Influence of International Standards of Internal Auditing on the Proficiency of Internal Audit Mechanism in Public Sector Universities of Pakistan

DOI:

https://doi.org/10.32350/aar.42.02Keywords:

Attribute standards, Higher Education Institutes (HEIs), internal auditing, performance standards, public sectorAbstract

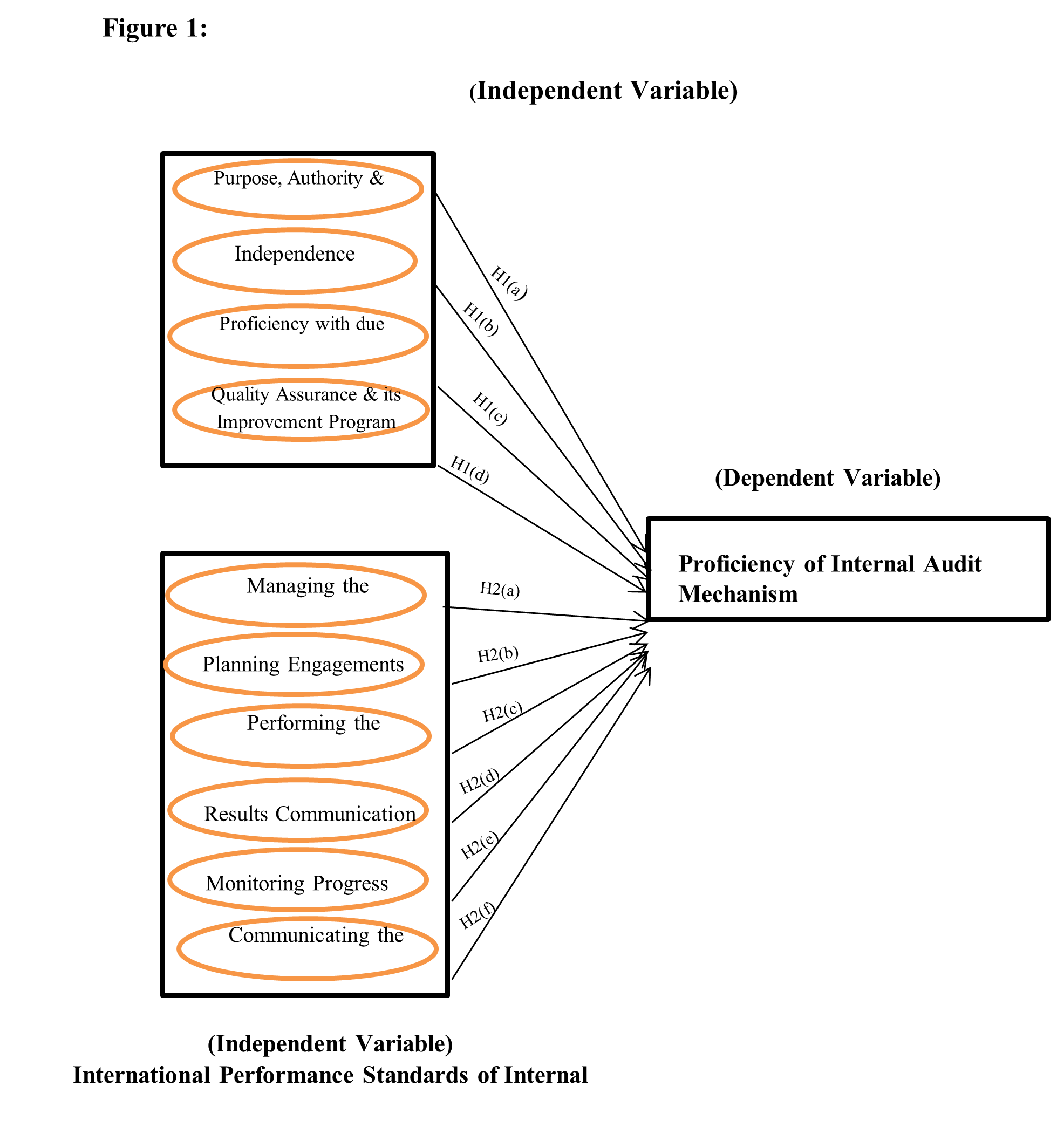

The current study aims to explore how the International Standards of Internal Auditing (ISIA) impact the proficiency of Internal Audit (IA) mechanism in the public sector of Pakistan. The study targets the public sector Higher Education Institutes (HEIs) of Pakistan which are the recipients of hefty financial resources from government. A questionnaire was distributed to 250 employees working in Internal Audit and Finance Department besides the members of statutory bodies of public sector HEIs of all five provinces (stratum) across Pakistan by using the purposive sampling. One hundred and fifty (150) valid responses were received back. The Institute of Internal Auditors (IIA) has framed two broader categories of ISIA, for instance (i) Attribute Standards (IAS) (ii) Performance Standards (IPS.) By deploying SPSS version 22.0, the results of regression analysis amongst ISIA and IA mechanism reveals that in the category of attribute standards of internal auditing, 3 out of 4 standards have a significant positive impact on the proficiency of (IA) mechanism in public sector HEIs of Pakistan. While, in the category of performance standards of internal auditing; only 3 out of 6 standards have a significant positive impact on the proficiency of (IA) mechanism. The findings would be useful in strengthening the Internal Audit Functions (IAFs) in public sector of Pakistan. Policymakers are recommended to implement the international standards of internal auditing which may lead towards enhanced proficiency of IA mechanism in public sector.

Downloads

References

Abdullah, R., Ismail, Z., & Smith, M. (2018). Audit committees' involvement and the effects of quality in the internal audit function on corporate governance. International Journal of Auditing, 22(3), 385–403. https://doi.org/10.1111/ijau.12124

Ali, S. I., & Ali, A. (2022). Internal auditing practices and internal control quality in state-owned enterprises: Evidence from Pakistan. Sarhad Journal of Management Sciences, 8(2), 139–162.

Alin, A. (2010). Multicollinearity. Wiley Interdisciplinary Reviews: Computational Statistics, 2(3), 370–374. https://doi.org/10.1002/wics.84

Alazzabi, W. Y. E., Mustafa, H., & Karage, A. I. (2023). Risk management, top management support, internal audit activities and fraud mitigation. Journal of Financial Crime, 30(2), 569–582. https://doi.org/10.1108/JFC-11-2019-0147

Alqudah, H. M., Amran, N. A., & Hassan, H. (2019). Factors affecting the internal auditors’ effectiveness in the Jordanian public sector: The moderating effect of task complexity. EuroMed Journal of Business, 14(3), 251–273. https://doi.org/10.1108/EMJB-03-2019-0049

Alzeban, A., & Sawan, N. (2015). The impact of audit committee characteristics on the implementation of internal audit recommendations. Journal of International Accounting, Auditing and Taxation, 24, 61–71. https://doi.org/10.1016/j.intaccaudtax.2015.02.005

Anojan, V. (2022). Factors affecting internal audit reporting on public sector in Sri Lanka, Journal of Accounting and Business Education, 6 (2), 22–33. http://dx.doi.org/10.26675/jabe.v6i2.21265

Alwan, A. H., & Bougatef, K. (2024). The quality of tax accounting in accordance with international internal auditing standards: The case of Iraq. Tec Empresarial, 19(1), 29–48.

Aryan, L. A. (2015). The relationship between audit committee characteristics, audit 153 firm quality and companies’ profitability. Asian Journal of Finance & Accounting, 7(2), 215–226. http://dx.doi.org/10.5296/ajfa.v7i2.8530

Asare, T. (2009). Internal auditing in the public sector: Promoting good governance and performance improvement. International Journal on Governmental Financial Management, 9(1), 15–28.

Asaolu, T. O., Adedokun, S. A., & Monday, J. U. (2016). Promoting good governance through internal audit function (IAF): The Nigerian experience. International Business Research, 9(5), 196–204. http://dx.doi.org/10.5539/ibr.v9n5p196

Bailey, C., Collins, D. L., & Abbott, L. J. (2018). The impact of enterprise risk management on the audit process: Evidence from audit fees and audit delay. Auditing: A Journal of Practice & Theory, 37(3), 25–46. http://dx.doi.org/10.2308/ajpt-51900

Bednarek, P. (2018). Factors affecting the internal audit effectiveness: A survey of the Polish private and public sectors. In Efficiency in Business and Economics: Proceedings from the 7th International Conference on Efficiency as a Source of the Wealth of Nations (ESWN), Wrocław 2017 (pp. 1-16). Springer International Publishing.

Calvin, C. G. (2021). Adherence to the internal audit core principles and threats to internal audit function effectiveness. Auditing: A Journal of Practice & Theory, 40(4), 79–98. https://doi.org/10.2308/AJPT-19-072

Christopher, J. (2015). The adoption of internal audit as a governance control mechanism in Australian public universities: Views from the CEOs. Journal of Higher Education Policy and Management, 34(5), 529–541. https://doi.org/10.1080/1360080X.2012.716001

Chan, K. C., Chen, Y., & Liu, B. (2021). The linear and non-linear effects of internal control and its five components on corporate innovation: Evidence from Chinese firms using the COSO framework. European Accounting Review, 30(4), 733–765. https://doi.org/10.1080/09638180.2020.1776626

Chang, Y. T., Chen, H., Cheng, R. K., & Chi, W. (2019). The impact of internal audit attributes on the effectiveness of internal control over operations and compliance. Journal of Contemporary Accounting & Economics, 15(1), 1–19. https://doi.org/10.1016/j.jcae.2018.11.002

Coetzee, P., & Lubbe, D. (2013). The use of risk management principles in planning an internal audit engagement. Southern African Business Review, 17(2), 113–139.

Cular, M., Slapničar, S., & Vuko, T. (2020). The effect of internal auditors’ engagement in risk management consulting on external auditors’ reliance decision. European Accounting Review, 29(5), 999–1020. https://doi.org/10.1080/09638180.2020.1723667

Chambers, D. A. (2014). New guidance on internal audit: An analysis and appraisal of recent developments. Managerial Auditing Journal, 29(2), 196–218. https://doi.org/10.1108/MAJ-08-2013-0925

Dascalu, E. D., Marcu, N., & Hurjui, I. (2016). Performance management and monitoring of internal audit for the public sector in Romania. Amfiteatru Economic Journal, 18(43), 691–705.

DeSimone, S., & Rich, K. (2020). Determinants and consequences of internal audit functions within colleges and universities. Managerial Auditing Journal, 35(8), 1143–1166. https://doi.org/10.1108/MAJ-10-2019-2444

Eltweri, A. M. E. H. (2015). An investigation into the auditing profession regulatory framework and the factors influencing the adoption of ISAs in the Libyan context. Liverpool John Moores University.

Farkas, M., Hirsch, R., & Kokina, J. (2019). Internal auditor communications: An experimental investigation of managerial perceptions. Managerial Auditing Journal, 34(4), 462–485. https://doi.org/10.1108/MAJ-06-2018-1910

Flatt, C., & Jacobs, R. L. (2019). Principle assumptions of regression analysis: Testing, techniques, and statistical reporting of imperfect data sets. Advances in Developing Human Resources, 21(4), 484–502. https://doi.org/10.1177/1523422319869915

Mattei, G., Grossi, G., & Guthrie AM, J. (2021). Exploring past, present and future trends in public sector auditing research: A literature review. Meditari Accountancy Research, 29(7), 94–134.

Mihret, D. G, & Yismaw, A. W. (2007). Internal audit effectiveness: An Ethiopian public sector case study. Managerial Auditing Journal, 22(5), 470–484. https://doi.org/10.1108/02686900710750757

Hassen, E. K., & Altman, M. (January, 2010). Public service employment and job creation in South Africa. Centre for Employment, Poverty and Growth, HSRC. https://miriamaltman.com/wp-content/uploads/2016/09/GOV_EMP031_HassenAltman_public_service_employment_scenarios_jan10.pdf

He, X., Pittman, J. A., Rui, O. M., & Wu, D. (2017). Do social ties between external auditors and audit committee members affect audit quality? The Accounting Review, 92(5), 61–87. https://doi.org/10.2308/accr-51696

Hegazy, M., & Farghaly, M. (2021). External and internal auditors’ perceptions on compliance with internal audit standards and practices: Spirit versus letters. Corporate Ownership & Control, 18(3), 31–45. https://doi.org/10.22495/cocv18i3art3

Horvat, T., & Zvorc, B. (2017, May). The impact of internal auditing on financial planning in public educational institutions. In Management of International Conference. University of Primorska Press.

Institute of Internal Auditors. (2017), International standards for the professional practice of internal auditing (standards). https://na.theiia.org/ standards -guidance/Public%20Documents/IPPF -Standards-2017.pdf

Invernizzi, M., & Parrinello, M. (2022). Exploration vs convergence speed in adaptive-bias enhanced sampling. Journal of Chemical Theory and Computation, 18(6), 3988–3996. https://doi.org/10.1021/acs.jctc.2c00152

Izedonmi, F. I. O., & Olateru-Olagbegi, A. (2021). Internal audit quality and public sector management in Nigeria. European Journal of Social Sciences Studies, 6(5), 10–33. https://doi.org/10.46827/ejsss.v6i5.1101

Janse van Rensburg, J. O., & Coetzee, P. (2016). Internal audit public sector capability: A case study. Journal of Public Affairs, 16(2), 181–191. https://doi.org/10.1002/pa.1574

Lenz, R., & O’Regan, D. J. (2024). The global internal audit standards: Old wine in new bottles? EDPACS, 69(3), 1–28. https://doi.org/10.1080/07366981.2024.2322835

Leung, P. & Cooper, B. J. (2009). Internal audit: An Asia-Pacific profile and the level of compliance with Internal Auditing Standards. Managerial Auditing Journal, 24(9), 861–882. https://doi.org/10.1108/02686900910994809

Mahzan, N., Zulkifli, N., & Umor, S. (2012). Role and authority: An empirical study on internal auditors in Malaysia. Asian Journal of Business and Accounting, 5(2), 69–98.

Marais, M., Burnaby, P. A., Hass, S., Sadler, E., & Fourie, H. (2009). Usage of internal auditing standards and internal auditing activities in South Africa and all respondents. Managerial Auditing Journal, 24(9), 883–898. https://doi.org/10.1108/02686900910994818

Marwa, B. J. (2023). Effect of I-tax Implementation on Revenue Collection in Kenya (Doctoral dissertation, University of Nairobi).

Mattei, G., Grossi, G., & AM, J. G. (2021). Exploring past, present and future trends in public sector auditing research: A literature review. Meditari Accountancy Research, 29(7), 94–134. https://doi.org/10.1108/MEDAR-09-2020-1008

Nipper, M. (2021). The role of audit committee chair tenure: A German perspective. International Journal of Auditing, 25(3), 716–732. https://doi.org/10.1111/ijau.12245

OECD, (2021). Ownership and Governance of State-Owned Enterprises: A Compendium of National Practices. https://www.oecd.org/corporate/Ownership-and-Governance-of-State-Owned-Enterprises-A-Compendium-of-National-Practices-2021.pdf

Osborne, J. W., & Waters, E. (2019). Four assumptions of multiple regression that researchers should always test. Practical Assessment, Research, and Evaluation, 8(1), Article e2. https://doi.org/10.7275/r222-hv23

Poonan, U. U. (2019). The transformation of the South African national parks with special reference to the role of the Social Ecology Directorate 1994-2004 (Doctoral dissertation).

Polizzi, S., Lupo, F., & Testella, S. (2022). Quality assurance and improvement program: Some considerations for central banks. The TQM Journal, 35(8), 2203–2227. https://doi.org/10.1108/TQM-05-2021-0128

Rabie, B., & Goldman, I. (2014). The context of evaluation management. In Evaluation Management in South Africa and Africa, Sun Press. 1–214.

Rashid, A., Salim, B., & Ahmad, H. N. (2021). Internal Audit Effectiveness and Audit 166 Committee Characteristics: Empirical Evidence from Pakistan. iRASD Journal of Management, 3(1), 1–13. https://doi.org/10.52131/jom.2021.0301.0021

Rönkkö, J., Lilja, M., & Oulasvirta, L. (2023). Voluntary adoption of the International Standards on Auditing (ISA) in local government audits: Empirical evidence from Finland. Public Money & Management, 43(3), 277–284. https://doi.org/10.1080/09540962.2022.2131290

Roussy, M. (2022). Engaging in internal audit research in the public sector no less: A Hara‐kiri for your academic career? Canadian Journal of Administrative Sciences/Revue Canadienne des Sciences de l'Administration, 39(3), 347–352. https://doi.org/10.1002/cjas.1661

Sawan, N. (2013). The role of internal audit function in the public sector context in Saudi Arabia. African Journal of Business Management, 7(6), 443–454.

Shaban, O. S., & Barakat, A. I. (2023). Evaluation of internal audit standards as a foundation for carrying out and promoting a wide variety of value-added tasks-evidence from emerging market. Journal of Risk and Financial Management, 16(3), Article e185. https://doi.org/10.3390/jrfm16030185

Shakeel, A., Rasheed, B., Ahmed, M., & Bakhsh, A. (2020). Effectiveness of the role of internal audit function: A perception of external auditors of Pakistan. Paradigms, SI(1), 75–80.

Shuwaili, A. M. J., Hesarzadeh, R., & Bagherpour Velashani, M. A. (2023). Designing an internal audit effectiveness model for public sector: Qualitative and quantitative evidence from a developing country. Journal of Facilities Management, 1(2), 25–60. https://doi.org/10.1108/JFM-07-2022-0077

Stewart, J., & Subramaniam, N. (2010). Internal audit independence and objectivity: Emerging research opportunities. Managerial Auditing Journal, 25(4), 328–360. https://doi.org/10.1108/02686901011034162

Tang, F., Norman, C. S., & Vendrzyk, V. P. (2017). Exploring perceptions of data analytics in the internal audit function. Behaviour & Information Technology, 36(11), 1125–1136. https://doi.org/10.1080/0144929X.2017.1355014

Vadasi, C., Bekiaris, M., & Andrikopoulos, A. (2020). Corporate governance and internal audit: An institutional theory perspective. Corporate Governance: The International Journal of Business in Society, 20(1), 175–190. https://doi.org/10.1108/CG-07-2019-0215

Vallabhaneni, S. R. (2005). Wiley CIA exam review, conducting the internal audit engagement. John Wiley & Sons.

Van Gils, D. (2012). The development of internal auditing within Belgian public entities: A Neo-institutional and new public management perspective [Doctoral Dissertation, Faculty of Social and Political Science, Université Catholique de Louvain].

Wiesel, F., & Modell, S. (2014). From new public management to new public governance? Hybridization and implications for public sector consumerism. Financial Accountability & Management, 30(2), 175–205. https://doi.org/10.1111/faam.12033

Yazid, H., & Wiyantoro, L. S. (2018). The effect of work experience, internal auditor competence, independence to due professional care and implications in internal audit quality. Advanced Science Letters, 24(4), 2565–2568. https://doi.org/10.1166/asl.2018.11006

Yusof, N. A. Z. M., Haron, H., Ismail, I., & Chambers (2018), A. Internal audit capability levels in Malaysian public sector organizations: The perceived role of management support and cooperation with external auditors. Journal of Governance and Integrity, 1(2), 25–60.

Zaman, M., & Sarens, G. (2013). Informal interactions between audit committees and internal audit functions: Exploratory evidence and directions for future research. Managerial Auditing Journal, 28(6), 495–515. https://doi.org/10.1108/02686901311329892

Published

How to Cite

Issue

Section

License

Copyright (c) 2024 Zahid Qadeer, Sammar Abbas, Tanveer Ahmed

This work is licensed under a Creative Commons Attribution 4.0 International License.

Authors retain copyright and grant the journal right of first publication with the work simultaneously licensed under a Creative Commons Attribution (CC-BY) 4.0 License that allows others to share the work with an acknowledgement of the work’s authorship and initial publication in this journal.