Maria Adil1, Muhammad Mudasar Ghafoor2, Muhammad Mobeen Shafqat1, Yasin Munir1, Ghulam Murtaza3, and Salman Naseer4*

1 Department of Business Administration, Government College Women University, Sialkot, Pakistan

2 Department of Commerce, University of the Punjab, Jehlum campus, Pakistan

3 Department of Commerce, Islamia University, Bahawalpur, Pakistan

4 Department of Information Technology, University of the Punjab Gujranwala Campus, Pakistan.

* Corresponding Author: [email protected]

The current research on Corporate Governance (CG) focused mainly on the linkage between board structure and Firm Performance (FP). This meta-analysis aimed to examine the connection between board structure and financial performance, as well as the moderating impact of firm age and size on the link between board structure and performance. A set of 228 effect sizes reported in 50 research studies published between 2015 and 2020 in 47 peer-reviewed publications, exploring board and performance correlations across 22 nations, was analyzed by using the meta-analysis approach proposed by Hedges and Olkin (2014). The analyses were performed in two stages. Firstly, the key effect of board characteristics was determined on FP and was checked for effect size heterogeneity across primary studies. Afterwards, the moderating effect of firm-specific characteristics was explored on this relationship. The results of this meta-analysis revealed that the impact of board structure on FP was influenced by the age and size of the firm. The findings specifically indicated that as compared to older and larger firms, younger and smaller enterprises exhibited a stronger effect of board structure on FP. Additionally, the study also explored particular board structure traits that, depending on firm age and size, had distinctive effects on company performance. Only empirical studies reporting correlation coefficients and regression coefficients as the effect sizes were included in the current research. Subgroup analysis was not performed due to limited time and resources. The current research added to the body of knowledge by carefully examining the findings of previously published studies and by proposing a single statistical value that represents the significant role of the board in FP. Moreover, the study also provided valuable insights that may help the regulators, Board of Directors (BODs), and Chief Executive Officers (CEOs) to make informed decisions in order to improve CG practices and FP.

Keywords: board structure, firm characteristics, Firm Performance (FP), meta-analysis

The business community, regulators, and capital market authorities are increasingly realizing that governance is a key factor in determining corporate performance (Abdullah et al., 2021). The Board of Directors (BODs) of a corporation are one of the most significant Corporate Governance (CG) structures. The CG is governed by board members and enforced and evaluated by different exercises within organizations (Shleifer & Vishny, 1997). The board's main responsibilities include policy planning and implementation, as well as fostering partnerships between the company and its external environment (Ruigrok et al., 2006). According to Brennan (2006), the board of companies is an important part of CG, since it serves as a liaison between stockholders and administrative staff. Resultantly, the board members serve as a liaison between the stakeholders and their representatives (Leech & Leahy, 1991). “Firm value and performance have also been utilized as an index for assessing a company's governance functionality,” in numerous academic research studies. However, the parameters which are used to assess the efficacy of governance processes have yielded inconsistent results.

The study on BOD is one of those parameters (Liu & Fong, 2010). The BODs have an important role in lowering agency costs and resolving disputes that arise from the division of ownership and management (Yu, 2023). Apart from the effectiveness of the BOD’s process, the relationship between BODs and Financial Performance (FP) has determined wide acceptance from both, academia and financial world. The BOD is a top-of-the-organization management group, appointed by shareholders. They are shareholders' elected officials, therefore it is their primary duty to ensure that the agents must act in the best interests of the shareholders. “By separating management and control sections of the decision-making process, the board avoids agency issues” (Panasian, 2003). Effective BOD oversight enhances CG by addressing agency issues and reducing disputes between owners and agencies. The structure of BODs has a profound influence on CG practice in both developed and developing economies. While, this integrative model is increasingly used to explore the effect of board structure on Federal Financial Participation in emerging economies, empirical evidence is still limited. CG, most importantly, is concerned with how authority is exerted over corporate bodies and it is based on the BODs. The BODs comprise of the owners – or their members – who have the power to make the decision and have the authority to recruit, fire, and pay top executives (Baysinger & Butler, 1985). Although, board structure research has been theoretically developed for a long time, it has required detailed debate and conclusive evidence (Bhagat & Bolton, 2008). However, corporate scandals involving some of the world's largest public corporations, such as Enron, WorldCom, and Parmalat, have attracted the masses' attention to BODs in the last two decades (Adams et al., 2010). Since then, boards have been the center of debate for policymakers and the focus of scholarly studies as well. During the COVID-19 outbreak, an organization’s environmental, social, and governance performance has become even more important (Abbas et al., 2022).

The structure of relationship between CG mechanisms and FP has been the subject of over 200 studies, however, the results are still inconsistent on the relationship of board structure with FP. Some studies indicate that a firm’s board structure enhances FP, while other studies state that it does not affect FP. Some scholars have used meta-analysis to examine the relationship and to provide consistent results. However, there is a lack of meta-analytic review on the moderating role of the firm age and firm size that can explain the connection between the structure of the BODs and the performance of the company. The current study aimed to fill this gap and extend the CG literature by analyzing the moderating effect of firm age and firm size. Moreover, this research employed 50 studies published in different journals from 2015-2020.

The existing studies have attempted to investigate the impact of corporate board structure on FP. A meta-analysis of the board structure on FFP is needed for two reasons. Firstly, although prior studies have explained the relationship between board structure and FP, the findings remain inconsistent and inclusive. Secondly, there has been little meta-analysis to focus on the moderating effect of firm age and firm size on the relationship between board structure and FP. The current study has attempted to fill this gap in CG literature.

The current study strives to achieve the following objectives:

i. To examine the impact of different characteristics of the board on FP.

ii. To examine the moderating effect of firm age and firm size on board structure and FP linkage.

iii. To provide a statistical synthesis of the existing research on the board structure and FP linkage.

iv. To assess the competing claims made about the impact of board structure on FP.

v. To explore the amount of heterogeneity in the study.

vi. To investigate and correct the evidence based for publication and misspecification biases.

The current study attempted to contribute to the body of knowledge by carefully reviewing the findings of 50 previous studies, based on five-year researches from the time period (2015-2020) by offering a combined value that would represent the board's position in FP. The study comprised of a large sample size; therefore, the results were more consistent and generalized. It also highlighted the value of CG, such as the BODs for organizations to improve their performance. The remaining sections of the study are based on the literature review, methodology, and conclusion of the study.

The concept of CG underlies the improvement of FP by setting up the responsibility of management to protect shareholders' interests (Dalimunthe et al., 2016). Prior research on the role of CG mechanisms and FP examined the interrelationship between several CG measures and FP (Yermack, 1996). A consensus of the researchers has reached on this point that good CG practices and board performance bring about several advantages for the firm (Pillai & Al-Malkawi, 2018; Pinto et al., 2019). Agency theory has well explained the CG and FP association. Advocates of agency theory suppose that splitting the role of owners and managers creates a divergence of interest between shareholders and management (Fama & Jensen, 1983). The BODs are at the top of hierarchical corporate control structures and their main responsibility is to oversee the agents' activities on behalf of principals (shareholders). The greater the board's authority and power over management, the fewer options managers (agents) have to participate in actions that do not maximize shareholder value (Liu & Fong, 2010).

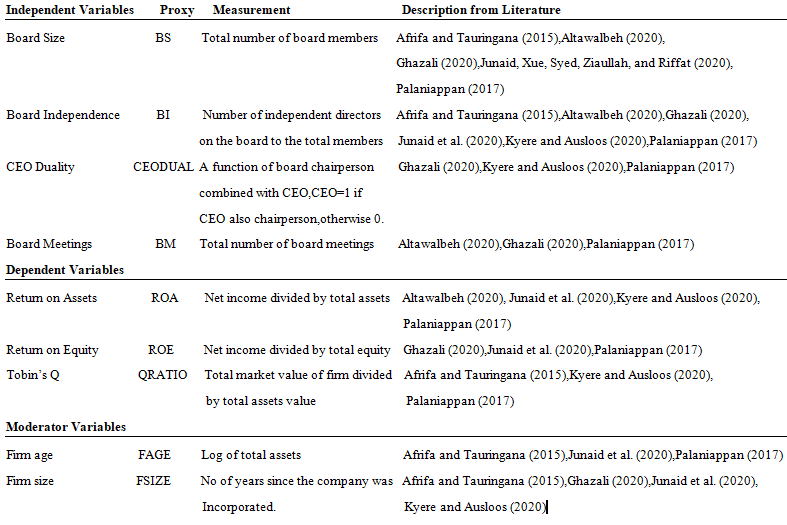

By analyzing the literature, four characteristics or dimensions of the board were selected for the Meta Analysis: that is, Balance Sheet/Board Structure (BS), Business Intelligence (BI), CEO duality, and board meetings. Return on assets (ROA), Return on equity (ROE), and Tobin’s Q are the measures of FP. Table 1 defines the characteristics and mechanisms of the board used in this study.

Table 1

Variable Definition

The CG scholars aimed to determine the optimal BS which improves the board's ability to perform its functions effectively. Agency theory contends that a larger board is enriched with more experiences and skills, thus increasing shareholder value (Saibaba & Ansari, 2012). Resultantly, they fix the agency's issues efficiently (Hussainey & Al‐Najjar, 2012). According to the resource dependence theory, a wider board should have directors from different fields of varying skill sets (Dalton et al., 1999). Since the board has a wider pool of expertise, the experience and intellect gained can be used to make critical strategic decisions for the organization (Pearce & Zahra, 1992; Dalton et al., 1999). The greater the number of board members, the better the company's monitoring capability and ability to shape external links (Goodstein et al., 1994). Khan and Mahmood (2023) states that a small board is beneficial for better firm FP. The empirical evidence on BS and FP relationship is mixed. Therefore, it is useful to look at this relationship in the following way:

Hypothesis 1: Board size significantly impacts the FP.

The percentage of non-executive or outside directors on a board is known as board independence. The firm board's advisory and supervising duties are directly affected by board independence (Handriani & Robiyanto, 2019). The role of the independent board in improving FP is explained from a theoretical perspective. Based on resource dependency theory, Scherrer (2003) argues that outside directors can be a good form of alternative expertise and information for a business (Govindan et al., 2023). Independent directors on boards, according to Jensen and Meckling (1976) safeguard shareholders' interests from opportunistic management actions and, thus they perform their primary role effectively. However, the stewardship principle states that inside board members are better stewards and lead to better management of companies than outside board members, thereby positively impacting the firm efficiency. Since, the empirical evidence of BI and FP is still inconclusive. To get a better understanding of this relationship, the following hypothesis has been considered:

Hypothesis 2: Board Independence significantly impacts FP.

The term "role duality" refers to the CEO's dual role as chairman of the BODs, since there is a risk of abuse of power (Core et al., 1999). According to the stewardship principle, the CEO and Chairman roles should be combined for the better FP of firms (Khan & Mahmood, 2023), while agency theory suggests a separation to avoid a conflict of interests for the chairman in the formulation and implementation of strategies. Gaur et al. (2015) argued that the duality of CEOs has a substantial positive impact on companies' financial position, this argument is aligned with stewardship theory. The individual roles of the Chairman and CEO contribute to the superior performance of companies (Ghazali, 2020; Govindan et al., 2023). In a study of 252 companies, Kyere and Ausloos (2020) found no connection between CEO duality and FP. To get a better understanding of this relationship, the following hypothesis would be considered:

Hypothesis 3: CEO duality significantly impacts the FP.

The number of board meetings conducted by the corporation indicates that there are issues that need to be addressed immediately. Board meetings provide board members with a wealth of knowledge about strategic planning and market conditions (Hahn & Lasfer, 2016). Board members become more efficient when they meet frequently and discuss the issues and suggest ways to resolve those issues on time (Lipton & Lorsch, 1992). Altawalbeh (2020) found that the frequency of board meetings has a positive effect on FP. On the other hand, Lopez-Quesada and Idowu (2018) discovered that frequent board meetings waste organizational energy and, therefore board meetings are negatively associated with firm efficiency. The empirical research studies show mixed results. Therefore, the following hypothesis was drawn to study the impact of board meetings on FP.

Hypothesis 4: Board meetings significantly impact the FP.

Firm age plays a significant role in determining a company's financial results since it indicates how much experience the company has in its operations. Firms, according to Ericson and Pakes (1995), develop and discover new ways to be more effective over time. Firms specialize and learn how to standardize, coordinate, and speed up their manufacturing processes while lowering their costs to improve efficiency. Different dimensions can be used to describe the relationship between firm age and organizational efficiency. The term "firm age" has been used in several studies to describe how long a business has been in operation (Boone et al., 2007; Borghesi et al., 2007; Gregory et al., 2005). It was pointed out that a company's age is a strong indicator of its potential growth prospects. Claessens et al. (2002) found that larger and older companies had more volatile trading, greater transparency, greater market coverage, and more varied operations, resulting in a lower risk of financial turmoil, however, fewer growth prospects. Conversely, smaller and younger businesses may have greater growth opportunities, however, they are more vulnerable to market conditions. Evans (1987) found that while older companies are more competent and have expertise, they are rigid and inflexible to changing market conditions. Different researchers have determined a positive relationship between age and performance since older firms have a superior understanding of the industry. Moreover, they also have the knowledge to solve difficulties and deal with a variety of unpredictable market scenarios. Additionally, older businesses have greater skills, experiences, and resources, thus they have superior FP (Pervan, Pervan, & Ćurak, 2017).

Conversely, Almajali et al. (2012) determined a negative relationship between age with performance. The inverse link implies that older organizations have a bureaucratic structure that renders them rigid and this is the key performance barrier. Previous studies used firm age as a control variable to investigate the performance of firms. None of the studies investigated the moderating role of firm age on the study variables. However, the current study aimed to explore the moderating effect of firm age on the relationship between board structure and FP. Board characteristics are linked to company age differences, the reason is that firms tend to become more complex as they grow, resulting in performance variance (Aktas et al., 2019).

Hypothesis 5: Firm age moderates the relationship between board structure and FP.

Many different factors influence a company's FP. Due to the strengths and weaknesses that come with different levels of development, it has been shown that the size of an organization affects its results and hlps to attain various advantages (Yu et al., 2022). Due to economies of scale, large businesses can benefit from cost savings (Chandler, 1990). Large companies are reluctant to introduce and implement emerging technology in some cases due to bureaucracy and organizational rigidities (Tripsas & Gavetti, 2000). In contrast to small businesses, which aim to capture new and future markets, large corporations have a propensity to concentrate solely on established markets. Academic literature acknowledges that the economies of scales and synergies exist up to a certain size of threshold. Beyond that point, financial organizations become considerably complicated to handle which results in scale inefficiencies. According to various studies, the relationship between firm size and efficiency is unclear (Agrawal & Knoeber, 1996; Durnev & Kim, 2005; Himmelberg et al., 1999; Nenova, 2003). Larger businesses have a better chance of internally generating and raising funds as well as foreign funding as compared to smaller businesses (Joh, 2003). Furthermore, according to Jensen (1986), agency problems can be identified by using a firm scale. Managers are encouraged to expand their businesses beyond the target size so the amount of assets under their supervision increases, giving them more leverage. According to Jensen (1986) as a firm's size grows, it becomes more diversified. It also means that larger companies need more board representation. Furthermore, larger companies are associated with more complex activities to execute their business strategies in a more effective way. According to Serrasqueiro and Nunes (2008), larger firms are more efficient because they have more ways to generate capital and have more diverse strategies. It also has a broad range of knowledge management. According to (Kim, Black, & Jang, 2006), firm size has a positive correlation with company performance. On the other hand, Agrawal and Knoeber (1996) negatively correlate with FP. They claim that larger companies are less competitive than smaller firms because management has little influence over strategic and operational practices as the company grows in size. According to Garen (1994), the expense of adhering to CG code standards would be relatively low for larger organizations. However, if the businesses are subjected to public scrutiny, this cost would rise. This is because they will be scrutinized by the media even more than smaller companies (Garen,1994). Finally, Jensen and Meckling (1976) conclude that as an organization increases in size, agency costs are likely to increase as well. The need for more control, as a result of managerial opportunism, has resulted in a rise in costs. Furthermore, the firm's expansion would necessitate the expansion of internal control methods for design and forecasting. This would necessitate the managers' and shareholders' interests to be aligned (Jensen & Meckling, 1976). Larger and more complicated firms are thought to have more formal governance mechanisms, which translates to greater monitoring than smaller firms (Strom et al., 2014). The natural logarithm of total assets will be used to measure FSIZE in this analysis, as it is used in previous research (Al-Matari et al., 2012; Elsayed, 2007; Muth & Donaldson, 1998; Topak, 2011). Previous studies used firm size as control variable. However, literature supports the moderation impact of firm size on the study variables (Yu et al., 2022). Thus, the current study constituted moderator analysis by using firm size explaining the board structure and performance linkage (Govindan et al., 2023).

Hypothesis 6: Firm size moderates the relationship between board structure and FP.

For data collection, original research papers were obtained based on the relationship between CG, board structure, and FFP. Some databases were searched for required articles, that is, Emerald, Google Scholar, Jstor, Springer Link, Wiley, and Elsevier, to ensure the effectiveness and to recognize the literature to be included in the current study. The following terms were used to search the published data for five years from the time period (2015-2020): CG, board structure, board characteristics and FP, and CG, FP, and risk management committee as a mediating variable. The data was collected from various recognized journals.

These journals include (1) International Journal of Business and Social Science, (2) Accounting and Finance Research, (3) International Journal of Emerging Markets, (4) The international Journal of Business in Society, (5) Gender in Management: An International Journal,(6) International Journal of Finance & Economics, (7) Management Decision, (8) Social Responsibility Journal, (9) Asian Journal of Accounting Research, (10) Green Finance, (11) Managerial Finance, (12) Procedia Economics and Finance, (13) Pacific Accounting Review, (14) European Journal of Management and Business Economics, (15) African Journal of Economic and Management Studies, (16) Journal of Asian Business and Economic Studies, (17) Asia-Pacific Journal of Business Administration, (18) Australasian Accounting Business and Finance Journal, (19) Handbook of Research on Accounting and Financial Studies (20) Journal of Asia Business Studies, (21) Advances in Economics Business and Management Research, (22) Finance and Accounting Area, (23) Sustainability, (24) International Journal of Law and Management, (25) International Business Review, (26) Journal of Finance and Bank Management,(27) Economic Research-Ekonomska Istraživanja,(28) International Journal of Contemporary Hospitality Management, (29) Research in Finance, (30) Global Business Review, (31) Chinese Management Studies, (32) International Management Review, (33) Journal of Accounting in Emerging Economic, (34) Journal of Advances in Management Research, (35) International Journal of Accounting and Information Management ,(36) Nankai Business Review, (37)Tourism Management perspective, (38) International Journal of Entrepreneurship and small Business, (39) International Journal of Business and Economics Research,(40) South Asian Journal of Business Studies, (41) Journal of International Studies, (42) International Journal of Advances in Management and Economics, (43) International Journal of Management, Accounting and Economics, (44) European Research Studies Journal, (45) International Journal of Productivity and Performance Management, (46) Int. Journal of Managerial and Financial Accounting, (47) Corporate Governance.

The inclusion criteria was based on the following dimensions for collection of studies. Firstly, the study must have indicators of an independent and dependent variable, at least one of the dimensions of board structure and FP. Secondly, the studies must be empirical and quantitative, thus excluding all the qualitative studies. Thirdly, studies having parameters of meta-analysis, that is, sample size, partial correlation, Pearson correlation, simple linear regression, multiple linear regression, and t value were chosen. Pearson correlation and partial correlation were used as the effect sizes (Mutlu et al., 2018). Fourthly, results already presented in other studies have been omitted (Wang et al, 2015). Fifthly, studies published during the period 2015-2020 were selected to conduct the current research. Sixth, selected studies have articles with full access.

The random effect model was used to test the hypothesis with a confidence interval of 95%. To search for heterogeneity between board characteristics and FP, the and Q values were then analyzed. If the index reaches 50%, then subgroup analysis would be carried out. Classic Fail-safe N Rosenthal,(1979) and Egger's regression intercept (Egger, Smith, Schneider, & Minder, 1997) were used to check publication biased. Publication bias exists when researchers publish significant results while leaving out insignificant results. A higher Fail-safe coefficient shows the best results. Egger’s regression intercept value, far off from 0.05, indicates the best results and claims that there is no bias in meta-analysis.

Publication Bias

The results of publication bias tests for the association between board structure and FP are presented in Table 2. Except for board meetings, Fail-safe N is high in all other relationships. Furthermore, except for the association between board independence and ROA, the p-value of Egger's regression intercept for all other relationships is more than .05.

Table 3 reports the results of relationship between board and FP. Overall results showed a positive relationship between board structure and FP. As shown in Table 3, board size positively correlates with FP measured by ROA ( =0.20), ROE ( =0.24) and Q ratio ( =0.18). Board independence also positively correlated with FP measured by ROA ( =0.18), ROE =0.18), and Q ratio ( =0.28). CEO duality positively influences the FP measured by ROA ( =0.21), ROE =0.35), and Q ratio =0.14). Furthermore, board meetings positively correlate with FP in terms of ROA =0.34), ROE =0.34), and Q ratio =0.34). A confidence interval of 95% does not have 0, which means that all results are significant. Firms can improve their performance by focusing on their board structure.

Table 2

The Results of the Publication Bias Test

|

Relationships |

K |

N |

Classic Fail-Safe N |

Egger’s Intercept |

p |

|

Board Size →ROA |

40 |

10532 |

4783 |

0.99 |

0.461 |

|

Board Size →ROE |

19 |

3767 |

1020 |

1.33 |

0.290 |

|

Board Size →Tobin’s Q |

23 |

6265 |

2335 |

-2.28 |

0.189 |

|

Board Independence →ROA |

36 |

6700 |

4720 |

-3.98 |

0.008 |

|

Board Independence →ROE |

21 |

4396 |

729 |

0.92 |

0.504 |

|

Board Independence →Tobin’s Q |

23 |

6839 |

6023 |

-2.11 |

0.361 |

|

CEO Duality →ROA |

18 |

6849 |

1023 |

2.79 |

0.116 |

|

CEO Duality →ROE |

10 |

2668 |

1134 |

1.13 |

0.609 |

|

CEO Duality →Tobin’s Q |

12 |

1884 |

113 |

0.84 |

0.786 |

|

Board Meeting →ROA |

12 |

5265 |

1735 |

0.81 |

0.472 |

|

Board Meeting →ROE |

7 |

1784 |

652 |

-2.57 |

0.233 |

|

Board Meeting →Tobin’s Q |

7 |

1296 |

369 |

0.30 |

0.896 |

Table 3

Meta-Analysis of Relationships between Board Structure and Firm Performance (FP)

|

|

K |

N |

RC |

95% CI (LL UL) |

Z |

Q |

PQ |

I2 |

|

|

Board Size →ROA |

40 |

10532 |

0.20 |

0.11 |

0.29 |

4.42 |

867.05 |

0.00 |

95.5% |

|

Board Size →ROE |

19 |

3767 |

0.24 |

0.14 |

0.34 |

5.13 |

138.11 |

0.00 |

86.97% |

|

Board Size →Tobin’s Q |

23 |

6265 |

0.18 |

0.09 |

0.28 |

3.95 |

368.85 |

0.00 |

94.04% |

|

Board Independence →ROA |

36 |

6700 |

0.18 |

0.10 |

0.27 |

4.44 |

878.68 |

0.00 |

96.02% |

|

Board Independence → ROE |

21 |

4396 |

0.18 |

0.06 |

0.30 |

3.18 |

190.03 |

0.00 |

89.48% |

|

Board Independence →Tobin’s Q |

23 |

6839 |

0.28 |

0.16 |

0.39 |

5.07 |

470.40 |

0.00 |

95.32% |

|

CEO Duality →ROA |

18 |

6849 |

0.21 |

0.09 |

0.32 |

3.72 |

314.31 |

0.00 |

94.59% |

|

CEO Duality →ROE |

10 |

2668 |

0.35 |

0.21 |

0.50 |

5.69 |

79.84 |

0.00 |

88.73% |

|

CEO Duality →Tobin’s Q |

12 |

1884 |

0.14 |

-0.08 |

0.35 |

1.41 |

358.80 |

0.00 |

96.93% |

|

Board Meeting →ROA |

12 |

5265 |

0.34 |

0.23 |

0.44 |

7.16 |

61.49 |

0.00 |

82.11% |

|

Board Meeting →ROE |

7 |

1784 |

0.34 |

0.17 |

0.51 |

4.83 |

45.00 |

0.00 |

86.67% |

|

Board Meeting →Tobin’s Q |

7 |

1296 |

0.34 |

0.17 |

0.50 |

4.88 |

28.26 |

0.00 |

78.77% |

Table 4

Moderating Effects of Firm Age on the Relationship between Board Structure and Firm Performance (FP)

|

Relationships |

K |

ꞵ |

LL |

UL |

P |

S.E |

R² |

|

Board Size →ROA |

16 |

0.01*** |

0.01 |

0.01 |

0.000 |

0.0010 |

26.48% |

|

Board Size →ROE |

9 |

-0.01*** |

-0.01 |

0.00 |

0.000 |

0.0018 |

42.43% |

|

Board Size →Tobin’s Q |

11 |

0.01*** |

0.01 |

0.01 |

0.000 |

0.0011 |

43.67% |

|

Board Independence →ROA |

16 |

0.00 |

0.00 |

0.00 |

0.960 |

0.0010 |

0.00% |

|

Board Independence →ROE |

10 |

-0.01*** |

-0.01 |

0.00 |

0.000 |

0.0018 |

42.39% |

|

Board Independence →Tobin’s Q |

11 |

0.01*** |

0.00 |

0.01 |

0.000 |

0.0010 |

16.71% |

|

CEO Duality →ROA |

10 |

0.01** |

0.00 |

0.01 |

0.004 |

0.0025 |

12.52% |

|

CEO Duality →ROE |

4 |

-0.01* |

-0.02 |

0.00 |

0.032 |

0.0034 |

14.73% |

|

CEO Duality →Tobin’s Q |

6 |

0.01 |

-0.01 |

0.03 |

0.294 |

0.0073 |

2.05% |

|

Board Meeting →ROA |

3 |

0.03 |

-0.09 |

0.15 |

0.292 |

0.0276 |

1.86% |

|

Board Meeting →ROE |

1 |

|

|

|

|

|

|

|

Board Meeting →Tobin’s Q |

2 |

2.14** |

-6.28 |

10.56 |

0.001 |

0.6625 |

100.00% |

Note. k = the number of samples in the regression analysis, S. E=standard error; firm size was coded as a log of firm assets. *p < .05. **p < .01. ***p < .001.

Table 5

Moderating Effect of Firm Size on the Relationship between Board Structure and Firm Performance (FP)

|

Relationships |

K |

ꞵ |

LL |

UL |

P |

S. E |

R² |

|

Board Size →ROA |

21 |

0.01*** |

0.13 |

0.23 |

0.000 |

0.0013 |

11.34% |

|

Board Size →ROE |

8 |

-0.03*** |

-0.04 |

-0.02 |

0.000 |

0.0051 |

84.64% |

|

Board Size →Tobin’s Q |

14 |

0.02*** |

0.01 |

0.02 |

0.000 |

0.0010 |

64.46% |

|

Board Independence →ROA |

20 |

0.02*** |

0.02 |

0.03 |

0.000 |

0.0011 |

62.22% |

|

Board Independence →ROE |

7 |

-0.02*** |

-0.03 |

-0.01 |

0.000 |

0.0053 |

37.63% |

|

Board Independence →Tobin’s Q |

14 |

0.02*** |

0.02 |

0.02 |

0.000 |

0.0010 |

64.38% |

|

CEO Duality →ROA |

12 |

0.02*** |

0.02 |

0.02 |

0.000 |

0.0014 |

59.34% |

|

CEO Duality →ROE |

4 |

-0.02 |

-0.05 |

0.02 |

0.108 |

0.0105 |

6.04% |

|

CEO Duality →Tobin’s Q |

9 |

0.01*** |

0.01 |

0.02 |

0.000 |

0.0014 |

47.53% |

|

Board Meeting →ROA |

5 |

0.00 |

-0.01 |

0.01 |

0.774 |

0.0021 |

0.09% |

|

Board Meeting →ROE |

2 |

0.04** |

-0.12 |

0.19 |

0.001 |

0.0122 |

100.00% |

|

Board Meeting →Tobin’s Q |

3 |

-0.02** |

-0.06 |

0.02 |

0.009 |

0.0090 |

10.51% |

Note. k = the number of samples in the regression analysis, S. E=standard error; firm size was coded as a log of firm assets. *p < .05. **p < .01. ***p < .001.

Tables 4 and 5 reports the results of the moderating effect of firm age and firm size on the relationship between board structure and FP.

Table 4 reports the moderating effect of firm age on the relationship between board structure and FP. Firm age positively moderates the relationship between board size and ROA (B=0.01, p˂.001), board size and Tobin’s Q (B=0.01, p˂.001), board independence and Tobin’s Q (B=0.01, p˂.001), CEO duality and ROA (B=0.01, p˂.01), board meeting and Tobin’s Q (B=2.14, p˂.01). Moreover, it negatively moderates the relationship between board size and ROE (B=-0.01, p˂.001), board independence and ROE (B=-0.01, p˂.001), CEO duality and ROE (B=-0.01, p˂.05). However, the moderating effect was not significant in other relationships, that is, board independence and ROA, CEO duality and Tobin’s Q and board meeting and ROA. Therefore, the hypothesis has been partially supported.

Table 5 reports the moderating effect of FSIZE on the relationship between board structure and FP. FSIZE positively moderates the relationship between BS and ROA(B=0.01, p˂.001), BS and Tobin’s Q (B=0.02, p˂.001), BI and ROA (B=0.02, p˂.001), BI and Tobin’s Q(B=0.02, p˂.001), CEO duality and ROA (B=0.02, p˂.001), CEO duality and Tobin’s Q(B=0.01, p˂.001), BM and ROE(B=0.04, p˂.01), and negatively moderates the relationship between BS and ROE(B=-0.03, p˂.001), BI and ROE (B=-0.02, p˂.001), BM and Tobin’s Q(B=-0.02, p˂.01). However, the moderating effect was not significant for the relationship between CEO duality and ROE, and BM and ROA. Therefore, the hypothesis is partially supported.

The current study attempted to explore the relationship between board structure and organizational performance through the moderating influence of firm age and firm size by using the technique of meta-analysis. The direct relationship between all four dimensions of board and performance was positive as shown in Table 3. The first hypothesis that board size significantly affects the FP is tested as indicated in Table 3. Table 3 reveals the correlation values that directly influences the relationship between size and FP as measured by different performance measures, such as ROA, ROE, and Tobin’s Q. The correlation values, that is, ROA=0.20, ROE=0.24, and Q ratio=0.18 confirm this relationship. Thus, the findings supported H1 which states that the board size positively and significantly affects the FP.

The second hypothesis posits that board independence has a positive effect on FP. The correlation values as measured by ROA=0.20, ROE=0.24, and Q ratio=0.18 prove this claim and the results are consistent with (Habbash & Bajaher, 2015). According to resource dependency theory, the independent directors are a good source of information and expertise. The findings were consistent with Handriani and Robiyanto (2019) which state that the independent directors directly influence all the decisions made by the supervisory board. The third hypothesis states that CEO duality influences the FP. The relationship between CEO duality and FP is confirmed by the correlation values measured by ROA=0.21, ROE=0.35, and Q ratio=0.14. The findings were consistent with (Gaur et al 2015) and also with stewardship theory.

Furthermore, board meetings positively correlate with FP in terms of ROA=0.34, ROE=0.34, and Q ratio=0.34. Thus, the findings supported H4. The relationship between board structure and FP is influenced or moderated by various contextual factors, such as firm age and firm size (Prashar & Gupta, 2021). The fifth hypothesis states that firm age moderates the relationship under study. This hypothesis is partially supported as indicated in Table 4 since some of the relationships are positive and some are negative and also some of the values measured by performance measures are insignificant. Hence, this relationship is partially supported. Literature supports the moderating role of firm age between CEO duality and FP, Bathula (2008). As firms grow in age and their operations increase, they require the separation of two positions to make fewer chances for CEO to misuse their power. The performance of the organization can be improved when the board is chaired by an independent person in the long run (Akisimire et al., 2020).

Hypothesis 6 proposes that firm size moderates the relationship between board structure and FP. This hypothesis is also partially supported as some of the relationships are positive and some are negative and some of the dimensions of board structure show insignificant results with different performance measures. According to contingency theory, firm size is one of the contingent organizational factors and it can be used as moderating variable which might influence firm activities. Studies show that larger board and FP depend on firm size because large boards inhibit positive benefits in small businesses. However, this detrimental effect lessens as firm size increases (Zona et al., 2013).

Regarding board independence, research shows that lack of interaction among group members reduces FP in small businesses where they are not supported to implement their innovative ideas in the best interest of firms. The failure rates of smaller firms are high because they cannot implement their strategies successfully as they do not have access to external resources, that is, outside directors (Zona et al., 2013). As far as the duality of CEO is concerned, small firms show a negative relationship between CEO duality and FP. However larger firms have access to more resources and can compete in the business environment. Moreover, their well-organized structure enables their CEOs to make quick decisions which ultimately results in the high performance of large firms. The CEOs in larger firms have fewer chances of fraud since they are supervised by a proper regulatory system, hence larger firms positively moderate the relationship between CEO duality and FP (Mubeen et al., 2021).

As far as the outsider ratio is concerned, the literature on group efficacy suggests that a lack of interaction between group members (for instance, an increasing proportion of part-time outside directors on the board) reduces firm innovation. Moreover, this negative effect increases in smaller firms, where boards are less supported by the organization while making decisions on corporate innovation (Zona et al., 2013). Interestingly, the results for the main effect (that is, before introducing the moderating variable; see Model 2 of Table 2) are consistent with the previous literature, because no significant association has been found between the outsider ratio and firm innovation.

For the last couple of decades, researchers have been extensively examining the impact of various mechanisms of CG on FP. The current literature has described board structure as one of the most robust and foremost mechanisms of CG that impacts FFP. The current study summarized the results of previous empirical research studies on the relationship between board structure and its effect on FP by using meta-analysis. The research goals were achieved by using meta-analysis approach suggested by Hedges and Olkin (2014). The online database search and inclusion-exclusion criteria provided 50 studies with 228 reported effects from 47 peer-reviewed journals published between the time period (2015-2020). Four attributes of the board were selected to investigate the board structure and performance linkage. Besides this, the current study explored the moderating effect of FAGE (Firm Age) and FSIZE (Firm Size). The analyses were performed in two steps. Firstly, the main effect of board characteristics was examined on FP. Afterwards, the moderating variable's effect was examined on the relationship between different dimensions of the board and FP. Incorporating the research findings of 50 empirical studies on the linkage between board structure and FP, the current study endorsed the pervasive argument that board structure improves the performance of the firms. One of the recent studies indicated the productive effect of innovative Corporate Social Responsibility (CSR) and business practices on FP that had lost their operational capabilities in COVID-19 pandemic (Abbas et al., 2022).

Another study recommended that the partial lockdown can enhance the performance of the firms by reopening them in COVID-19 situation as the positive cases had a spillover effect on health and economy and the management could function properly without narrowing its size and locking down operational capabilities with partial lockdown restrictions (Wang et al., 2021). Meta-Analysis further acknowledged the results from the relevant study for the main effect that revealed that Board Size, Board Independence, CEO Duality, and Board Members have significant and positive impact on the performance through innovative business strategies. In any crisis, the innovative business approach and CSR are helpful to improve the performance of the firms through spiritual leadership to stimulate positive behavior of the employees (Usman et al., 2021). Moreover, in crisis management the social media marketing plays a moderating role between environmental factors and CSR to strengthen the firm’s sustainable business performance (Abbas et al., 2019). In the current study, although some of the results contradict the hypothesis, they do confirm the moderating effect of FAGE on the relationship between board and FP. The results of moderator analysis indicate that FAGE positively moderates the relationship between different characteristics of the board and performance, measured by ROA and Tobin’s and negatively moderates the relationship between the board and ROE. Additionally, the results confirm the moderating effect of FSIZE on the relationship between the board and FP. The results indicate that firm size positively moderates the relationship between BS, BI, CEO duality, and performance (ROA, Tobin’s Q) and negatively moderates between these three mechanisms of board and ROE. While, FSIZE positively moderates between board meetings and ROE and negatively moderates between a board meeting and market performance (Tobin’s Q).

The results of previous empirical researches have been incorporated into the current study by using meta-analysis approach which added to the research field. The current study underscored the significance of the board as an instrument to strengthen the CG and has theoretical and practical implications. The prior researches provided inconsistent conclusions while investigating the impact of board structure on FP. However, this study provided reliable correlation coefficients between several variables by controlling the possible errors, that is, measurement and sampling errors existing in previous empirical studies. Therefore, based on previous empirical studies, the current study yielded more consistent findings and facilitated a thorough understanding of the relationship between different dimensions of the board and FP. This, in combination with other theories, such as agency theory, resource dependency theory, and stewardship theory have been used to postulate the hypothesis in order to explain the role of board characteristics in improving the performance. The current study also established that firm age and firm size moderate the association between board and FP.

This study also served as a valid reference to guide future researchers in exploring the association between board characteristics and FP, and further identifying the moderating factors, such as FAGE and FSIZE that influence the relationships. The results provided conclusive suggestions for the practitioners to consider board characteristics in improving the FP. It also provided the managers with a thorough understanding of the structure of the board and its effectiveness in improving the performance. It provided guidelines for corporations to formulate their structure and policies. Top executives may persuade their owners to maintain the optimum size of the board which can help the firms cope with uncertain settings in which the firm operates. Practitioners also need to take into account different contextual factors, such as firm size and age while designing BODs because board structure influences the FP depending on these factors.

One of the objectives of the current study was to combine and organize the previous studies in order to identify the research gaps. This study emphasized the inconsistencies in the previous studies on the linkage between board and FP. There could be different reasons, that is, the difference in measures for performance, economic and political situations of nations, and different estimates used to evaluate these measures. The impact of four dimensions was examined on FP. Whereas, other dimensions, such as directors and manager’s specific characteristics (age, tenure, experience), board gender diversity, director’s remuneration, their shareholdings, and other board committees could not be included implying that enough literature was not available for these dimensions. The current study exhibited the findings of meta-analysis on the linkage between dimensions of board and FP by summarizing previous research studies reporting correlation coefficient as effect size. Studies reporting other effect sizes, such as z-value, were eliminated. Another limitation of the study is that subgroup was not conducted due to limited time and resources.

Future researchers must adopt uniform measures of FP. The internal CG mechanisms have been used in the current study, however, external CG mechanisms, such as ownership concentration and audit committees can also be included in meta-analysis. Future researchers may conduct subgroup analysis based on different factors, such as by grouping the firms in developed and developing economies. Future researchers can also perform analysis on companies having homogenous characteristics or can also make comparisons between firms of different sectors. Additionally, future researchers should confirm the moderating effect of FAGE and FSIZE with the help of more empirical studies. The moderating role of other variables may also be explored, such as CSR, family control, and leverage with meta-analysis.

Policymakers should take into account the guidelines and doctrines recommended by international organizations to ensure the best practices (Van Essen, van Oosterhout, & Carney, 2012). Different sensitization programs need to be conducted to aware the owners of the CG practices. Moreover, such programs would make the organizations aware of the benefits of adopting CG practices, especially having a well-structured board to improve organizational FP. Overall results indicated that board characteristics are crucial and carry significant implications for FP. Prior studies are organized and combined in this meta-analysis to promote empirical understanding of this concept (Card, 2015). Thus, the findings reaffirmed that FP can be improved by implementing good CG practices (Khan & Mahmood, 2023). An important limitation is that the political engineering of the system always remains obstacle in getting best output from the policy. Political phenomenon sometimes leads to corruption and ultimately disturbs the CSR that effects the performance of the firms (Hossain & Kryzanowski, 2021).

Abbas, J., Al-Sulaiti, K., Lorente, D. B., Shah, S. A. R., & Shahzad, U. (2022). Reset the industry redux through corporate social responsibility: The COVID-19 tourism impact on hospitality firms through business model innovation. In M. Shahbaz, D. B. Lorente & R. Sharma (Eds.), Economic growth and environmental quality in a post-pandemic world (pp. 177–201): Routledge. https://doi.org/10.4324/9781003336563

Abbas, J., Mahmood, S., Ali, H., Ali Raza, M., Ali, G., Aman, J., Bano, S., & Nurunnabi, M. (2019). The effects of corporate social responsibility practices and environmental factors through a moderating role of social media marketing on sustainable performance of business firms. Sustainability, 11(12), Article e3434. https://doi.org/10.3390/su11123434

Abdullah, A. H., Yusoff, S., Islam, A., & Ahmad, H. A. (2021). Effect of board composition on the corporate performance: The moderating role of corporate governance practices in Iraq. Psychology and Education Journal, 58(3), 2688–2706.

Adams, R. B., Hermalin, B. E., & Weisbach, M. S. (2010). The role of boards of directors in corporate governance: A conceptual framework and survey. Journal of economic literature, 48(1), 58–107.

Agrawal, A., & Knoeber, C. R. (1996). Firm performance and mechanisms to control agency problems between managers and shareholders. Journal of Financial and Quantitative Analysis, 31(3), 377–397. https://doi.org/10.2307/2331397

Akisimire, R., Abaho, E., & Tweyongyere, M. (2020). CEO duality and financial performance: testing the moderating role of firm age: Evidence from a developing economy. Journal of Economics and Behavioral Studies, 12(3), 53–64. https://doi.org/10.22610/jebs.v12i3(J).3016

Aktas, N., Andreou, P. C., Karasamani, I., & Philip, D. (2019). CEO duality, agency costs, and internal capital allocation efficiency. British Journal of Management, 30(2), 473–493. https://doi.org/10.1111/1467-8551.12277

Al-Matari, E. M., Al-Swidi, A. K., Fadzil, F. H., & Al-Matari, Y. A. (2012). The impact of board characteristics on firm performance: Evidence from nonfinancial listed companies in Kuwaiti Stock Exchange. International Journal of Accounting and Financial Reporting, 2(2), 310–332. http://doi.org/10.5296/ijafr.v2i2.2384

Almajali, A. Y., Alamro, S. A., & Al-Soub, Y. Z. (2012). Factors affecting the financial performance of Jordanian insurance companies listed at Amman Stock Exchange. Journal of Management Research, 4(2), 266–289. https://doi.org/10.5296/jmr.v4i2.1482

Altawalbeh, M. A. F. (2020). corporate governance mechanisms and firm’s performance: Evidence from Jordan. Accounting and Finance Research, 9(11), 11–22. https://doi.org/10.5430/afr.v9n2p11

Bathula, H. (2008). Board characteristics and firm performance: Evidence from New Zealand [Doctoral dissertation, Auckland University of Technology]. The AUT Research Repository. https://openrepository.aut.ac.nz/items/5bc22f28-ad72-4986-9fb4-ee80fd2d55af

Baysinger, B. D., & Butler, H. N. (1985). Corporate governance and the board of directors: Performance effects of changes in board composition. Journal of Law, Economics, & Organization, 1(1), 101–124.

Bhagat, S., & Bolton, B. (2008). Corporate governance and firm performance. Journal of corporate finance, 14(3), 257–273. https://doi.org/10.1016/j.jcorpfin.2008.03.006

Boone, A. L., Field, L. C., Karpoff, J. M., & Raheja, C. G. (2007). The determinants of corporate board size and composition: An empirical analysis. Journal of financial Economics, 85(1), 66–101. https://doi.org/10.1016/j.jfineco.2006.05.004

Booth, J. R., & Deli, D. N. (1996). Factors affecting the number of outside directorships held by CEOs. Journal of Financial Economics, 40(1), 81–104. https://doi.org/10.1016/0304-405X(95)00838-6

Borghesi, R., Houston, J., & Naranjo, A. (2007). Value, survival, and the evolution of firm organizational structure. Financial Management, 36(3), 5–31. https://doi.org/10.1111/j.1755-053X.2007.tb00078.x

Brennan, N. (2006). Boards of directors and firm performance: is there an expectations gap? Corporate Governance: An International Review, 14(6), 577–593.

Chandler, A. D. (1990). Strategy and structure: Chapters in the history of the industrial enterprise (Vol. 120). MIT press.

Card, N. A. (2015). Applied meta-analysis for social science research: Guilford Publications.

Claessens, S., Djankov, S., Fan, J. P., & Lang, L. H. (2002). Disentangling the incentive and entrenchment effects of large shareholdings. The Journal of Finance, 57(6), 2741–2771. https://doi.org/10.1111/1540-6261.00511

Core, J. E., Holthausen, R. W., & Larcker, D. F. (1999). Corporate governance, chief executive officer compensation, and firm performance. Journal of Financial Economics, 51(3), 371–406. https://doi.org/10.1016/S0304-405X(98)00058-0

Dalimunthe, D. M. J., Fadli, I. M., & Muda, I. (2016). The application of performance measurement system model using Malcolm Baldrige Model (MBM) to Support Civil State Apparatus Law (ASN) Number 5 of 2014 in Indonesia. International Journal of Applied Business & Economic Research, 14(11), 7397–7407.

Dalton, D. R., Daily, C. M., Johnson, J. L., & Ellstrand, A. E. (1999). Number of directors and financial performance: A meta-analysis. Academy of Management Journal, 42(6), 674–686. https://doi.org/10.5465/256988

Durnev, A., & Kim, E. H. (2005). To steal or not to steal: Firm attributes, legal environment, and valuation. The Journal of Finance, 60(3), 1461–1493. https://doi.org/10.1111/j.1540-6261.2005.00767.x

Elsayed, K. (2007). Does CEO duality really affect corporate performance? Corporate Governance: An International Review, 15(6), 1203–1214. https://doi.org/10.1111/j.1467-8683.2007.00641.x

Egger, M., Smith, G. D., Schneider, M., & Minder, C. (1997). Bias in meta-analysis detected by a simple, graphical test. Bmj, 315(7109), 629-634.

Ericson, R., & Pakes, A. (1995). Markov-perfect industry dynamics: A framework for empirical work. The Review of Economic Studies, 62(1), 53–82. https://doi.org/10.2307/2297841

Evans, D. S. (1987). The relationship between firm growth, size, and age: Estimates for 100 manufacturing industries. The Journal of Industrial Economics, 35(4), 567–581. https://doi.org/10.2307/2098588

Fama, E. F., & Jensen, M. C. (1983). Separation of ownership and control. The Journal of Law and Economics, 26(2), 301–325.

Garen, J. E. (1994). Executive compensation and principal-agent theory. Journal of Political Economy, 102(6), 1175–1199.

Gaur, S. S., Bathula, H., & Singh, D. (2015). Ownership concentration, board characteristics and firm performance. Management Decision, 53(5), 911–931. https://doi.org/10.1108/MD-08-2014-0519

Ghazali, N. A. M. (2020). Governance and ownership in Malaysia: Their impacts on corporate performance. Asian Journal of Accounting Research, 5(2), 285–298. https://doi.org/10.1108/AJAR-03-2020-0017

Goodstein, J., Gautam, K., & Boeker, W. (1994). The effects of board size and diversity on strategic change. Strategic Management Journal, 15(3), 241–250. https://doi.org/10.1002/smj.4250150305

Govindan, K., Karaman, A. S., Uyar, A., & Kilic, M. (2023). Board structure and financial performance in the logistics sector: Do contingencies matter? Transportation Research Part E: Logistics and Transportation Review, 176, Article e103187. https://doi.org/10.1016/j.tre.2023.103187

Gregory, B. T., Rutherford, M. W., Oswald, S., & Gardiner, L. (2005). An empirical investigation of the growth cycle theory of small firm financing. Journal of Small Business Management, 43(4), 382–392.

Habbash, M. S., & Bajaher, M. S. (2015). An empirical analysis of the impact of board structure on the performance of large Saudi firms. Arab Journal of administrative sciences, 22(1), 91–105.

Hahn, P. D., & Lasfer, M. (2016). Impact of foreign directors on board meeting frequency. International Review of Financial Analysis, 46, 295–308. https://doi.org/10.1016/j.irfa.2015.11.004

Handriani, E., & Robiyanto, R. (2019). Institutional ownership, independent board, the board size, and firm performance: Evidence from Indonesia. Contaduría y Administración, 64(3). https://doi.org/10.22201/fca.24488410e.2018.1849

Hedges, L. V., & Olkin, I. (2014). Statistical methods for meta-analysis. Academic Press.

Himmelberg, C. P., Hubbard, R. G., & Palia, D. (1999). Understanding the determinants of managerial ownership and the link between ownership and performance. Journal of Financial Economics, 53(3), 353–384. https://doi.org/10.1016/S0304-405X(99)00025-2

Hossain, A. T., & Kryzanowski, L. (2021). Political corruption and corporate social responsibility (CSR). Journal of Behavioral and Experimental Finance, 31, Article e100538. https://doi.org/10.1016/j.jbef.2021.100538

Hussainey, K., & Al‐Najjar, B. (2012). Understanding the determinants of RiskMetrics/ISS Ratings of the quality of UK companies' corporate governance practice. Canadian Journal of Administrative Sciences, 29(4), 366–377. https://doi.org/10.1002/cjas.1227

Jensen, M. C. (1986). Agency costs of free cash flow, corporate finance, and takeovers. The American Economic Review, 76(2), 323–329.

Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305–360.

Joh, S. W. (2003). Corporate governance and firm profitability: Evidence from Korea before the economic crisis. Journal of financial Economics, 68(2), 287–322. https://doi.org/10.1016/S0304-405X(03)00068-0

Khan, K. M., & Mahmood, Z. (2023). Impact of corporate governance on firm performance: a case of Pakistan stock exchange. Liberal Arts and Social Sciences International Journal (LASSIJ), 7(1), 24–38. https://doi.org/10.47264/idea.lassij/7.1.2

Kyere, M., & Ausloos, M. (2020). Corporate governance and firms financial performance in the United Kingdom. International Journal of Finance & Economics, 26(2), 1871–1885. https://doi.org/10.1002/ijfe.1883

Kim, W., Black, B. S., & Jang, H. (2006). Does corporate governance predict firms' market values? Evidence from Korea. The Journal of Law, Economics, and Organization, 22(2), 366-413.

Leech, D., & Leahy, J. (1991). Ownership structure, control type classifications and the performance of large British companies. The Economic Journal, 101(409), 1418–1437. https://doi.org/10.2307/2234893

Lipton, M., & Lorsch, J. W. (1992). A modest proposal for improved corporate governance. The Business Lawyer, 48(1), 59–77.

Liu, H., & Fong, M. W. (2010). Board characteristics of medium and large Chinese companies. Corporate Governance, 10(2), 163–175. https://doi.org/10.1108/14720701011035684

Lopez-Quesada, E., & Idowu, S. O. (2018). Corporate governance practices and comprehensive income. Corporate Governance, 18(3), 462–477. https://doi.org/10.1108/CG-01-2017-0011

Mubeen, R., Han, D., Abbas, J., Álvarez-Otero, S., & Sial, M. S. (2021). The relationship between CEO duality and business firms’ performance: the moderating role of firm size and corporate social responsibility. Frontiers in Psychology, 12, Article e669715. https://doi.org/10.3389/fpsyg.2021.669715

Muth, M., & Donaldson, L. (1998). Stewardship theory and board structure: A contingency approach. Corporate Governance, 6(1), 5–28. https://doi.org/10.1111/1467-8683.00076

Mutlu, C. C., Van Essen, M., Peng, M. W., Saleh, S. F., & Duran, P. (2018). Corporate governance in China: A meta‐analysis. Journal of Management Studies, 55(6), 943–979. https://doi.org/10.1111/joms.12331

Nenova, T. (2003). The value of corporate voting rights and control: A cross-country analysis. Journal of Financial Economics, 68(3), 325–351. https://doi.org/10.1016/S0304-405X(03)00069-2

Panasian, C. (2003). The impact of the 1995 TSE Corporate Governance Guidelines on the performance of Canadian companies: A simultaneous equation approach. Concordia University.

Pervan, M., Pervan, I., & Ćurak, M. (2017). The influence of age on firm performance: Evidence from the Croatian food industry. Journal of Eastern Europe Research in Business and Economics, 2017(1), 1-10. https://dx.doi.org/10.5171/2017.618681

Pearce, J. A., & Zahra, S. A. (1992). Board composition from a strategic contingency perspective. Journal of Management Studies, 29(4), 411–438. https://doi.org/10.1111/j.1467-6486.1992.tb00672.x

Pillai, R., & Al-Malkawi, H.-A. N. (2018). On the relationship between corporate governance and firm performance: Evidence from GCC countries. Research in International Business and Finance, 44, 394–410. https://doi.org/10.1016/j.ribaf.2017.07.110

Pinto, I., Gaio, C., & Gonçalves, T. (2019). Corporate governance, foreign direct investment, and bank income smoothing in African countries. International Journal of Emerging Markets, 15(4), 670–690. https://doi.org/10.1108/IJOEM-04-2019-0297

Prashar, A., & Gupta, P. (2021). Corporate boards and firm performance: a meta-analytic approach to examine the impact of contextual factors. International Journal of Emerging Markets, 16(7), 1454–1478. https://doi.org/10.1108/IJOEM-10-2019-0860

Ruigrok, W., Peck, S. I., & Keller, H. (2006). Board characteristics and involvement in strategic decision making: Evidence from Swiss companies. Journal of management Studies, 43(5), 1201–1226. https://doi.org/10.1111/j.1467-6486.2006.00634.x

Rosenthal, R. (1979). The file drawer problem and tolerance for null results. Psychological bulletin, 86(3), 638.

Saibaba, M., & Ansari, V. A. (2012). Impact of board size: An empirical study of companies listed in BSE 100 index. Indian Journal of Corporate Governance, 5(2), 108–119. https://doi.org/10.1177/0974686220120202

Scherrer, P. S. (2003). Directors’ responsibilities and participation in the strategic decision making process. Corporate Governance, 3(1), 86–90. https://doi.org/10.1108/14720700310459890

Serrasqueiro, Z. S., & Nunes, P. M. (2008). Performance and size: Empirical evidence from Portuguese SMEs. Small Business Economics, 31(2), 195–217. https://doi.org/10.1007/s11187-007-9092-8

Shleifer, A., & Vishny, R. W. (1997). A survey of corporate governance. The Journal of Finance, 52(2), 737–783. https://doi.org/10.1111/j.1540-6261.1997.tb04820.x

Strom, R. Ø., D’Espallier, B., & Mersland, R. (2014). Female leadership, performance, and governance in microfinance institutions. Journal of Banking & Finance, 42, 60–75. https://doi.org/10.1016/j.jbankfin.2014.01.014

Topak, M. S. (2011). The effect of board size on firm performance: Evidence from Turkey. Middle Eastern Finance and Economics, 14(1), 1450–2889.

Tripsas, M., & Gavetti, G. (2000). Capabilities, cognition, and inertia: Evidence from digital imaging. Strategic Management Journal, 21(10‐11), 1147–1161. https://doi.org/10.1002/9781405164054.ch23

Usman, M., Ali, M., Ogbonnaya, C., & Babalola, M. T. (2021). Fueling the intrapreneurial spirit: A closer look at how spiritual leadership motivates employee intrapreneurial behaviors. Tourism Management, 83, Article e104227. https://doi.org/10.1016/j.tourman.2020.104227

Van Essen, M., van Oosterhout, J. H., & Carney, M. (2012). Corporate boards and the performance of Asian firms: A meta-analysis. Asia Pacific Journal of Management, 29, 873-905.

Wang, C., Wang, D., Abbas, J., Duan, K., & Mubeen, R. (2021). Global financial crisis, smart lockdown strategies, and the COVID-19 spillover impacts: A global perspective implications from Southeast Asia. Frontiers in Psychiatry, 12, Article e643783. https://doi.org/10.3389/fpsyt.2021.643783

Yermack, D. (1996). Higher market valuation of companies with a small board of directors. Journal of Financial Economics, 40(2), 185–211. https://doi.org/10.1016/0304-405X(95)00844-5

Yu, M. (2023). CEO duality and firm performance: A systematic review and research agenda. European Management Review, 20(2), 346–358. https://doi.org/10.1111/emre.12522

Yu, S., Abbas, J., Draghici, A., Negulescu, O. H., & Ain, N. U. (2022). Social media application as a new paradigm for business communication: the role of COVID-19 knowledge, social distancing, and preventive attitudes. Frontiers in Psychology, 13, Article e903082. https://doi.org/10.3389/fpsyg.2022.903082

Zona, F., Zattoni, A., & Minichilli, A. (2013). A contingency model of boards of directors and firm innovation: The moderating role of firm size. British Journal of Management, 24(3), 299–315. https://doi.org/10.1111/j.1467-8551.2011.00805.x