Attiya Ammar*

National Institute of Management, Lahore, Pakistan

*Corresponding Author: [email protected]

The developmental process in Pakistan has been hindered due to the large informal economy and insufficient tax compliance. Successive governments have failed to change the mindset due to flawed policies, administrative constraints, and rambling corruption. The gap in tax revenue is due to tax evasion and avoidance practices. The economy is constrained by individuals who fiddle with policies that affect both the society and the state. The core issues have been delineated along with the potential results. Qualitative research method has been employed to analyze the performance, challenges, and prospects of broadening the tax base. The findings of the study portray that although the implementation of tax policy aimed to broaden the tax base has improved considerably, however, simplifying tax codes and making them clearer can improve compliance, reduce errors, and make the system fairer. This can be achieved by minimizing exemptions, deductions, and loopholes. This policy could prove beneficial for stakeholders, particularly the policymakers, to formulate the future tax policy and strategies in order to obtain maximum tax revenue.

Keywords: Informal economy, policy making, tax base, tax revenue

Tax revenue functions as a catalyst for a country's economic growth. Comparing Pakistan to other developing and regional economies, the country's tax-to-GDP ratio remains relatively low. Experts estimate that Pakistan's population and economy require a sustainable growth rate of at least 8% to support around 2.5 million jobs every year, based on research by the International Monetary Fund (Cevik, 2016).

Pakistan's federal tax system encompasses various taxes, such as income tax, sales tax, customs duties, and other levies. A substantial portion of economic activities in Pakistan remains informal, resulting in many individuals and businesses operating outside the tax net. Tax evasion and avoidance are prevalent issues, with some taxpayers deliberately underreporting income, engaging in fraudulent practices, or exploiting loopholes in the tax system to reduce their tax liabilities. Weak compliance and low documentation of the economy provide a safe passage to millions of potential taxpayers to stay out of the tax net. Owing to the low tax-to-GDP ratio, Pakistan heavily relies on aid from foreign resources like the World Bank (WB), International Monetary Fund (IMF), and International Donor Agencies (IDA) to meet its financial needs. Improvements are necessary in Pakistan's tax policy to address the evolving demands of the contemporary world and to promote public services and growth. Pakistan's tax system is complicated, has a limited scope, and has inefficient administrative procedures. The government's continued dependence on borrowing from external and domestic sources reflects a lack of public trust and unscrupulous activities. To boost economic activity, the government has introduced amnesty programs for asset declaration, tax breaks for the building sector, and whistleblower awards programs (Amjad, 2021).

Pakistan ranked 161st among 190 economies for "paying tax" indicator in the 2020 Doing Business Report. The low performance for this indicator is attributable to the complex tax structure and high tax compliance costs (Khalid, 2020).

Expanding the tax base in Pakistan is a critical challenge that requires immediate attention and effective policy-driven solutions. The population of Pakistan is approximately 238.1 million, out of which 2,472,609 individuals filed their tax returns in 2020, which shows that there is an urgent need to bring more people into the tax net. In a recent tax gap study conducted by FBR, the careful annual potential tax gap in Pakistan amounts to approximately Rs1,289 billion, leading to significant revenue shortfalls. These shortfalls hinder the government's ability to fund essential public services, promote economic development, and address socio-economic disparities. The primary reason for the FBR's failure to expand the tax base in the country lies in the weak political will of the Government and its non-responsive policies. This policy paper shall examine a proposed scheme for the Broadening of the Tax Base (BTB).

The challenges of tax collection are not new, as historical examples like the Romans hiding gold to evade luxury taxes or homeowners hiding fireplaces to avoid hearth taxes illustrate (Oates & Schwab, 2015). Tax collection remains a challenging task in any society, as there will always be individuals in society who attempt to evade taxes. Pakistan's economic conditions have long been challenging, and tax funding is crucial for running huge government machinery and providing public services.

The broadening of the tax base in Pakistan poses a significant challenge that hampers the country's economic development and fiscal stability. Despite having a population of 238.1 million, only a fraction of individuals and businesses are part of the formal tax system i.e. less than 1% of the population of the country submits their annual tax returns. The low tax compliance, characterized by widespread tax evasion and avoidance, leads to substantial revenue shortfalls, hindering the government's ability to fund essential public services and address socio-economic disparities. The government's non-responsive policies and practices further impede efforts to expand the tax base. Pakistan's complex tax system and lack of trust in government services contribute to the persistently narrow tax base. Resolving these issues is crucial to ensuring sustainable revenue generation and promoting economic growth in Pakistan.

The policy paper on broadening the tax base in Pakistan aims to analyze the challenges and factors hindering the expansion of the country's tax net in the last ten years. It also examines the effectiveness of the current strategies and campaigns in bringing a wider range of potential taxpayers into the tax net. The study explores the reasons for the non-documentation of the economy and the failure to develop a fair, effective, and efficient policy to ensure that every potential taxpayer pays their fair share of taxes. The research provides insights to identify the limitations of tax agencies in widening the tax base and provides proposals for policymakers and stakeholders to develop effective policies for BTB. Pakistan's taxation system is suffering from a narrow tax base. The table based on FBR data from 2013-2016, shows that a reliable number 0.61% of the population files tax returns and only 2.13 % of the population is registered with FBR.

Table 1

Data about Return Fillers for Five Years TY 2012 to TY 2016:

|

Sr. |

Taxpayer's category |

Tax year |

||||

|

2012 |

2013 |

2014 |

2015 |

2016 |

||

|

1 |

Companies |

25,912 |

26,945 |

29,414 |

30,936 |

31,359 |

|

2 |

AOPs |

41,012 |

44,790 |

47,154 |

47,674 |

48,652 |

|

3 |

Business Individual |

561,658 |

588,787 |

702,820 |

752,339 |

735,415 |

|

4 |

Salaried Individual |

185,823 |

250,660 |

330,712 |

409,209 |

405,060 |

|

Total |

|

814,405 |

3,660,509 |

3,802,002 |

3,977,949 |

1,220,486 |

The BTB involves various interconnected sets of actions, including the registration of eligible individuals with the tax department, filing of income returns, and payment of due taxes within a given time. A successful expansion of the tax base can have a significant impact on the overall GDP ratio of the nation, assuming other variables remain constant.

In the early 2000s, FBR undertook several initiatives to expand tax net in the country. The campaign was initiated through a laborious nationwide door-to-door survey conducted by joint teams of FBR and military personnel, to gather extensive data on potential taxpayers. However, despite the accumulation of a substantial amount of actionable data, the impact of this endeavor was minimal due to the inability of tax agencies to utilize the data effectively. Over time, political will was diminished and the collected data became redundant. A serious campaign was lost as the goals of documentation and expansion were not achieved. Again after 2009, on frequent and multiple demands of donor agencies, i.e. IMF and World Bank, BTB campaigns were started and legal frameworks were developed to bring potential taxpayers into the tax net. These efforts helped to implement a strong withholding taxation regime in Pakistan to document the economy and gave birth to famous notion of filer and non-filer.

This withholding taxation regime was aimed to document the economy and most withholding taxes are adjustable which often results in the issuance of refunds but this has helped FBR bring many potential taxpayers into the tax net. This also helped tax agencies in creating economic profiles for taxation purposes. Data on economic activities, such as real estate purchases, vehicle acquisitions, air travel, service usage, school fees, and other expenses were recorded in a central database and categorized using the common denominator of the Computerized National Identity Card (CNIC). This laid strong foundations for data keeping, particularly of financial transactions.

This study analyses the experiences of Asian nations from a comparative standpoint and addresses the issues of what kind of taxes and tax base expansion are preferable from the standpoint of economic theory. A nation that has more government spending relative to its gross national product is more likely to have a budget deficit. Import and export taxes, among other trade levies, are detrimental to development because they generate market distortion and encourage strategies focused on import substitution. Although desired, land and property taxes are rarely enacted due to political challenges. Despite the desirability of a personal income tax, its ability to generate money is constrained (Hamada, 1994).

Tax reform is not a novel topic on developing nations' economic agendas. Since 1945, more than a hundred initiatives have been made in emerging nations to alter their tax systems, as noted by Gillis. Nonetheless, a lot of these nations may have seen a shift in their reasons for tax reform over the past 25 years. Policy reform has moved from being something that was wanted or chosen to something that is now required. Tax reform became necessary for some nations to close their budget deficits, but it also became critical for others to preserve—and in some cases, improve—their competitiveness internationally (Diokno, 1993).

In order to establish a framework for deciding how much the environment needs to be safeguarded, an operational definition of sustainability is provided. After examining the causes of environmental issues, the study explores potential policy solutions. Alternative policy tools, including tradeable permits, taxes, and subsidies, are studied. These tools can be used for both incentive-based and command and control policies. There is a discussion of the advantages, expenses, efficacy, distributive implications, implementability, and suitability of alternative policy tools for various kinds of issues (Parikh, 1994).

Prichard et al. (2019) in their paper present a conceptual framework that identifies three dimensions of innovation in tax compliance: policy, administration, and technology. Policy innovation involves developing new tax policies, such as introducing incentives or simplifying tax codes, to encourage compliance.

The amount of taxes is essential to the government's survival. The purpose of this paper is to identify the factors that contribute to tax evasion and avoidance in Pakistan. The correlation between the factors that contribute to tax evasion and avoidance is also examined. After examining the literature, a questionnaire is created to gather responses. Percentages, arithmetic means, variance, standard deviation, central limit theorem, cumulative normal distribution calculator, factor analysis, and correlation techniques are used to analyse data. The findings show that every variable related to the causes and reasons of tax evasion and avoidance in Pakistan is accurate. Additionally, at the 100% significance level, there is a highly significant positive correlation between the individual variables of the causes and reasons for tax evasion and avoidance in Pakistan (Mughal, 2012).

With the increasing global debt levels due to the COVID-19 pandemic and the Global Financial Crisis (GFC) of 2007-2008, expanding the tax base has been suggested by the World Bank as a means to address rising debt. The study reviewed identifies the tipping point where sovereign debt becomes problematic, and it suggests that gradual fiscal consolidation and tax base expansion can lead to a decline in the debt-to-GDP ratio and a rise in output, ultimately achieving stable economic conditions over time (Ghufran et al., 2022).

The informal economy of Pakistan constitutes an estimated 35% of the GDP and plays a significant role in the country's economic landscape. It encompasses a wide range of economic activities that are not regulated or officially recognized by the government, including street vending, small-scale manufacturing, household enterprises, and unregistered businesses. The informal economy poses several challenges as it operates outside the tax net, leading to revenue losses for the government. This limits the government's ability to provide essential services and invest in infrastructure and social development.

Efforts have been made to formalize the informal sector and bring it into the mainstream economy. However, addressing the complexities and the needs of the informal economy requires comprehensive policies and targeted interventions across all federal and provincial departments to ensure documentation of the economy and sustainable economic & revenue growth.

This study is conducted using qualitative methods to analyze the performance, challenges, and prospects of BTB. Primary Data was collected from FBR and secondary data was collected from articles, research papers, books, and policy documents of the FBR. Also, the NIM library was consulted for available literature and all the sources available on the e-print, Jstore, emerald, and newspapers were explored. A comprehensive phone interview was conducted with Mr. Zubair Bilal, Director General BTB, heading the Directorate General of Broadening of Tax Base, FBR HQ. This research also sought insights from Dr. Hamid Attique Sarwar, ex-member policy, regarding the current situation of the tax net in Pakistan.

Tax Gap is a buzzword these days and widely used across developing economies. In the U.S. the "official' IRS definition of the tax gap is simply: "The difference between the tax that taxpayers should pay and what they pay on a timely basis" (Gemmell & Hasseldine, 2012). FBR's Tax to GDP Ratio is 9% for the year 2021-22. Its tax-to-GDP ratio excluding agricultural income is 11.8% whereas, its provincial tax to GDP Ratio is 0.9%. Tax gaps also include taxes to be paid by the undocumented economy, tax evasion, and tax expenditures. BTB deals with the undocumented economy and tax evasion.

The tax is usually collected from a few already registered persons; while many potential taxpayers with huge financial transactions dodge tax authorities and evade the tax by not filing tax returns (The World Bank, 2019).

Broadening the tax base is possibly the most critical economic challenge facing Pakistan. The lower side estimated of annual income tax gap is 730 billion rupees or 31% of the total income tax that could be collected (Federal Board of Revenue Pakistan, 2022). For reliability, a similar tax gap was examined for salaried people using the Labour Force Survey (LFS). Addressing this huge tax gap in Pakistan requires sincere efforts by the government involving improvements in the tax policy, making effective enforcement, and eradicating the trust deficit between taxpayers and tax agency.

Avoiding tax through legal means by taking advantage of legal loopholes, asking lawyers and accountants to calculate less amount of tax is "Tax Avoidance". A tax avoidance scheme is used to circumvent paying higher tax. However, in Pakistan, a large number of wealthy citizens avoid paying their taxes by scheming with tax officials to minimize their incomes or by taking advantage of legal loopholes. These are ways to reduce the taxes by introducing investments like tax-exempt municipal bonds that may be difficult to confront (Dyreng et al., 2019).

Tax evasion is a deliberate act of a person not registering with the tax department or paying less tax with the intention of reducing their due tax liability. Tax avoidance is also not legal in Pakistan and is termed as tax evasion, attracting prosecution.

There are numerous challenges of governance and social behaviors in Pakistan that keep defeating the drive and spirit of BTB. According to a study conducted by Rana (2021), there are approximately 4.7 million citizens in Pakistan who possess valid National Tax Numbers (NTNs) but avoid filing tax returns, despite the legal obligation under Section 114(1) b (vii) for NTN holders to file tax returns. Additionally, out of the total 7.2 million companies, only 2.7 million have filed income tax returns. Encouraging compliance among these individuals and companies poses a significant challenge for the FBR under Universal Self-Assessment Scheme (USAS). The widespread mistrust of public in government as a result of decades of corruption leads many to avoid paying the tax. Corruption in tax department enables taxpayers to pay fewer taxes and also helps potential tax payers to stay out of tax net. Moreover, according to the research survey conducted regarding BTB "individuals primarily choose non-compliance due to the complexity of tax laws and the high costs associated with compliance. The FBR's return-filing software, IRIS, is recognized for being extremely complicated and user-unfriendly, further supported by the survey findings."

BTB in Pakistan faces several challenges, and high level of informality in the economy is one of them. Poor tax compliance is also influenced by the complex tax system and lack of trust in the government's ability to provide essential services. Additionally, tax officials, usually in collusion with the potential taxpayers through informal consultancies, help them either stay out of the tax net or assist them pay much less tax than due taxes. This policy paper will look into the policy options of the tax machinery, identify potential bottlenecks for the implementation of different measures, and present recommendations as the outcome of the research.

FBR has taken a number of initiatives and persuaded many campaigns to expand the tax base in the country, but these efforts have faced significant challenges. There is a huge consensus amongst all stakeholders of the state, economy, and tax system that broadening the tax base is the single most important area to optimize tax revenues in the country. Unfortunately, besides undisputed agreement, non-willingness of the business communities, lack of political will by successive governments and non-cooperation of federal and provincial governments have frustrated all efforts to increase the tax net. FBR had established a full fledge directorate of Broadening of Tax base in 2009-2010 to devise policies and action plans to increase return filling, but due to policy shift, it was dissolved and BTB functions were given to field offices without any direct and active monitoring of FBR. Since then, often and on BTB remained in talks and agendas with varied focus until recent years. Now a full fledge Directorate General has been established at FBR and it has developed a live monitoring mechanism with field formations. A number of different action plans are under implementation to increase taxpayers' numbers.

The tax agency has failed to get credible information on huge investment transactions about potential taxpayers, beside that every department responsible for the documentation of valuable transactions has been digitalized. These data sets are isolated and have been fetched as per requirements of the FBR.

There have been many efforts made by FBR to align all such data centers with FBR's requirements for documentations, but many practical issues are still unresolved. For example, transactions of immoveable properties are being recorded and maintained by local governments at every district level; similarly, registration of motor vehicles is managed and recorded at every district level by the Excise and Taxation Office, both are provincial departments. Every Government department wants to keep its data isolated and monopolized, that's why sharing of data has been a huge issue. It is also found that many a time, shared data is not actionable due to the absence of real-time details.

Researchers contacted the responsible office of BTB and sought their version and input, according to the DG BTB "Due to the lack of administrative ownership by the chief commissioners of RTOs where BTB commissioners and their teams were stationed, the operational design of the BTB wing was also problematic. According to the system, BTB commissioners were responsible for reporting to the DG BTB at FBR but were reliant on the chief commissioners of RTO for funding. Other difficulties included conflicting jurisdictions, a lack of RTO-level ownership, double reporting structures, and a lack of administrative monitoring. The databases of other organizations, particularly those in the public sector, were not linked to those of FBR. As a result, it became very challenging to create an economic picture of a potential taxpayer. Later on, the BTB zones were eliminated.

"The tenth schedule to the Income Tax Ordinance of 2001 has encouraged those who are not registered to do so in order to benefit from lower withholding tax rates. The key is to go after the big fish; amid all these considerations, the true difficulty would be to include those taxpayers on the tax registers who considerably improve revenue collection" (Malik, 2022).

Efforts are underway to expand the tax net through campaigns utilizing different types of third-party data including data from commercial and industrial consumers of power distribution companies, gas companies, immovable property registrations, and motor vehicle registration authorities. There are many practical issues in reaching out to potential taxpayers like lack of updated data of NADRA, incomplete addresses of land owners, and CNICs of the consumers using utilities i.e. gas and electricity. Health and actionability of data remained a major source of failures of previous BTB campaigns. The research proposes a two-pronged policy for the Broadening of the Tax Base having the following main features of effective policy to improve the tax base.

Income Tax Ordinance, 2001 provides a complete solution to improve the tax base, but as per the outcome of the research, this paper proposes the following legal interventions for effective BTB drive.

The Following administrative measures are also proposed for broadening of tax base

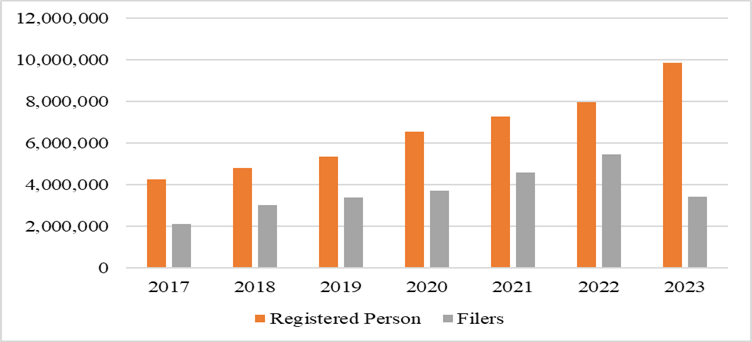

The following data has been sought from the Federal Board of Revenue During recent years, the implementation of tax policy aimed to broaden the tax base has improved considerably. Simplifying tax codes and making them clearer can improve compliance, reduce errors, and make the system fairer. This can be achieved by minimizing exemptions, deductions, and loopholes. The following table shows the difference in the number of registered persons and filers spanning the years 2017-2023. It is visible that the number of filers has increased due to policy interventions.

Table 2

Registered Persons and Filers Spanning the Years 2017-2023

|

Income Tax |

Percentage growth (Tax Reg VS Return fillers) |

||

|

Tax Year |

Registered Person |

Filers |

|

|

2017 |

4,257,280 |

2,100,219 |

49.33 % |

|

2018 |

4,800,746 |

3,017,402 |

62.85% |

|

2019 |

5,349,921 |

3,391,837 |

63.33% |

|

2020 |

6,552,399 |

3,698,130 |

56.43% |

|

2021 |

7,287,829 |

4,596,008 |

63.06% |

|

2022 |

7,969,009 |

5,438,972 |

68.25% |

|

2023 |

9,865,326 |

3,415,416 |

34.62% |

Note. *Returns are being filled for TY 2023; numbers of returns are expected to increase.

Figure 1

No. of Filers compared to Registered persons

As evident from the discussion above, FBR deals with problems on many different levels, including poor strategy, a lack of resources, and a workforce that is both undertrained and unmotivated, among other issues. The withholding tax system is very important to Pakistan's tax base as this paves the way for the documentation of numerous financial transactions of potential taxpayers. Section 114 of IT Ordinance 2001 outlines a comprehensive list of individuals obligated to file their annual income tax returns, which serves as the legal framework in place today. However, the vast majority of those required to file returns largely disregard this national obligation. The documentation of the economy is a collective exercise involving all government departments and provides foundations for broadening the tax base. Two prolonged policy measures proposed by this research aim to enable tax agencies to improve compliance and strengthen legal and administrative frameworks.

This research has proposed actionable policy measures to enable FBR to expand its tax net. To broaden the tax base effectively, it is important to have a real-time centralized database of all transactions regarding immovable properties, utility customers, and motor vehicles. Introducing a simple and user-friendly online system for the public to file income tax returns is crucial. Moreover, there is a need to shift from manual to real-time digitized invoices and capturing of sale/purchase transactional data on a real-time basis. The need to integrate businesses and banks' software with FBR's computer system is essential. A lot of initiatives have been taken to broaden the tax base by using technology such as Taxray, the FBR database, and collaboration with NADRA. It is anticipated that tax agency, after considering policy proposals of this research, would be able to double the number of their taxpayers within the next five years, reaching the milestone of 15% tax to GDP ratio.

Amjad, M. (2021). Tax policy in Pakistan: Concerns and reforms. SSRN, Article e3791148. http://dx.doi.org/10.2139/ssrn.3791148

Cevik, S. (2016). Unlocking Pakistan's revenue potential. International Monetary Fund. https://www.imf.org/external/pubs/ft/wp/2016/wp16182.pdf

Diokno, B. E. (1993). Structural adjustment policies and the role of tax reform. Asian Development Review, 11(2), 140–153. https://doi.org/10.1142/S0116110593000119

Dyreng, S. D., Hanlon, M., & Maydew, E. L. (2019). When does tax avoidance result in tax uncertainty? The Accounting Review, 94(2), 179–203. https://doi.org/10.2308/accr-52198

Federal Board of Revenue Pakistan. (2022). Tax gap report 2022. https://download1.fbr.gov.pk/Docs/2023118141362748Tax-Gap-Report-2022-Final.pdf

Gemmell, N., & Hasseldine, J. (2012). The tax gap: a methodological review (Vol. 20). Emerald Group Publishing Limited.

Ghufran, M., Ashraf, J., Rizwan, M., Ali, S., & Aldieri, L. (2022). Tax base-broadening a light at the end of the tunnel in the fiscal consolidation dynamics. Modern Economy, 13(3), 397–424. https://doi.org/10.4236/me.2022.133022

Hamada, K. (1994). Broadening the tax base: The economics behind it. Asian Development Review, 12(2), 51–84. https://doi.org/10.1142/S0116110594000096

Khalid, M. (2020). Tax structure in Pakistan: Fragmented, exploitative and anti-growth. The Pakistan Development Review, 59(3), 461–468.

Malik, M. B. (2022). Appraisal of comprehensive scheme of increasing tax base proposed by FPCCI. Journal of Public Policy Practitioners, 1(2), 1–32. https://doi.org/10.32350/jppp.12.01

Mughal, M. (2012). Reasons of tax avoidance and tax evasion: Reflections from Pakistan. Journal of Economics and Behavioral Studies, 4(4), 217–222. https://doi.org/10.22610/jebs.v4i4.320

Oates, W. E., & Schwab, R. M. (2015). The window tax: A case study in excess burden. Journal of Economic Perspectives, 29(1), 163–180. https://doi.org/10.1257/jep.29.1.163

Parikh, K. (1994). Sustainable development and the role of tax policy. Asian Development Review, 13(1), 127–166. https://doi.org/10.1142/S0116110595000054

Prichard, W., Custers, A. L., Dom, R., Davenport, S. R., & Roscitt, M. A. (2019). Innovations in tax compliance: Conceptual framework. The World Bank. https://doi.org/10.1596/1813-9450-9032

Rana, S. (2021). Only 2.5m people file tax returns. The Tribune. https://tribune.com.pk/story/2324997/only-25m-people-file-tax-returns

The World Bank. (2019). Project information document. https://documents1.worldbank.org/curated/en/637701556009042302/pdf/Project-Information-Document-Pakistan-Revenue-Mobilization-Project-P165982.pdf