Muhammad Rehman Shafique1, Aamir Sohail2*, Shoaib Nisar3, and Muhammad Munir 4,5

1Superior University, Lahore, Pakistan

2Thal University, Bhakkar, Pakistan

3Lahore Garrison University, Pakistan

4Harbin Institute of Technology, Shenzhen, China

5University of Sahiwal, Sahiwal

* Corresponding Author: [email protected]

This research aims to investigate the critical factors that affect the financial decision-making of retail investors in Pakistan Stock Exchange (PSX), with a focus on the moderating role of financial literacy. This information is crucial to understand the behavior of retail investors which can help financial institutions and market regulators to develop effective strategies to educate and guide investors. A quantitative research approach was employed to conduct this study. A sample of retail investors who invested in PSX was selected. Data was collected using a simple random sampling technique. After evaluating the missing values, 365 responses were considered for the final analysis. Smart-PLS was used for analyzing both the measurement model (used to analyze the validity and reliability of data) and the structural model (used to test the hypothesis). In the current study, a higher-order construct approach was adopted to evaluate the reflective-formative indicators of factors affecting the financial decision-making of retail investors. The results revealed that all exogenous variables have a significant influence on the financial decisions of retail investors in the PSX. As per the empirical findings, financial literacy moderates the relationship between exogenous and endogenous variables. The results would be useful for policymakers, financial regulators, and investment firms in designing effective financial education programs and investment products that meet the needs and preferences of retail investors in PSX.

Keywords: behavioral finance, financial literacy, financial decisions, Pakistan Stock Exchange (PSX), retail investors

The investment decisions of investors are one of the main indicators that define the micro and macro levels of an economy. Investments play an essential role by contributing to the development of the economy. The ever-increasing trading volume in the stock markets indicates a growing investment-related financial literacy (Chakraborty et al., 2023). Recent economic developments and improvements indicate that stock markets are currently more volatile and unstable than they were in the past. Due to the increase in volatility, the risks associated with the stock market have also grown. Professionals, academics, and investors have been troubled by the volatility of the stock market for decades (Sohail et al., 2020).

According to conventional finance, the stock market has always been effective for the economy and the prices associated with the stock market have always reflected all available information. Traditional finance also implies that investors are always rational in the market and base portfolio construction on these rational assumptions (Ahmad et al., 2020). Researchers presented numerous theories, such as the Efficient Market Hypothesis (EMH) and the Expected Utility Theory in support of conventional finance. The theory of EMH is based on two main assumptions including the stock price in the market which reflects all information (previous, public, and private), indicating that the market is efficient. The second assumption is that there are no anomalies in the market since investors are always rational in the market and choose the company to invest in, based on their rationality (Chakraborty et al., 2023).

The assumption behind expected utility theory, which lends credence to the position taken by conventional finance, is that investors in the stock market act rationally and arrive at their financial choices after carefully weighing a number of available options. On the other hand, the researchers provide a new paradigm of behavioral finance which states that investors do not behave in a logical manner while dealing with the market. In the published works (Bosch-Rosa & Corgnet, 2022; Botzen et al., 2021), many factors have been identified that affect retail investors' financial decision-making. Recent studies support that the irrational behaviors of investors come from behavioral biases, emotions, and social pressures. In the previous literature (Bouteska & Regaieg, 2017; Trejos et al., 2019; Warmath et al., 2019), various factors affect retail investors' financial decisions. Risk and return are the major elements that receive maximum consideration from the investor's side while investing in the financial market. However, it is not the only criterion for investing, for instance, according to Jaiyeoba et al. (2018), physiological factors are one of the major factors that elaborate the investment pattern of the retail investor.

Financial literacy is a crucial tool for investors to make informed investment decisions. It entails having the knowledge and abilities to understand financial concepts, such as risk, return, and diversification as well as the ability to employ this understanding to make sound investment decisions (Jain et al., 2022). Financially literate investors are capable of evaluating investment opportunities, analyzing financial data, and managing portfolio risks. Moreover, they can also set attainable investment objectives based on their financial situation and investment objectives, thereby enhancing their long-term financial success. In today's complex and dynamic investment environment, where there are numerous investment products and financial instruments, investors must be financially literate (Ansari et al., 2022).

In addition to the knowledge of financial concepts and products, financial literacy also requires the ability to employ this knowledge in real-world situations (Gupta & Shrivastava, 2022). Investors who are financially proficient are capable to evaluate investment opportunities and make well-informed investment decisions based on their knowledge of financial concepts and personal financial objectives. Additionally, they are more likely to recognize and avoid investment schemes, which may result in substantial financial losses. Financial literacy is a valuable instrument for investors to achieve financial success and make informed investment decisions following their investment objectives and risk tolerance (Gupta & Shrivastava, 2022).

Over the last several years, retail investors have begun to direct significant attention to the Pakistani stock market (Naveed et al., 2020). On the other hand, it has also been noticed that the financial decision-making of these investors is impacted by several circumstances which may lead to biased investment judgments and the possibility of financial losses. In spite of the expanding number of retail investors in the Pakistani stock market, there is lack of research on the crucial aspects that influence the financial decisions taken by these investors. Additionally, financial literacy has been highlighted as a key factor in making informed investment choices; however, the moderating role of financial literacy was not observed by most of the researchers (Song et al., 2023). For that reason, the purpose of the current research was to analyze the important elements impacting the financial decision-making of retail investors in the Pakistani stock market and the moderating effect that financial literacy has in that decision-making. The outcomes of this study would provide investors, financial advisors, politicians, and academics with invaluable insights on how to enhance the investment decision-making process of retail investors along with increasing the financial literacy.

The basic objective of the current study is to examine multiple factors that influence the decision-making of retail investors. The core objective of the study has various sub-objectives which are as follows,

Investors' Financial Behavior and Biases

Financial decision-making refers to a process in which investors take a variety of criteria into account to assess the merits of various investment opportunities. These characteristics include age, gender, race, income, level of education as well as technological considerations, situational elements (such as economic, cultural, environmental, social, and legal issues), and behavioral factors (Osman et al., 2023). According to Gupta and Shrivastava (2022), the process of the financial choices of individual investors is dependent on internal and external elements that impact their investment behavior. These factors may influence their investment behavior in either a positive or a negative way.

The retail investor's financial choices are heavily influenced by psychological considerations, making this one of the most important components to examine. Numerous researches (Goyal et al., 2023; Grable & Rabbani, 2023; Nair et al., 2022) amongst others, investigated the connection between various psychological aspects and the choices made by retail investors regarding their finances. Based on the results, the researchers concluded that various psychological elements considerably impact the financial choices made by individual investors.

: Behavioral Biases significantly influence the perception of an individual investor while investing.

Quddoos et al. (2020) suggested another important dimension regarding investors' overconfidence. For instance, sometimes, investors analyze the future of the market based on previous or past trends without examining the actual or fundamental conditions' analysis regarding the trend line. Muneeswaran et al. (2020) studied the impact of various behavioral biases upon the financial decision-making of retail investors and found that overconfidence bias had a significant effect on the decision-making of retail investors. Shahid et al. (2018) found that the S&P 500 faced the problem of inflation due to over-optimistic behavior and the overconfidence bias of investors. The irrational behaviors are connected with the retail investors and influence the institutional investors' decision-making. According to Waweru et al. (2008), investigations revealed that the investment decisions of institutional investors on the Nairobi stock exchange were influenced by the overconfidence bias. Thus, the following hypothesis was drawn.

: Overconfidence significantly influences the perception of an individual investor while investing.

According to the findings of a study carried out by Chen et al. (2021) to observe the herd behavior in rich nations (including the United States of America, France, Italy, Germany, Australia, Hong Kong, and Britain) as well as developing countries, the researchers found that there was no significant difference between the two types of countries (Brazil, Malaysia, Turkey, and Argentina). The least-square approach was employed to determine the influence of herd behavior on the decision-making process of investors while investing. However, it was discovered that there was no rule of herd behavior in this respect. Meanwhile, the regression analysis was carried out to validate the findings, and observations were made on the major influence that herd behavior had on the decision-making process. Other researches came to the same conclusion that the market time frame also plays a part in defining the consequences that herd behavior has on the thinking of investors. It was found that investors are more likely to follow the crowd when it comes to making decisions. According to the results, herd behavior is a significant factor in the decision-making process during the period in which stock values rise as a result of a bull run. On the other hand, in a bear market, when stock prices fall, the herd mentality does not strongly associate with the financial choices made by retail investors, regardless of whether they are from an established or emerging stock market. This is the case regardless of whether the stock market was developed or developing (Adil et al., 2022; Gupta & Shrivastava, 2022). Therefore, the following hypothesis was derived,

: There is a significant impact of herd behavior on the financial decisions of individual investors in PSX.

Rasool and Ullah (2020) examined various factors that impact the financial decision-making of investors. It was determined that mental accounting significantly influences the investing decisions of Pakistani investors who invest in the Pakistan Stock Exchange (PSX). Setayesh and Sarmadinia (2019) explored various psychological factors that make an investor irrational in the stock market. According to this study, many behavioral biases including herd behavior, mental accounting, gambler fallacy, anchoring, and overconfidence are significantly associated with investors' intentions while making the investment. On the other hand, Asad et al. (2018) conducted their study to observe the mental accounting state of Pakistani investors and found no significant relationship between mental accounting and investment decisions. According to Goyal and Kumar (2021), the gambler fallacy is not significantly associated with retail investors' investment decision-making process. Thus, the following hypothesis was derived.

: Mental accounting significantly influences the financial decision-making of retail investors in Pakistan.

Financial literacy is an essential aspect that assists investors in making informed investment choices and avoiding irrational behavior in the market. According to several studies, having a strong understanding of finances may lessen the influence of cognitive biases on investment choices and boost the efficiency of financial educational programs. (Agnew & Harrison, 2015). In addition to this, it has been shown that the level of financial literacy of an individual might limit the connection between important aspects and the process of investment decision-making. For instance, Rasool & Ullah (2020) found that the level of financial literacy of an individual moderates the link between one's risk tolerance and investing decision-making. A similar finding was made by Rahayu et al. (2022), that a person's level of financial literacy moderates the association between experience in the stock market and investing decision-making. Thus, it was hypothesized that,

H2: Behavioral biases significantly influence the financial decision-making of retail investors in Pakistan with the moderating impact of financial literacy.

The current study is quantitative in nature. Additionally, positivism was the philosophical basis for the current research. The unit of analysis was PSX retail investors. Resultantly, the primary objective of this study was to examine the factors that influence the financial decisions of retail investors in Pakistan. Therefore, the demographic details comprised all retail investors who invested in PSX. The literature review discussed two main sampling techniques including probability sampling and non-probability sampling techniques. To select the sample for the current study, a convenience sampling technique was employed. This technique was selected because the exact population was not known and responses were required as per conveniently available investors in PSX.

To collect data, a structural questionnaire was utilized which was adapted from existing literature. To determine an appropriate sample size, a free calculator was used recommended by Patel et al. (2003) with a 95% confidence level and 5% margin of error. Based on the formula, a sample size of 310 was deemed sufficient for the data collection purpose. About 500 questionnaires were distributed among retail investors and 365 responses were received which were included in the final sample. The current study used Structural Equation Modeling (SEM). This technique divided the whole analysis into two parts or phases. In the first phase, the measurement model was analyzed, moreover, the construct's reliability and validity were also examined. On the other hand, in the second phase, the structural model was measured to analyze the level of significance between all exogenous and endogenous variables.

A disjointed two-stage methodology was employed to analyze the data. In the initial phase, the measurement model was examined for the lower-order construct and the validity and reliability of all lower-order constructs. In the second phase, the measurement model of the higher-order construct was examined to corroborate the construct's validity. A pilot study was conducted to determine the validity and reliability of the data. For the measurement model analysis, data was collected from 55 investors. Cronbach alpha and composite reliability were greater than 0.7 in the pilot study, indicating the reliability of the construct. Additionally, the Average Variance Extracted (AVE) was employed to assess the construct's validity. The AVE of all constructs was greater than 0.5 which was sufficient for data validation. HTMT was utilized to determine the discriminant validity of constructs that must be less than 0.85. The HTMT of constructs was below 0.85, indicating the discriminant validity of the data.

Demographic Analysis

Table 1

Frequency Analysis

|

Variable |

Frequency |

Percent |

|

Gender |

|

|

|

Male |

201 |

55.1 |

|

Female |

164 |

44.9 |

|

Age of Respondents |

|

|

|

20-30 |

172 |

47.1 |

|

31-40 |

132 |

36.2 |

|

41-50 |

53 |

14.5 |

|

51-above |

8 |

2.2 |

|

Education |

|

|

|

Bachelor Degree |

19 |

5.2 |

|

Master |

257 |

70.4 |

|

MS |

55 |

15.1 |

|

Doctorate |

20 |

5.5 |

|

Diploma |

14 |

3.8 |

|

Investment Experience |

|

|

|

< 10 years |

163 |

44.7 |

|

11 – 15 years |

92 |

25.2 |

|

> 16 -25 years |

93 |

25.5 |

|

> 25 years |

17 |

4.7 |

Table 1 demonstrates the demographic profile of the respondents. The findings suggested that majority of the respondents were male (55.1%). Furthermore, the table demonstrates that the majority of the respondents' age was 20 to 30 years, (47.1%) having mostly qualification of Master (70.4%). Moreover, the results also demonstrated that most of the respondents' investment experience was less than 10 years (44.7%).

According to Yamamoto et al. (2014), the outer factor loading represents how much each item contributes to the formation of each latent variable. The minimum requirement for the outer loading was 0.7, so all those items were excluded whose outer loading was less than 0.7. Table 2 shows the construct reliability of the variables which clearly states that all the variables were reliable for further analysis.

Table 2

Construct Reliability

|

Cronbach's Alpha |

rho_A |

Composite Reliability |

|

|

Financial Literacy |

0.71 |

0.72 |

0.87 |

|

Herding Behaviour |

0.73 |

0.73 |

0.8 |

|

Investors Financial Behaviour |

0.78 |

0.78 |

0.84 |

|

Mental Accounting |

0.74 |

0.76 |

0.82 |

|

Over-confidence |

0.81 |

0.83 |

0.86 |

AVE was used to analyze the construct validity. According to Alarcón and Sánchez (2015), it should be more than 0.5. Table 3 represents the AVE of the lower-order construct that was almost more than 0.5. VIF is normally used by researchers to analyze the multi-collinearity of items. VIF should be less than five which shows no multi-collinearity between the indicators. Annexure 02 shows the VIF table of the measurement model.

Table 3

Average Variance Extracted (AVE)

|

Average Variance Extracted (AVE) |

|

|

Financial Literacy |

0.78 |

|

Herding Behaviour |

0.51 |

|

Investors Financial Behaviour |

0.53 |

|

Mental Accounting |

0.59 |

|

Over-confidence |

0.56 |

Table 3 represents the results of HTMT to determine the discriminant validity between constructs. The figures of HTMT should be less than 0.9 and if it is more than 0.9, it means that the data does not have discriminant validity.

Table 4

Construct Validity (HTMT)

|

Financial Literacy |

Herding Behaviour |

Investors Financial Behaviour |

Mental Accounting |

Over-confidence |

|

|

Financial Literacy |

|||||

|

Herding Behaviour |

0.31 |

||||

|

Investors Financial Behaviour |

0.49 |

0.43 |

|||

|

Mental Accounting |

0.86 |

0.31 |

0.51 |

||

|

Over-confidence |

0.41 |

0.35 |

0.56 |

0.4 |

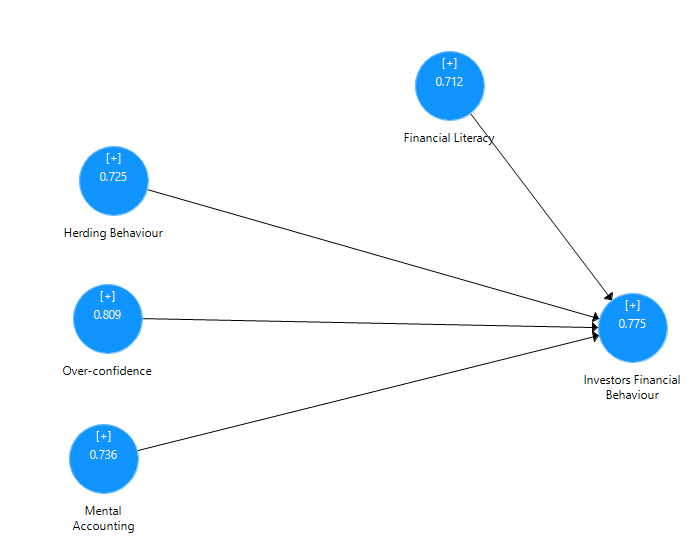

Table 5 shows the discriminant validity using Fornel and Larcker by comparing the square root of each AVE in the diagonal with the correlation coefficients (off-diagonal) for each construct in the relevant rows and columns. Overall, discriminant validity may be accepted for this measurement model and support the discriminant validity between the constructs.

Table 5

Discriminant Validity_ Fornell Larcker Criterion

|

Financial Literacy |

Herding Behaviour |

Investors Financial Behaviour |

Mental Accounting |

Over-confidence |

|

|

Financial Literacy |

0.48 |

||||

|

Herding Behaviour |

0.23 |

0.56 |

|||

|

Investors Financial Behaviour |

0.37 |

0.33 |

0.65 |

||

|

Mental Accounting |

0.64 |

0.24 |

0.4 |

0.7 |

|

|

Over-confidence |

0.31 |

0.27 |

0.5 |

0.33 |

0.75 |

Figure 1

Reliability Analysis

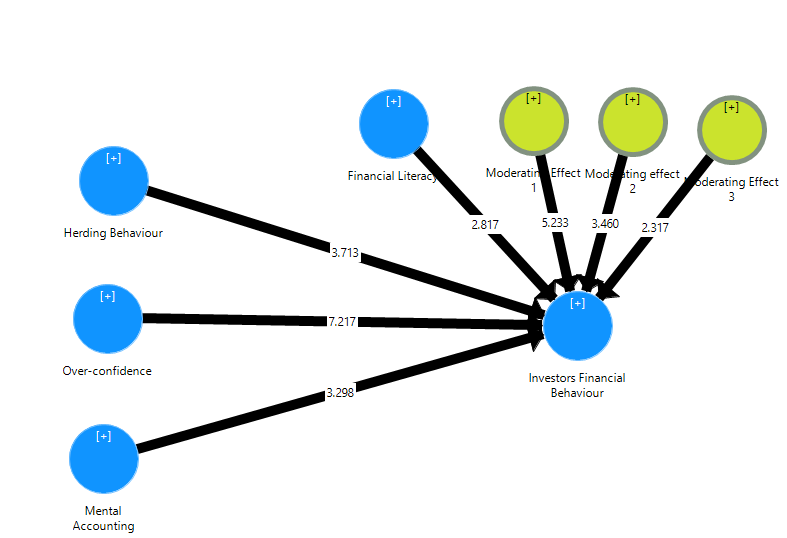

To assess the structural model, path analysis was conducted using Smart PLS software. Additionally, the SRMR (Standardized Root Mean Square) was calculated through PLS-Bootstrapping to determine the model fitness. According to Sarstedt and Cheah (2019), an SRMR value of less than 0.08 indicates a good fit. The calculated value of SRMR for the model used in the current study was 0.052, indicating that the model is a good fit. This assessment follows the measurement model assessment conducted earlier which analyzed the validity and reliability of the model.

Table 6

Results of R Square

|

R Square |

R Square Adjusted |

|

|

Investment Decision |

0.711 |

0.701 |

|

Financial Literacy |

0.729 |

0.719 |

Table 6 represents the results of the R square from the PLS bootstrapping. R square shows how much percent change in the dependent variable is explained by the independent variables. These results show that approximately 70% of the change in investment decisions is captured through the available independent variables. While, the R square of risk perception is 0.729 which shows a 72% change in risk perception due to change in independent variables.

Table 7

Path Coefficients

|

|

Original Sample (O) |

t Statistics (|O/STDEV|) |

p Values |

|

Herding Behaviour -> Investors' Financial Behaviour |

-0.12 |

3.71 |

0.000 |

|

Mental Accounting -> Investors' Financial Behaviour |

-0.13 |

3.30 |

0.000 |

|

Over-confidence -> Investors' Financial Behaviour |

-0.36 |

7.22 |

0.000 |

|

Financial Literacy -> Investors' Financial Behavior |

0.10 |

2.82 |

0.010 |

Table 7 shows the results extracted from PLS-SEM to show the significance of the impact of exogenous variables on endogenous variables. The table shows that all exogenous variables have a significant impact on endogenous variables. The was accepted since behavioral biases affect investment decisions at a 0.1 level of significance.

Table 8

Moderation Analysis (Financial Literacy)

|

Original Sample (O) |

t Statistics (|O/STDEV|) |

p Values |

|

|

Moderating Effect 1 -> Investors' Financial Behavior |

0.16 |

5.23 |

0.000 |

|

Moderating effect 2 -> Investors' Financial Behavior |

0.15 |

3.46 |

0.000 |

|

Moderating Effect 3 -> Investors' Financial Behavior |

0.06 |

2.32 |

0.020 |

Table 8 shows the moderation analysis through the path coefficients. The results show that financial literacy plays its role as the moderator variable between all exogenous variables (Herding behavior, Over-Confidence, Mental Accounting) and endogenous variables which are investment decisions. Based on these results, the research hypothesis was accepted.

Figure 2

Structural Equational Modeling (SEM)

The results indicated that overconfidence has a significant influence on the financial decisions of investors. The performance of an investment might be negatively impacted by overconfidence. Those investors who are aware of their propensity for overconfidence may be able to limit its impacts by adopting a more careful and disciplined approach to investing. This may include adhering to a long-term investment strategy and avoiding rash choices based on short-term shifts in the market. The findings are also consistent with the findings of previous research (Ansari et al., 2023; Bihari et al., 2023; Quang et al., 2023). Furthermore, the findings indicated that Herding behavior has a significant influence on the financial decisions of investors. Both, the success of investments and the overall efficiency of the market may be negatively impacted by herding behavior. Investors who are aware of the inclination towards herding behavior may be able to lessen its impacts by adopting a more independent and analytical approach to investing decision-making and by diversifying their portfolio in order to prevent overconcentration in any one asset or industry. The findings are also consistent with the findings of previous research (Goyal et al., 2023; Mishra & Mishra, 2023; Sachdeva et al., 2023). Furthermore, the findings also determined that mental accounting has a significant influence on the financial decisions of investors. The use of mental accounting might have a negative impact on the performance of investments. Investors who are aware of the inclination towards mental accounting may be able to limit the consequences of this tendency by seeing money as a fungible resource and concentrating on the success of their portfolio as a whole rather than the performance of their individual assets or accounts. The findings were also consistent with the findings of previous research (Elvira et al., 2022; Sherani et al., 2023). Lastly, the moderating effect of financial literacy was also examined between observed variables. The findings were also consistent with the findings of previous research (Grable & Rabbani, 2023; Mustafa et al., 2023; Mutereko et al., 2021).

Stock exchange is the backbone of a country since it directs economic stability and progress. It is very important to analyze the momentum of the stock market, so that the policymakers may use this information while deciding the future aspects of economic growth. Investor behavior is a major factor that decides the future progress of a stock market. The literature identified various factors that cause changes in the investment behaviors of retail investors; still, there remains a gap in the existing knowledge to evaluate these factors in the context of Pakistan. The current study attempted to fulfill this gap and examined various factors that affect the financial decision-making of retail investors who invest in PSX.

The results showed that all exogenous variables have a significant impact on the investment decisions of the retail investor. It was concluded that risk perception plays a role in partial mediation between these variables.

The moderating role of financial literacy can help investors make more informed and effective investment decisions. For instance, financially literate investors are more likely to consider fundamental factors, such as company financials and market trends while evaluating investment opportunities. They are also more likely to diversify their portfolios and manage risks effectively which may help reduce the impact of market volatility and protect their investments. The current research can help to identify effective strategies for improving financial decision-making and promoting financial literacy among investors which can ultimately lead to better investment outcomes and greater financial success.

The current study attempted to explore various dimensions and enhanced the body of existing knowledge regarding the investors' intentions towards investing in PSX. It has some limitations just like the other studies. It analyzed the investment behaviors of retail investors who invest in PSX. Investor behaviors vary within and outside geographical boundaries. Therefore, the future researcher may also conduct research to analyze the behavior of investors who invest in a developed/developing country and then compare the behaviors of individual and institutional investors to get an in-depth understanding. Furthermore, only three indicators of behavioral biases were considered, while future researchers may consider other biases as well to determine the impact of these biases on investor behaviors. In the future, researchers may also go for the exploration of factors affecting the investment decisions of institutional investors in Pakistan.

Adil, M., Singh, Y., & Ansari, M. S. (2022). How financial literacy moderate the association between behaviour biases and investment decision? Asian Journal of Accounting Research, 7(1), 17–30. https://doi.org/10.1108/AJAR-09-2020-0086

Agnew, S., & Harrison, N. (2015). Financial literacy and student attitudes to debt: A cross national study examining the influence of gender on personal finance concepts. Journal of Retailing and Consumer Services, 25, 122–129. https://doi.org/10.1016/j.jretconser.2015.04.006

Ahmad, A., Sohail, A., Hussain, A., & Hussain, F. (2020). Assessment of investment decisions and its determinants among retail investors in emerging economies: Sequential mixed method analysis. Assessment, 11(3), 243–254.

Alarcón, D., Sánchez, J. A. (2015). Assessing convergent and discriminant validity in the ADHD-R IV rating scale: User-written commands for Average Variance Extracted (AVE), Composite Reliability (CR), and Heterotrait-Monotrait ratio of correlations (HTMT). Spanish STATA meeting. https://www.stata.com/meeting/spain15/abstracts/materials /spain15_alarcon.pdf

Ansari, Y., Albarrak, M. S., Sherfudeen, N., & Aman, A. (2022). A study of financial literacy of investors—A bibliometric analysis. International Journal of Financial Studies, 10(2), Article e36. https://doi.org /10.3390/ijfs10020036

Ansari, Y., Albarrak, M. S., Sherfudeen, N., & Aman, A. (2023). Examining the relationship between financial literacy and demographic factors and the overconfidence of Saudi investors. Finance Research Letters, 52, Article e103582. https://doi.org/10.1016/j.frl.2022.103582

Asad, H., Khan, A., & Faiz, R. (2018). Behavioral biases across the stock market investors: Evidence from Pakistan. Pakistan Economic and Social Review, 56(1), 185–209.

Bihari, A., Dash, M., Muduli, K., Kumar, A., Mulat-Weldemeskel, E., & Luthra, S. (2023). Does cognitive biased knowledge influence investor decisions? An empirical investigation using machine learning and artificial neural network. VINE Journal of Information and Knowledge Management Systems. (ahead of print). https://doi.org/10.1108/ VJIKMS-08-2022-0253

Bosch-Rosa, C., & Corgnet, B. (2022). Cognitive finance. InHandbook of Experimental Finance(pp. 73–88). Edward Elgar Publishing. https://doi.org/10.4337/9781800372337.00013

Botzen, W., Duijndam, S., & van Beukering, P. (2021). Lessons for climate policy from behavioral biases towards COVID-19 and climate change risks. World Development, 137, Article e105214. https://doi.org /10.1016/j.worlddev.2020.105214

Bouteska, A., & Regaieg, B. (2017). Overconfidence bias, over/under-reaction of financial analysts on the Tunisian stock market, and their impact on the earnings forecasts. International Journal of Economics and Financial Issues, 7(2), 208–214.

Chakraborty, D., Gupta, N., Mahakud, J., & Tiwari, M. K. (2023). Corporate governance and investment decisions of retail investors in equity: do group affiliation and firm age matter? Managerial Auditing Journal, 38(1), 1–34. https://doi.org/10.1108/MAJ-06-2021-3177

Chen, Y.-F., Chiang, T. C., Lin, F.-L., & Yang, S.-Y. (2021). Dynamic common properties of national herd behavior of stock markets. In Advances in Pacific Basin Business, Economics and Finance. Emerald Publishing Limited. https://doi.org/10.1108/S2514-465020210000009009

Elvira, V., Sutejo, B. S., & Marciano, D. (2022, December). The Effect of financial literacy and demographic factors on behavioral biases of investors during a pandemic (Paper presenttion). In19th International Symposium on Management (INSYMA 2022)(pp. 47-54). Atlantis Press.

Goyal, K., & Kumar, S. (2021). Financial literacy: A systematic review and bibliometric analysis. International Journal of Consumer Studies, 45(1), 80–105. https://doi.org/10.1111/ijcs.12605

Goyal, P., Gupta, P., & Yadav, V. (2023). Antecedents to heuristics: decoding the role of herding and prospect theory for Indian millennial investors. Review of Behavioral Finance, 15(1), 79–102. https://doi.org/10.1108/RBF-04-2021-0073

Grable, J. E., & Rabbani, A. (2023). The Moderating Effect of Financial Knowledge on Financial Risk Tolerance. Journal of Risk and Financial Management, 16(2), e137. https://doi.org/10.3390/jrfm16020137

Gupta, S., & Shrivastava, M. (2022). Herding and loss aversion in stock markets: mediating role of fear of missing out (FOMO) in retail investors. International Journal of Emerging Markets, 17(7), 1720–1737. https://doi.org/10.1108/IJOEM-08-2020-0933

Jain, R., Sharma, D., Behl, A., & Tiwari, A. K. (2022). Investor personality as a predictor of investment intention–mediating role of overconfidence bias and financial literacy. International Journal of Emerging Markets, (ahead of print). https://doi.org/10.1108/IJOEM-12-2021-1885

Jaiyeoba, H. B., Adewale, A. A., Haron, R., & Che Ismail, C. M. H. (2018). Investment decision behaviour of the Malaysian retail investors and fund managers: A qualitative inquiry.Qualitative Research in Financial Markets,10(2), 134–151. https://doi.org/10.1108/QRFM-07-2017-0062

Mishra, P., & Mishra, S. (2023). Do banking and financial services sectors show herding behaviour in Indian Stock Market amid COVID-19 pandemic? Insights from quantile regression approach. Millennial Asia, 14(1), 54–84. https://doi.org/10.1177/09763996211032356

Muneeswaran, R., Babu, M., Gayathri, J., & Indhumathi, G. (2020). Investors cognitive biases and investment decision. International Journal of Management, 11(10), 1643–1650. https://doi.org/10.34218/IJM.11.10.2020.149

Mustafa, W. M. W., Islam, M. A., Asyraf, M., Hassan, M. S., Royhan, P., & Rahman, S. (2023). The effects of financial attitudes, financial literacy and health literacy on sustainable financial retirement planning: the moderating role of the financial advisor. Sustainability, 15(3), Article e2677. https://doi.org/10.3390/su15032677

Mutereko, S., Hussain, A., & Sohail, A. (2021). Assessment of individual and institutional investor's investment behavior during covid-19. A case of emerging economy. Gomal University Journal of Research, 37(3), 267–277.

Nair, P. S., Shiva, A., Yadav, N., & Tandon, P. (2022). Determinants of mobile apps adoption by retail investors for online trading in emerging financial markets. Benchmarking: An International Journal(ahead of print). https://doi.org/10.1108/BIJ-01-2022-0019

Naveed, M., Ali, S., Iqbal, K., & Sohail, M. K. (2020). Role of financial and non-financial information in determining individual investor investment decision: a signaling perspective. South Asian Journal of Business Studies, 9(2), 261–278. https://doi.org/10.1108/SAJBS-09-2019-0168

Osman, I., Alwi, S. F. S., Rehman, M. A., Muda, R., Hassan, F., Hassan, R., & Abdullah, H. (2023). The dilemma of millennial Muslims towards financial management: an Islamic financial literacy perspective. Journal of Islamic Marketing, (ahead of print). https://doi.org/10.1108/JIMA-09-2021-0283

Patel, M. X., Doku, V., & Tennakoon, L. (2003). Challenges in recruitment of research participants. Advances in Psychiatric Treatment, 9(3), 229–238. https://doi.org/10.1192/apt.9.3.229

Quang, L. T., Linh, N. D., Van Nguyen, D., & Khoa, D. D. (2023). Behavioral factors influencing individual investors' decision making in Vietnam market. Journal of Eastern European and Central Asian Research (JEECAR), 10(2), 264–280. https://doi.org/10.15549/jeecar.v10i2.1032

Quddoos, M. U., Rafique, A., Kalim, U., & Sheikh, M. R. (2020). Impact of behavioral biases on investment performance in Pakistan: The moderating role of financial literacy. Journal of Accounting and Finance in Emerging Economies, 6(4), 1199–1205. https://doi.org /10.26710/jafee.v6i4.1512

Rahayu, R., Ali, S., Aulia, A., & Hidayah, R. (2022). The current digital financial literacy and financial behavior in Indonesian millennial generation. Journal of Accounting and Investment, 23(1), 78–94. https://doi.org/10.18196/jai.v23i1.13205

Rasool, N., & Ullah, S. (2020). Financial literacy and behavioural biases of individual investors: empirical evidence of Pakistan stock exchange. Journal of Economics, Finance and Administrative Science, 25(50), 261–278.https://doi.org/10.1108/JEFAS-03-2019-0031

Sachdeva, M., Lehal, R., Gupta, S., & Garg, A. (2023). What make investors herd while investing in the Indian stock market? A hybrid approach. Review of Behavioral Finance, 15(1), 19–37. https://doi.org /10.1108/RBF-04-2021-0070

Sarstedt, M., & Cheah, J.-H. (2019). Partial least squares structural equation modeling using SmartPLS: A software review. Journal of Marketing Analytics, 7, 196–202. https://doi.org/10.1057/s41270-019-00058-3

Setayesh, M. H., & Sarmadinia, A. (2019). A moderate viewpoint to efficient-market hypothesis and behavioral finance: The efficiency of the behavior of participants in transactions. Iranian Journal of Accounting, Auditing and Finance, 3(1), 1–12. https://doi.org/10.22067/ijaaf.v3i1.79558

Shahid, M. N., Aftab, F., Latif, K., & Mahmood, Z. (2018). Behavioral finance, investors' psychology and investment decision making in capital markets: An evidence through ethnography and semi-structured interviews. Asia Pacific Journal of Emerging Markets, 2(1), 14–37.

Sherani, A. W., Naeem, A., & Shah, M. (2023). Following the crowd or making informed choices? the impact of heuristic and prospect biases on portfolio management and performance: Evidence from pakistan's stock market downturn in 2022. International Journal of Business and Management Sciences, 4(1), 203–221.

Sohail, A., Husssain, A., & Qurashi, Q. A. (2020). An exploratory study to check the impact of COVID-19 on investment decision of individual investors in emerging stock market. Electronic Research Journal of Social Sciences and Humanities, 2, 1–13.

Song, C. L., Pan, D., Ayub, A., & Cai, B. (2023). The interplay between financial literacy, financial risk tolerance, and financial behaviour: The moderator effect of emotional intelligence. Psychology Research and Behavior Management, 16, 535–548.

Trejos, C., van Deemen, A., Rodríguez, Y. E., & Gómez, J. M. (2019). Overconfidence and disposition effect in the stock market: A micro world based setting. Journal of Behavioral and Experimental Finance, 21, 61–69. https://doi.org/10.1016/j.jbef.2018.11.001

Warmath, D., Piehlmaier, D., & Robb, C. (2019). The impact of shared financial decision making on overconfidence for married adults. Financial Planning Review, 2(1), e1032. https://doi.org/10. 1002/cfp2.1032

Waweru, N. M., Munyoki, E., & Uliana, E. (2008). The effects of behavioural factors in investment decision-making: a survey of institutional investors operating at the Nairobi Stock Exchange. International Journal of Business and Emerging Markets, 1(1), 24–41. https://doi.org/10.1504/IJBEM.2008.019243

Yamamoto, H., Fujimori, T., Sato, H., Ishikawa, G., Kami, K., & Ohashi, Y. (2014). Statistical hypothesis testing of factor loading in principal component analysis and its application to metabolite set enrichment analysis. BMC bioinformatics, 15(1), 1–9. https://doi.org/10.1186/1471-2105-15-51