive Statistics

|

Variables |

Mean |

SD |

Min |

Max |

|---|---|---|---|---|

|

Green Finance |

3.9971 |

0.67119 |

2.17 |

5.00 |

|

CSR |

3.8286 |

0.65383 |

1.71 |

5.00 |

|

Fintech Adoption |

4.0560 |

0.70335 |

1.60 |

5.00 |

|

Green Innovation |

3.8131 |

0.79052 |

1.00 |

5.00 |

|

Environmental Performance |

3.7687 |

0.73930 |

1.33 |

5.00 |

Regression analysis was employed to determine the effect size (β coefficients) of each predictor variable on environmental performance. The results in Table 6 show that 43.4% of the variance in environmental performance is explained by the given predictors (R2 = 0.434). Additionally, the overall model is also statistically significant (p-value of F change = 0.000 < 0.05). Furthermore, the findings report no issue of autocorrelation as per the Durbin-Watson test (dwstat = 1.87 < 2).

Table 6

Model Summary

|

R |

R² |

Adjusted R² |

SE |

R² Change |

F Change |

df1 |

df2 |

p |

Durbin Watson |

|---|---|---|---|---|---|---|---|---|---|

|

.659 |

.434 |

.428 |

.55894 |

.434 |

75.761 |

4 |

395 |

.000 |

1.872 |

The results in Table 7 show that the regression model is statistically significant, with F (4, 395) = 75.76, p < 0.001. Hence, the findings suggest that green innovation, fintech adoption, CSR, and green finance can explain a significant portion of the variation in banks’ environmental performance.

Table 7

ANOVA Results

|

Source |

SS |

df |

MS |

F |

p |

|---|---|---|---|---|---|

|

Regression |

94.68 |

4 |

23.67 |

75.76 |

< .001 |

|

Residual |

123.41 |

395 |

0.31 |

||

|

Total |

218.08 |

399 |

The regression coefficients in Table 8 show magnitude and direction, as well as the significance for each predictor. Firstly, FA influences EP significantly (β = 0.36, t = 7.12, p < 0.001). This implies that the banks with a higher level of fintech adoption tend to do better with respect to environmental performance. This is because the integration of digital platforms or other financial technology serves to improve efficiency and reduce carbon footprint. Further, it also attracts environmentally responsible investors. Secondly, the table shows that GF significantly affects EP (β = 0.30, t = 5.36, p < 0.001), indicating that the banks highly involved in green financing allocate their capital to environmentally friendly opportunities, which also improves their reputation in the banking sector. Hence, green financing leads to better environmental performance and sustainability profile. Thirdly, the results show that CSR does not significantly influence the EP of Pakistani banks (β = 0.02, t = 0.41, p > 0.001). This shows that CSR remains a symbolic activity, since it is not directly integrated into core operations and remains rather external-facing. Hence, it does not lead to environmental performance. Lastly, GI also remains an insignificant factor for EP (β = 0.09, t = 1.66, p > 0.001). The reason could be that green innovation is still in its nascent stages in Pakistan’s banking sector. The benefits of such innovation take longer to materialize. Hence, even though it might have the potential to improve banks’ environmental performance, it still requires institutional support and policy frameworks.

Table 8

Regression Coefficients

|

Predictor |

B |

SE |

β |

t |

p |

VIF |

|---|---|---|---|---|---|---|

|

Constant |

0.54 |

0.19 |

2.76 |

.006 |

||

|

FA |

0.38 |

0.05 |

.36 |

7.12 |

.000 |

1.77 |

|

GF |

0.33 |

0.06 |

.30 |

5.36 |

.000 |

2.14 |

|

CSR |

0.03 |

0.06 |

.02 |

0.41 |

.679 |

2.03 |

|

GI |

0.08 |

0.05 |

.09 |

1.66 |

.097 |

1.80 |

To test whether green innovation mediates the impact of fintech adoption, green finance, and CSR on banks’ environmental performance or not, Hayes PROCESS Model 4 was employed.

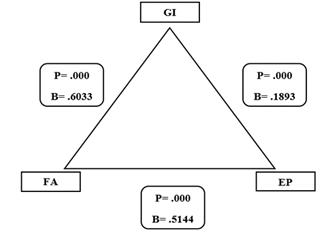

Mediation of Green Innovation Between Fintech Adoption and Environmental PerformanceTable 9 shows that FA significantly impacts EP (β = 0.5114, p < 0.0001), indicating that with fintech adoption, the banks’ environmental performance also increases. FA also exerts an indirect effect on EP through GI (indirect effect = 0.1142, 95% CI = 0.0533 – 0.1890). As the interval does not include zero, these findings imply that green innovation partially mediates the relationship between fintech adoption and environmental performance. So, the results show that banks that adopt fintech also consider innovative and sustainable measures to improve environmental outcomes. Hence, the impact of fintech adoption is boosted by green innovation initiatives, which explains the partial mediation.

Table 9

Mediation FA-GI-EP

|

Path |

Coeff |

SE |

t |

p |

95% CI |

|---|---|---|---|---|---|

|

LL, UL |

|||||

|

FA → GI (a) |

0.6033 |

0.0475 |

12.6926 |

.0000 |

0.5099, 0.6968 |

|

GI → EP (b) |

0.1893 |

0.0437 |

4.3322 |

.0000 |

0.103, 0.275 |

|

FA → EP (c′) |

0.5114 |

0.0491 |

10.4156 |

.0000 |

0.415, 0.608 |

|

FA → GI → EP (ab) |

0.1142 |

— |

— |

— |

0.0533, 0.1890 |

The results depicted in Figure 2 show that all paths are significant. This indicates the existence of partial mediation between fintech adoption and banks’ environmental performance. Therefore, the banks which have adopted fintech also have the mindset to incorporate green innovation. This ultimately improves their environmental performance. However, it does not mean that fintech adoption alone is not sufficient; rather, it helps to improve operational efficiencies by promoting eco-friendly financial practices.

Figure 2

Mediation between FA and EP

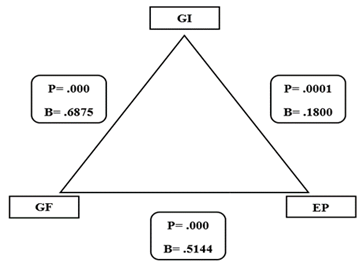

Mediation of Green Innovation between Green Finance and Environmental Performance

Table 10 delineates the significant direct effect of GF on EP (β = 0.5114, p < 0.0001), indicating that green finance independently contributes towards improving EP. The indirect effect is also significant as there is no zero in the confidence interval (indirect effect = 0.1238, 95% CI = 0.0493 – 0.2083). Thus, GI also partially mediates the relationship between GF and EP, facilitating the aforementioned direct relationship. This indicates that green finance directly enhances environmental performance. However, its influence is further enriched when paired with green innovation. Hence, having a green, innovative culture, along with the provision of green finance, is crucial to banks’ environmental performance.

Table 10

Mediation GF-GI-EP

|

Path |

Coeff |

SE |

t |

p |

95% CI |

|---|---|---|---|---|---|

|

LL, UL |

|||||

|

GF → GI (a) |

0.6875 |

0.0479 |

14.3417 |

.0000 |

0.5932, 0.7817 |

|

GI → EP (b) |

0.1800 |

0.0464 |

3.8839 |

.0001 |

0.0889, 0.2712 |

|

GF → EP (c′) |

0.5114 |

0.0546 |

9.3675 |

.0000 |

0.4041, 0.6188 |

|

GF → GI → EP (ab) |

0.1238 |

— |

— |

— |

0.0493, 0.2083 |

Figure 3

Mediation between GF and EP

As per the results shown in Figure 3, all three relationships, i.e., GF-EP, GF-GI, and GI-EP, are found to be statistically significant. This suggests that green innovation partially mediates the relationship between green finance and environmental performance. Hence, the banks providing green financing options also foster a mindset of innovative green financial products and services. This improves their environmental performance by reducing their ecological footprint. However, the relationship between GF and EP also holds statistically significant even in the absence of GI. This underscores the dual significant impact where green finance drives environmental performance, both directly and indirectly.

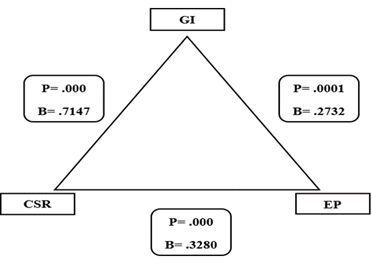

Mediation of Green Innovation between CSR and Environmental PerformanceTable 11 shows that CSR significantly affects EP (β = 0.3280, p < 0.0001). This indicates that CSR activities carried out by banks translate into better environmental performance. Moreover, the 95% confidence interval for the mediating role of GI between CSR and EP (0.1140, 0.2904) does not include zero. This confirms its statistical significance, indicating that GI is only a partial mediator, which enhances the benefits of CSR for EP. This result tells the importance of CSR-driven green innovation, which serves to optimize the impact of corporate social responsibility on environmental performance.

It also indicates that the environmental benefits of banking institutions can be maximized if they commit to CSR and simultaneously work on green innovation.

Table 11

Mediation CSR-GI-EP

|

Path |

Coeff |

SE |

t |

p |

95% CI |

|---|---|---|---|---|---|

|

LL, UL |

|||||

|

CSR → GI (a) |

0.7147 |

0.0489 |

14.6194 |

.0000 |

0.6186, 0.8108 |

|

GI → EP (b) |

0.2732 |

0.0497 |

5.4927 |

.0000 |

0.1754, 0.3709 |

|

CSR → EP (c′) |

0.3280 |

0.0601 |

5.4542 |

.0000 |

0.2097, 0.4462 |

|

CSR → GI → EP (ab) |

0.1952 |

— |

— |

— |

0.1140, 0.2904 |

Figure 4 shows that all paths are significant, suggesting that partial mediation holds between green finance and banks’ environmental performance. Hence, the banks that undertake CSR activities tend to promote green innovation inside the organization as well. This results in better environmental performance when energy-efficient technologies and environmentally conscious practices are introduced within the banks. However, CSR also directly boosts the environmental performance of banks, independent of green innovation, by embedding sustainable practices into banking operations.

Figure 4

Mediation between CSR and EP

Discussion

The results of this research show that fintech adoption, green finance, CSR, and green innovation are crucial resources for improving banks’ environmental performance. However, their mere presence is not enough, rather, they should be implemented effectively and efficiently. The findings of this study support the resource-based theory, the hypotheses postulated, and effectively answer the research questions. The results are also in line with the previous literature. The first hypothesis aimed to understand if adopting financial technology results in better environmental performance of banks. As the findings were significant, H1 is accepted. Previous literature reported similar results, implying that fintech is a valuable resource with unique operational capabilities, including efficiency, sustainability, and transparency, as provided to banks (Badrous et al., 2025; Naz et al., 2023; Yan et al., 2022; Yuan, 2025). Therefore, tracking the carbon footprint and mitigating all the ill-impacts of banking operations is possible with the help of fintech (Dong & Yu, 2023).

In the context of Pakistan’s banking system, this impact is meaningful because the State Bank of Pakistan (SBP) emphasizes integrating digital modes of banking into financial services. This is done to promote financial inclusion and reduce traditional resource-intensive banking operations. Secondly, the results also suggest that green finance facilities, such as green bonds, green credit, and sustainable investment products provided by banks to other sectors serve as crucial financial resources that boost their reputation, thereby increasing their environmental performance. These financial mechanisms directed by the SBP support eco-friendly projects and discourage high-emission industries, thus promoting environmentally sustainable activities. This corroborates with the existing literature (Badrous et al., 2025; Talha, 2023). Hence, H2 is accepted. Green finance promotes pro-environmental behavior and accelerates green growth by aligning banks’ strategies with community values.

Thirdly, the findings show that the banks that carry out CSR activities demonstrate better environmental performance as they integrate sustainability into their core operations. This is also in line with the previous literature (Dai et al., 2022; Gazi et al., 2025). Especially in Pakistan, banks must continue striving for this obligation to create value for the community. Hence, H3 is accepted and it is reported that CSR acts as a strategic resource and provides a competitive advantage, thereby strengthening the stakeholders’ trust.

Concerning the indirect effects, green innovation has been found to partially mediate all three relationships and establish a significant direct impact on the banks’ environmental performance. It suggests that green innovation acts as a strategic resource contributing to their environmental performance. This aligns with RBV. According to the theory, banks’ valuable technological capabilities, social responsiveness, and financial mechanisms are transformed into environment-related performance benefits using responsible, innovative techniques. These results are in partial agreement with prior studies and delineate the facilitating role of green innovation (Dai et al., 2022; Gazi et al., 2025; Kraus et al., 2020). This means that banks that adopt fintech foster green innovation, which improves their environmental performance. Similarly, banks that offer green financing also promote green innovative products and make operational improvements that result in better environmental performance. Lastly, CSR activities carried out by banks encourage green innovation, which then increases their environmental performance. However, these results differ from previous studies because partial mediation was found in the current study, implying that while green innovation serves as a key mechanism due to its facilitating role, its presence is only complementary. Moreover, even in its absence, direct impacts are possible.

ConclusionThis research sought to determine the contribution of fintech adoption, provision of green finance, and undertaking of CSR activities in improving the environmental performance of the banks. Additionally, it explored whether green innovation acts as a mediator between these relationships. To conduct this research, data were collected from 400 bank employees using a questionnaire. Using multiple linear regression and Hayes PROCESS, it was found that fintech adoption, green finance, and CSR directly boost environmental performance, while green innovation partially supports them. These findings have theoretical implications because they extend the resource-based view. Fintech adoption, green finance, CSR, and green innovation are referred to as strategic resources and innovative capabilities that help to enhance the environmental performance of banks. Furthermore, green innovation as partial mediator suggests that innovation can link these dynamic resources to favorable environmental outcomes. The findings also take the RBV theory one step ahead by stating that such resources provide a competitive advantage in more than just financial terms. Moreover, they also focus on how innovative capabilities can help to operationalize strategic resources and bridge the gap between merely possessing strategic resources to effectively implementing them in order to leverage their benefits.

There are several practical implications of this study for the banks, policymakers, regulators, and the SBP. For banks, it is recommended to adopt financial technology in their core operations, expand green financing options for environment-focused projects, and allocate budget to carry out CSR activities. Additionally, it is suggested to promote green innovation to foster energy-efficient banking operations and translate strategic resources into tangible outcomes, such as increased environmental performance. For policymakers, it is recommended to develop policies to incentivize banks to implement green innovation. For central bank, it is suggested to provide incentives to those banks that opt for sustainable banking practices and have better environmental performance. Additionally, environmental performance disclosures should be mandated to further strengthen the impact. Lastly, training and workshops should be conducted for the bank staff to equip them with practical knowledge, so that they can effectively adopt fintech, green finance, green innovation, and practice CSR.

The research has certain limitations. Firstly, the generalizability of these results is limited to Pakistan, a developing country. Secondly, the results are only relevant to the banking sector. Thirdly, as a questionnaire was used to collect the data, respondents may be influenced by various biases, such as the social desirability bias or mistakes in responses. Based on these limitations, future researchers have several avenues to explore. These include exploring the role of Fintech-driven sustainability in financial businesses other than the banking sector, such as insurance, investment, and financial markets. If they want to stick to the banking sector, they can investigate how regulatory frameworks and governmental policies promote fintech-oriented sustainability. A robust framework can be formulated to assess the financial and environmental performance of the banks. Cross-country comparison, or developed vs. developing economies comparison, can be conducted using the conceptual model of this research to gain insights regarding differences in practices and the role of contextual elements. Future researchers can also study the role of investors, consumers, and employees in employing fintech-driven environmental initiatives in the banks. Lastly, collaboration and information sharing among banks, Fintech companies, and other beneficiaries can be explored to promote sustainable innovation and best practices. Hence, the understanding and implementation of sustainable banking practices can be enhanced further by investigating these prospective study avenues.

Author Contribution

Fareeha Waseem: conceptualization, supervision, investigation, validation, methodology. Veera Salman: writing -original draft, review & editing. Zahra Batool: formal analysis, visualization, writing – original draft

Conflict of Interest

The authors of the manuscript have no financial or non-financial conflict of interest in the subject matter or materials discussed in this manuscript.

Data Availability Statement

The data associated with this study will be provided by the corresponding author upon request.

Funding Details

No funding has been received for this research.

Generative AI Disclosure Statement

The authors did not used any type of generative artificial intelligence software for this research.

REFERENCES

Abbas, N., & Shahid, M. S. (2024). Mapping the impact of green finance on corporate sustainability: A bibliometric analysis. Audit and Accounting Review, 4(1), 101–130. https://doi.org/10.32350/aar.41.05

Ahmad, N., Ullah, Z., Arshad, M. Z., waqas Kamran, H., Scholz, M., & Han, H. (2021). Relationship between corporate social responsibility at the micro-level and environmental performance: The mediating role of employee pro-environmental behavior and the moderating role of gender. Sustainable Production and Consumption, 27, 1138–1148. https://doi.org/10.1016/j.spc.2021.02.034

Al-Ali, H. A., & O'Mahony, B. (2025). Corporate social responsibility and environmental performance: The mediating role of green capabilities and green innovation. Journal of Asia Business Studies, 19(4), 973–997. https://doi.org/10.1108/JABS-08-2024-0472

Ali, S., Yan, Q., Sajjad Hussain, M., Irfan, M., Ahmad, M., Razzaq, A., Dagar, V., & Işık, C. (2021). Evaluating green technology strategies for the sustainable development of solar power projects: Evidence from Pakistan. Sustainability, 13(23), Article e12997. https://doi.org/10.3390/su132312997

Ashta, A. (2023). How can fintech companies get involved in the environment? Sustainability, 15(13), Article e10675. https://doi.org/10.3390/su151310675

Asif, M., Sarwar, F., & Lodhi, R. N. (2023). Future and current research directions of FinTech: A bibliometric analysis. Audit and Accounting Review, 3(1), 19–51. https://doi.org/10.32350/aar.31.02

Aslam, W., & Jawaid, S. T. (2023). Green banking adoption practices: Improving environmental, financial, and operational performance. International Journal of Ethics and Systems, 39(4), 820–840. https://doi.org/10.1108/IJOES-06-2022-0125

Badrous, Y. M. L., Tawfik, O. I., Elmaasrawy, H. E., Srour, M. I., & Sharaf, M. A. A. (2025). Fintech adoption and commercial banks' environmental performance: Do green accounting practices matter? International Journal of Financial Studies, 13(2), Article e90. https://doi.org/10.3390/ijfs13020090

Bai, R., & Lin, B. (2022). Access to credit and green innovation: Do green finance and digitalization levels matter? Journal of Global Information Management (JGIM), 30(1), 1–21. https://doi.org/10.4018/JGIM.315022

Barney, J. (1991). Firm resources and sustained competitive advantage. Journal of Management, 17(1), 99–120. https://doi.org/10.1177/01492063910170010

Bartlett, M. (1935). Some aspects of the time-correlation problem in regard to tests of significance. Journal of the Royal Statistical Society, 98(3), 536–543. https://doi.org/10.2307/2342284

Bimha, A., & Nhamo, G. (2017). Measuring environmental performance of banks: Evidence from Carbon Disclosure Project (CPD) reporting banks. Journal of Economic and Financial Sciences, 10(1), 26–46. https://doi.org/10.4102/jef.v10i1.3

Bruna, M. G., & Lahouel, B. B. (2022). CSR & financial performance: Facing methodological and modeling issues commentary paper to the eponymous FRL article collection. Finance Research Letters, 44, Article e102036. https://doi.org/10.1016/j.frl.2021.102036

Cao, J., Law, S. H., Samad, A. R. B. A., Mohamad, W. N. B. W., Wang, J., & Yang, X. (2021). Impact of financial development and technological innovation on the volatility of green growth—evidence from China. Environmental Science and Pollution Research, 28(35), 48053–48069. https://doi.org/10.1007/s11356-021-13828-3

Chen, J., Siddik, A. B., Zheng, G.-W., Masukujjaman, M., & Bekhzod, S. (2022). The effect of green banking practices on banks' environmental performance and green financing: An empirical study. Energies, 15(4), Article e1292. https://doi.org/10.3390/en15041292

Chen, Y.-S., Lai, S.-B., & Wen, C.-T. (2006). The influence of green innovation performance on corporate advantage in Taiwan. Journal of Business Ethics, 67, 331–339. https://doi.org/10.1007/s10551-006-9025-5

Dai, X., Siddik, A. B., & Tian, H. (2022). Corporate social responsibility, green finance and environmental performance: Does green innovation matter? Sustainability, 14(20), Article e13607. https://doi.org/10.3390/su142013607

Desai, R., & Patel, S. (2025). Analysing the research development in green finance: Performance analysis and directions for future research. FIIB Business Review, 14 (1), Article e23197145241306838. https://doi.org/10.1177/23197145241306838

Desalegn, G., & Tangl, A. (2022). Enhancing green finance for inclusive green growth: A systematic approach. Sustainability, 14(12), Article e7416. https://doi.org/10.3390/su14127416

Dong, X., & Yu, M. (2023). Does FinTech development facilitate firms' innovation? Evidence from China. International Review of Financial Analysis, 89, Article e102805. https://doi.org/10.1016/j.irfa.2023.102805

Dwivedi, P., Alabdooli, J. I., & Dwivedi, R. (2021). Role of FinTech adoption for competitiveness and performance of the bank: A study of banking industry in UAE. International Journal of Global Business and Competitiveness, 16(2), 130–138. https://doi.org/10.1007/s42943-021-00033-9

Gazi, M. A. I., Hossain, M. M., Islam, S., Al Masud, A., Amin, M. B., Senathirajah, A. R. b. S., & Abdullah, M. (2025). Effect of corporate social responsibility on sustainable environmental performance: Mediating effects of green capability and green transformational leadership; moderating effects of top management environmental concern and perceived organizational support. Environment, Development and Sustainability, 1–34. https://doi.org/10.1007/s10668-025-06082-x

Gidage, M. K., & Bhide, S. (2024). Does ESG impact the financial well-being of companies?: Evidence from India. In Emerging perspectives on financial well-being (pp. 74–94). IGI Global Scientific Publishing.

Guang-Wen, Z., & Siddik, A. B. (2022). Do corporate social responsibility practices and green finance dimensions determine environmental performance? An Empirical Study on Bangladeshi Banking Institutions. Frontiers in Environmental Science, 10, Article e890096. https://doi.org/10.3389/fenvs.2022.890096

Hu, Y., & Zheng, J. (2021). Is green credit a good tool to achieve "double carbon" goal? Based on coupling coordination model and PVAR model. Sustainability, 13(24), Article e14074. https://doi.org/10.3390/su132414074

Indriastuti, M., & Chariri, A. (2021). The role of green investment and corporate social responsibility investment on sustainable performance. Cogent Business & Management, 8(1), Article e1960120. https://doi.org/10.1080/23311975.2021.1960120

Klassen, R. D., & Whybark, D. C. (1999). The impact of environmental technologies on manufacturing performance. Academy of Management journal, 42(6), 599–615. https://doi.org/10.5465/256982

Kraus, S., Rehman, S. U., & García, F. J. S. (2020). Corporate social responsibility and environmental performance: The mediating role of environmental strategy and green innovation. Technological Forecasting and Social Change, 160, Article e120262. https://doi.org/10.1016/j.techfore.2020.120262

Lisha, L., Mousa, S., Arnone, G., Muda, I., Huerta-Soto, R., & Shiming, Z. (2023). Natural resources, green innovation, fintech, and sustainability: A fresh insight from BRICS. Resources Policy, 80, Article e103119. https://doi.org/10.1016/j.resourpol.2022.103119

Liu, J., Jiang, Y., Gan, S., He, L., & Zhang, Q. (2022). Can digital finance promote corporate green innovation? Environmental Science and Pollution Research, 29(24), 35828–35840. https://doi.org/10.1007/s11356-022-18667-4

Liu, L. (2024). Green innovation, firm performance, and risk mitigation: Evidence from the USA. Environment, Development and Sustainability, 26(9), 24009–24030. https://doi.org/10.1007/s10668-023-03632-z

Naz, S., Asif, M., & Hameed, S. (2023). Fintech's role in sustainable banking performance: Are green banking policies driving sustainability in pakistan's banking system? Gomal University Journal of Research, 39(3), 294–312.

Nkansah, B. K. (2018). On the Kaiser-Meier-Olkin's measure of sampling adequacy. Mathematical Theory and Modeling, 8(7), 52–76.

Rehman, A., Ullah, I., Afridi, F.-e.-A., Ullah, Z., Zeeshan, M., Hussain, A., & Rahman, H. U. (2021). Adoption of green banking practices and environmental performance in Pakistan: A demonstration of structural equation modelling. Environment, Development and Sustainability, 23(9), 13200–13220. https://doi.org/10.1007/s10668-020-01206-x

Riyanti, R. S., Wulandari, P., Prijadi, R., & Tortosa-Ausina, E. (2025). Green loans: Navigating the path to sustainable profitability in banking. Economic Analysis and Policy, 85, 1613–1624. https://doi.org/10.1016/j.eap.2025.01.028

Sadiq, M., Paramaiah, C., Dong, Z., Nawaz, M. A., & Shukurullaevich, N. K. (2024). Role of fintech, green finance, and natural resource rents in sustainable climate change in China. Mediating role of environmental regulations and government interventions in the pre-post COVID eras. Resources Policy, 88, Article e104494. https://doi.org/10.1016/j.resourpol.2023.104494

Sajid, R., Ayub, H., Malik, B. F., & Ellahi, A. (2023). The role of fintech on bank risk‐taking: Mediating Role of bank's operating efficiency. Human Behavior and Emerging Technologies, 2023(1), Article e7059307. https://doi.org/10.1155/2023/7059307

Subanidja, S., Sorongan, F., & Legowo, M. B. (2022). Sustainable bank performance antecedents in the covid-19 pandemic era: A conceptual model. Emerging Science Journal, 6(4), 786–797. https://doi.org/10.28991/ESJ-2022-06-04-09

Talha, M. (2023). Green financing and sustainable policy for low carbon and energy saving initiatives: Turning educational institutes of China into green. Engineering Economics, 34(1), 103–117. https://doi.org/10.5755/j01.ee.34.1.32837

Tan, Y., Lin, B., & Wang, L. (2025). Green finance and corporate environmental performance. International Review of Economics & Finance, 98, Article e103929. https://doi.org/10.1016/j.iref.2025.103929

Turker, D. (2009). Measuring corporate social responsibility: A scale development study. Journal of Business Ethics, 85(4), 411–427. https://doi.org/10.1007/s10551-008-9780-6

Wang, Q.-J., Wang, H.-J., & Chang, C.-P. (2022). Environmental performance, green finance and green innovation: What's the long-run relationships among variables? Energy Economics, 110, Article e106004. https://doi.org/10.1016/j.eneco.2022.106004

Wang, Y., & Zhi, Q. (2016). The role of green finance in environmental protection: Two aspects of market mechanism and policies. Energy Procedia, 104, 311–316. https://doi.org/10.1016/j.egypro.2016.12.053

Xu, N., Huo, B., & Ye, Y. (2024). The impact of supply chain pressure on cross-functional green integration and environmental performance: An empirical study from Chinese firms. Operations Management Research, 17(2), 612–634. https://doi.org/10.1007/s12063-024-00439-7

Xu, S. (2025). Corporate social responsibility and financialization: Is CSR used as a financial tool? European Management Review. https://doi.org/10.1111/emre.70013

Xue, Q., Bai, C., & Xiao, W. (2022). Fintech and corporate green technology innovation: Impacts and mechanisms. Managerial and Decision Economics, 43(8), 3898–3914. https://doi.org/10.1002/mde.3636

Yan, C., Siddik, A. B., Yong, L., Dong, Q., Zheng, G.-W., & Rahman, M. N. (2022). A two-staged SEM-artificial neural network approach to analyze the impact of FinTech adoption on the sustainability performance of banking firms: the mediating effect of green finance and innovation. Systems, 10(5), Article e148. https://doi.org/10.3390/systems10050148

Yu, C.-H., Wu, X., Zhang, D., Chen, S., & Zhao, J. (2021). Demand for green finance: Resolving financing constraints on green innovation in China. Energy policy, 153, Article e112255. https://doi.org/10.1016/j.enpol.2021.112255

Yuan, X. (2025). Integrating Fintech, CSR, and green finance: impacts on financial and environmental performance in China. Humanities and Social Sciences Communications, 12(1), 1–15. https://doi.org/10.1057/s41599-025-05064-8

Zheng, G.-W., Siddik, A. B., Masukujjaman, M., & Fatema, N. (2021). Factors affecting the sustainability performance of financial institutions in Bangladesh: the role of green finance. Sustainability, 13(18), Article e10165. https://doi.org/10.3390/su131810165